Thanks a lot!! Never knew about this site before.

1 Like

Hello,

This thread has been incredibly helpful.

I have a question.

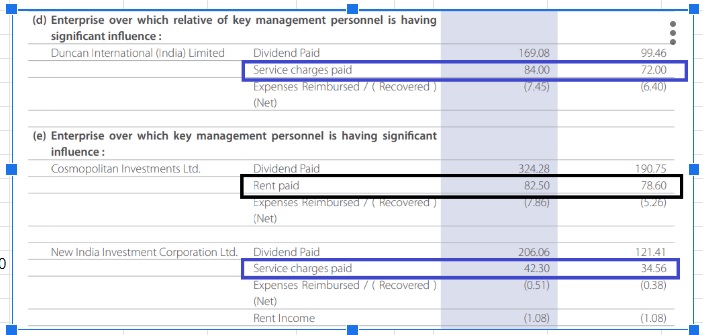

There are unexplained services charges of 1.26 cr in FY22 (and 1.07 cr in FY21) to Duncan International (India) and New India Investment Corp, which are promoter entities.

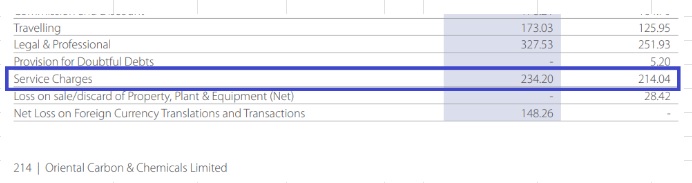

There is an additional annual service charge of 1.08 cr, which is embedded in the highlighted line item below.

These service charges make up 1.7% and 2.1% of other expenses (and 0.6% of sales) in FY22 and FY21. These service charges are present in prior ARs as well.

Question: Does anybody know what these charges are for ? Dividends to these entities make sense, but couldn’t find any info on these charges. I can try my luck and write to the company, but thought of checking with this community first.

Btw, in addition there are miscellaneous expenses, which make up 1.8% and 2.0% of Sales in FY22 and FY2 , respectively. They could itemize this and provide some detail given these are not very small numbers. Anyways, any info re: service charges would really be appreciated.

Thanks,

Gautam

2 Likes

It looks like Aug 2 is the final hearing for NCLT approval : https://www.bseindia.com/xml-data/corpfiling/AttachLive/5eb0df2a-40cc-4b61-b8db-579f635d9801.pdf

1 Like

This stock is really trying patience, lately I was studying about the sulphuric acid which OCCL has added capacity. Sulphuric acid is also used for

The sulphuric acid used in the production of aluminium fluoride is a byproduct of the sulphuric acid production process. The sulphuric acid production process involves the burning of sulphur to produce sulphur dioxide, which is then reacted with water to produce sulphuric acid.

The sulphuric acid used in the production of aluminium fluoride is a high-purity grade, as it must be free of impurities that could contaminate the aluminium fluoride. The sulphuric acid is also a concentrated grade, as it must be able to dissolve the aluminium fluoride in the water.

The sulphuric acid used in the production of aluminium fluoride is a hazardous material, as it is corrosive and can cause burns. The sulphuric acid must be handled and stored carefully to prevent accidents.

presently sulphuric acid is imported to reduce the import dependency and rise in production capacities of Steel and other sectors where energy is required at higher temp, aluminium fluroride is required to

- reduce cost

- improve efficiency

- high grade product

questions :

- what is the total capacity OCCL is coming up for H2SO4 ?

- projections basis additional capacities ?

- More Views and News on OCCL !!

**Invested & Portfolio stock

3 Likes

Sulphuric Acid is a byproduct of IS manf & is a commodity chemical.

Background

Oriental Carbon and Chemical Limited’s (OCCL) primary business is focused on producing insoluble Sulphur which is a specialty chemical used as a vulcanizing agent to make rubber stronger and more elastic. The largest use of insoluble Sulphur is in the production of tires. OCCL’s market cap on 1st August 2023 is approximately $100M (8 billion INR) with approximately 80% of it constituting tangible book value.

Outside of China, there are only three large producers of insoluble Sulphur – Eastman Chemicals (70% market share which has sold its tire additive business to a private equity firm for $800M in 2021), Shikoku (15% market share) and OCCL (10% market share). Of these three, OCCL is the only pure play on insoluble Sulphur. Chinese production has typically been consumed within China.

