yes… but still 3.41% remains… which clearly states may be liquidated for needful of funds.

1 Like

Key development in Insoluble Sulphur business, Eastman Chemical Company having 65% of the global Insoluble Sulphur’s market share has sold it’s Tire Additives business to a PE firm.

See below:

Eastman would be focusing more on innovative products. Key point for us OCCL share holders to note is valuation of the deal. While valuation has not been declared in the sale proceeds, on deeper digging i found something.

On the day of declaration Eastman’s CFO had a call with Deutsche Bank & this point came up in opening dialogue.

https://www.eastman.com/Company/investors/Events_Presentations/Documents/EMN-USQ-Transcript-2021-06-09.pdf

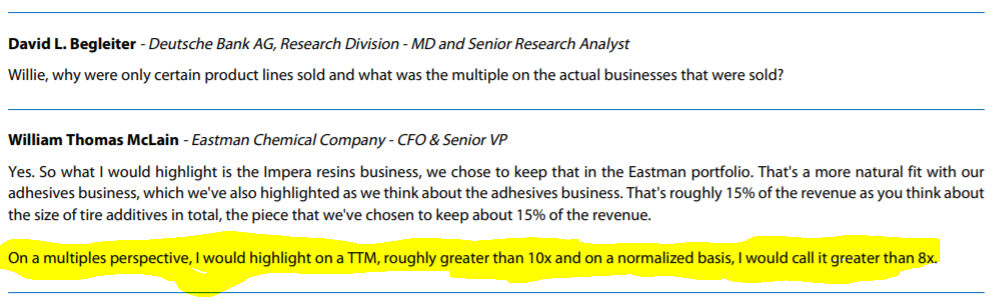

See below:

Key point here is valuation, let’s take 10x as base price then clearly current valuations of OCCL at 17x that to including commodity chemical business are frothy.

Invite views from other members.

Disc: Invested, 6% of portfolio

7 Likes

Normalize the EBITDA. Take into account the growth from capex coming onstream in July. Bake in the fact that OCCL has a 60% market share in India where tire industry is growing given radialization having a larger impact on indian market plus ADD on Chinese tires. Also the 17x you are referring to is OCCL PE and the CFO is talking about a EV/EBITDA multiple

8 Likes

You have a point Riddhesh

Didn’t realised that they value business on EV/EBITDA for such deals.

Let’s revisit valuations post Q4’21 results

All the best

1 Like

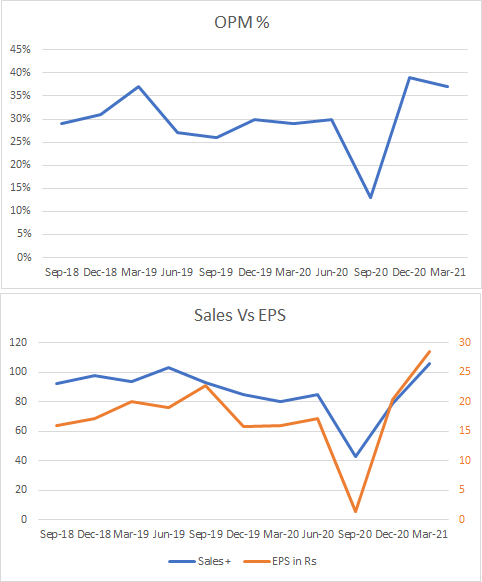

In 4QFY21 Co. Reported:

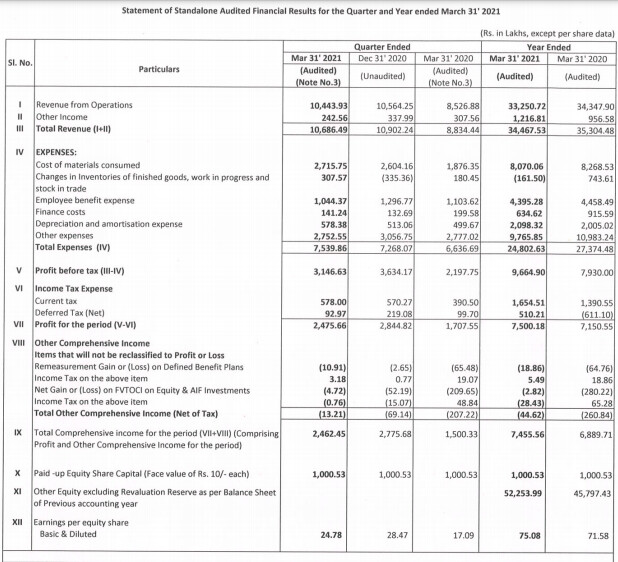

Total Income: 107cr

Ebitda income: 38.7cr

Ebitda Margin: 36.2%

Commentary: New announcements on tyre capacity expansions by various

companies will drive demand for insoluble sulphur.

Company have recommended a final dividend of Rs. 10 per equity share of Rs.10/- each.

Capex is facing delay and expect Phase- 1 of 5,500 TPA insoluble

sulphur line and 42,000 TPA sulphuric acid line in Dharuhera {Haryana) to be commissioned by Oct-21.

Disc: Invested from lower levels

3 Likes

Looks good, but there has been a run up in the last year of more then 50%. Will the market continue rewarding?

2 Likes

Was waiting for Q4 Concal to do the valuations. Pl find the link below of the conal:

Strong Qualitative patterns are emerging from commentary basis Q3 & Q4’s concals. Upcoming Annual report would be interesting document to evaluate for this story.

Key points:

-

Management has done upward revision of guidance in EBITA margins to 28-32%. Basis the trends, even 34-35% is also possible, seems management would like to under commit & over deliver

-

Surprising, less homework done by management of Eastman’s sale. Since valuations were not declared as part of the deal, they did internal calculations & estimated this to be 6-7 times of EBITA while it is 10. They should have done some Google search instead of guess estimating (refer to my earlier post, Eastman’s CFO had shared the valuation in an unrelated interview).

-

Revenue addition post brownfield phase 1 & 2 would be approx 165 crores. Ref concal this capacity can come at the earliest in Mar. 2023. Let’s consider FY 25 as having full year with additional capacity.

-

Further Brownfield expansion is not possible & management feels Greenfield expansion shall not give any payback. This point has been re-emphasised number of times. i shall need some finance lessons to understand, how come at 30% EBITA margin, a greenfield doesn’t give pay back? Govt schemes in this regard needs close observation otherwise this is a spoke in OCCL’s growth wheel.

-

This would mean that FY 25 onwards OCCL shall become cash generating machine with challenges of capital allocation. Management has made it clear that they shall not like to invest in unrelated field. Current fireside investments needs separate review, should be able to do post AR issuance.

-

Prices of raw materials are increasing & shall be passed on to customers.

-

Would like to simple valuation of OCCL on terminal value in FY 25 using the matrix of EV/EBITA (taking cue from Eastman’s deal). Here we go:

a. Bull Case Scenario:

20% Revenue growth from base of FY19 (lower capacity utilisation in FY20 & 21 due to Covid) & Price increase of 20% + 165 crore from new capacity.

Total Revenue : 770 crores

EBITA Margin : 34%

EBITA : 262 crores

Multiples : 12 times EBITA considering market potential in India

Other investments : 200 crores (includes Duncan Engg.+inv in 2020-21+ future cash flow)

Valuation : Rs. 3344 crores

b. Base Case Scenario

20% Revenue growth from base of FY21 and Price increase of 10% + 165 crore from new capacity.

Total Revenue : 651 crores

EBITA Margin : 31%

EBITA : 262 crores

Multiples : 10 times EBITA, same as for Eastman

Other investments : 150 crores (includes Duncan Engg.+inv in 2020-21+ future cash flow)

Valuation : Rs. 2168 crores

b. Bear Case Scenario

20% Revenue growth from base of FY21 including Price increase + 165 crore from new capacity.

Total Revenue : 614 crores

EBITA Margin : 28%

EBITA : 172 crores

Multiples : 10 times EBITA, same as for Eastman

Other investments : 150 crores (includes Duncan Engg.+inv in 2020-21+ future cash flow)

Valuation : Rs. 1870 crores

Key point to observe would be how management does the capital allocation & creates shareholders value. Focus on operational excellence, persuasion with new customers can create lot of wealth. During FY’21 60 crores has been invested in non-core businesses. Instead of such allocations, diversion of funds to share buy backs would create substantial value for shareholders.

