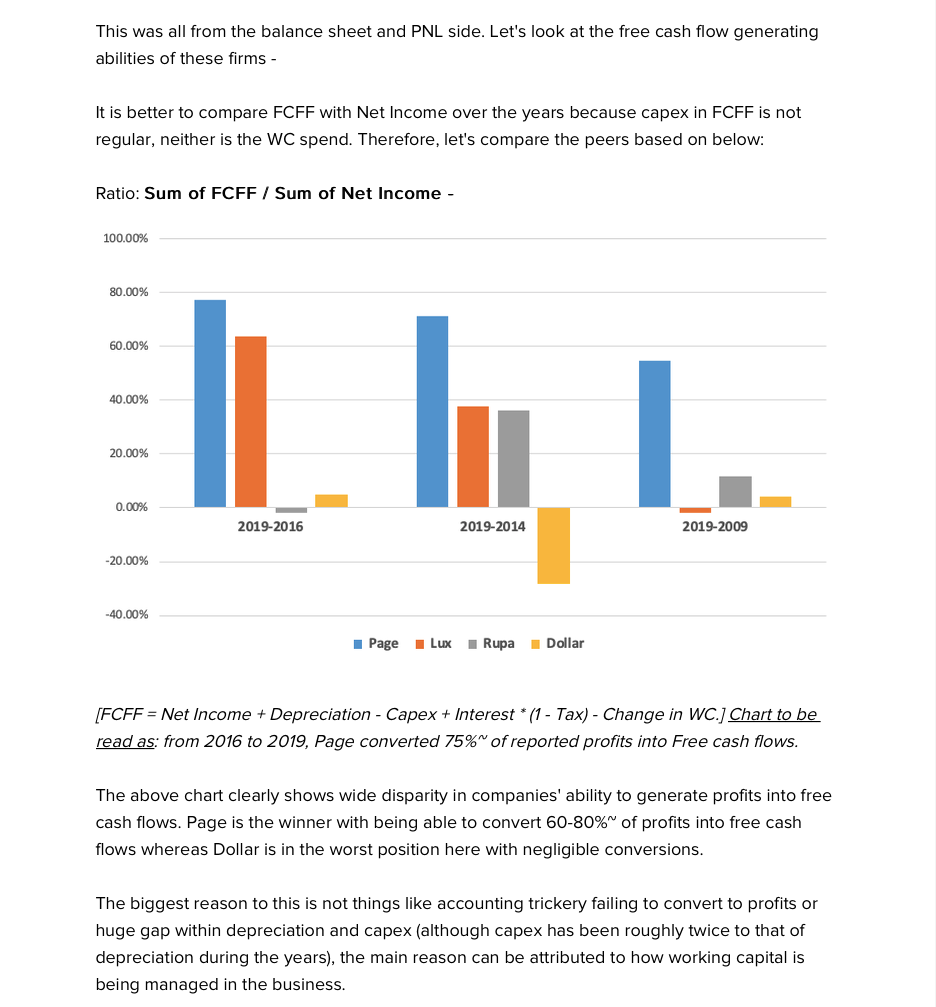

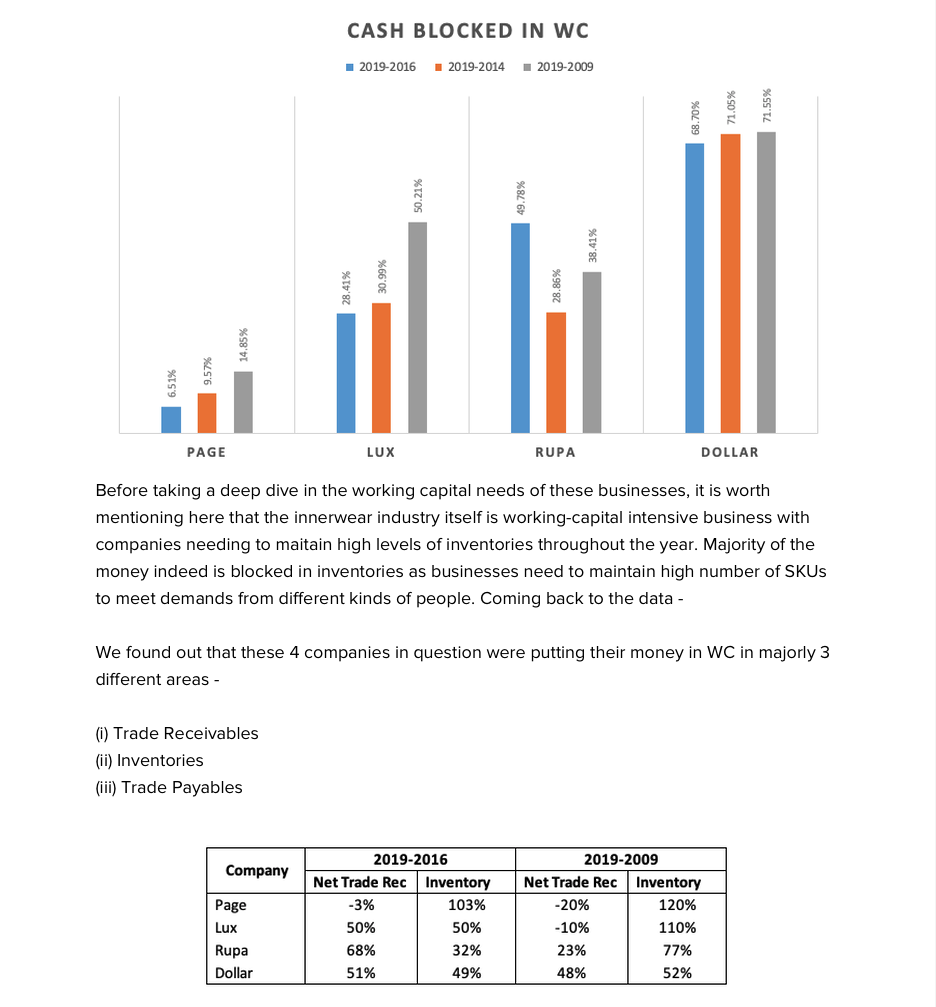

Page industries

Key takeaways from the conference call

Healthy recovery witnessed

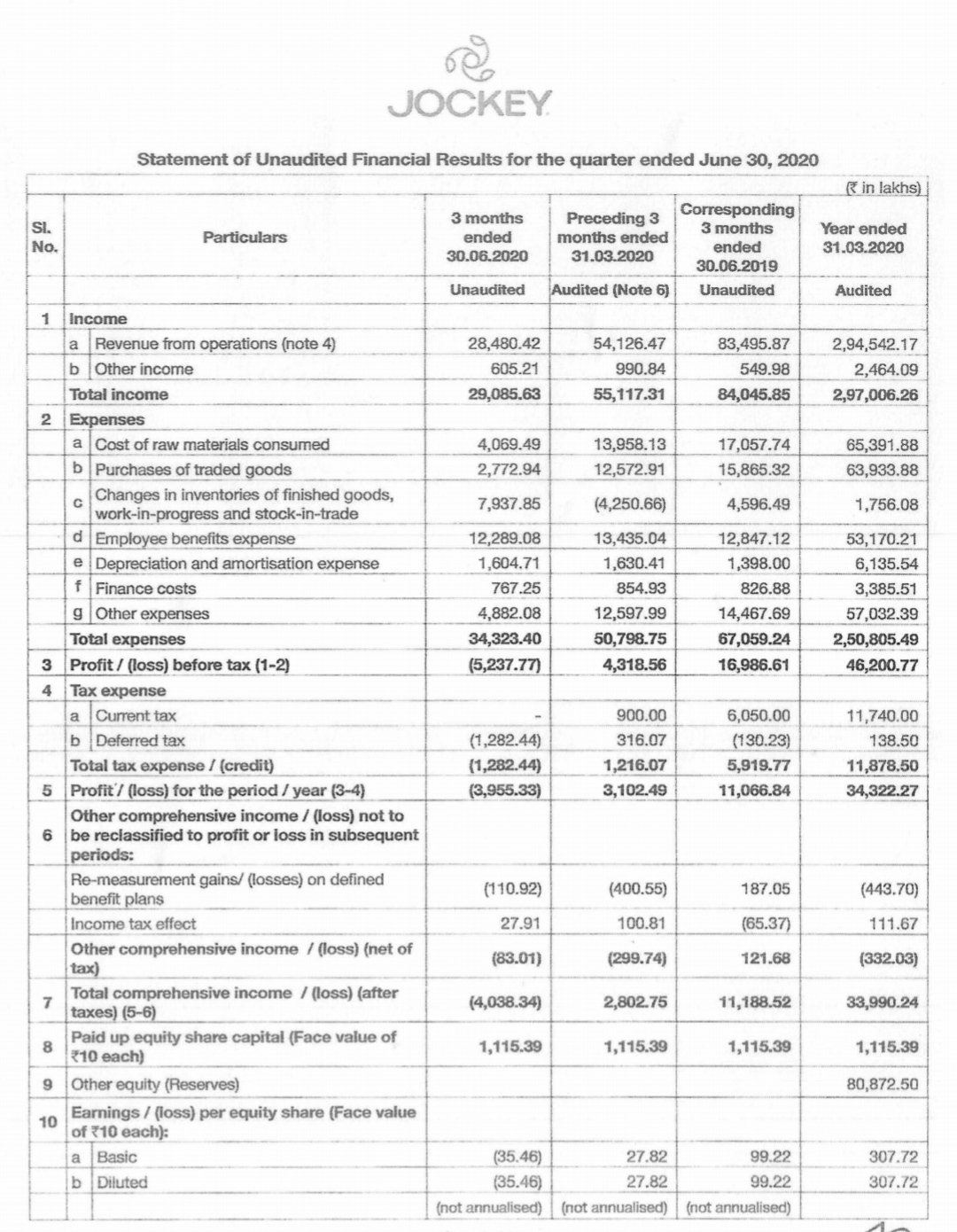

• Post the complete shutdown in April, business resumed only in the

last week of May, resulting in only 33 working days available in 1Q.

This led to 66% sales decline, with underlying volumes down 69%.

• The athleisure segment has seen a significant increase in demand and is on a growth path. E-commerce made a double-digit

contribution to sales in 1Q (3.5% last year)

• The LFS channel underperformed in 1Q, whereas EBOs have done relatively well

• Management stated that sales declined more than peers, given the strong reliance on sales from metros and A-class cities (60% from

six main metros, including Ahmedabad and Pune + mini metros).

• The sales recovery was healthy, with August registering flattish sales

YoY.

• By June, 80% of the workforce had returned to factories (~90%

now). Contract manufacturing partners are better placed than the

company itself, given that most are operating in smaller towns

• Capacity utilisation stands at 85-90% and all factories are open.

However, intermittent issues arising from government regulations

persist. The situation on the supply side is improving

• Management remains hopeful of a strong recovery around the

festive season.

Hopes to achieve 21% Ebitda margin going forward

• Page has increased prices across three products.

• Ad expenses were deferred during the quarter. This along with cost

control measures resulted in lower operating expenses. Some of

these savings are expected to sustain going forward. Marketing

spends will increase going forward.

• The company hopes to achieve 21% Ebitda margins in normal times.

• The innerwear and outerwear segments have a similar gross margin.

• A provision of Rs107m was made for slow-moving inventory in 1Q.

