Concall excerpts Q2FY21

Sunder Genomal, MD:

-

We have had a heartwarming experience since the economy has opened up

-

We have continued to add distributors and opened new EBOs despite a tough environment

-

October was the turnaround month, November is double-digit. We expect to continue with the double-digit growth in Q3

-

Revenue target of $1bn in 5-years remain intact

-

Investments into Salesforce, ARS, separate MIS for analytics, re-engineering

Vedji Ticku, CEO:

-

160% revenue growth from the previous quarter, volumes down 13% YOY

-

95% MBOs are fully functional, all the EBOs are opened

-

60 new EBOs have been opened in the last quarter. Total number of EBOs should be 810+

-

Greater demand in e-commerce and Athleisure

-

Digital marketing is the new area of focus for us

-

We are Present in 2870 cities+ now

Chandrasekhar, CFO:

-

PAT margin of 15% (best in 3-years), implemented through tight opex control

-

Gross margins are back to 40%, the EBITDA margin is at 22%

-

The net working capital is 536 million

Q&A:

Bhargav Buddhadev - Kotak

Q) Is it possible to share the trend in secondary sales?

- It’s one of the best in recent the quarters

Q) Any supply constraints?

-

Yes, in the earlier quarters

-

Whatever revenues we have lost cannot be recovered

Q) Yarn prices up 12% in a month, any price hike?

-

this is the prices of the old crop, new crop comes in December/Jan and the prices will be back to normal

-

We touch 8000 stores in Juniors, 15 EBOs for Juniors

Aaditya Soman - Goldman

Q) Guidance for Q4 is 100% but why not for Q3. Supply constraints leading to revenue loss, how much was it?

- Management didn’t specify how much revenue was lost but touched on the trend and didn’t comment on the specific question

Q) Is it because of the pent-up demand we are seeing growth?

- Sales are on a rising trajectory from August, it’s not a pent-up demand

Q) 13.5% volume decline but 4% revenue decline, what was the mix like?

- Athleisure is in good shape, didn’t specify the split, double-digit MOM growth seen for Athleisure

Nihal Jham - Edelweiss

Q) Comment on the cost-saving initiatives?

- We spent less on ads and marketing, the overall reduction of 45 crores

Q) The expansion was 60EBOs but how many MBOs and what’s the plan for MBO expansion?

- We push the count at an average of 10% every year

Arnab Mitra - Credit Suisse

Q) E-commerce - what’s the current traction like; and will it continue post lockdown?

- E-commerce has been the silver lining this year, there was a struggle in the previous quarter from our end in terms of supply, we worked on improving our infra which took 30-45 days, average demand is ~2x compared to earlier years

Q) Margins are at 22%, will the opex come back to previous levels once the ad spends and other operating costs?

- There’ll be an increase in ad spends and digital transformation but margins will sustain

Avi Mehta - Macquarie

Q) Is urban which contributes to 60% revenue in the top cities still under pressure?

- Most of the metros are back expect Mumbai. This is no longer a headwind

Q) Provision of slow-moving inventory in Q1, is it written out now?

- it still continues

, as we move into Q3 and Q4 they’ll be sold

, as we move into Q3 and Q4 they’ll be sold

Q) Any price increase taken? Other income down?

-

subsides are low this year and hence lower other income

-

There wasn’t a significant price increase, we thought that there were a few products were priced way below the minimum price and hence we adjusted the prices

Sameer Gupta

Q) Double-digit growth in September? Is it also because of people spending more people at home, will this revert when we revert back to normal?

- We cannot have only Athleisure growing for the overall co to grow at double-digits, Innerwear has also grown well. We don’t think the demand will be subdued post people going back to work.

Q) People will see the quality of the product and the value for money

Gross margins are up, is it because of writing down the 110 crore inventory in the last quarter?

-

no, that’s due to the improvement in this quarter

-

3% improvement in raw materials, we didn’t buy in Q1, 1.5% increase in Q2

Mihir - Edelweiss

Q) Will we see double-digit growth in Q3?

- Trajectory from August is good and improving every month, we hope it’ll be much better. Didn’t specify if they would see double-digit growth in Q3

Bharat Shah - ASK

Q) Not a question for this quarter, it’s a broader question. We’re invested in Page for the past 10-years and growth has been smooth & easy except for the last few quarters. There has been a significant improvement in technology initiatives, design capabilities, product placement etc… Have we crossed the hump and can we see the Page of the old in terms of growth? Discipline is good, no easy credit is given. I’m really delighted. Discipline in cash flow and working capital improvements. Will the difficult phases be behind in 5-years?