Looking forward for inputs to shape up long term view on OCCL

Disc. Invested at lower levels. First time tried to do such valuation on VP.

11 Likes

Let think this way

As mentioned by the management a line of 5500 MT can genrate revenue of Rs 70 cr. So with optimal utilization maximum revenue possibillity would be :

70/5500*45000=570 crs + New Sulphuric Acid plant 25 Cr, so total comes to around 600 crs. If we add another 60-70 crs for Duncan then it comes to 650-670 crs range to be maximum revenue on consolidated basis.

yes, that is in base case scenario

Have attented the concall on 23rd June. What are your thoughts on the company making a move to invest 20% of Networth of the company into investments rather than increasing the reward to share holders or even planning to move into newer value added products ?

OCCL

Planned capex of Rs 2.16 bn - to increase IS capacity by 11,000 MTPA

-

OCCL is incrementally enjoying a favourable market positioning as the „Second Alternate Supplier‟ in global markets, particularly in the West. The Company is increasing it‟s IS and Sulfuric Acid capacity by 11,000 MTPA and 42,000 MTPA respectively at Dharuhera. The total capex is estimated at ~Rs 2.16 bn, of which IS expansion is estimated at ~Rs 1.83 bn, funded through a mix of debt and internal accruals of 2:1. IS expansion comprises two equal phases of 5,500 MTPA each.

-

With COVID outbreak, Phase-I has been delayed due to suspension of civil work and labour availability issues faced by the Company. With this delay, Phase-I capacity of IS and the entire capacity of Sulphuric Acid is expected to get commissioned in October 2021 (earlier expected by the end of July 2021). The Company will undertake Phase-II expansion, after commissioning of Phase-I, depending on automotive market conditions.

2 Likes

Hi @srikanth767

There are 3 aspects to your point & unfortunately all 3 are pain points:

1. Management lacks long term vision, where they want to take OCCL beyond 5 years? They were clueless/ struggling to answer, when analysts raised this point in last concal.

2. Lack of Innovation, as per one of the studies global market of IS is growing @3% p.a., post expansion by China Sunsine & OCCL there is going to be enough supply to cater the demand of many years. Such situations require innovative managements to explore/ venture in related chemicals. In ARs of last few years we hardly see any serious effort to optimise cost of production.

Disc.: Coming from manufacturing background, i could quickly evaluate their initiatives on operational excellence.

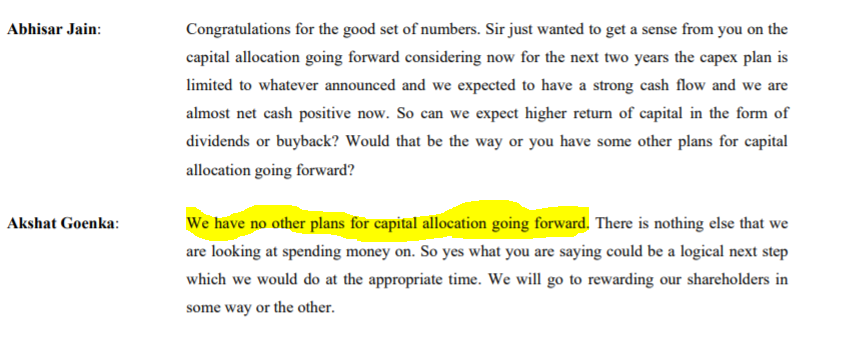

3. Capital Miss-allocation Before we go forward pl see following snip from Concal Q3’21

You would have heard the contradiction in Q4’21’s concal.

Basis the track record of management, am not raising Red flag on their integrity, but post observing this behavior, am getting convinced that they lack long term vision.

Disc. Invested.

1 Like

Thanks for the valuable information.

But could this be an instance of promoters trying to siphon out minority shareholder’s funds? I’ve noticed this happen with other companies where they are big fish in a small pond like OCCL. Were there any red flags against the management earlier?

I’ve been only researching this company for the last 6 months. Apologies if the question is too extreme.

