So what is the harm by company executives to give a transparent info about CEO? What is point of hiding and beating around the bush!

Have an investment too around 4% of portfolio.

So what is the harm by company executives to give a transparent info about CEO? What is point of hiding and beating around the bush!

Have an investment too around 4% of portfolio.

Disclosure : Invested from 240Rs till 100 Rs

Parag milk foods : I saw company is struggling to make inroads into market share.

Premium value segment is not growing as fast as expected.

But i feel, we need to give time to the company as 25+ years in same industry will definitely has some advantages. That also means company has power to bounce back from difficulties.

I read SWOT: Parag

My interpretation is that the company is bit more diversified and could not focus on one segment fully.

is is the case of misallocation of capital?

or is it internal management vision struggle?

i am not able to judge that as of now

I would wait for these quarter results atleast to exit or make fresh purchase into shares

Hi everyone,

I have a small position in Parag Milk Products. I have read all the comments in this thread and they can be classified under the following k categories:

My own overall reading is that:

Overall, I found this company to be quite cheap relative to their quality and growth prospects. I added about 6% of direct stock portfolio at 60 rupees buying price. Will add more if the stock falls due to a second coronavirus market crash (although I don’t expect it to breach 50 rupees price again).

would suggest you go over the last few quarterly earnings concalls to understand the negativity around this stock before taking a bolder allocation.Best of luck

Until last quarter result I owned Parag milk food. After listen to last quarter con cal . I book my lose. I don’t happy with management commentary.

Dis. Not holding any position

Hi Sahil

Some additional thoughts for your consideration. Disclosure: I have now a significant holding (as per my portfolio) but have some red flags that I am monitoring very closely. First all the good news

a. From a market growth perspective there is significant potential (unorganised to organised, coop to private, consumption habits to value added, etc). @dineshssairam shared some valuable data sources you could review if you are interested

b. From a market structure perspective, it is very fragmented. Even Amul (which is a goliath in this market is potentially ~10% of the total market). In balance I would say this is a good thing because it is a growing market and private players (with strong regional presence - Hatsun, Heritage) can add market share if they execute well. Milk procurement is both a challenge as well as a moat once you have it

c. Company strategy and financials: They have been innovative (as have other private dairy players) in their approach - they pushed the concept of cow’s milk rather than buffalo, new business models like Pride of Cows subscription, investment in cheese as a category and now 2nd in the market, new categories like Avvatar whey (which is a by product of cheese),etc. As a result their share of value added products to liquid milk is one of the highest in the market - which I think is better for an ‘FMCG-like’ player and generally reflects in higher margins compared to others. The growth in the last few quarters has slowed because of shortage of milk and the market seems to have been disappointed that growth will not pick up until the next flush - which will be from Sep onwards. Of course the business has some covid protection due to being essential so should be ok even during these trying times. Single digit PE ratio at this point seems undervalued given the expected profit growth and ROCE of 15-20%

d. From a promoter perspective, there has been a overhang on the promoter pledge shares and there is now a commitment from the management to reduce the pledge to zero (90 days from March 02 2020). They had a total outstanding of Rs 33 crores on March 02 which is down to Rs 10 crores as of now. Not long to go for 90 days - could be a short term trigger either ways. I also like the fact that the promoter’s daughter has a senior role in the business having worked her way through. This could cut both ways - but for me it is an indication of the promoter trying to build something more permanent to pass on to the next generation

Now for the flags or the bad news

a. Their product and brand strategy worked well as they were growing (more of a shotgun approach) but they need to be concentrating their firepower now (look at Amul - they are spending like crazy in this downturn). Specifically, Go and Gowardhan make sense as brands with their portfolios. Perhaps even Pride of Cows as a premium brand. But then why launch another premium ghee brand called Aurum (which I think they have withdrawn) - and not under Pride of Cows (see https://www.whytefarms.com/ ). Is Topp Up necessary as another brand? If they want to be an FMCG company they need to build brands (along with distribution). To do this they need a more coherent branding strategy - it feels like they are focused on innovation and while that is a good thing, they need consolidation for growth as well. Pride of Cows current offering is difficult to scale (they own they dairy farm) and yet they decided to start selling this in Singapore some time back? This seems more opportunistic than brand oriented. Thankfully they have pulled back from this

b. Professionalizing the management. They have now made two efforts at this. In Jun 2018 they brought in a new CFO, COO, Sales etc. Most if not have all left in a year or so. They then got in a new CEO - who said all the right things (at least from my perspective) and after not attending the last call due to medical reasons now has his linkedin profile saying he is on a sabbatical. He may very well be unwell but a request for clarification to their investor relations brought no response.

