Paradeep Phosphates:

Background:

Paradeep Phosphates Ltd. (PPL) is a recently listed fertilizer company. PPL is the second largest private sector manufacturer of non-urea fertilizers in India and the second largest private sector manufacturer in terms of Diammonium Phosphate (DAP).

PPL was incorporated in 1981 and Zuari Maroc Phosphates Private Limited (“ZMPPL”), a joint venture of Zuari Agro Chemicals Limited (“ZACL”) and OCP Group S.A. (“OCP”), currently holds 80.45% of the equity share capital of the Company, with the balance being held by the Government of India. The GoI completed its exit during the IPO

IPO Objectives:

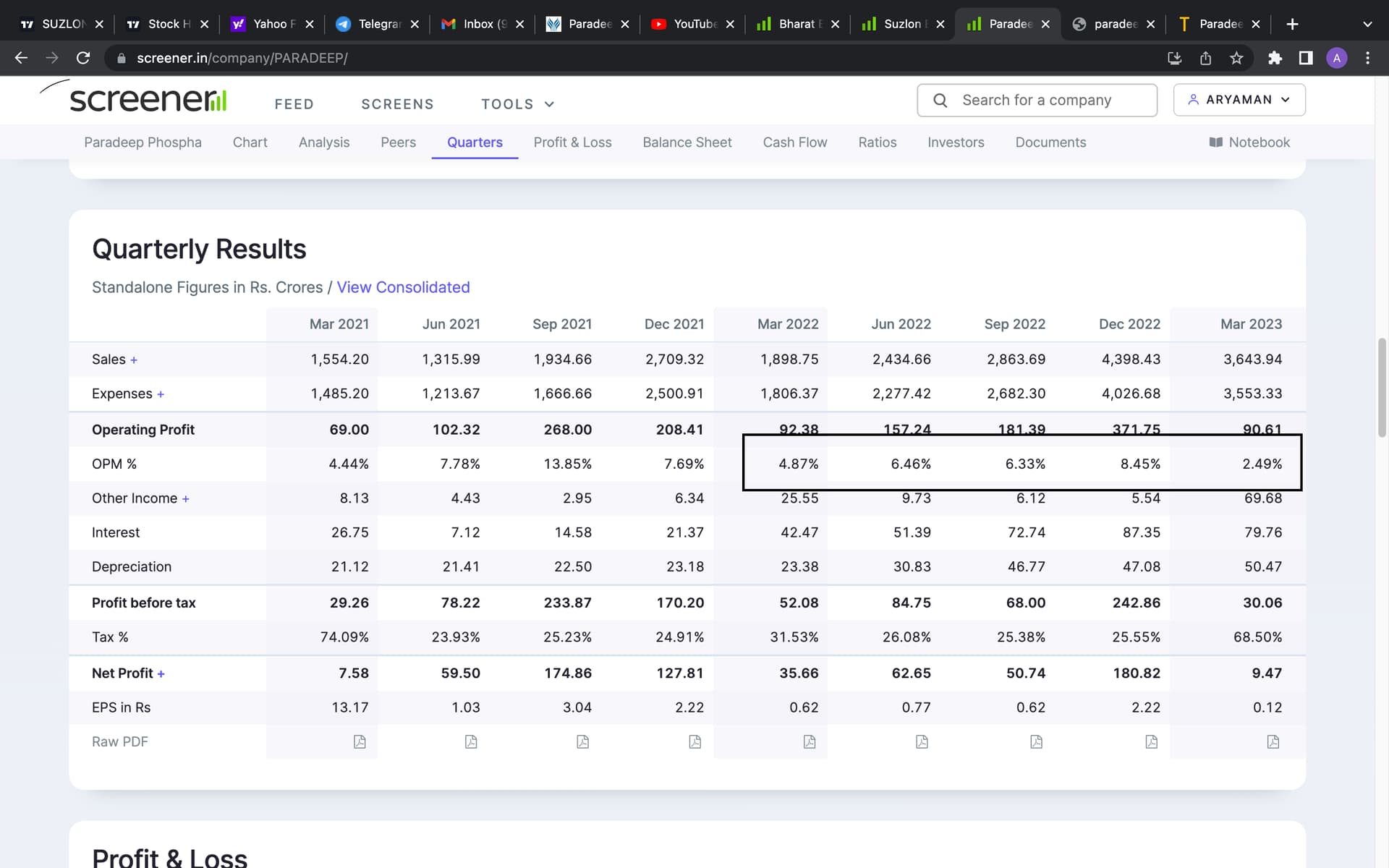

The main objective for the IPO was the part financing of acquisition of a manufacturing facility in Goa. PPL entered into an agreement to purchase a fertilizer plant from Zuari Agro in Goa for a consideration of ~INR 2000 cr. This was done with the view of expanding the product portfolio and also expanding in high demand markets of Maharashtra and Karnataka. Post-acquisition the company’s capacity will increase by 1.2 million MT comprising DAP and NPK granulation capacity of 0.80MT and Urea capacity of 0.4 MT.