Haven’t seen Red flag regarding Management’s Integrity in the past.

To me, this seems to be the case of complacency & competency than of integrity.

2 Likes

Annual report issued, shall cover 2 key aspects from this report.

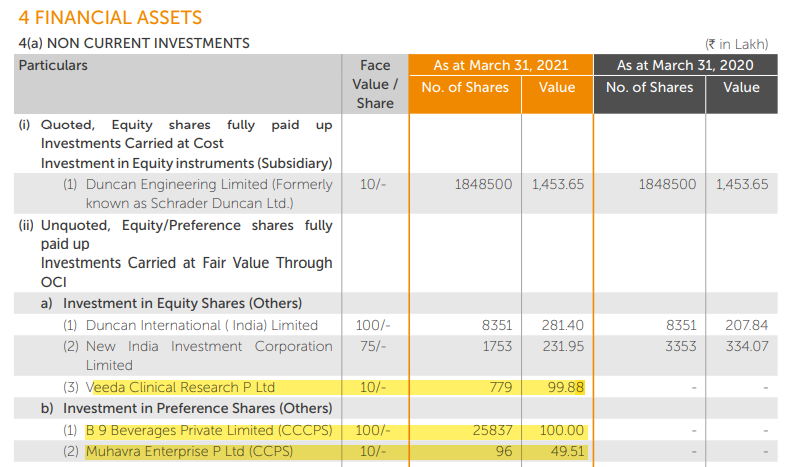

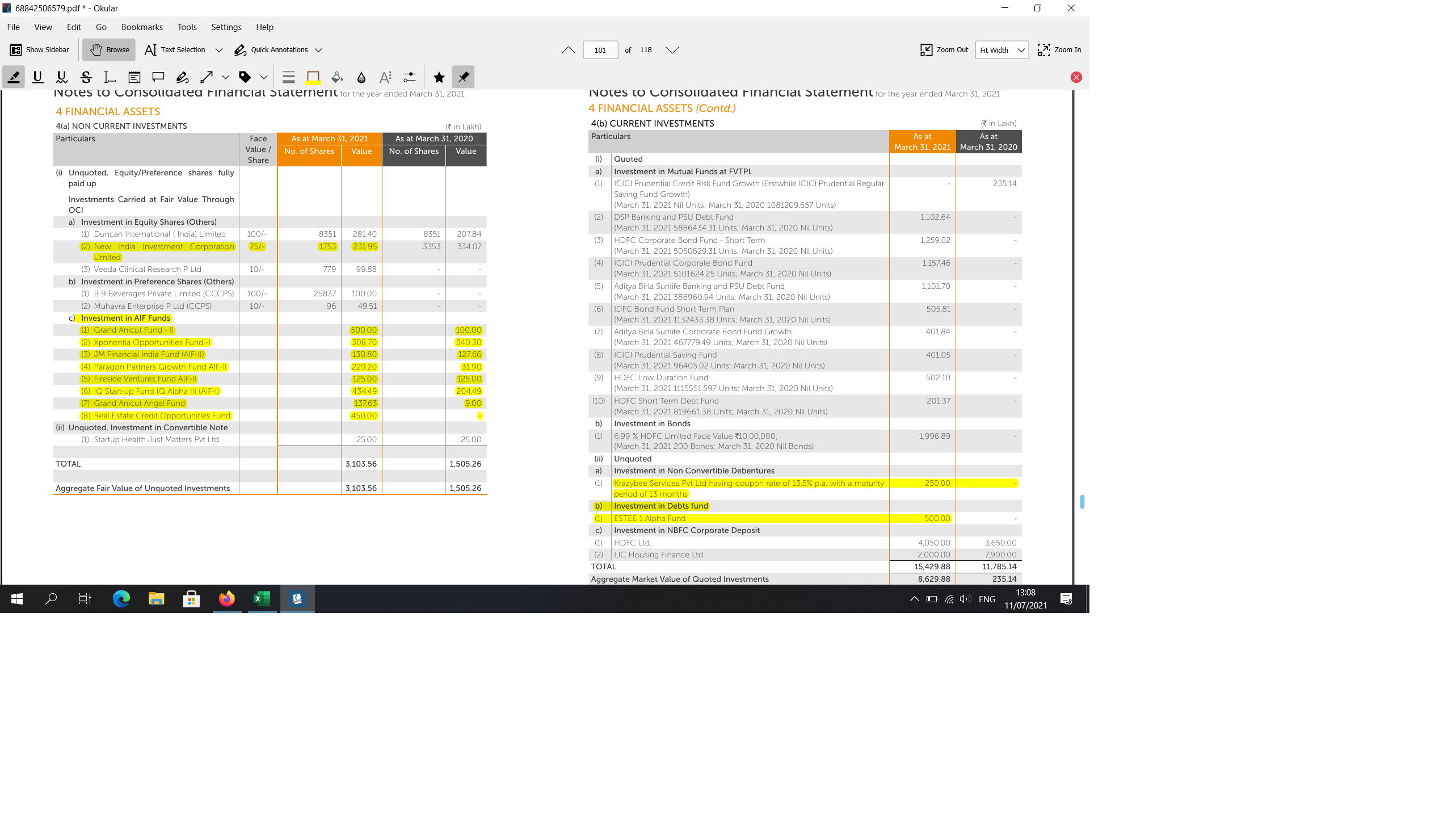

1. Investments :

Finally, we came to know, where all the investments have been made. Found the same on page 140 (72 in pdf), 3 new investments have been made in start up world:

Out of these:

Veeda is Ahmedabad bases CRO, might get benefited by ongoing traction in this space

B9 Beverages is BIRA Beer

Muhavra is an e-commerce player, servicing in Coffee beans, Coffee Grinders & Blenders through Amazon etc.

My Opinion: while quality of investments seem good, these all are in unrelated fields. Questions must be asked from management in AGM. This must be raised as Red Flag to emphasise focus of the management on Core business.

Other investments:

- Total investments through AIFs has increased from 29.6 Cr to 45.6 Cr.

- Current investments in Debt Mutual funds & Corporate deposits has increased from 117.9 to 153.3 Cr.

Key point : As OCCL is becoming a cash generating machine, we remain concerned about Capital allocation strategy.

- Competitive Moat:

OOCL has aspired to increase their Global share from 10 to 12%. This is a welcome move. As per my scuttle butt analysis : to do this they can have 3 competitive moats viz. Low Cost Producer, Quality, Lower carbon foot prints. Good thing is, AR is covering 3 aspects in different aspects.

Lower cost producer: There are references to Operational Excellences initiatives. This should help the company. Important point to mention here in is that China Sunshine’s upcoming plant is fully integrated & shall put substantial pressure on the margins in case other 2 moats are not leveraged.

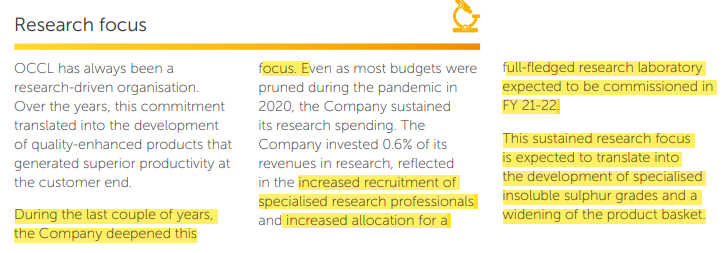

Quality : IS supplier needs to keep innovating & renovating their products to meet growing demand of customers. This has become more relevant today with higher demand of low energy consuming tyres. OCCL has recognised this as aspect. Ref. Research Focus, in the AR resources in terms of manpower & upcoming research lab should add value.

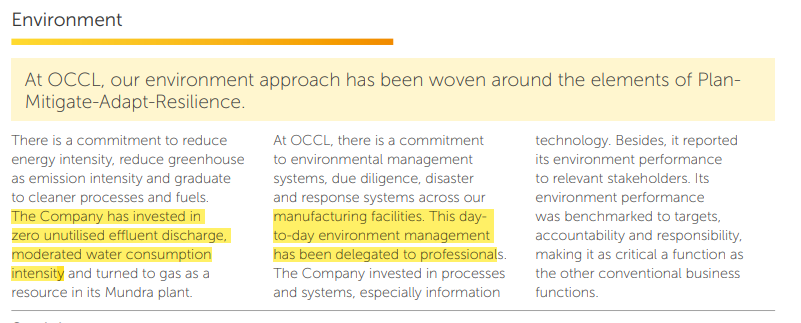

Environment :

Tyre companies are under pressure for being Environment Unfriendly. Big players are striving hard to reduce their carbon foot prints. In short term customer can give additional cost to save on Carbon Foot prints. We see that OCCL has hired professionals & is putting up the focus.

