I was hoping someone would ask them about the other income component. I had emailed them regarding their growth plan and details of their B2C offering but haven’t received a reply yet

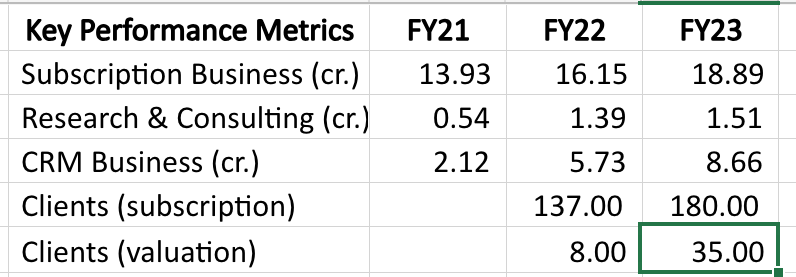

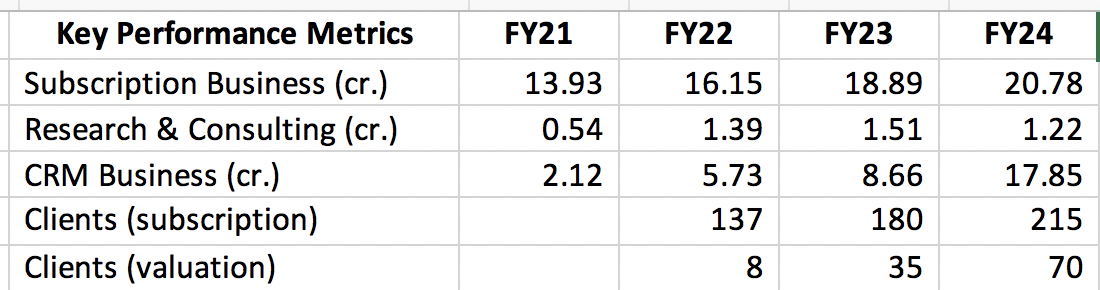

Propequity has been doing very well business wise, growing both their subscription and valuation vertical very well. Breakup between them can be seen below (CRM is their valuation business).

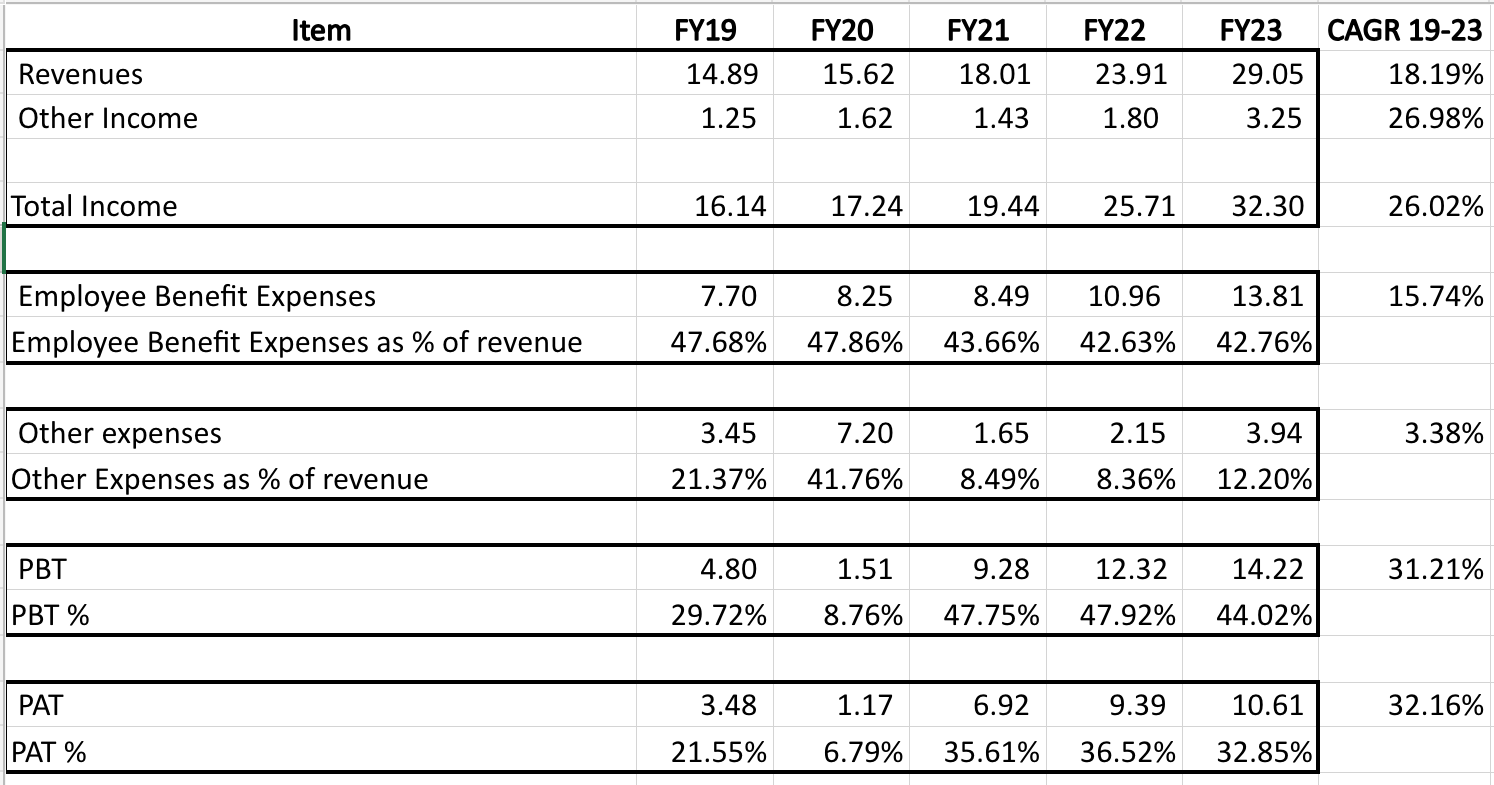

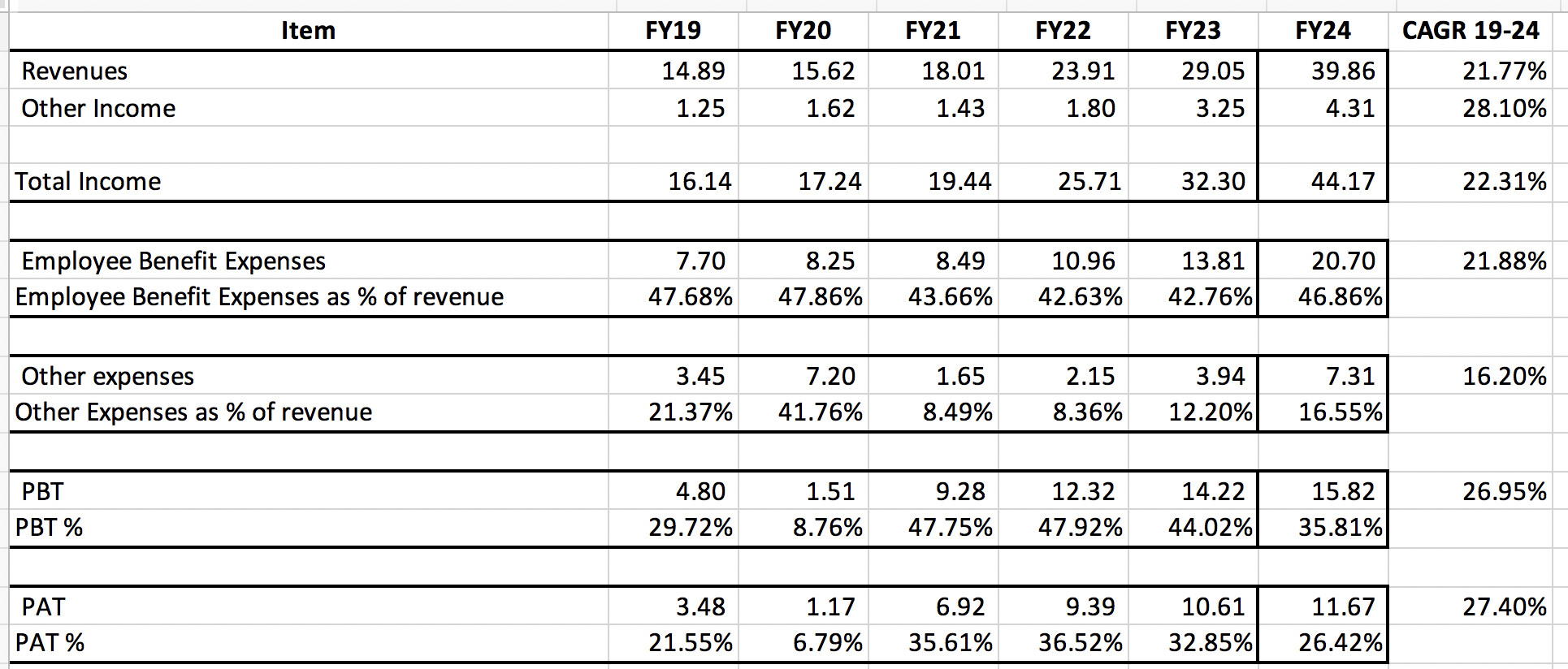

Longer term financials are below.

I am sharing notes from their recent annual report.