c. Update on key initiatives. There are two key initiatives they have been talking about - Vector Consulting in Mumbai using theory of constraints to improve their distribution systems. Results are now overdue by a quarter (they keep saying next quarter). The acquisition of the Danone plant and how that is doing in the NCR region - milk procurement, products, sales. I think they last updated a few quarters ago indicating approx Rs 7 crores / month exit in Q419. Need to see whether they have been able to make this work - else they will remain a regional player with others attacking them

In conclusion, for me the company looks very interesting in terms of innovation, portfolio and market opportunity. But if I keep seeing red flags on scaling up the business to the next level, it could be a sign to exit. Wish you the best

The CEO has resigned due to personal reasons (he was anyway on sabbatical since april). This development has made me reexamine the wisdom of investing in this company and I’m planning to reduce my stake by 50% over next few days.

Mr. Venkat Shankar from Britania joined Parag Milk Foods as CEO on 4th July 2019. It is not good to see CEO leaving the organization in such a short span.

Some red flags highlighted here

Disclosure: Not invested.

The company is still in growth phase. The revenue keeps increasing at 15%. The major competitor is the unorganized market and the unorganized to organized shift is a big trigger in terms of future growth.

The promoter is a veteran and is in the dairy industry for over 20 years. The company has very limited debt and they have been considerably reducing the debt. The promoter’s children have joined the business (which just shows that they are in it for the long haul). Yes, they have had problems with the professionals they hired, but i honestly believe that they are not ready for professionals yet. The company has to keep experimenting and working on ground-breaking products (like whey protein in the long run).

Their Operating cash has almost been equal to net profit in the past 5 years. They have been getting subsidies and are in an industry that is generally considered “positive” for society.

Another point is that their net profit margin has been steadily increasing every year (except for this year because of exceptionally high procurement costs). This is because of the focus on value added products and good branding.

The promoters have released quite a significant portion of the pledged shares in the past few months. Good sign. The company seems to have all the right ingredients to become an FMCG bigwig (except recurring management changes/resignations - hope that’s resolved soon). The product line is also quite diverse (cheese, butter, curd, paneer, yoghurt, whey powder and traditional desert mixes)….& most of their products are really good (been trying them out). Since value added products contribute over 67% to revenues (followed by liquid milk - 18.5% & skimmed milk powder - 12.3%), the company should be able to maintain a healthy growth trajectory (consumption of branded processed milk products is on the rise). The only major risk (other than the management changes) seems to be that the margins are vulnerable to milk procurement prices. Hope they’re able to get around that problem.

Disc: Invested recently

Screener currently shows 24% pledged shares and 0.24% debt to equity. Does this still mean 0.24% debt or we need to also account for 24% pledged shares? Can anyone clarify?

Long time ago, I had a tracking position in Parag. I sold off because Q on Q results were very unpredictable. Now I see this company at sub 10 PE. Then also it used to be cheap at say 20-25 PE. but at sub 10 PE looks strange. A company with such known food products like Go, Gowardhan etc. so cheap …somehow I trust the Market more than my own skills so I feel I am missing something here, rather than being smart in getting a branded foods business cheap…the only issue is I am so far not able to find what am I missing and why this only gets cheaper? if anyone can share thought would be great. Thanks

Yesterday, I was speaking with a portfolio manager of a PMS who used to own this name till some time back. We happened to discuss this stock as well, in which he expressed his disapproval and disappointment over the company’s decision to stop hosting post-result conference calls, for the 2nd quarter in a row. Irrespective of the actual reasons for such a decision, companies should never take such sporadic decisions. Investor communication, ideally, should be a consistent exercise without any correlation to the stock price. I vividly recollect having attended one of their analyst meets which was held in a grand manner, while everything was seemingly ok in the stock. With the price coming down and the profits under pressure, companies need to realise that keeping the communication channel open to investors is of paramount importance. By not addressing investors during such times, companies leave them in the dark thereby letting them form their own perceptions, which will be detrimental for the company from a long term perspective. While most of the promoters are aware of this, but sadly very few promoters appreciate and follow it.

what made it go up by 15% today, I cannot find any news, promoters released the pledged shares?

Disc. Invested

Apparently, Radhakishan Damani, Akash Bhanshali, Mukul Agarwal are in the shareholders list. Darshan Mehta of ex-ET tweeted about it.

The apprehension over corporate governance issues must’ve been the reason in this case. Regardless, quite a few superstar investors like RK Damani, Madhu Kela, Akash Bhansali seems to have taken stake in the company taking the benefit of the dirt cheap valuation.

Few updates in order to revive this thread.

