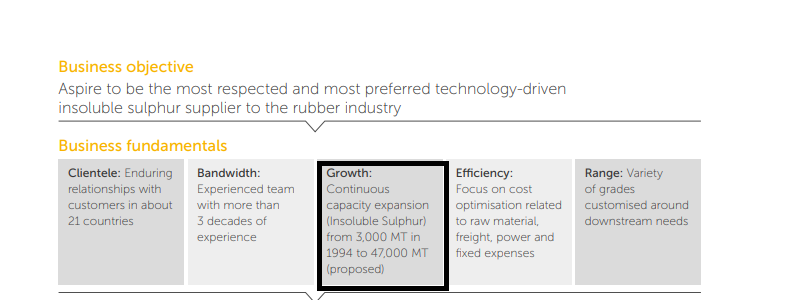

As per public available information after 11000 MT expansion ,total capacity of IS will be 45000 MT (34000+11000) . In the recent concalls and 2021 AR it is mentioned that , after this expansion capacity will be 47000 MT. I am attaching the screenshots of the same. Please comment -

Hello, i have not seen much discussions on this good fundamental company since few months.

Would like to ask your views on the recent capex being done by the company, and if enough demand is there, for them to protect their operating margins.

With a current market cap of approx 1k Cr, and if OCCL compunds their book value every year @ 20% for the next 5 years, where would a logical investor asess the Market Cap after 5 years?

Please let us know for any new developments at the company operation level or if any positive/negative development in the market/region where their products are sold.

Insoluble prices (IS) have been declining over the years and there seems to be an overcapacity in the industry (with no greenfield expansion viable) as a new capacity from Eastman, OCCL and China Sunsine has all come on stream in the last 5 years (have covered China Sunsine’s per ton realizations in the attached link)

On the other hand, there has been a decline in CV sales in india and also globally, which has muted IS demand (a commercial tire uses 10x IS as compared to a passenger tire).

Despite all the advantages discussed here in the prior posts (oligopolistic market, large approval time, high MS of OCCL), here are the risks that one needs to be careful of -

With 10% new capacity coming on stream globally in next 1 year, overcapacity can further increase OCCLs overheads as new capacity is commissioned.

Sale of IS business by Eastman – Eastman Chemicals sold its tyre additives business to a PE fund called One rock Capital. The sale has been at low multiples, suggesting that the business was struggling – “We are pleased to reach this agreement with One Rock and to have a clear path forward for the rubber additives business. We continue to evaluate other actions to improve our AFP segment. The company expects to recognize asset impairments or a loss from the agreement and completion of the sale.

A large number of CV radial tyres are imported from China. In Jun20, India imposed various curbs on import of tyres from China. While this is a positive for OCCL, any changes in this policy will have an impact on domestic industry along with OCCL.

Promoter Capital Allocation – Of the INR 123 crores excess cash in OCCL BS, INR 31 crore has deployed in startups like Bira (1 cr), Blue Tokai (0.5 cr) and AIFs like Grand Anicut Fund (5 cr) IQ Startup fund (4.3 cr). The total committed capital to these investments in INR 60 crores, almost 11% of NW. based on investor feedback, the mgmt. has revised the dividend policy to 50%. With no new capex in the next 3 years, cash generation is expected to increase.

Despite the above risks, I think the current valuations have a reasonable reward to risk ratio.

Bad Set of results due to higher input costs. Profit down 50% QoQ.

More worrying sign is the demerger of the chemicals business to a subsidy with the current company becoming a holding/investment company. They also mentioned of going into commodity trading.

Can someone please explain the advantages/disadvantages of this Demerger?

I think we would receive shares of OCCL Ltd. in addition to current company shares but the total value of both company shares would remain same as before. Is this right?

How would demerger result in value-unlocking for shareholders?

There is systematic deworsefication by management in investment business,1st there was VC investment in Startups, now commodity trading.

Management is considering IS business as cash cow, gave guidance of OPM in 30-32% region. Now when, margins have been challenged, we don’t see focus on protecting the bottom line.

Overall i see OCCL on loosing stream in medium term due to:

Surplus IS capacity globally

Inability to protect margins

Deworsification in unrelated areas.

Furthermore, i find this too much of structure in a 700 cr company

Disc. Was invested to long term (10% of PF since 2017), sold 50% last year due to diversion in investment business. Sold 50% yesterday morning at 780. Hence negative bias.

With the demerger announcement and the recent market fall in prices, what impact do you see on ur earlier thesis. Few observations on biz and demerger :-

The subsidary Duncan Engg will remain part of holding investment company

Per recent concall, mgmt mentioned that the cost to put up Greenfield plant is arnd 3 L\ton. That brings replacement value itself at 1000 crs.