Financials

- Revenue breakup

- No income from future and options (vs 64 lakhs in FY22)

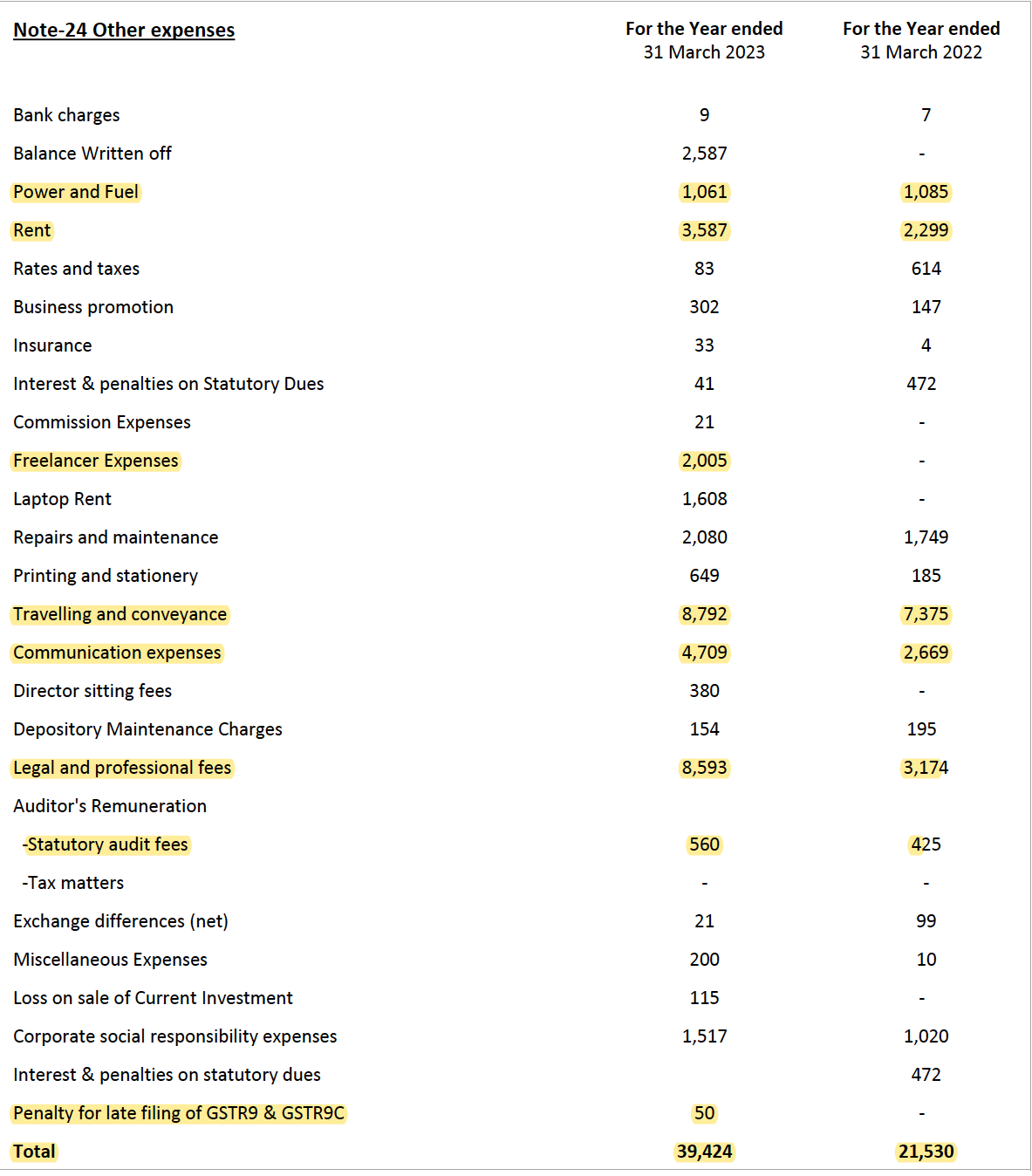

- Other expenses breakup

- Foreign exchange income: 90.5 lakhs

-

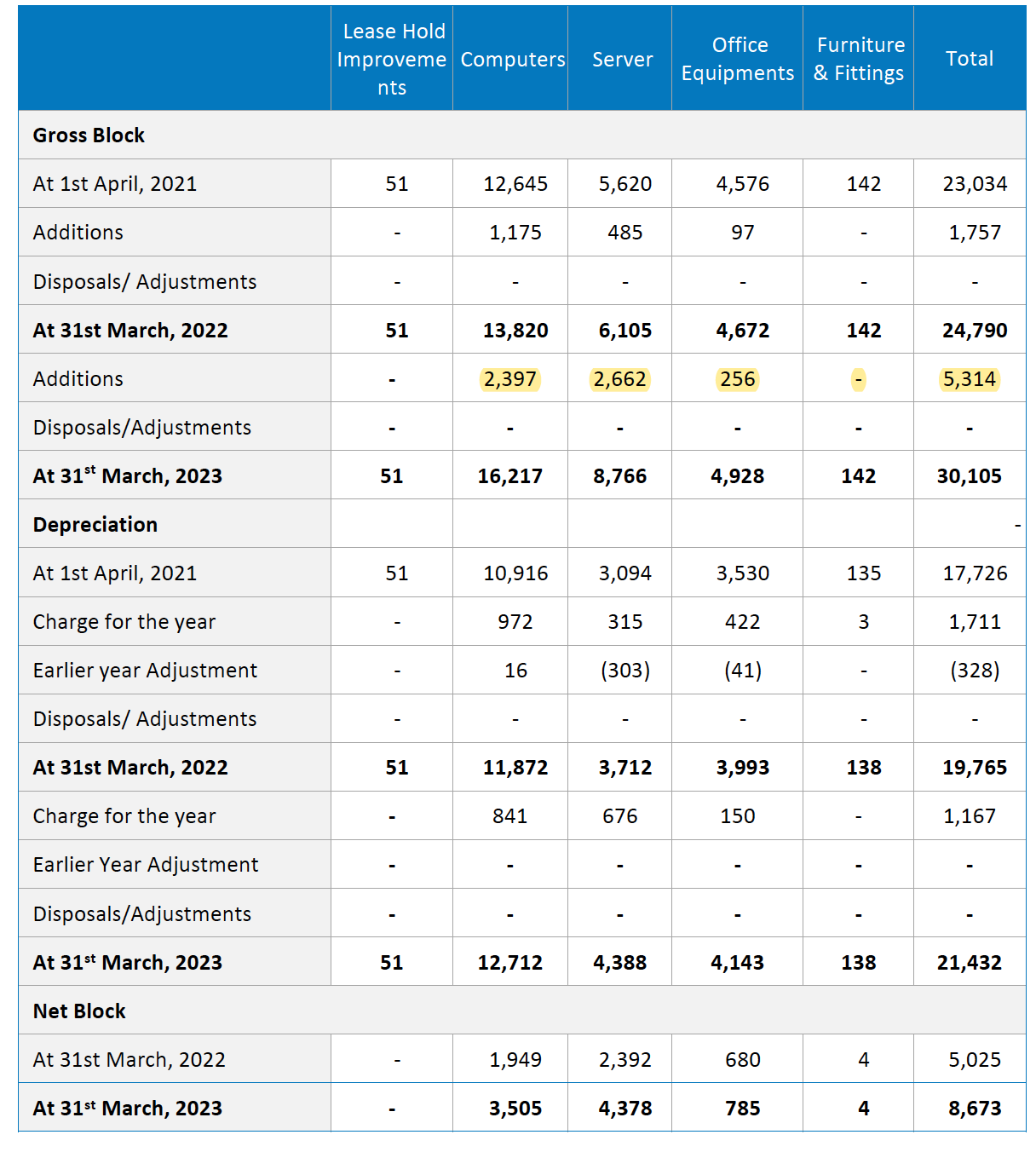

Capex: 53 lakhs (vs 28 lakhs in FY22). Computers + servers

- Share investment: 6.16 cr. (HPCL, IOC, ITC, ONGC) vs 5.1 cr. in FY22

- Other cash equivalent: 59.64 cr. (vs 62.14 cr. in FY22)

- Net liquid resources: 65.8 cr. (vs 67.24 cr. in FY22)

