Palred looks like to an interesting story to track. Here is what I like about the company:

(1) pTron has created a very decent niche brand in low cost mobile accessories. The products have quite a lot of traction on e-cormmerce platforms like Amazon. Product prices are almost 40-50% lower than other similar brands like boat and noise. Ratings are okay. Here is a tech radar article which mentions pTron as the lowest cost brand in the market:

(2) They are constantly trying to expand their product portfolio. Recently launched smart watches at a Rs 899 price point! If we go by their success in the earphones market, they should have a decent market share in the low cost smart watches segment too.

(3) Company is targeting 60L-80L annual product sales in the next 2-3 years. Even with Rs 500 ticket size that translates into Revenues of Rs 300-400cr. Current sales is just Rs 100cr!

(4) They are starting a few assembly lines and manufacturing some parts in india. Being a distribution brand is a very low margin business especially on e-commerce platforms. Therefore if they can do some part of the work in-house it can lead to a very good margin increase. Hence, this seems like a step in the right direction.

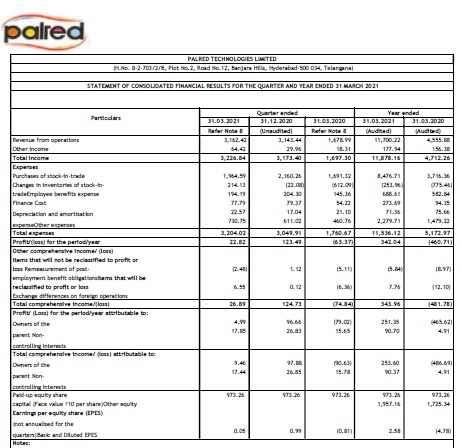

(5) Doing a quick back of the envelope calculation: Current PAT is just Rs 2cr! Assuming they reach Rs 400-500cr sales with in-house assembly and bigger scale (hence better deals from Chinese manufacturers) and hence manage net margins of 5-7%, the PAT can go upto ₹25-35cr. Current market cap is just Rs 140cr.

Things which I don’t like about the company i.e. points which need further research:

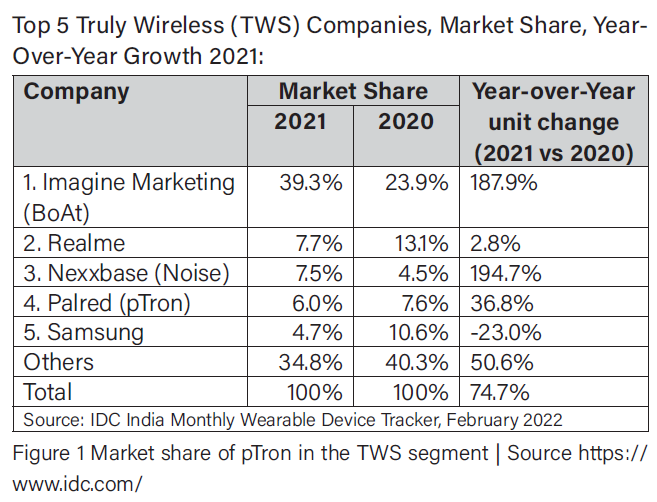

(1) Smartphone accessories is a hyper competitive market. There are players like boat, noise and Boult plus all the mobile phone brands which have started coming out with their own accessories.

(2) If we do a quick google search most articles on best earphones don’t mention pTron in their lists. The only article which I found has been shared above in the positive points. Are they really able to deliver good quality?

(2) They don’t have any sustainable competitive advantage.

(3) In a business like this, since they don’t manufacture in-house, other factors like Brand, design, digital marketing and technology become really important. A quick look at their linkedin page, the team lacks quality in all these departments compared to players like Boat and Noise. How will they compete remains to seen!

(4) Management has an insider trading case and a few other issues which have been highlighted in the past. This puts a question mark on the ethics of the team.

These are my inputs on the business. It will be great if more valuepickrs get involved to study this company further.

Disclosure: Not invested. Tracking with interest.