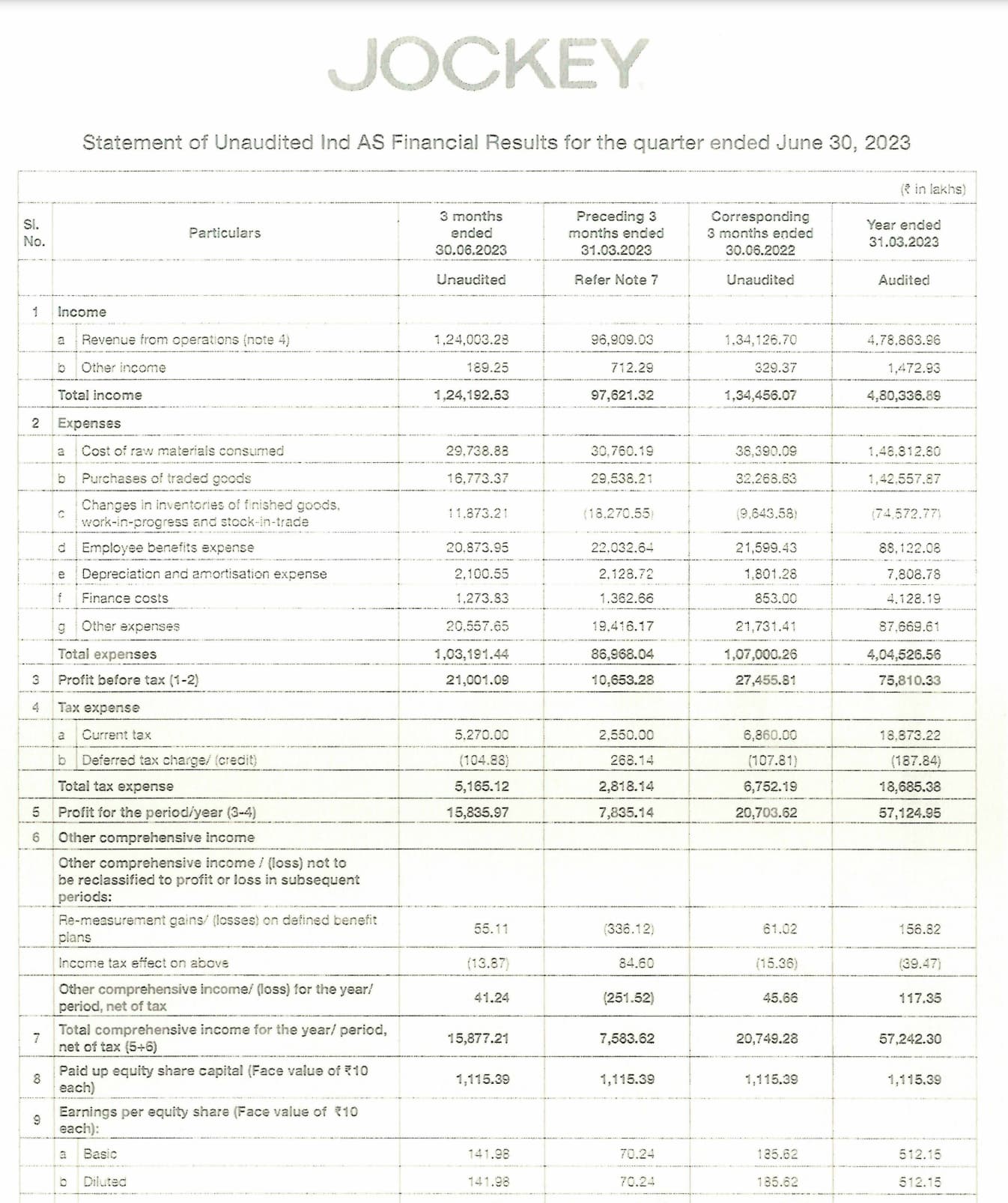

Another excellent quarter from Page

- Q4 revenues are up 26.2%, while volume growth was 8.7%.

- Operating profits grew 61% in the quarter backed by volume growth lead operating leverage.

- EBITDA margins touched 24%

- Announced a ₹70 per share 4th interim dividend for the year. Dividend per share for fy22 will be ₹370 (~410 crores)

- Full-year (fy22) revenues are up 37% (volume growth - 29%)

- Operating profits grew 52% and EBITDA margins were 20.2%. GM ~40%

- 110k MBOs, 1130 EBOs and 2800 LSFs spread across 2850+ cities

- Speedo: 1,340 stores, 26 EBOs and 12 LSFs spread across 90+ cities

Q4-FY22 results

Investor presentation

Concall highlights:

VSG (CEO):

- growth was broad-based (distribution, modern trade and ecom)

- digital initiatives, new product launches, retail expansion, and agile supply chain were the drivers of growth

- the supply chain is back on track

- experienced very high inflation trend (including packaging, logistics and cotton); measured price increase and optimum use of inventories sufficed our margins in spite of the inflationary pressures

- all categories are growing; equal focus on t3 and t4 cities as with t1 and metro

- speedo is back on track

- 27k team members, channel and supply partners were working very closely with us

- outlook very very bullish; firing on all cylinders to continue and sustain growth

KC (CFO):

- the best ever financial year in history

- gross margins at 43%

- building high inventory; hence cash down to 283cr (vs 435 cr fy21)

- the net-working capital is 631.7 crores (vs 512.8 crores in FY21); nwc days have come down to 60 days

- inventory stood at 950cr (vs 554 cr)+ at 92 days vs 71 days

Q&A:

inventory levels change of 150 cr+ vs Q3

- during the pandemic, we had to dig to reserves (inventory); most stock is high-selling stock making sure there are no opportunity losses like we had last year

any new price increases taken/planned?