-

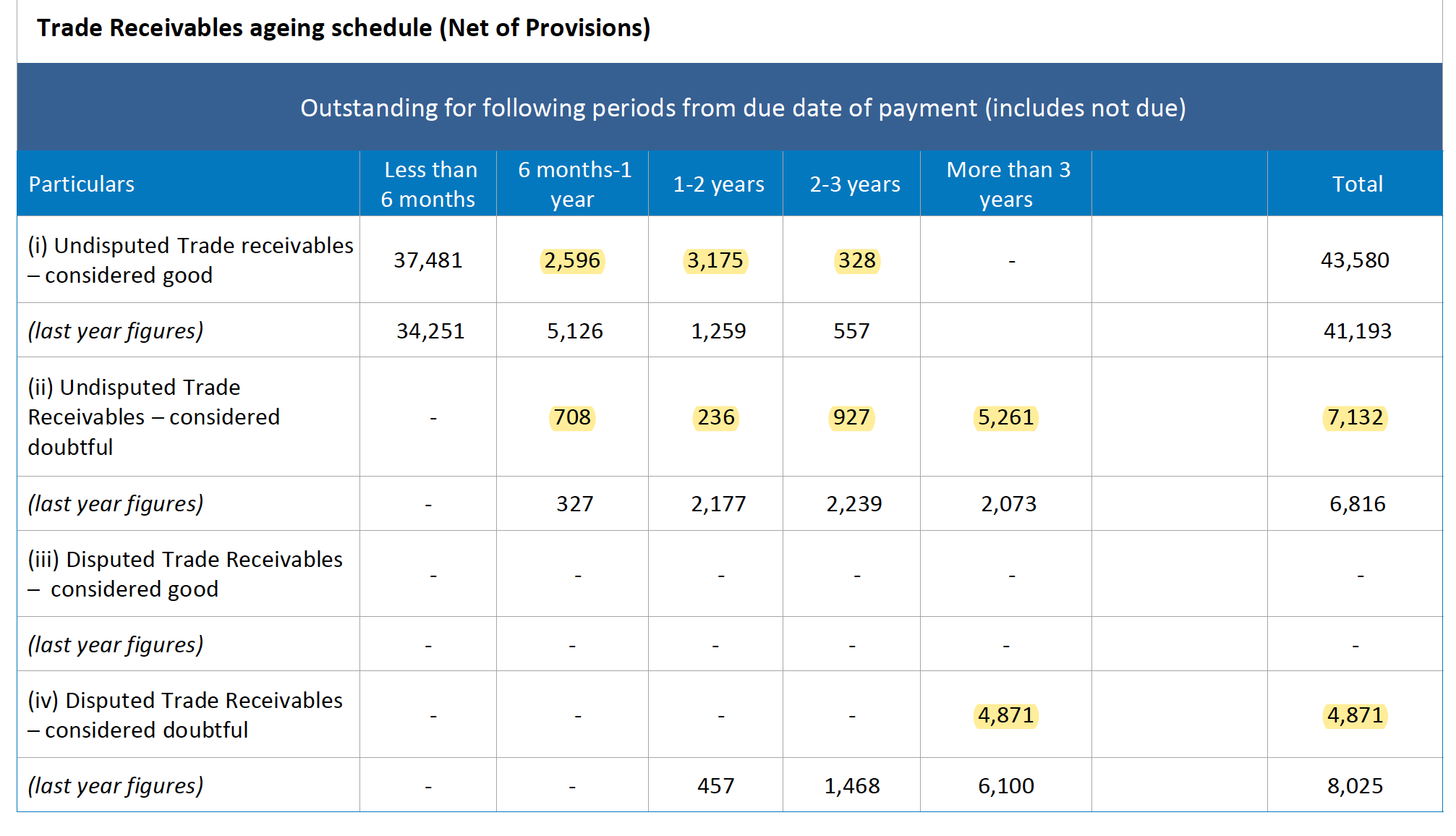

Receivables: doubtful of 1.2 cr. (vs 1.48 cr. in FY22)

General points

- 192 months of catalogued month-on-month real estate price data, requiring investment of 90 cr. Invest 6cr.+ annually

- 80% market share in residential B2B market

- 180+ institutional clients in subscription business (added 52 new clients which is highest since their inception). 80% retention

- Employees: 370+

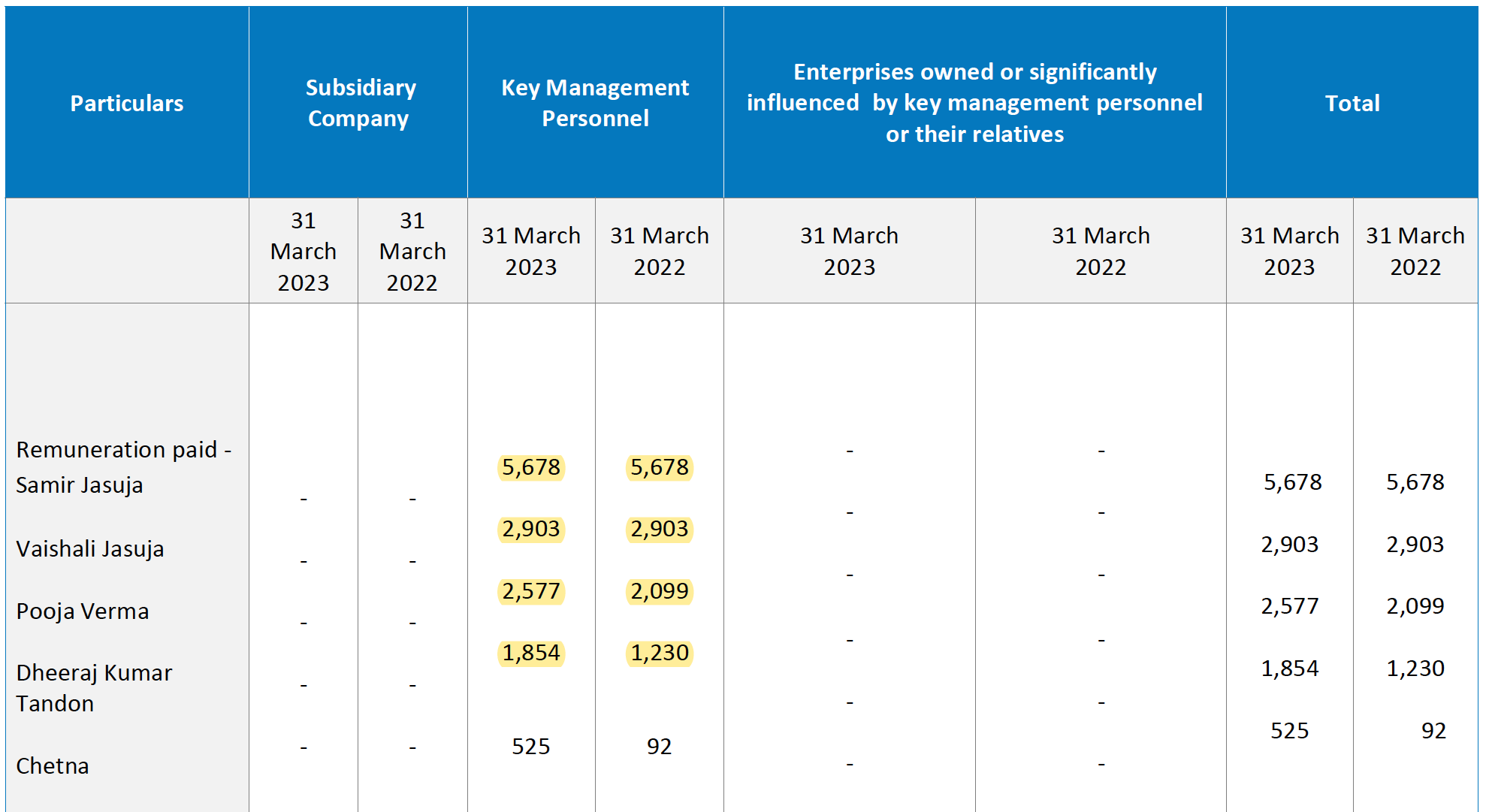

- Standalone remuneration: Average increase in managerial remuneration was 6.75% & average increase in salary of employees other than managerial personnel was 10%

- FY20: Launched commercial leasing data product

- FY21: Launched retail valuation business vertical

- Planning to enter B2C Segment and YouTube Channel

- Banker: ICICI

Propedge:

- Sales: 8.66 cr., PAT: 1.64 cr., shareholding: 80%

- Expanded to 36 cities in 10 cities

- Serving 35 clients (vs 8 in FY22)

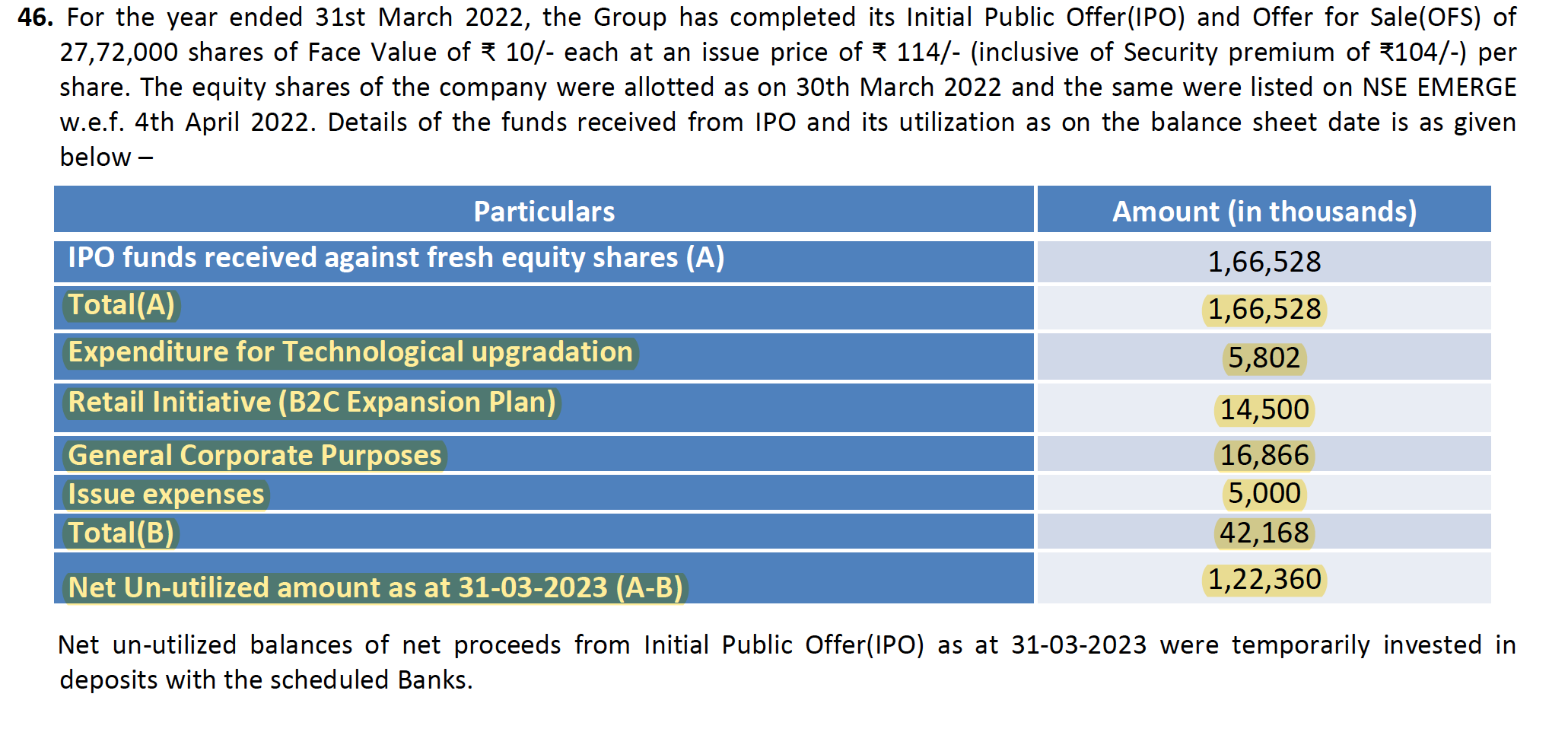

IPO utilization

Related party transactions

- Pays rent to Topaz IT Services Pvt Ltd (16.2 lakhs annually) for office space in Gurgaon