Business drivers

86% of OCCL’s revenues stem from insoluble Sulphur with the remaining coming from byproducts like sulphuric acid and oleum. Of the total revenue of insoluble Sulphur, 50% comes from international consumers. OCCL is the sole manufacturer of insoluble Sulphur in India with about 50-60% of domestic market share and 10% of the global market share (mostly focused on India and Europe but growing in the USA as well). Insoluble Sulphur is approximately 2% of the cost of tires. While the tire market has many players and is fragmented, the market for insoluble Sulphur is highly concentrated. Overall, in the world and specially withing India, the number of kilometers driven per capita is bound to increase, and thus the market for OCCL is going to grow.

The key business drivers affecting the demand of insoluble Sulphur are the replacement market which is about 70% of the tire demand and commercial vehicles which consume approximately 10 times the amount of insoluble Sulphur as passenger vehicles. Typically tire manufactures enter into a five-year contract or longer with a supplier of insoluble Sulphur and thus the barriers to entry for competition are high. Moreover, the standards for insoluble Sulphur are consistently increasing, thus making it hard for new players to enter the space.

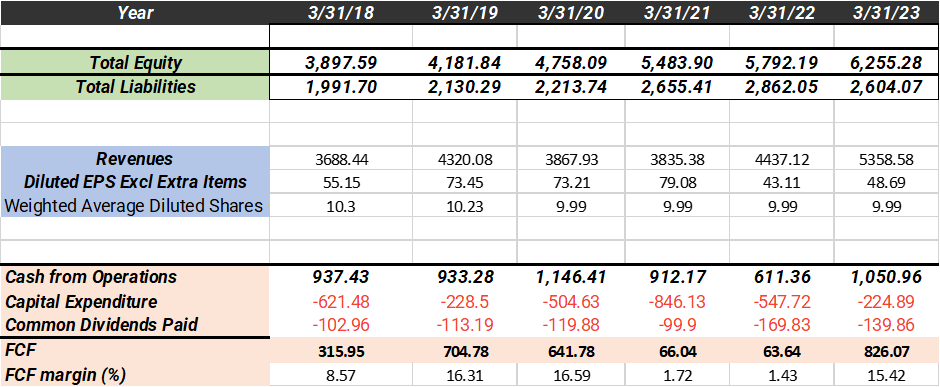

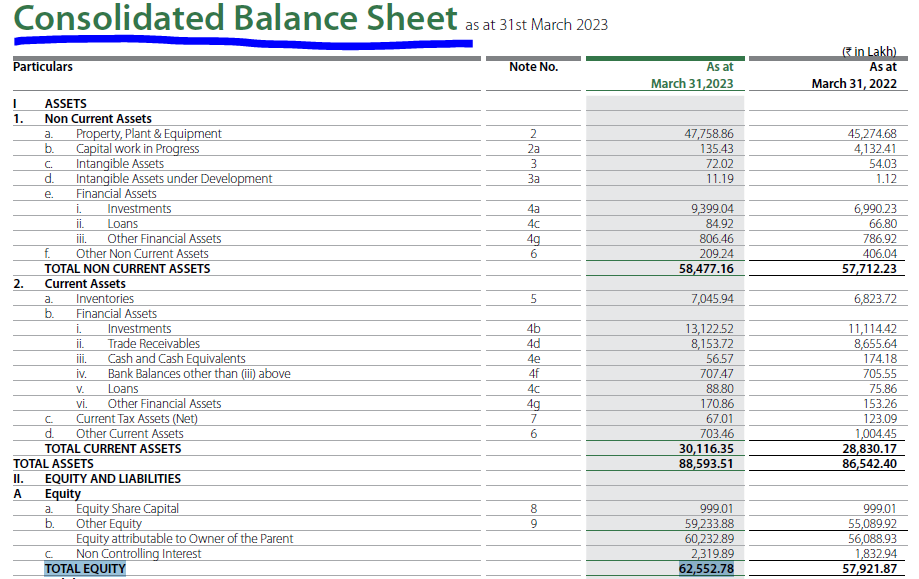

Analysis of Financial Statements

Table 1: Key metrics from financial statements in millions INR over the past five years.