Products & Distribution:

PPL is primarily engaged in manufacturing, distribution, trading and sales of complex fertilizers such as DAP, three grades of NPK (NPK-10, NPK-12 and NP-20), MOP, Zypmite, and its by-product, Phospho-gypsum. It also distributes Ammonia and Sulphuric acid for industrial consumption in and around Odisha. It has an extensive sales and distribution network, with a strong presence in the eastern part of India. It distributes its products across 14 states in India through its network of 11 regional marketing offices and 468 stock points as of March 31, 2022. Its network includes 4,761 dealers and over 67,150 retailers.

Raw Material sourcing:

Efficient manufacturing of fertilizers is heavily dependant of access to reliable and cost-effective raw materials. PPL’s raw material include Phosphate Rock, Phosphoric acid, Ammonia, Sulphur and MOP. PPL derives its rock phosphate through long term contracts with its parent OCP (one of the world’s largest rock phosphate producers). It produces some of its Phosphoric acid and Sulphuric acid requirements, with the other raw materials being sourced from suppliers. The company is also backward integrated in Phosphoric acid and Sulphuric acid.

Some strategic advantages of the above are:

- Reduction of raw material costs and logistics costs as it produces Phosphoric acid

- Ability to fully utilize the by-products and waste products generated from manufacturing process

- Ability to store and sell excess Ammonia and Sulphuric acid to maximize efficiency of its production plants and enhance revenue and profitability

- Reduction of reliance on external suppliers for Phosphoric acid, thereby helping to maintain a steady production of DAP and NPK, and limiting exposure to price volatility

- Ability to manufacture more products, including different products with weak Phosphoric acid and strong Phosphoric acid across the production chain

Manufacturing:

PPL’s manufacturing facility is strategically located near the Paradeep port, where it owns a captive berth with 14 meters draft with facilities to unload solid and liquid cargo. It has capacity to store up to 120,000 MT, 65,000 MT, 55,000 MT and 35,000 MT of Phosphate Rock, Phosphoric acid, Sulphur and MOP, respectively. It also has an Ammonia storage facility of approximately 40,000 MT. The ability to store raw materials at its facility enables it to withstand disruptions in supply as well as volatility in the price of raw materials for a short duration.

Financials:

| Revenues (mil) | EBITDA | Net Profit | EBITDA Margin | PAT Margin | Net Worth | RoNW | EPS | |

|---|---|---|---|---|---|---|---|---|

| FY18 | ₹ 37,965.70 | ₹ 4,445.70 | ₹ 1,505.80 | 11.7% | 4.0% | ₹ 13,954.40 | 10.8% | |

| FY19 | ₹ 43,972.10 | ₹ 4,808.40 | ₹ 1,589.60 | 10.9% | 3.6% | ₹ 14,827.10 | 10.7% | ₹ 3.60 |

| FY20 | ₹ 42,277.80 | ₹ 4,946.40 | ₹ 1,932.20 | 11.7% | 4.6% | ₹ 16,035.30 | 12.0% | ₹ 4.60 |

| FY21 | ₹ 51,839.40 | ₹ 5,614.50 | ₹ 2,232.70 | 10.8% | 4.3% | ₹ 18,275.10 | 12.2% | ₹ 4.30 |

| FY22 | ₹ 78,979.90 | ₹ 7,100.00 | ₹ 3,984.50 | 9.0% | 5.0% | ₹ 21,887.90 | 18.2% | ₹ 6.92 |

| 15.8% | 9.8% | 21.5% | 14.0% |

With the acquisition of the Goa facility now complete, the total capacity of PPL is ~3 million MT. Based on this the current year’s financial projections would be as follows:

- Capacity: 3000000

- EBITDA/ton as per guidance: 4800 (as per Q1FY’23current concall)