- IT related services to Marquest (3.94 lakhs)

Disclosure: Invested (position size here, no transactions in last-30 days)

20 Likes

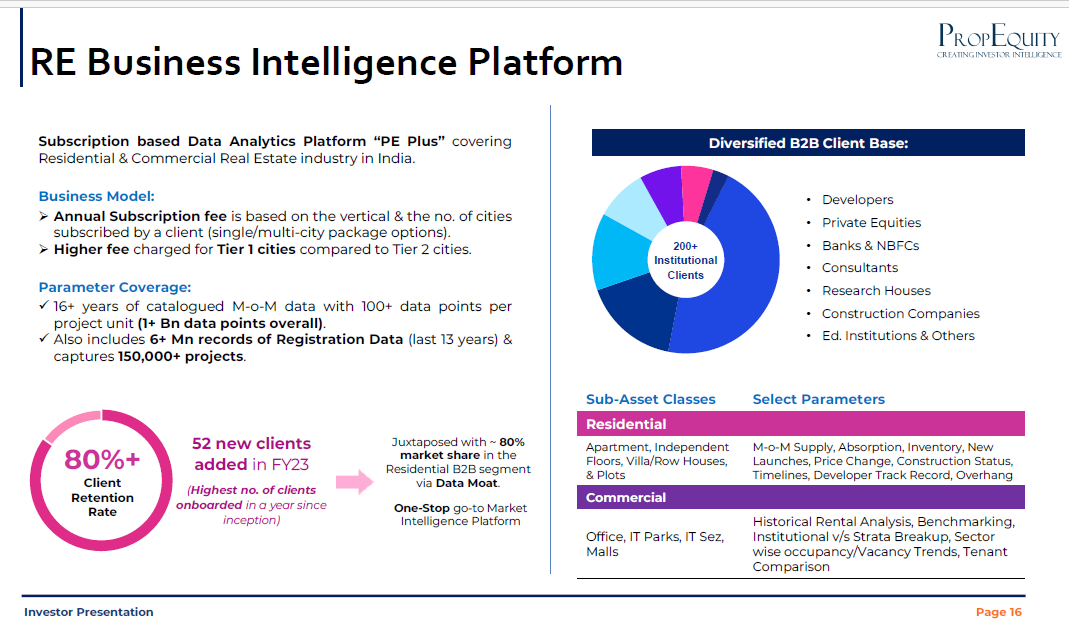

Latest PPT for Propequity is out. Attaching some of the interesting snippets here.

Would appreciate your thoughts on how Propequity is evolving here @harsh.beria93. TAM for the business looks huge ostensibly, strong growth in the valuation business along with multiple optionalities to grow look possible.

4 Likes

I feel their current size is very small compared to the opportunities out there. An example is their valuation services business, where conservatively the TAM is 300-500 cr. annually, and they are only at 15-20 cr. revenues. Their main competitors are individual valuers who might not give the same level of standardization and turn around times. I imagine this vertical can easily reach 80-100 cr. in next 5 years.

Another way I have been looking at their business setup, is that their main customers are financial institutions and they are looking to build multiple service lines to increase their product offerings (e.g. valuation services, project construction monitoring, project prices, etc.). This is simply customer mining and a relatively low hanging fruit.

They have also been talking about building a B2C line of business, the details of which was hazy in the past. In this presentation, they have clearly highlighted their plans of going into asset light model of development management, and building a social media reach to generate potential leads.

So there are lots of opportunities and it will boil down to their execution skill. Samir is a veteran in this industry and has all the relevant contacts. Maybe @Deenar_Toraskar , @Chins or @nirvana_laha can add more as they have done significant amount of work on this industry. My notes from their presentation is below.

02.02.2024 presentation

-

Annual subscription fee is based on the vertical & #cities subscribed by a client. Fees is higher for Tier 1 cities vs Tier 2 cities

-

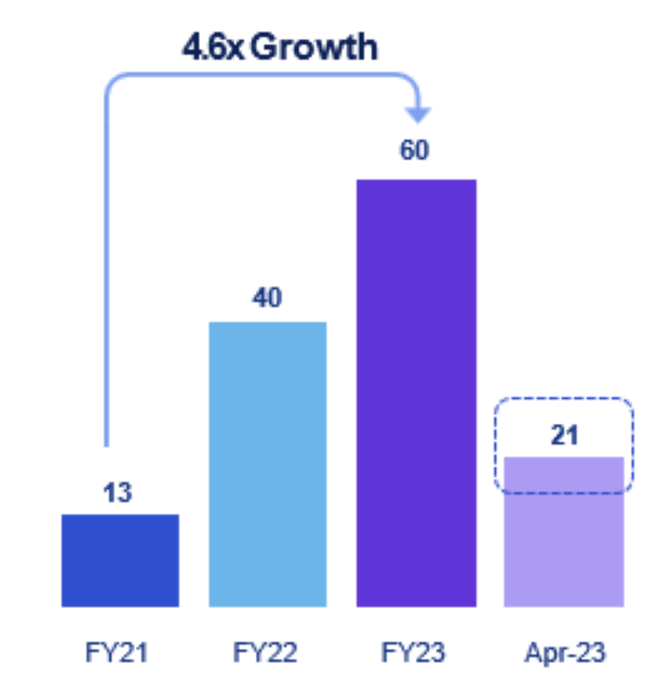

Construction finance reporting: 21 reports were processed in a single month in FY24 vs 5/month in FY23 (see image below)

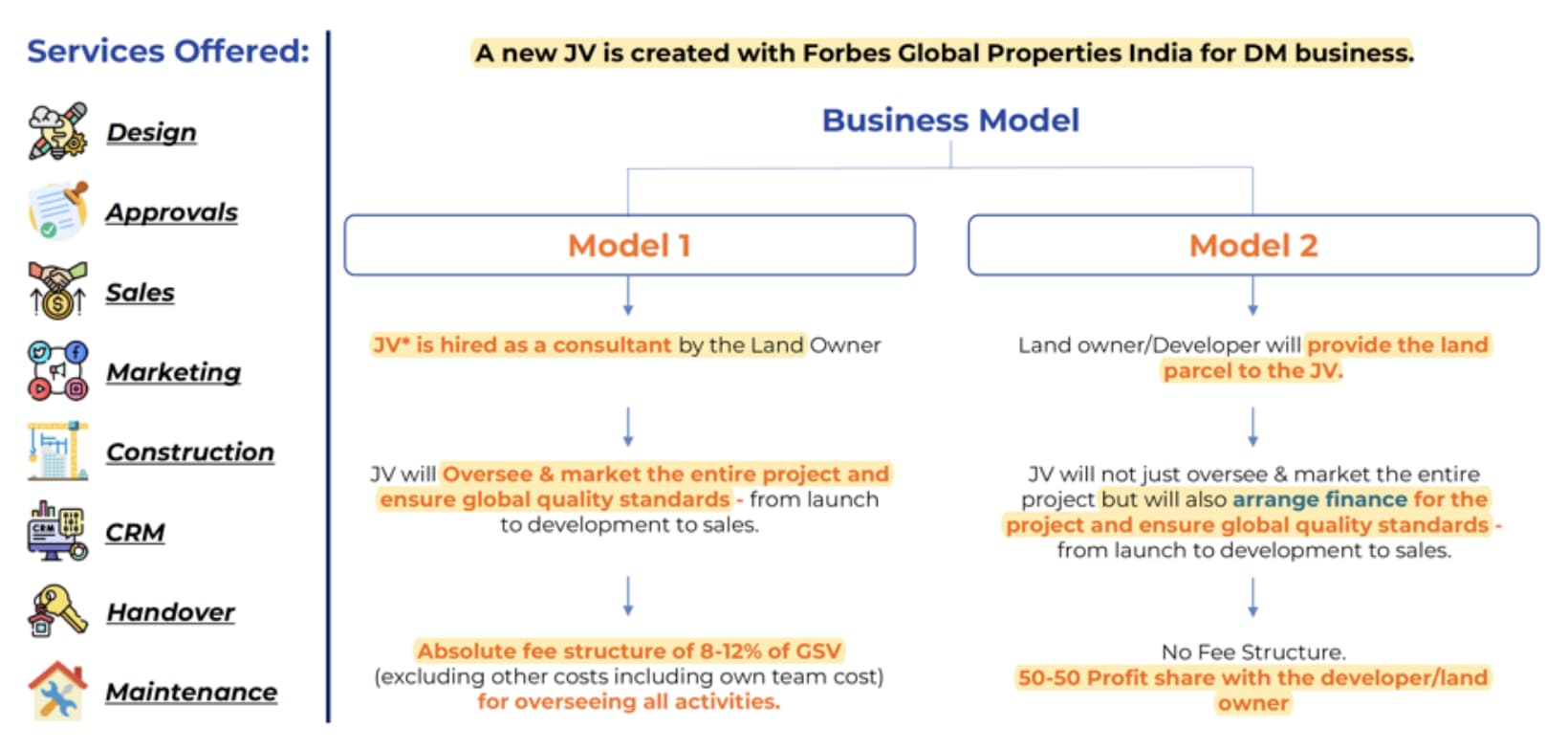

- Developer Management: In JV with Forbes Global properties (2 models shown below)