- You’ve been a shareholder for a long time and we thank you for that

. Yes, we believe we’ll be back in terms of growth. We’ve come a long way, new interventions put together, achieving a revenue of $1bn in 4-5 years is our target. We’re ready to take the big leap (the exact same statement was heard in the last quarter and it was Bharat Shah who had asked the question)

. Yes, we believe we’ll be back in terms of growth. We’ve come a long way, new interventions put together, achieving a revenue of $1bn in 4-5 years is our target. We’re ready to take the big leap (the exact same statement was heard in the last quarter and it was Bharat Shah who had asked the question)

Q) I’m not concerned about the pandemic, does the long term growth remains intact?

Yes, we strongly believe so

Akhil Parikh - Illara capital

(Call got disconnected, missed the next 5 minutes)

Sunder Genomal was trying to clear the air on the human rights violation issue: We never stop to invest into ourselves to outperform. 1bn revenue isn’t a big ask compared to the market potential we’re in. Our essence remains the same, strategies will be improvised. The fundamentals are very strong in the backend. We have 15 manufacturing and warehousing locations with 17000 workers, Norway allegations were made in 2018 by a handful for disgruntled employees in the Bengaluru plant (1000+ people). We explained point by point to the council. As per their policy, for reassessment, they’ll do it at the earliest possible time (middle of next year). All those allegations are false, the truth will prevail.

Raj Motiwala

Q) Can you specify the break-up of the revenue across segments?

- We used to give this earlier, we’ve stopped in the last 10 quarters.

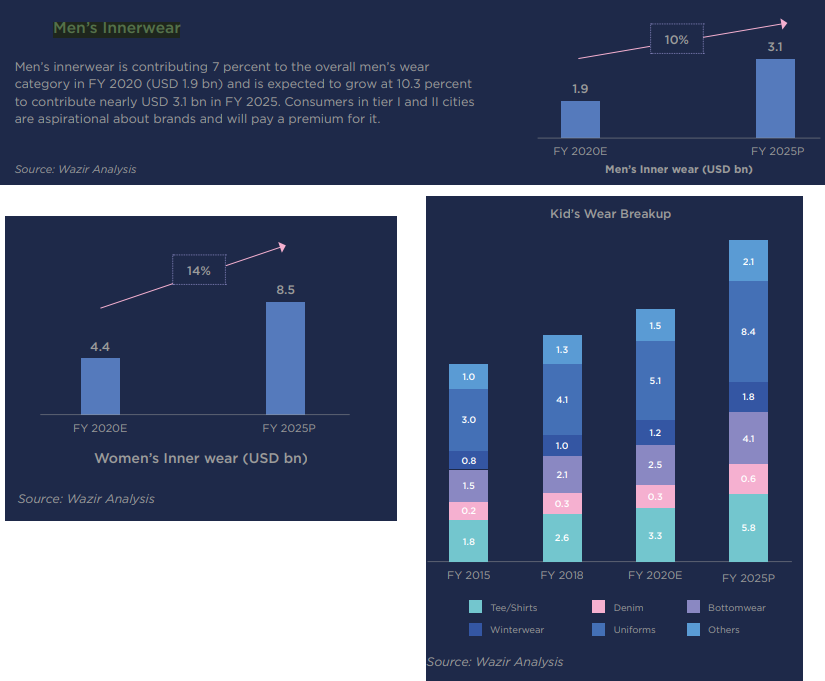

Q) Have you found a formula to open the women innerwear market after seeing sales data through eCommerce players?

- Our penetration levels are low in women’s innerwear (5%) compared to men’s (20%) and it’s a bigger market then the men’s innerwear market. We have major plans for the women’s segment in the near future

Q) New product launches look impressive, is the larger focus on Athleisure?

- Athleisure is the second largest in terms of overall revenue. The market is growing fast with the into of gym wear etc

Ankit Kedia - Philip Capital

Q) Digital transformation, how will it help at the backend? Deadline for JBA (for billing) is by December, DHL on logistics……

-

We want a seamless supply chain. We want to know what we need to sell and it should be available at the right time.

-

JBA will collate info on the demand pool and feed it to SAP. DMS - distribution management software, we have a clear vision on understanding what the stock is at the distribution end. ARS helps in creating automatic ordesr from the distributor when the inventory is lowering up, FSA is for tertiary demand. We want zero sales loss, the customer gets the best service through MBO, EBO

Q) What will be the capex for the $1bn revenue plan, will the Ananthpur facility be ready in Q4?

-

Orissa plan will be first, it’s a large facility. Ananthpur is next in the line

-

This year, we haven’t planned any capex, 73 crores (this year so far). FY22 Capex not planned yet. The expectation of all capex put together will be 200 crores (in 4-5 years?)

-

Orissa plant: We don’t want to put all eggs in one basket. This is done for a risk management point of view since most of our plants are in Karnataka

Q) Total retail reach in women’s (store wise)

- 45% out of the total number of stores