With a market cap of INR 8000 million, the tangible book value is INR 6255 million and there is a healthy five-year equity growth rate of nearly 10% per annum. EPS growth rate has been low because of high input costs (Sulphur, coating oil – these are byproducts of oil refining and OCCL competes with fertilizer manufacturers for these raw materials), high freight costs and high costs of energy in 2022-23. This has also pulled down the ROIC by several percentage points in 2023 to 10% (five-year average is 14%). Total debt levels are reasonable at six times average five-year FCF of which long term liabilities are just INR 800 million. Dividends are sustainable at only 32% of five-year FCF. EV to EBIT is 11.4 in 2023 but this is with subdued earnings owing to high input, freight and energy costs.

On a ten-year DCF basis, using FCF as the input, and assuming conservative growth rates (10% and 7% for the first 5 and last five years with a historical PE of 15), the stock is currently priced for 8.3% return.

Table 2: A DCF valuation for normal, best case and worst-case scenarios using FCF as input.

Investment thesis

While a specialty chemical with several barriers to entry, insoluble Sulphur has the characteristics of a niche commodity. OCCL has a strong balance sheet but only mediocre ROIC and needs continuous capex (despite that typical FCF margins are 15%). There is a large and growing opportunity in India where OCCL does have an advantage in terms of lower freight costs for the finished product. To have a good margin of safety, a good entry price would be close to book value to minimize downside risks and leaving just the upside which can be a 2x. For now, wait for a 20% decrease in price to buy.