-

PropMonitor: Monitors under construction projects for banks and gives reports to them for release of construction finance payments

-

PropBuild: New B2B construction portal

-

Will double valuation business revenues in FY24 (8.7 cr. in FY24)

-

Clients increased to 205 (vs 190 in Q2FY24) in website subscription business. Retention ratio is 85%

-

Cash grows to 71 cr. in FY24Q3 (vs 65 cr. in FY24Q2)

-

SamirJasuja-PropEquity: Youtube channel for lead generation for projects (aims to reach 1mn+ followers)

Disclosure: Invested (position size here, no transactions in last-30 days)

15 Likes

Propequity grew sales by 37% in FY24 and plan to maintain this trajectory. They are launching a number of new verticals which might keep margins in check. Management seems very growth hungry and want to scale to 500-1000 cr. revenues. Concall notes below.

FY24Q4

-

Website subscription

-

Clients increased to 215 (vs 205 in Q3FY24) in website subscription business. Retention ratio is 81% (vs 85% in Q3FY24)

-

47 of top 50 developers are their clients

-

Average client generates 10L/year, they are now selling at 5L/year to smaller developers to increase market size

-

Residential peers: Liases Foras, Commercial peers: Propstack, CE matrix

-

-

Valuation

-

Clients increased to 70 (vs 65 in Q2FY24) in home valuation business

-

Valuation business is now operating at 2 cr./month in March 2024, targeting 75-100% growth in sales in FY25 (vs 17.85 cr. in FY24)

-

Make 1200-3000 per valuation report depending on city and bank

-

Will make 15-25% EBITDA margins until they reach 100 cr.

-

-

Auto financing

-

TVS and Mahindra are the 2 incumbents (100 cr.+ revenues each), they outsource employees. Propedge has started this division on request of banks

-

In housing finance business, 10-15% of housing valuation business of a single bank can be given to Propedge, however there are no such restrictions in auto valuations

-

50L second hand car market annually; Rs. 600/inspection (atleast 300 cr. market size)

-

5-6 valuations done at one shot which makes unit economics better than housing

-

Will be launching in 3 cities in next 3 months

-

-

Plant & machinery valuations: Will be launched in next 6 months

-

Will be going overseas (Middle east) & launch B2B consulting services

-

Project monitoring vertical (B2C)

- 2300 cr. project monitoring market size – if this picks up it will be bigger than all their other verticals put together

-

Developer asset management

-

Charge 8-10% of project revenues

-

Will raise separate real estate private equity fund which will be used for project financing (won’t use Propequity’s balance sheet for this)

-

Original plan with Berkshire Hathaway was to do high end valuations, however then Berkshire pivoted to development only which has also not taken up

-

Forbes will be involved only when developer asks for the Forbes brand name

-

In other developer asset management, will do standalone and not partner with anyone

-

-

Social media

-

Will help them generate leads for developers + give them a captive user base for their project management vertical

-

Invested 50 lakh in FY24 (social media + developer management)

-

Will be investing 1.2 cr. in social media vertical in FY25

-

10% army discount for TATA projects, don’t know how they will monetize the Youtube channels so far

-

60 leads in last 2 months

-

-

Research & consulting will reach 2-2.5 cr. in FY25 (50% EBITDA margin)

-

No plans of paying dividends as they have lots of growth opportunities

-

Current focus is on growth and not on optimizing margins

Disclosure: Invested (position size here, no transactions in last-30 days)

23 Likes

Interesting insights from the presentation -

• Client retention rate stood at 81% in FY 2024.

• Added over 8400+ residential and 950+ commercial and retail projects, exceeding 1,73,000+ projects and 57,500+ developers across 44 cities in residential, commercial and retail asset class.

• Cash reserves and liquid current assets have exceeded over Rs. 750 million as of 31st March, 2024. (Around 25% of current Market Cap)

• Subscription business revenues grew by 10%, consulting vertical was flat

• added 54 new clients in the subscription business, current annual subscription contracts stood at 215 as of 31st March, 2024.

• Revenues from valuation business have more than doubled from last financial year

• grown from 35 to 70+ clients (Banks, HFCs and NBFCs) in valuations and CRM vertical

• Adding new verticals in the valuation business, Auto Valuations and Plant and Machinery Valuations in FY 24-25.

• 369 employees in FY24. (195 in FY23)

• International expansion through Middle East

• Company is also looking for right projects to launch their Developer Asset Management Business. Completely asset light with no investments from Propequity’s balance sheet

4 Likes

Excellent thread on what looks like a promising business.

Key questions are:

Subscription

- 80% retention is low - to achieve 20% growth, they need to make 40% from new client wins / existing customer x-sell (doesn’t look like much chance of x-sell yet). That’s not happening! Strong growth in overall business is masked by the web subscription business growing at c.10%, which is less impressive for a company of this size. This is not a SaaS business, but as a reference, best in class SaaS businesses have 90-95% gross retention (i.e. from purely existing customers reducing spend / churning) and net retention ratio of close to 105-110% (through x-sell / price increases etc.)

- What is the level of recurring level of customer usage of this platform? i.e. why can’t customers buy it in a year, download reports / take screenshots on reference benchmarks and cancel their subscription because of low usage? Sure, they keep refreshing this database with new properties and that’ll be appealing to the likes of KKR / Godrej / HDFC Bank etc. which are large spenders, but for a marginal developer where they are trying to target incremental sales to, I am not sure if there’s a need to keep purchasing this annually

CRM

- I’m actually more bullish on this opportunity as this is a high frequency, transactional nature (think like payments), and clearly they’ve got the right data to augment banks’ internal assessments with their valuation / collateral management tool. Unsurprisingly, this has grown at a rapid pace, and there’s more to come out of it. Whilst for their current scale, it should be fine, as they capture a large share of the market, they’ll be exposed to real estate cyclicality imo

Other

- Why is so much cash sitting on their books? Have they got a definitive M&A pipeline? This is not a pharma business where you need to invest into capex / product pipeline.

- How closely linked is the business growth to current real estate upcycle? Do we expect growth to sustain if the real estate activity slows down?

- Why are they already thinking about international expansion? What data have they got outside of India? India TAM itself must be big. I mean Zomato tried going to the middle east, and they scaled down because they realised they haven’t got the expertise. I’d rather bet on a business that sees a market fully

- Their pricing needs more thinking (and transparency), as charging just 10L p.a. to top-tier PEs like KKR or Blackstone and large banks like HDFC Bank is criminal. With a professional investor, they could make significantly more

Overall, feels like a strong business with a moat, but as always, some questions loom over given low coverage. Would be nice to get views from other forum members who’re tracking this stock.

6 Likes

Re-posting this here as this is the main thread for P.E Analytics

Business: Data and Analytics in real estate Industry.

PROPEQUITY_13052024185901_Final_TranscriptIntimation.pdf (nseindia.com)

Hi. Reproducing my blog post below

Business Model

PE Analytics is an analytics firm. They have a database on real estate transactions and valuations in India. They sell subscriptions to this database and that is how they earn revenue.

Founder and Management

Samir Jasuja is the founder. He has been working in the Indian real estate industry for more than 25 years. He has an MBA from Fore School of Management in Delhi in 1996. He started the company in 2008 when he realised that there is hardly any database in the country which has updated information about real estate transactions in India. He does not have a tech background. His strong suit is marketing. In fact he has co-hosted weekly TV programmes for NDTV and CNBC in India on the real estate sector. He owns about 70% of the company. His wife is also involved in the day to day running of the company. Together both of them take about 1.5 crores of salary and rent from the company annually. On the capital allocation front, Samir has definitely improved. The company was losing money on F&O a couple of years back. They have now completely stopped doing F&O. I hope Samir continues to be judicious with the 60 crore plus cash balance that the company has today.

Samir has collected a decent management team around him. There are a couple of important people who have kept working along with him for more than 10 years. One is Avinash Jha who does sales. The other is Shantanu who handles all IT and Tech. But there is no formal ESOP plan in the company. The founder has not announced any plans to beef up the management team as the company tries to grow 30% year on year. This remains a company which is heavily dependent on the promoter.

Product

They have a database which has data for more than 10 years on the real estate industry. For example at what price have flats been sold in an apartments complex over the past 10 years. They keep updating this database regularly. They have a team of 200 people on the ground across the country which also manually collects information related to real estate projects. This information is then fed into this database. Each subscriber to the database pays 10 lakhs annually on an average to access this database. I have no evidence of AI being used to make this database more useful to its users. For example can the user ask questions about the Gurgaon sector 55 market using a chatbot? The company has a small tech team of about 12 people. So I am not sure how much they are focusing on enhancing the technical features of this database. For now I am going to consider this as a giant excel sheet which the company maintains. They have launched some simple features such as placing a pin on a google maps and getting to know about real estate transactions within 2 kms of that pin. But I am not sure how are they going to make this DB even more useful?