In nutshell : Overall good report except distraction of investments

Disc. : Invested , tracking closely

10 Likes

In addition, investments in AIFs have increased from INR 9.38 crore in March 2020 to INR 23.15 crore in March 2021 (increase of approx. INR 14 crore). Also, in 2021, they have invested INR 5 crore in Estee I-Alpha Fund which is a hedge fund (Link: Estee Funds) and INR 2.5 crore in the NCDs of Krazybee Services which is an unsecured personal loan provider (Link: Krazy Bee

In my view, capex can be easily funded from internal accruals (company has current investments of INR 154 crore) instead of using those towards unrelated investments in AIFs, hedge funds, NCDs, and start-ups and leveraging the company (total debt as on March 31, 2021 was INR 179 crore (page 181 of the Annual Report)).

3 Likes

OCCL AR 2021Notes

Company is one of a handful of global manufacturers of insoluble sulphur, a key raw material for tyres manufactured through a sophisticated process. Apart from this product, the Company manufactures sulphuric acid and oleum in its Dharuhera plant.

- Company possesses state-of-the-art manufacturing facilities in Dharuhera (Haryana) and Mundra (Gujarat). Manufacturing operations commenced with a modest capacity of 3000 MT per annum in 1995, which has since grown to an aggregated 34,000 MT per annum. The Company also possesses a capacity of 46,000 MTPA for the manufacture of sulphuric acid and oleums.

- In addition to the manufacture of insoluble sulphur and sulphuric acid, the Company owns a majority stake in Duncan Engineering Ltd. (formerly Schrader Duncan Ltd). This company is a leading four-decade manufacturer of pneumatic products and accessories trusted for reliability and customisation

- Capex

- In 2019 started brownfield expansion of an additional 11,000 MTPA of Insoluble Sulphur capacity at Dharuhera in two phases.

- It will complete phase one of its major capex cycle related to the Dharuhera expansion by October 2021.

- In the first phase, the Company intends to expand capacity by 5,500 MTPA of insoluble sulphur and 41,250 MTPA of sulphuric acid by the third quarter of the current financial year.

- In the second phase, the Company intends to raise its insoluble sulphur capacity by another 5,500 MTPA.

- Company’s Rs. 215 Crore capex cycle – with hardly Rs. 60 Crore of its investment in-the second phase left is likely to be completed by 2023

- First phase will potentially increase the Company’s global insoluble sulphur market share about 10% to 12%

- Company invested in world-class research infrastructure that will be commissioned in FY 21-22.

- The Company is likely to experience peak debt in the first half of the current financial year, following which a structured repayment programme could moderate debt sizably leading to the possibility of free cash generation across the foreseeable future

- by selecting to invest during the down cycle, possibly one of only two such instances in the world at this juncture, the Company intends to emerge opportunity-ready – not just larger but stronger as well

- Along with the Capacity Expansion of Insoluble Sulphur, the Company is also expanding Sulphuric Acid capacity mainly with the view of providing steam for the new Insoluble Sulphur lines.

-

Capacity as on 31.03.2021

- Insoluble Sulphur:

Dharuhera (Haryana): 12000 MT

SEZ Mundra (Gujarat): 22000 MT

Total: 34000 MT - Sulphuric Acid/Oleum: 46000 MT at Dharuhera (Haryana).

- Insoluble Sulphur:

- The Company’s principal brand - Diamond Sulf – for insoluble sulphur is synonymous with world-class quality, helping downstream customers succeed in their journey for excellence.

- The Company’s products are EU-REACH-compliant. Besides, the Company’s facilities and processes have been certified for IATF16949, ISO 9001, ISO 14001 and ISO45001, enhancing customer confidence.