- price increase of 8-9% in Q3 and 5% in Q1; no further price hike since December

gross margins dropped by 200bps but ebitda margins up by 500bps, any explanation for the same?

- price increase was 8% in Q3 lead to higher margins; operating leverage kicked in q4 (opex as a % of revenue has gone down)

- we are fine with 40% gm and 20-21% was ebitda margins

Volume growth for the quarter and full year?

- volumes for q4: 50 vs 46; 191 vs 148 for full year

revenue mix?

- we have stopped sharing that; growth is similar across categories. Athleisure was higher during the pandemic

ebitda margins sustainability at 24%?

- margins are dictated by input costs, we are always a value for money brand for consumers; costs (raw material costs) are beyond our control as of now, can’t say for sure if we can maintain these margins

raw material inflation?

- yarn prices have doubled in the last 14 months; still seeing further upward trends in prices as of Q4

sales and marketing spends are up this quarter, can we control this?

- not stopping this; they are very essential for the brand to capture the shelf space

- we have implemented automation to enable leadership manage better productivity; discretionary spends like travel are in control, to strengthen our leadership, new CPO (Ravi Kumar) has been onboarded

query on the productivity of existing stores after 45-50k store addition, how’s the repeat orders and productivity of new stores?

- entire distribution is bottoms-up where we see demand/customer base; it is strategic. we do check if the outlet justifies our brand. New store repeat orders are above 80%, productivity in the second year is higher with bookings coming from other segments

- a target of 1.5lakh+ stores in two years

other expense is 11% vs 16% average, what lead to this and is it sustainable?

- no moderation of overheads; all the expenses have grown but as a percentage of revenues is down; 2.5% in ads for the last two years

can we expect higher margins due to Athleisure coming in?

- we will be happy with 20-21% ebitda margins, don’t want to increase prices further. Want to compensate due to better operating efficiencies

kidswear trajectory?

- growth in-line with other categories; merged with Women’s in retail touchpoint. Present across 25% of the retail touchpoints

metro vs t1 vs rural markets? any pressure points in rural markets due to higher pricing?

- growth is similar across all segments (metro, t1 and rural); opportunities are higher in t3 and t4 cities

- EBOs registering double-digit same-store growth

rural - select few products at affordable prices; are they present in other stores as well?

- there are no specific products for rural, all products launched in rural markets are available in cities too

international markets?

- seeing huge potential; dedicated leadership. Focus on the middle east (mainly EBOs, up from 4 to 8)*; Sri Lanks is struggling. International is 1% of revenues. It is a franchise-based model like we do in India, the only change is that the partner would manage multiple channels

revenue growth, volume growth target for next 2-3 years?

- we have set a target of $1bn by 25-26 (we may even accelerate). We are now looking at aspirations of $2bn and beyond

- fy22 was the first time we took two price increases; the outlook is based on input cost inflation. Happy to see that premiumisation is happening as we expected

capacity, utilisation and expansion plans?

- utilisation is close to 80% (in-house); capex plans in-line with 3-year growth plans

- Odhisa plant will be operational by q4 fy23

- target: 70-30 (in-house vs outsourcing). Mostly we will stick with the same vendor partners for outsourcing. Currently, outsourcing is 33%

speedo recovery?

- we see long term potential in the brand; prudent for us to stay invested. Even with the reduction in EBOs, volumes are flat and early days w.r.t profitability. India is the fastest-growing swimwear market

store expansion in fy22: MBO (Gagan) up 42% and EBO (Rahul) in 21%; how do we prevent cannibalization of sales?

- MBOs expansion was done by geotagging existing presence; we only expanded new stores strategically to service the customer better. Existing stores have grown (sales) too along with the new stores. Growth is healthy double-digit; we monitor it monthly

dividend distribution policy?

- 50% of PAT (also a function of cash; higher sometimes like we did in 2019)

fixed asset turns?

-

12 to 13; should be stable even with the upcoming plants in Odisha

-

existing capacities are not good enough to serve the increasing demand, hence we are increasing capex; we mostly manufacture elastic too for backward integration. We have planned investments looking at long term; no brownfield, greenfield expansions only

is our customer base expansion low versus our volume share gain ?

- we are getting more wardrobe-shelf of the same customer due to increasing wallets, more products ; also onboarding new customers

Is any downtrading seen in the customer base due to high inflation?

- we don’t have a high asp; sell essential products; relevant across the year. Customers can downgrade seasonal products but we see this as an opportunity