In addition to this revenue stream, they also help out banks with property valuations and project monitoring. For example if a bank has lent money to a borrower for construction of his home, then the bank wants to monitor the state of the building on an ongoing basis. Instead of hiring its own team, the bank can outsource this part to PE Analytics. The company charges a fee per job to the bank.

Distribution

The company has a captive user base of about 180 clients who are already using their database. The company has not laid out in detail how many sales people actually go and pitch the database to other potential users. The company claims that currently their database is being used by institutional players who have assets of 5 billion USD under management. This includes the likes of real estate focused PE funds. But this is a very small pie of the total real estate market in India. How will the company reach the remaining institutions is unclear to me. It seems the company will continue to use their existing salesforce for this purpose.

For the valuations business, the company already has a relationship with banks and NBFCs because they were using its database earlier. The company is now trying to mine the same customer base for this revenue stream as well. The company has managed to increase the number of clients for this vertical very well for the past two years. Again here the company will continue to use its existing sales force to get new clients.

Brand

The company has a very good brand. They are well known across the real estate B2B industry. One reason for this is that the company has been around for more than 15 years. Second reason is that the promoter has taken efforts to associate the company’s brand with well reputed brands like Berkshire Hathaway, Indian Army, NDTV, CNBC and Forbes. He understands how you can enhance your brand value by associating the brand with other reputable brands. And he has done so without spending a ton of money.

Even today he continues his brand building efforts by launching a new Youtube channel where he addresses retail real estate investors directly. These videos have high production values and seamlessly promote the management, the Propequity brand with the data based monologue of the promoter. Going ahead since most of the revenue is going to come from the B2B market, the spends on branding should continue to be controlled.

Financials

This is a cash rich company. They have about 70 crores of cash and are adding about 12 crores annually. They have hinted at deploying this cash in their growth efforts but they have not clearly spelled out exactly where would that be. The traditional database subscription business is a cash cow with high operating leverage. They have already built the database and spend some money annually to keep it updated. Each new rupee of revenue from this business almost goes directly to the bottomline. The TAM for this business is low though. So this business will probably continue to grow at the rate of inflation in the country.

The company does not have any debt. The ROCE and ROE is depressed because the company does not know what to do with the cash it has or with the cash that it has generated.

Bull case

The company is trying out multiple options to open up new revenue streams. They are trying out project management of real estate projects in collaboration with Forbes. They are launching in the Middle East. Though I am not exactly sure which business line. The most exciting potential business line is a B2C vertical. The company has launched a Youtube channel where they post short videos which are relevant to a real estate retail investor. For example is it the right time to buy a residential flat in Gurgaon? In such video they share data based observations about the real estate micro market. I am not sure how exactly will the company monetise all the followers and subscribers to this business. I guess they are also still figuring that out.

Second part of bull case is explosive growth in their property valuation business. Banks currently work with many small independent valuers of mortgage properties. The company can take away market share from this semi-organised competition. This business is growing at 40% year on year for now. The company already has a network within banks and other lenders. Also, going ahead with improvement in drone technology may be the company can use drones to increase the productivity of their field force. May be 1 person can monitor 10 under construction projects in a day across the city by using drones instead of him physically visiting each property.

Bear case

The promoter may end up misusing the cash on books. He may announce a huge increase in promoter salary or he may suddenly increase the size of related party transactions. The promoter can also blow up a lot of money in building the B2C business. He may end up spending tons of marketing money on Facebook and Google ads and not be able to generate commensurate revenue from the customers thus acquired.

Or the company may not be able to handle the scale as the valuation business starts scaling. The promoter may not build the management strength needed to handle scale as he may loth to increase the autonomy granted to his management team in decision making.

Finally, the government may create a real estate database as a public good which would collate all real estate transactions being registered across the country. Right now this data is in silos and is not available as a public database which can be queried via an API. The government may do that and that would reduce the usefulness of the proprietary database that the company has. And finally, we may come to later discover that the company used illegitimate methods to collect data for its proprietary database. For example the company claims to know the rental which is decided between a landlord and a tenant in a mall. But I am not sure how does the company get access to this information? Isn’t this information only available to the two parties entering the agreement?

P.S. My internal blogs/drafts for this post are below.

Disclaimer: The views expressed in this blog are personal. I may or may not hold investments in the stocks mentioned.

Saturday, 25 May 2024 at 12:30:29aPM

I have spent more time on the company. I have read the annual reports. And I have looked at whatever management interviews I could find over YouTube. And I don’t have a clear verdict. First let’s just talk a bit about the history of the company. So the founder completed his MBA in 1996 and started a company in 2000. He was early to figure out that the internet will become big in India and all over the world. But he was only 27 years old. And could not really accomplish a lot with his first company. But this idea of the internet being a medium through which information can be easily shared stayed in his head.

So he joined as an employee then with a company which was into real estate. Now here he learned something important. This industry which was so near to the heart of India men. This industry had no data at all. I mean no centralised repository of transactions happening all across the country. When you considered investing into a real estate project, you were flying blind. You used the inefficient method of tapping your network to gather intelligence about the viability of your proposed real estate investment. And now it was up to the quality of your network to determine the actual quality of your decision. Also, till this time FDI was not allowed in this industry. So I can assume how the builder cartel would have controlled most of the supply. And also how the builder cartel would have controlled access to all information (at least as much as possible).

Now Samir (the founder), figured out that as FDI will be allowed, the industry would also attract foreign investors such as foreign PE firms. Now those firms do not have a deep network in India. They would hire Indian professionals and depend on the decision making of those professionals to make money in India. But even the boss of such PE firms sitting in the US would like to have as much data as possible at his disposal. He would want to keep a check on the activities of his Indian staff and he would want to compare what the data is saying with what his team is telling him. All the data was collected by government agencies. But the data was in silos. Also, government had not properly digitised everything and also had not properly made everything transparent. And therefore there was an opportunity to become the data ocean, in which you gather data from all the data lakes where data was residing. Now Samir does not have technical chops. But I think he loves real estate. He has been toiling in the industry for more than 25 years. He is a marketer par excellence. But he hasn’t been able to discover something which would scale up a lot. But he doesn’t stop trying.

So without much of a plan, he did launch Propequity in 2008. This is exactly when the global financial crisis was going on and when the Indian real estate market was almost at its peak. The next 12 years were bad for real estate in India. There was so much supply built in 2005-08. And before it could be absorbed completely, so many other projects were started in 2009. And then 2011 onwards the market completely tanked in North India at least. But Samir still kept going. He just approached all big investors in real estate. He told them that look I have collected all this data. And more than collection, I keep monitoring this data on a monthly basis. And I am only charging you a small subscription fee considering the size of the funds that you have. For example I am only charging you 6 lakhs a year. A good analyst will cost you that much straight out of college. And the institutional real estate investor looked around and found that there was simply no other option as compared to Propequity. And so they went ahead and started paying him. But more than the money I think what they gave Samir was a sense of validation that he was on the right path. So Samir started building this business in earnest from then on. And his customers also told him exactly what kind of data they wanted. So he started collecting more kind of data. The good thing about his business is that he would start collecting one type of data basis the recommendation of one customer, and suddenly that type of data would also be useful to most of his other customers also. This is the operating leverage one gets with digital businesses.

One thing remains a mystery to me though. What is the source of the information that Samir is collecting? For example I understand how he gets the data on whether a real estate project is RERA approved or not. This is public knowledge and is posted on probably some government website somewhere. Or may be at the request of some customer he monitors a project under construction. He may be sends one of his employees with a camera to the site of the project and this employee clicks pictures of the project and uploads it to Propequity’s database. This part is easy to understand. But how would Samir get the data for the rental which has been decided between a tenant and a landlord in a mall. This is private information and is only known to the two parties to the agreement. How does this information get out? Samir is very confident about this data. In fact he even highlights in his official documentation that he has access to this data. But he never discloses how exactly is he collecting this data.

Ok back to the story of the company. So Samir kept going through the decade of the 2010s. This was a tough decade for the Indian real estate market. There was overcapacity built in the previous decade. And more than that banks did not have liquidity to lend easily to real estate projects. Banks were going through NPA problems and therefore builder financing was not coming through. Also, then there was a crisis starting 2018 in the NBFC sector. Now he was facing another problem. He was making revenue and profits. He was paying himself a decent salary of 70 lakhs a year. Nothing too fancy. But the problem was that there was no deluge of foreign capital and foreign institutional investors coming into India. During the boom years of 2005-2007 everyone was expecting that over the next twenty years so much of foreign capital would come into India for everything. We will get money for real estate and for startups. But as the next decade went by we realised that India is not very welcoming for foreign capital. The corruption at the local levels of the government was still there. The government at the top level could not convince foreign investors that we have the honesty and the expertise to successfully deploy foreign capital and generate returns on it. So even though Samir kept increasing his clientele, but they were not growing at an exponential rate. He was not able to sell hundreds of licenses a year for the database that he had built. May be he was able to sell a few licenses a year.

While all this was going on, he figured out that there was nothing much that he could do about the pace at which the market would grow. What he could do was he could do some marketing for himself and the company which would not be very expensive. And so therefore he went ahead and approached NDTV and CNBC and convinced them that he had the data which would be useful to retail investors. And retail investors were the customers of these news channels. After all they loved to consume TV since it did not involve a ton of thinking. And so Samir hosted a couple of weekly TV shows about the real estate sector. He already had the data, he just chose to present it to the viewers. And he got distribution because of these news channels. Now exactly what he got paid in return I do not know. But at least it got him some marketing. I think inherently also he likes to be in front of the camera. He is a bit flamboyant. He is not the best capital allocator. He does not have the baniya brain when it comes to money. Instead he is an optimistic flamboyant marketer who loves talking about real estate. And he keeps looking for opportunities where he can combine his love for the camera and marketing for his company. For example he has recently started a YouTube channel and named the channel on his name and the company’s name. On this channel, he talks about different micro markets across the country from a real estate perspective. For example I saw a video where he was pontificating on why the Gurgaon real estate market would remain stagnant going ahead. But we are getting ahead of ourselves. Let’s come back to the story of Propequity.