Thr was a mention of continuing with the 50% dividend policy. Now, I am not sure, but my guess is that this is from the Chemicals biz only so further cash can be funneled for investment company

Do let us know ur updated views.

Disclosure :- Not invested. Came across this only as a demerger play.

the thesis based on which i had invested is solely on the IS business.

While i have already expanded on the business in the post above, this demerger does not change my thesis which in short is -

a. overcapacity in the industry compressing realizations for all players.

b. OCCL, with its scale, will come out stronger.

c. the industry seems to have entered a phase where no new capacity will be coming in for the next 3 years.

d. this overcapacity co incides with slump in global CV movement (refer Eastman CEO comments in my post above)

c. the recent fall in price was more on account of margin compression, which ought to reduce once pass throughs kick in.

the way i see it, many things that could wrong for OCCL, already have and are baked in the price.

uptick in CV → increase in IS prices → better cashflows.

they should not have put money in all of these exotic instruments. at this price, i can live with it (surprisingly, those investments have done well). hopefully, after the demerger, all the cap table fun will be in a diff company.

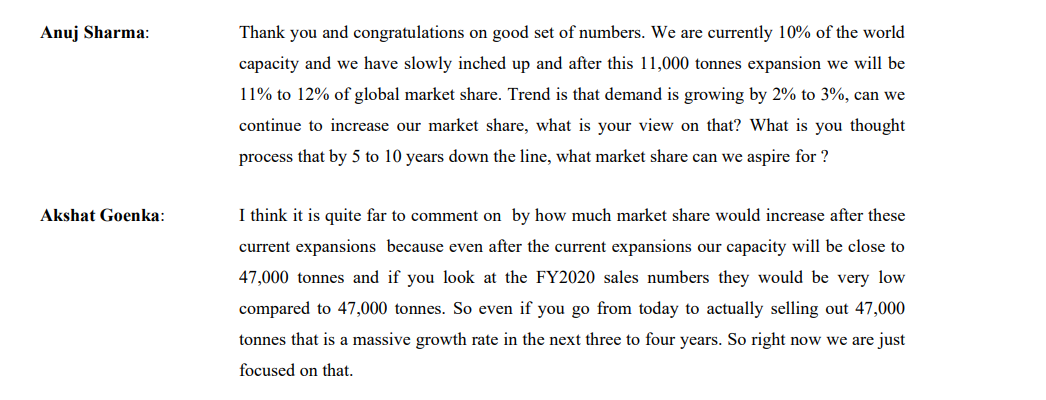

The big red flag is inability to increase market share beyond 10-12% globally since last few years. The company is looking to grow with new capacity in North America. But why have not they increased market share as they were not operating at 70% capacity(from prev quarterly concalls).

Either the existing customers has capped quantities per supplier or the nature of the product is such that beyond a certain grade, would not really improve the cost side for the customer.

This could have been the best time to gain market share in international markets where demand has been flat. Future growth can be a function of overall demand improvement rather than gain in market share.

“Going forward we expect our long term EBITDA margins to be in the range of 28% to 32%”

Forward to q2fy23 concall, management says EBITDA margins vary relative to sales. EBITDA margin per ton is what their focus is on. One more clarity given is the company sells by having fixed rupee over fixed costs than a % of fixed costs. so if fixed costs come down, ebitda margin as a % of sales go up.

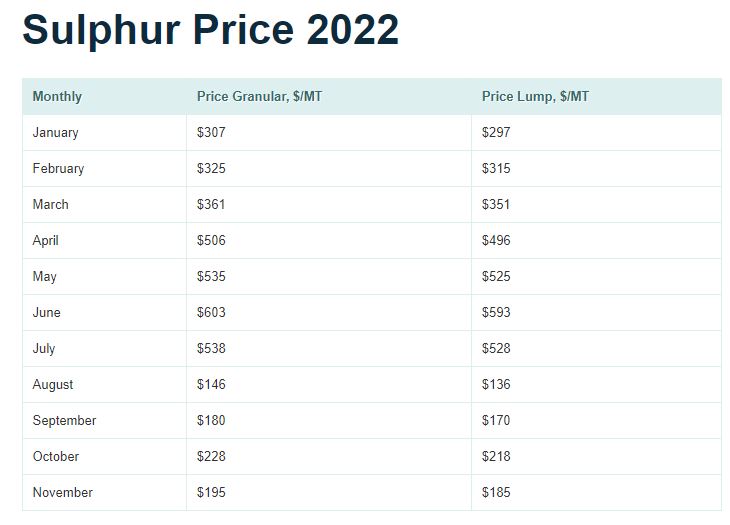

So in 2021 concall CFO might have not factored in the sharp rise of RM & freight costs that came later.

raw suplur prices rose up sharply and have now collpased … now margin might easily hit 30% as the pass through kickes in … but lower demand from west might be dampner…