- EBITDA: INR 1500cr

- PAT: INR 750cr

- Est EPS: 9.21

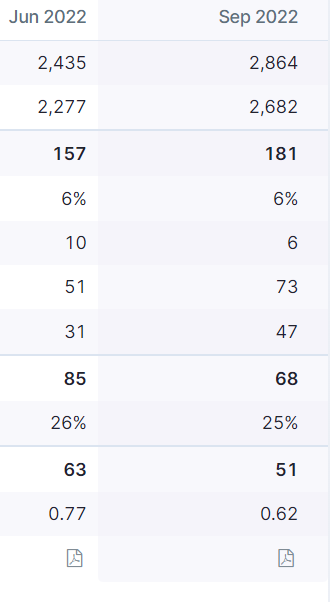

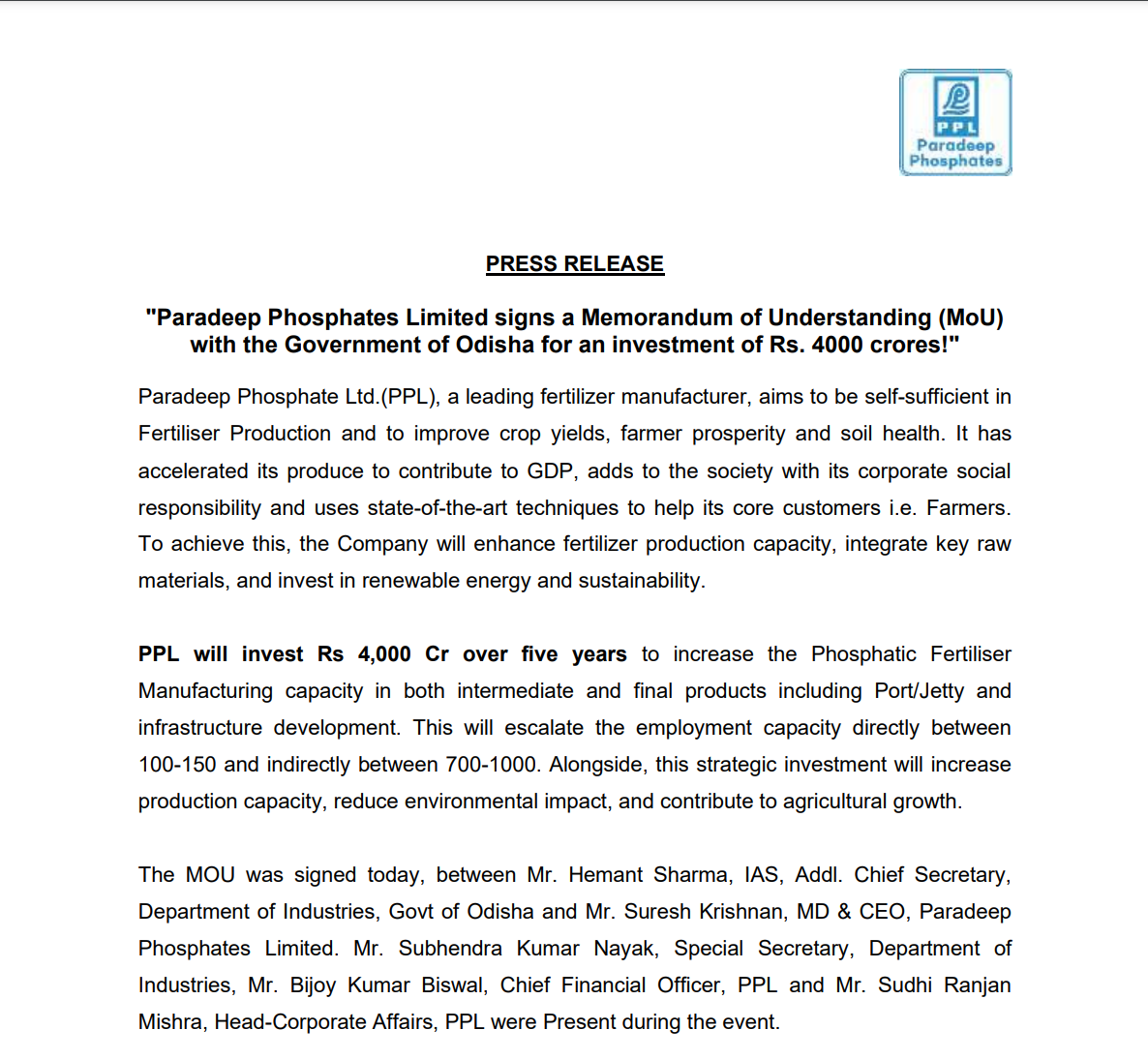

Highlights on Q3FY’23 Concall:

- Strong demand environment. Govt. clearing subsidy on time

- Received 1000cr subsidy from govt. 1000cr is balance

- Phosphoric acid plant meets 90-95% of internal capacity at Paradeep plant

- All 4 granulation trains to be active by October 2022

- Q1 EBITDA/ton was 4853 vs 4600 last fiscal

- Gross debt at 3627 cr. Net debt at 3427 cr. Cash on books 200cr

- Guidance for long term debt of less than 1000cr

- Goa plant will produce NPK. Will benefit from OCP relationship

- Focus on current and next fiscal is to drive capacity utilization and FCF generation

Risks:

a. Any change in Government policies towards the agriculture sector or a reduction in subsidies provided to farmers could adversely affect the business.

b. Risk that working capital might increase if the govt. doesn’t clear subsidy in time

c. Concentration risk to revenues since most of the topline is derived from eastern states

d. Imports of raw material exposes it to forex risk

D: Invested. Bullish