ICRA Ratings downgraded to [ICRA] A/Negative/A2+

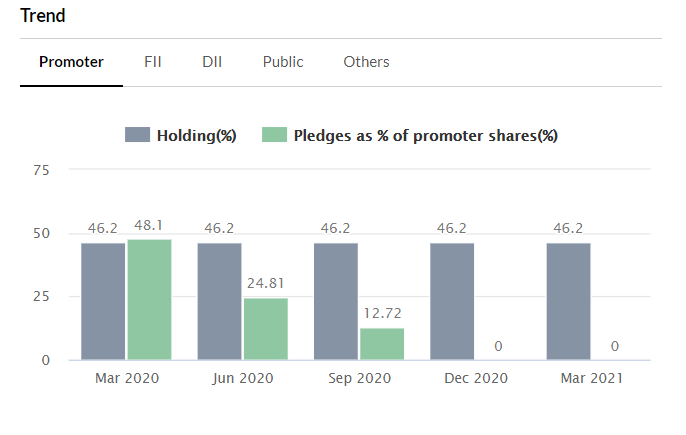

Pledge has come down gradually since March quarter (48%) to Jun (25%) to Sep (13%).

Disc: Exited at 190. Evaluating now. Regular consumer of their Cheese & Paneer. Impressed with the quality. Nowadays I find their product discounted aggressively compared to Amul’s (at least 5% less) in Grofers / Bigbasket.

All pledge has been released according to Dec quarter shareholding.

has anyone gone through parag milk EGM agenda, a quick glance shows that they are offering shares at 111/- to private investors, so will this be the floor for the stock price in the near term ?

Some interesting stuff happening here. Not sure what it will lead to. In addition to promoters releasing all pledges last year between Mar and Dec. To put it in perspective, the promoters held 46.2% in which 48.1% was pledged (1.84 Cr shares) as of Mar 2020. Pledge release came at a time when the business was performing its worst.

Then all this dilution and fund raising bringing in a fair bit of cash (205 Cr right away and 111 Cr when promoters convert).

4.27% to Sixth Sense

Sixth Sense II - 18 lakh shares at 111 (20 Cr)

Sixth Sense III - 27 lakh shares at 111 (30 Cr)

6.41% to IFC

IFC - 67.56 lakh shares at 111/s (75 Cr)

FCCB to IFC

IFC - $10.68 million (80 Cr) convertible at Rs.145/share

Terms of FCCBs show that interest rates to be paid are tied to share price (Above 200/s Nil)

Promoters

Devendra Shah - 50 lakh warrants at 111 (55 Cr)

Netra Shah - 50 lakh warrants at 111 (55 Cr)

This is some big dilution and big money coming into what looks like a distressed business. But promoters appear to be showing a lot of faith in releasing all pledges (and also subscribing to the warrants, though it favors them).

Am not sure what the plan for the cash is, considering the Danone plant they acquired itself doesn’t appear to be contributing much. Maybe they will use this to reduce debt? That itself could do wonders to the B/S and P/L as currently they have 400 Cr debt and interest outgo itself is 43 Cr/year on it. Valuation has been cheap and the market appears to be pricing in doom here while some savvy guys seem to be betting not.

Disc: Have positions around 140 levels

Hi Phreak

Indeed - the pledged shares were initially the big trigger for the exit of a large investor (Government Pension Fund Global - I think this is the Norwegian sovereign fund) sometime after Dec 2019 leading to a big drop in prices. The promoter claimed it was to raise funds to acquire more shares. Subsequently the promoter issued a statement to the exchanges indicating they will remove the pledge and gave a date as well but were unable to achieve their targeted date due to covid. To their credit, they kept at it and the graph you show above indicates their efforts to remove all pledges

In discussion with their investor relations they have indicated a plan to reduce debt by INR 65 cr in FY22 - so part of the new funds will go there. The rest is apparently for capacity expansion over the next two years as they prepare for a new growth phase.

I would like to highlight a couple of risks that I see and have not been able to satisfactorily get to the bottom of

a. Overall revenues are down due to reduction in HORECA revenues (which is about 15%) and de-emphasizing liquid milk. These are both acceptable strategic moves

b. However, the management seems to indicate that revenues in value added (paneer, cheese, ghee) for domestic continue to grow - but I was not able to make this calculation. You may be aware that their distribution was reliant on modern retail and ecommerce plays a negligible role - both took a hit during covid and are yet to get back to full normalcy

c. They have further gone into lactose - a B2B product and a by product of cheese production - which they claim is another niche imported product (like avataar whey protein). This still remains to be proven

d. The Danone plant is at least a year behind in terms of reaching targeted revenues - although seems to be growing steadily

e. I think Pride of Cows looks to be an interesting position in the market - although the story still has to play out (you may have tracked the sub brands into ghee and dahi)

I continue to have faith in the promoters and business - and their innovation - but am tracking this very closely to keep checking for any red flags.

Disc: Also invested with a reasonable position size