Company news

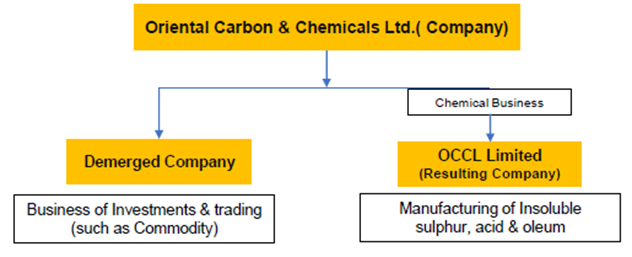

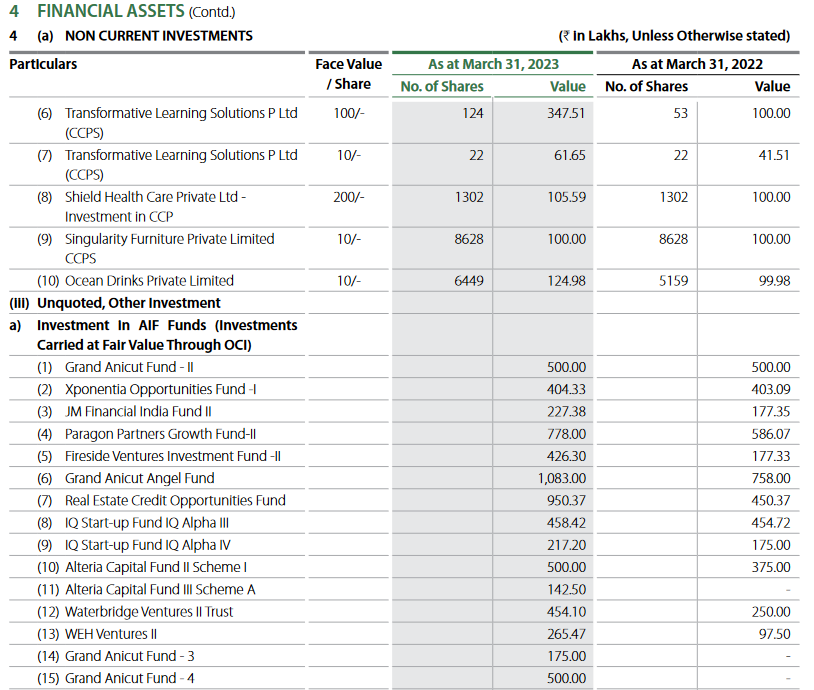

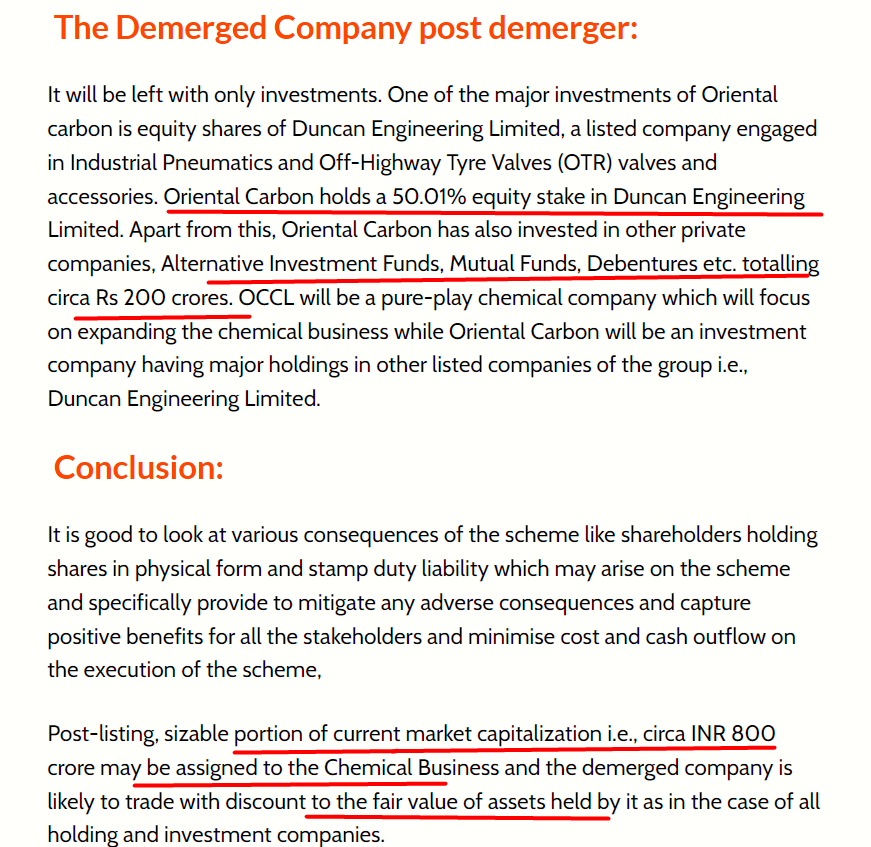

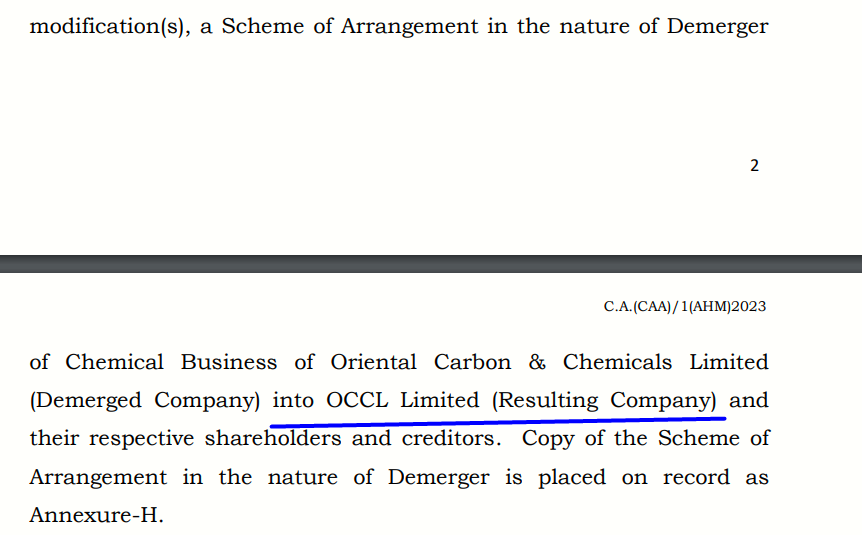

OCCL over the last few years has invested in unrelated companies (VC style) with approximately 12.5% of market cap held in these instruments. While these investments have been successful so far, there is a risk of deworsification. However, the company had announced a demerger with the chemical business (cash cow) separating from the rest. This is expected to materialize in 2023.

Catalyst

A lot of bad news is already baked into the price. Both the demerger and the normalization of input, freight and energy costs (or even one of them) will improve margins and EPS. The tangible book value provides a floor for price. If purchased close to book value, this is a good risk reward play.

** Invested

15 Likes

ppt

1 Like

summary of the bullet points from the company’s concall transcript:

Revenue and Financials:

- Q1 FY24 revenues declined by 20% due to lower sales of insoluble sulphur and correction in sales prices of sulphur and acid.