So Samir then got slightly bored. He was selling new licenses every year. The older clients were getting retained at about 80% every year. But there was not a lot for him to do daily. His TV programmes were doing ok. But they were not setting the country on fire. So he started dabbling in futures and options and stocks. As usually happens he lost money in F&O. I think in 2019 or 2020 he lost about 4 crores in F&O. And this was at a time when the overall profitability of the company was not that great. May be the company was doing a profit of 6-7 crores annually. But ever the excitable adolescent, Samir had discovered something new and shiny.

And then covid happened. And the whole world stopped. Samir too was confused about what to do next. He was unhappy that he had lost so much money in F&O. So he reduced the F&O activity that he was doing. He did not completely stop it but he reduced it. And everyone anyway was being a doom monger and saying that real estate has crashed and will take many many years to come back. Samir somehow continued to retain his clientele. The ones paying him a subscription fee for his database. And then it suddenly occurred to him. The data that he continued to collect showed him that the real estate market has started to recover. He was not sure why. He did not really understand the relationship between the huge stimulus launched by the western governments and how it would impact the real estate industry in india. So he was not aware about why real estate was showing a revival. But he was sure that there was a revival happening. And this gave him hope. That may be he should try again. He should try to be a big shot. And in parallel he got the idea that he can become a vital cog in the way the mortgage market works in india.

So right now if you are a bank in india, you have people coming over to you and asking you for home loans. Now as a bank you need to do a lot of homework before giving out a home loan. You need to see the home prices in the locality where the home is located. And you went to the data that Samir had for this. Thankfully this saved you a lot of time that you would have spent in talking to brokers in the area. But then your homework doesn’t stop here. You still need to physically send someone to the location and see for yourself what is the condition of the building where the borrower wants to buy a home. And you need to have manpower for this. And then you are always monitoring whether the person you have hired on your rolls to do this is not wasting his time and also providing accurate information to you every time. It is a lot of hassle to manage people. And then to manage people who are physically away from you is even more of a hassle. And you are not paying this person a lot of money. You are paying him may be 30,000 a month and you are not going to get a top class Human Resource at that price in India. So as a bank you look for alternatives. Why can’t some professional company do this job for you and you would be happy to pay them per job. So as I understand there are right now independent valuers who are basically a one man company. These are contracted by banks to carry out this job. These people are not on the pay roll of any one single bank. They are instead paid for every job that they do. But again banks face the problem of unprofessionalism here. For example one bank may pay him 500 rupees extra for a job and therefore this independent valuer may not turn up on the day he is supposed to. He might make an excuse and he might try and delay doing his job for your bank.

And a bank cant afford this indifferent to the deadline. Banks have a TAT. They have made a commitment to their borrower that the bank would do its job properly and on time. And the bank knows that now the borrower has many options. If the bank does not deliver a quick TAT on such procedural jobs, then the customer may be poached by a competitor. Everyone in india wants to do property loans, as the collateral is easily available. So this is where Propequity has seen an opportunity. Propequity already has a relationship with banks and other property lenders like HFCs. They all use its database to figure out what is happening on the ground in the property market all across the country. And now Samir is convincing them that I will do the valuation and other procedural tasks that you want and in return you pay me a fee for every such job that I do. Samir is also telling them that I already have my people on the ground across the country and they are collecting data for my database. I am going to use the same people to also do the job for you and therefore the money that I charge for such valuations would not be exorbitant. And this is the business vertical that Samir is now focused on.

He made a subsidiary which is dedicated to doing this. And this business is now growing 40% year on year. Because of inflation anyway this business will continue to grow at 7% year on year. And right now Samir is taking away market share from individual proprietors. So for the next few years he should be able to continue to grow this business at 40%. On top of that the overall industry is growing very well. Home mortgages in India will continue to grow fast for the next couple of decades as people continue to upgrade their lifestyle and their homes. So let’s see how much is Samir able to run with this business.

He is also trying out other options. For example he has recently spoken about going to the Middle East. Exactly what will he do there I am not sure yet. He has also done a tie up with Forbes magazine. As part of this tie up Forbes will lend its brand to developers in India for a high end luxury residential project. Think homes upwards of 1 million USD a year. Propequity would run the operations on the ground on behalf of Forbes. For example Forbes may agree with a developer that they will be building an apartment building where minimum area would be 10,000 square feet. And now Forbes does not have people in India who will actually monitor daily whether the builder is keeping his word or not. That is what Propequity would do on behalf of Forbes. There may be other nuances to this arrangement. But this is all I could gather till now.

So what he is cleverly trying to figure out is that how can he leverage his expertise and database and plug himself deeper into the real estate value chain without allocating a lot of capital to this initiative. Actually he raised about 10 crores in the IPO promising that he would use up this money to launch a B2C vertical of his database. Right now each subscription to his database costs 5,00,000 a year. This is too much for a retail investor. Also, the marketing cost to reach retail investors is very heavy. For example if he starts spending on google ads for his B2C vertical then he would be fucked. The money he would be spending to get even one user would be much less than what he can get from that one user. And he does not have a lot of money to spare. So instead he is trying to first build an audience in the retail vertical. He is doing YouTube videos which talk about real estate micro markets in a way which is relevant to the retail investor. And he is getting views and subscribers. But how will he exactly get revenue from this I am not sure. Is he going to depend on the ad revenue that will be generated by his videos? Or will he launch an app and he will ask retail investors to register themselves on that app? But what would the user do after registering on the app? I dont know. He hasn’t spelled that out yet.

But my point is that he is definitely trying to figure out options for ways he can look to diversify his revenue streams. He only has the valuations business doing some of that for him. But other than that he has nothing going on which is contributing meaningfully to the revenue. Let us see what happens.

14 Likes

Judging from the discussion so far, the following points seem to be the consensus view:

-

Investors find the subscription business unexciting.

-

The valuation vertical seems promising, but no one seems to have more insights to share.

-

The cash on the balance sheet is a common concern.

I have done a significant amount of work on the industry in the last year with @nirvana_laha. I have met with management a few times since listing, spoken to several of Prop Equity’s clients as well as competitors in the valuation vertical. In the interest of raising the quality of the discussion on the company, here’s my view on how one should look at the company.

1. The valuation vertical has the highest probability of scaling successfully

I spoke to senior management at one of the largest PSUs, as well as a private bank, both are Prop Equity’s clients. Here are the key points:

-

Banks get valuation reports made for loans against property as well as new developments. For almost all private banks and PSUs, this is outsourced to companies like Prop Equity.

-

Depending on the ticket size, they need either two or three reports per property, and use the consensus to determine the loan eligibility / amount.

-

A vast majority of these reports are done by small brokers that operate out of a few districts in a city. (Example: Patwardhan Consultants that cover Mumbai / Pune / Nashik) There are only two or three companies that offer valuation services pan-India. Prop Edge and Adroit are in this list.

-

Banks have their own issues working with smaller regional brokers:

-

Lack of a uniform reporting format - A valuer in Bangalore may provide a different kind of property report from a valuer in Kolkata. This quickly becomes a headache with scale.

-

Small brokers don’t have bandwidth - The last week of a month is extremely busy, as banks try to clear pending loan cases. During this period, smaller valuers who run a 5-6 person office get overloaded, and they can’t cater to everyone at the same time. During this period, the turn around time for a report gets stretched to several days, while every bank wants them asap.

-

-

Larger organisations like Prop Equity or Adroit don’t run offices as lean (40-50 employees in major cities), and therefore have more people. This allows them to meet TAT targets during these busy periods. They also have standardised reports from across the country.

In cities where Prop Equity and Adroit have scaled successfully, they have taken 30% wallet share each from a large bank, displacing smaller unorganised brokers.

The thesis here is a shift from the unorganised to organised given a lack of serious pan-India players. There is room for 3-4 pan India companies to empanel with a bank, as banks have limits on how much wallet share a single valuer can take.

I leave it up to the reader to determine the market size for this vertical in India, but I have high confidence in Prop Equity scaling this vertical to 100 Cr. topline, with 40% EBITDA margins in the next few years.

2. The subscription business does not deserve bandwidth

It’s very difficult to raise prices for the subscription vertical as it stands right now. They have onboarded almost every large developer and bank. The TAM for this subscription business is at its infancy in India, and it’s far more profitable to build and sell value add services on the data they have collected.

This business will continue to bring in 40-50% margins as the costs are fixed, and this is why management calls this a cash cow. Any incremental effort spent on this vertical wont be as rewarding as the other new verticals that management has incubated, so it’s completely reasonable for management to focus efforts elsewhere.

The proof of this is in the valuation vertical: in 3 years, they have built this business from scratch and scaled to the size of the subscription business already, with over 400 employees and a topline of 20 Cr.

3. The cash on the balance sheet will be used on new verticals

Management’s model here is to incubate a new vertical, provide equity to the partner running the vertical, see how it fares with clients, and only after seeing success, spend on scaling the business.

There are three new verticals being scaled at the moment: developer management, project monitoring, and the vehicle valuation. Management mentioned that if project monitoring sees good traction in the next year or two, they’ll increase the spending on sales & marketing to increase visibility and win clients.

