Can get earphone for 150rs in roadside. Making Brand promotion will position them amongst leading Brand. Getting even a low single digit market share from unorganised market will do wonders in the revenue side. But competing with cheap china products and winning will prove.

1 Like

https://www.instagram.com/p/Ckh5i_hsTYe/

They have sold a Million products in October-2022.

Even if we take the average price to be 350, then the October Sales could be 35 crores.

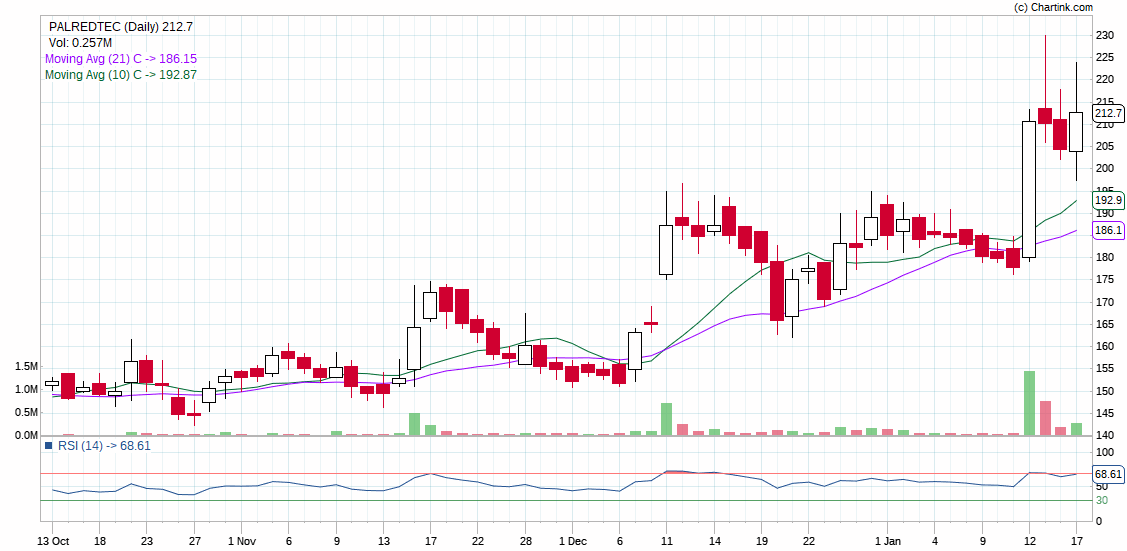

The stock hasn’t gone anywhere in the past 6 months or so. But seems like the Mathey Cyriac factor has started to show in the Sales.

The real game will happen will it will show in the bottomline.

4 Likes

Hi Folks,

I think the single biggest thesis factor for investing in Palred is big stake (>20%) taken by Mathew. He is well known turnaround specialist with some highly successful companies (gokaldas, MTAR Tech).

Palred also has started to increase the price point of their products from mid 100s to mid 1000s which should help them in acheiving faster growth and potentially higher margins. Company is now at an interesting juncture and valuations also seem to be reasonable.

Would be interesting to see how the next 1-2 years pan out for the company

1 Like

Very poor set of numbers by Palred. Sales are same yoy and declined sharply qoq. Company is back to posting loses. All this even after higher marketing and visibility efforts.

Market has rightly put the stock in LC today.

Anyone tracking the company or in touch with management and get some insights on their plans?

cons : Its in a rapidly changing Industry. With cheap ear pods available in nook and corner of the street. At one extreme Apple pods positioned itself for highly premium segment. What unique one can find in Ptron?

pros : Mathew investing. A small % share from bottom of the pyramid can have huge impact in Turnaround.

FY2022-23 AGM Notes:

competition is very intense.

11-12% promotional and marketing expenditure as percentage of sales

Promotional expenses:

Pooja Hegde as brand ambassador

meta-ads and google search ads.

promotion in offline stores ( Vijay sales, Croma, Reliance)

focus on make in India product.

in house manufacturing

no comments on Mathew c as a board member

online is 80% business.

sold 40 lacs Pisces during the years.

Right of use assets includes (2 manufacturing Wearhouse in Hyderabad)

Average revenue per product around 375

180000 Pieces one shift manufacturing capacity

Target is to double the manpower will increase manufacturing capacity.

currently we import PCBs, in future target is to be manufacturing in local.

Material cost was 50% as percentage of sales befor 2021 becouses of B2C business model

Currently material cost is arround 70% becouse change in business model from B2C to B2B

1 Like

1 Like

Any idea why the share is suddenly hitting back to back circuits ? any leaks ? looks like some news might come