- In FY 20-21, the Company generated more than 90% of its revenues from insoluble sulphur customers of five years or more, a trend likely to sustain.

- Company showcased from the second half of FY 19-20 with the objective to moderate costs even before the insoluble sulphur sector had slowed or the pandemic had brought the global economy to a standstill. I am pleased to communicate that as a result of proactive urgency, we right-sized our Profit & Loss – using the same quantum of resources across an expanded capacity – whose visible impact will become evident from FY 21-22 onwards.

- We are cautiously optimistic of prospects as some of our customers, who approved our products for use in Thailand, India and Europe, are now providing approvals to our products for use in North America. We believe that by sweating these long-standing relationships better, we stand to enhance our revenues across the foreseeable future.

- We also believe that a number of insoluble sulphur customers, already buying a large quantity from China, will seek to broadbase their procurement from non-China countries like India, benefiting companies like ours.

- OCCL demonstrated its competitiveness by breaking even at a mere 40% capacity utilisation during the first quarter. From the second quarter onwards, the Company was required to increase output. OCCL reported peak revenues during the third quarter, 33% higher than the revenues reported during the corresponding quarter of the previous financial year. With sales reaching 95% of capacity; the Company reported its best quarter by PAT in Q3 FY 20-21 and its best quarter by margins in Q3 FY 20- 21. This performance could not be extended into the last quarter following a sharp increase in raw material costs.

- Company expects to report EBITDA margins between 28 and 32% across the foreseeable future based on the existing realities.

- OCCL intends to focus on increasing its market share in North America to 10% in three years. The Company intends to increase global market share from 10% to 12%. The Company intends to sustain the increased share of Indian revenues at 40% across the foreseeable future

- Indian market share of insoluble sulphur at ~60%. Global market share of ~10%

- During the year under review, Europe and India were the two major markets of the Company, accounting for more than 60% of the Company’s revenues. Over the years, the Company focused on reducing its dependence on Europe (where the market has been flat) in favour of growing markets like US, Latin America and South East Asia.

- No country (except India) accounted for more than 10% of the Company’s revenues in FY 20-21.

- OCCL added 17 new customers.

- Increased the share of value added products to more than 40%.

- Total forex earned at Rs. 172 cr and forex used at rs. 8 cr.

- Strategic framework

- OCCL is among the most competitive insoluble sulphur manufacturing companies in the world (even while it is not necessarily the largest).

- The Company possesses proprietary manufacturing technology in a sector where this knowledge is guarded among half a dozen manufacturers. The time and effort an intending competitor could consume to develop such a proprietary technology could be so long that after having stabilised production, it could take perhaps twice the number of years to get the product approved by demanding customers and recoup investments

- Besides, the quality standards among downstream tyre companies are rising all the time; the acceptable benchmark of yesterday becomes redundant a few years later. Customers take years to approve vendors prior to initial engagement; purchases are only progressively scaled; the quality derived out of each successive capacity expansion needs to be approved all over again by the customer.

- The business is capitalintensive, marked by a capital: turnover ratio of 1:1, deterring fresh industry entry

- OCCL is an employer of more than 450 people (full time and contractual) across its two facilities

- The global demand of insoluble sulphur was estimated at about 273KMT in 2020; demand in India was placed at about 17KMT. Other major players in the global Insoluble Sulphur market comprised Eastman (USA), Shikoku Chemicals (Japan) and Sunshine (China).

- Contributions from Sulphuric acid are expected to be under pressure going forward as two more plants of Sulphuric Acid (with combined additional capacity of about 250 MTPD) are expected to be commissioned during the year in North India. However, there might be some respite due to expected robust demand in the fertilizer sector and prevailing high international prices.

- the global insoluble sulphur market size is projected to reach USD 1.2 Billion by 2027 registering a CAGR of 2.9%. The sulphuric acid market is projected to grow at a CAGR of 3% between 2020 and 2025. (Source: Mordor Intelligence).

- The Company was audited by Eco Valdis for three successive years, including a Gold rating, strengthening its marketing pitch in an increasingly sensitised world.

27 Likes

Thanks, @harshitgoel for the highlights. Do we have any information available, how much sales growth the 17 new customers can contribute?