4. There are several dormant optionalities

- Developer management is a vertical with Forbes Global that could have a large leap for Prop Equity given the profit sharing agreement. The JV will earn 10% of the sales value of any property developed and sold by the JV, and distributed to the partner that brought in the deal. They also have an agreement to develop one such property within five years.

-

Project Monitoring is the B2C vertical that management has been working on for the last 3 years. His claim is that this market is larger than the valuation vertical, and there is no competition in this space in India right now.

-

YouTube can be a very powerful platform with scale. There are numerous success stories of people who have started with producing videos, gaining a following, and then starting a business / selling a product to subscribers. If management can scale this to 100k followers and beyond, this could be a great platform for lead generation for all the other verticals.

In my opinion, I think investors should focus more on the valuation vertical scaling, and treat project monitoring, developer management and the automobile valuations as an optionalities without pricing them in.

D: invested in family accounts, no transactions in the last 30 days.

I’m amazed by how confidently people can write such things about others they’ve never met. Especially on a first name basis. I feel it’s undeserving of this forum.

28 Likes

Hi. I have noted your feedback. I like to use stories to explain things better. It’s a mix of facts and creative writing to keep it interesting. Happy to chat more about it!

2 Likes

to peope who track prop equity closely, is there a seasonlity in the business of valuations? is q1 relatively weaker?

can use q1 update by comapny as a reference.

Disc- Invested

1 Like

Hi, Is the Q1 result has been declared ?? can anyone post a link of the same, checked in their website, screener, some other sites too, can’t find it for Q1 FY 25

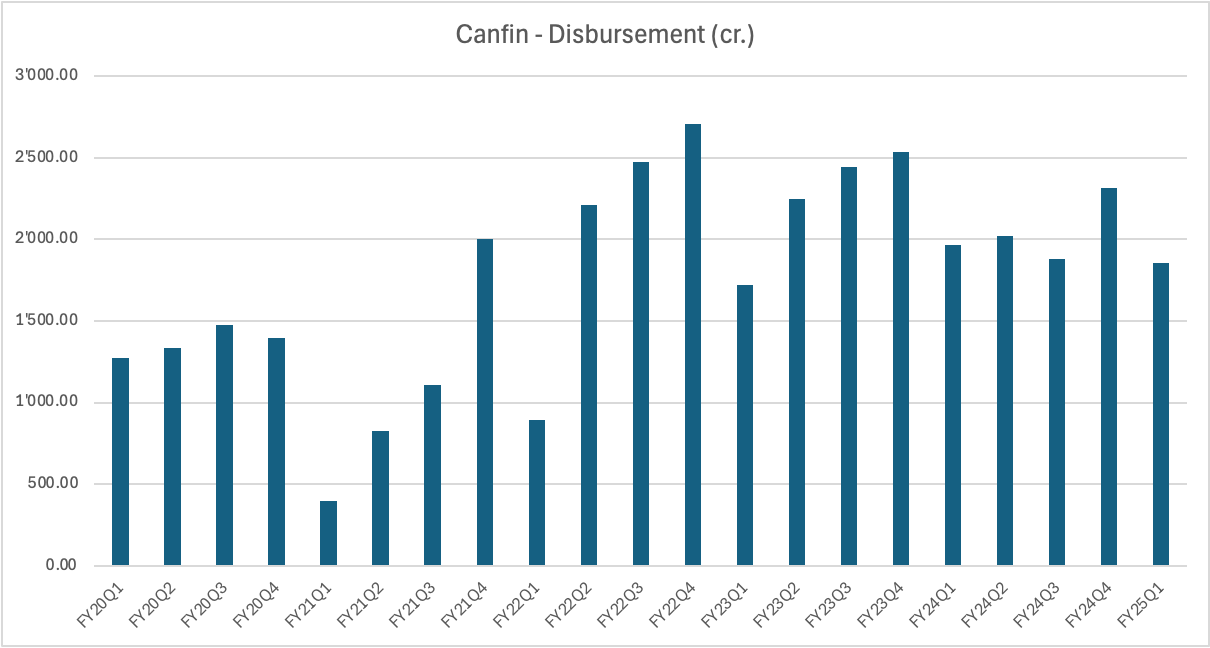

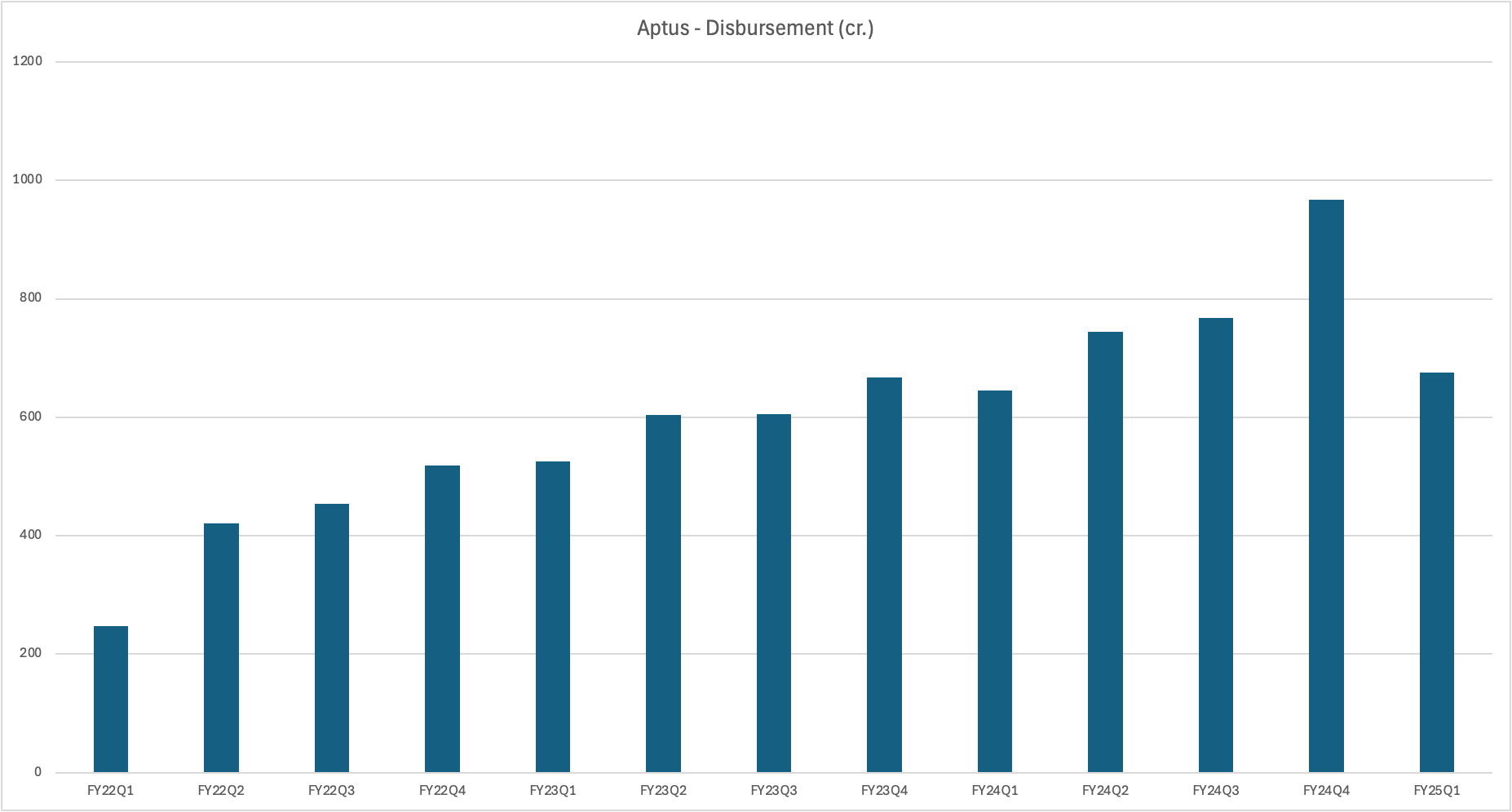

I think housing loan growth shows some seasonal trends, with lower disbursements in Q1 and it rises until Q4. Sharing some examples below.

Canfin quarterly disbursements

Aptus quarterly disbursements

I guess the same is now getting reflected in Propedge’s revenues as they are reaching decent market shares.

Propequity reports half-yearly results as they are a SME. However, they post quarterly presentations.

https://nsearchives.nseindia.com/corporate/PROPEQUITY_19082024094126_Investorpresentation_final.pdf

14 Likes

I think Homesfy providing real estate brokerage only in B2B and B2C segment, meanwhile PE Analytics providing Prop Intelligence, data from past to present. Both are different is respective segments. Pls correct me if I am wrong. Noob here

i have few hypothesis for your queries, which may or may not be true.

This is the problem for any type of directory service-based business or educational content based revenue type (selling courses),

so I think one they won’t be giving any download option or based on extra charges they may allow, making difficult to copy or scrape the data (Ex: LinkedIn) like legal clause to go against scraping and such I guess or you can completely block the scraping bots

Second is value addition although not at drastic level but keeping the customer through maintaining their digital history, notes and things like that, all are subtle , or creating the reports for the banks integrating with other products (I m just speculating how they may retain the customer)

this may be linked to your other point, I agree with you that it may be closely related to the real estate market,

so may be to reduce the dependency on this real estate cycle they may venture into other countries (again speculating)

all of this can be clarified on con call or AGM meeting

1 Like

The results for q4 are out.. Any reason why they havent put out Investor presentation this time? There was a change in head for valuation business, Want to understand how this segment performed this quarter

1 Like