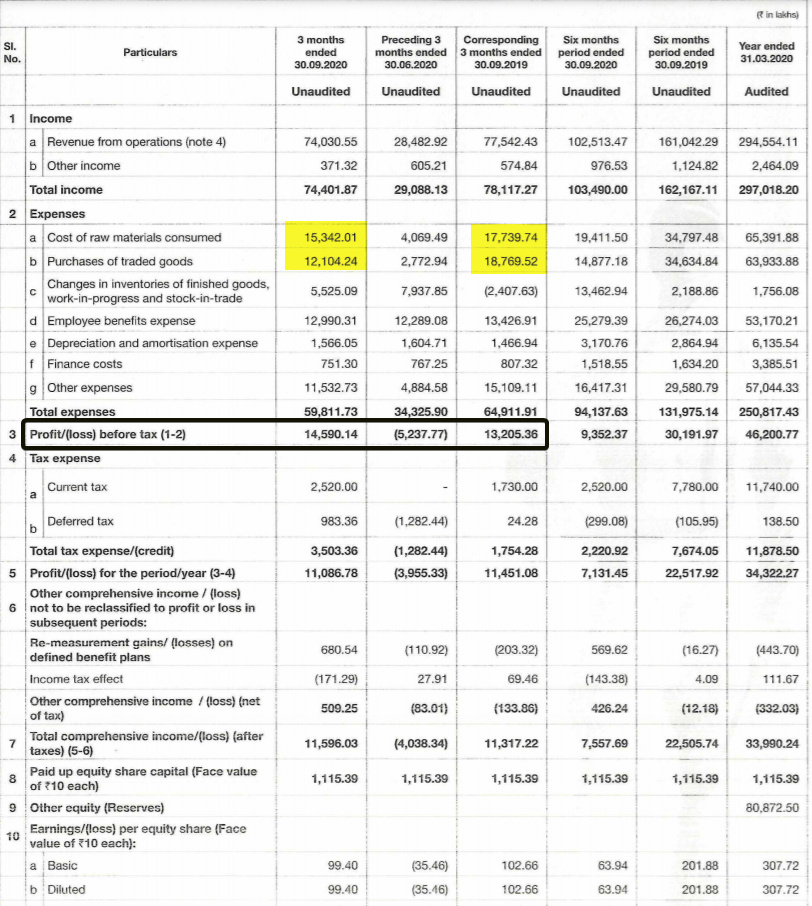

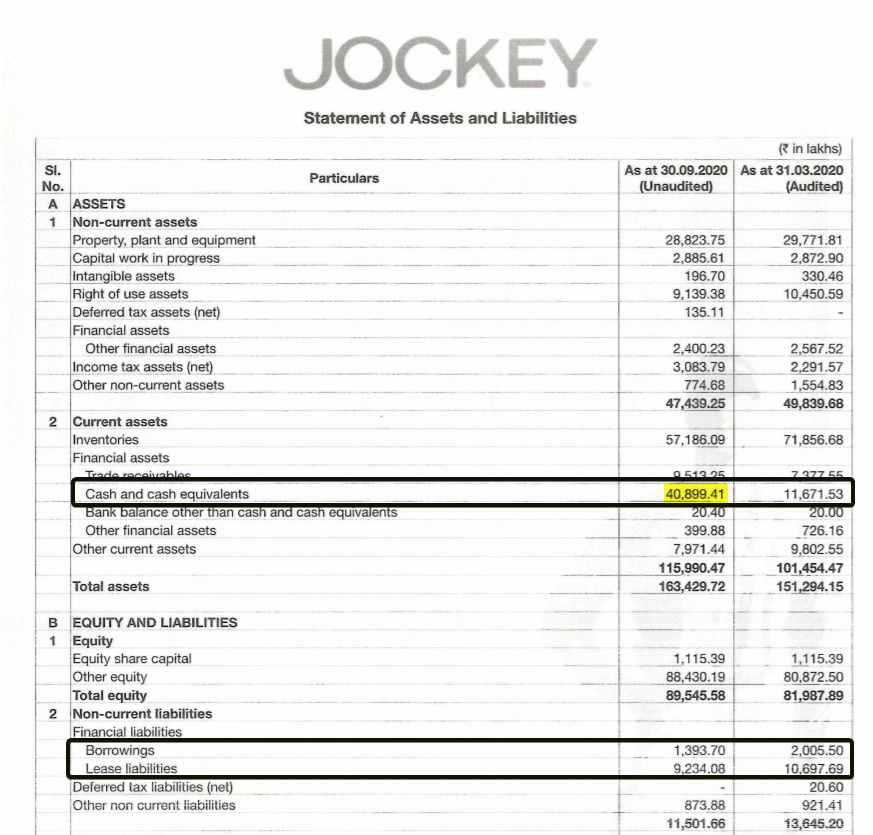

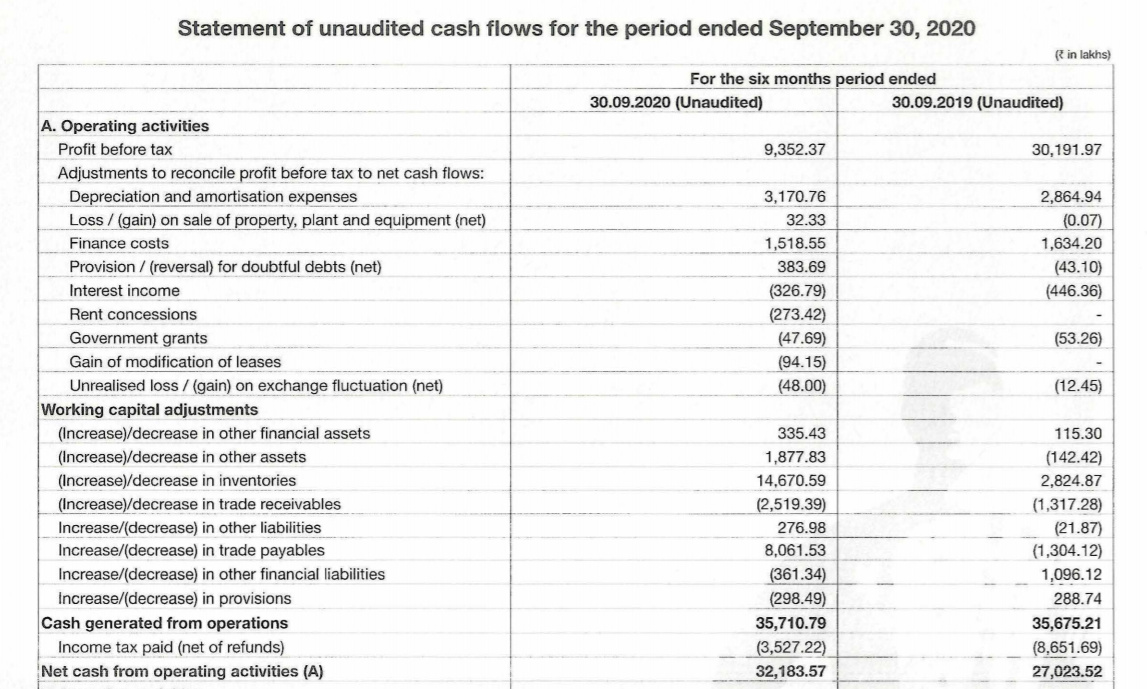

Balance sheet remains healthy

• Cash & cash equivalents

increased 56% QoQ to Rs1.7bn due to

better working capital management. Working capital reduced to

Rs4.1bn in 1Q. The company did not borrow any funds during the

quarter.

• Inventory levels had stabilised and were down QoQ at the end of

1Q.

Others

• Management has clarified that they strictly adhere to all labour laws

• Outsourced production share stands at around 30%, while 70%

goods are produced in-house

• Company has 100% of outerwear distribution under ARS, while

innerwear is closer to 60%

• The new face-mask launch was met with good indicators

• Muted capex is expected this year. Most of it will begin post 2020