- EBITDA grew by 15% and profit after tax increased by 9% for the same period.

- Margins improved due to correction in international freight costs and reduction in sulphur prices.

- The company is debt-free and has a positive net cash position.

Industry Outlook:

- CV industry expected to grow mid- to high single digit in FY24, driven by promising monsoon and government efforts to boost infrastructure.

- Indian tyre manufacturers anticipate investing INR 5,000 crores in FY23 and FY24, driven by strong demand for radial tires in the domestic market.

- Demand weakness in Europe attributed to inventory correction and challenges faced by European tyre companies.

- OCCL’s market share expected to increase with additional orders and evolving trends in the tyre industry, including the growth of electric vehicles.

Expansion and Market Share:

- OCCL focused on expanding in geographies like North America and increasing market share in India.

- Current capacity utilization for insoluble sulphur below optimum levels, but additional orders expected next year to utilize expanded capacity.

- Demerger proposed by OCCL awaiting approval from NCLT, with next hearing scheduled for October 11, 2023.

Guidance and Demand:

- Company does not provide specific guidance on margins or volumes due to various factors affecting costs and demand.

- Demand for insoluble sulphur expected to grow between 3% to 4% on a long-term basis.

8 Likes

How your calculating tangible book value, can u guide how to get this

Just use the balance sheet to check the total equity and subtract out any goodwill to get tangible book value.

2 Likes

https://nclt.gov.in/case-details?bench=YWhtZWRhYmFk&filing_no=MjQwMTEwNTAxOTg5MjAyMg==

NCLT disposed the case in May '23. What more needs to happen for the demerger to go through? @R_J

Disc.: invested

Update based on Nov 2023 con-call

- Revenue lower because of sluggish Europe, lower costs of raw materials.

- Equal profits even with lower revenues because of lower raw materials.

- Keep in mind, 50% of the sales are outside of India

- Contracts a are 3,6 and 12-month basis so if raw material was purchased at higher prices, not all

of it can easily be passed through – basically sales prices is pre-negotiated so there is inventory

risk. - Apparently, Chinese competition has had approvals in certain areas and competition is reducing

margins. - On a half-yearly basis compared to last year freight has come down quite substantially from

around INR26.5 crores to INR9.5 crores.

2 Likes

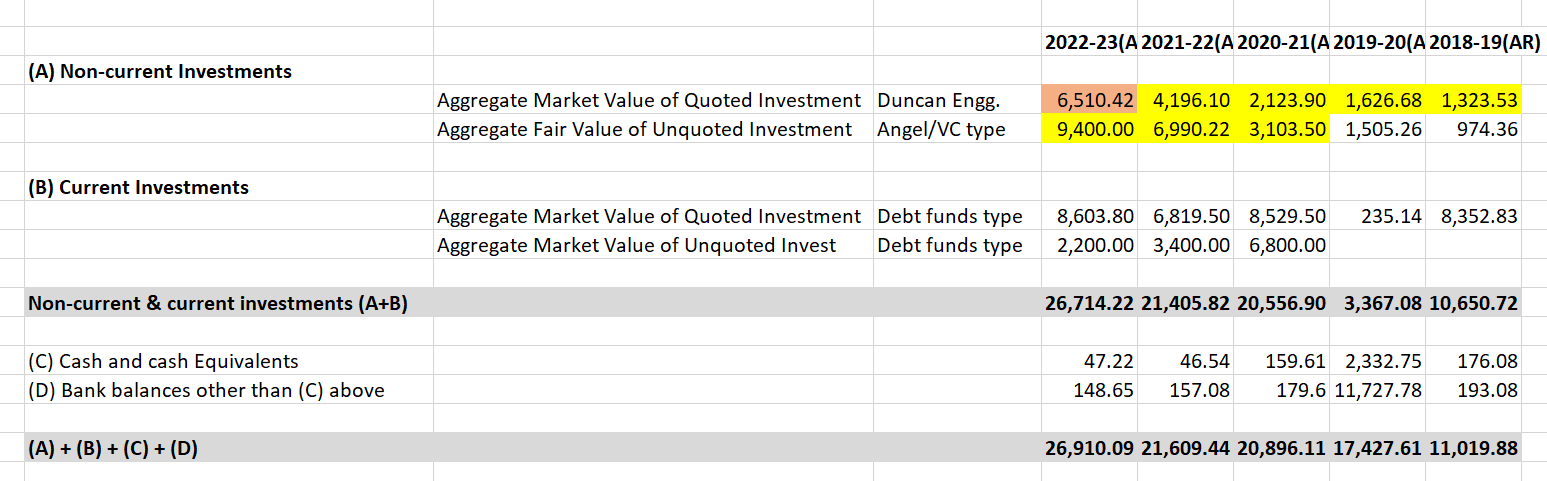

I looked at the last 5 ARs to analyze the investments made by OCCL:

- The growth between FY22 and FY23 has largely come from appreciation in the value of Duncan Engg., followed by VC-type investments

- Based on the current stock price of Duncan, the 65 cr number in FY23 should read ~75 cr

(numbers in the table below are in lakhs)

- Pretty much all VC-type/AIF-type investments are doing really well. Wingreen Farms and Bira91 are couple of names that resonate with him (strong consumer brands)

- Another interesting thing I found is that Akshat Goenka makes VC-type investments through his family office as well; pretty impressed to see that he put his money in SpaceX

https://agventures.co.in/about/

Disc.: invested

7 Likes

It seems the NCLT approval for demerger is still pending as per this new case details: https://nclt.gov.in/case-details?bench=YWhtZWRhYmFk&filing_no=MjQwMTEwNTAwOTUyMjAyMw==

The next hearing is set on 11 Jan 2024.

1 Like

Sharing con call transcript from “Oriental Carbon & Chemicals Limited

Q4 FY’23 Earnings Conference Call”

May 24, 2023

disc: invested

2 Likes

What my understanding says as per above info

Occl will become holding company , hence it should ideally trade at 0.4 price to book .

Either goes down from here (unlikely)

Or book value increases (time correction)

Folks please share views

Invested

2 Likes

Can you explain in detail, please

Bro occl hold multiple investment in unlisted space , hence the valuation of unlisted companies need to be built in the price .

What I shared is a perspective !!

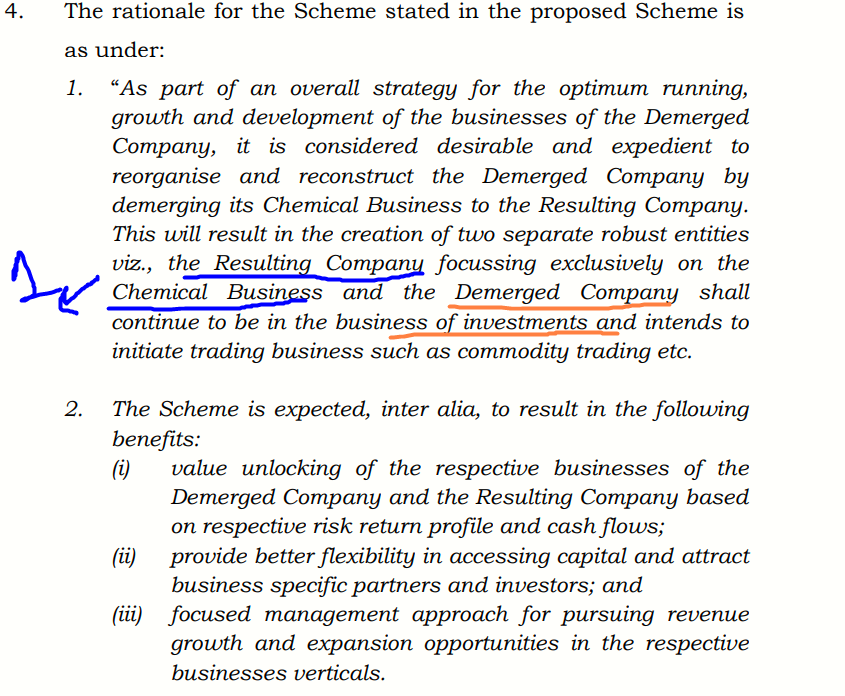

as per my understanding, the resulting company will be OCCL Ltd will be Chemical Business that’s major chunk of revenue. For Demerger Company holding company of OCCL ltd , plans are for investments commodity trading ( not shared much details )

The question is, if the OCCL Ltd is proxy to the growth potential of the Tyre industry and if there is growth comes back , could the stock be revalued? Can you assist me in verifying this?

2 Likes