Do we have more insights on this as well? This seems to have gone unanswered.

Can someone please share the initial coverage report by IIFL on OCCL in Dec’19.

Thank you

Please search on Google for the same.

But sharing the below link which is released in jan 2020.

Also adding 2 more youtube video links.

https://www.youtube.com/watch?v=_eaU1FOEtQk

Hope this will be helpful.

Regards,

Vikas

2 Likes

This looks like a Value-pick now, notwithstanding the concerns mentioned in this thread. While this and next 1-2 yrs will witness 0 to negative growth, the co. will have certain things going in its favor:-

- Reduced competitive intensity - Apart from the new capacities being put-up, none of the competitors will risk putting up new capacities for the time being

- Tire market being more resilient :- Compared to auto industry, tires have a huge replacement market as well, which might not witness comparative de-growth. And this product is a must-have for any tire company.

- Reduced risk of alternatives - Following on the (1) above, these are not the times when chances of R&D being put up to search alternatives for insol. sulphur are minimal. Thus, tires, and in-turn, Insol Sulphur will continue to have a stable, moderate demand.

7 Likes

These points were same years ago and same even now … What has changed ? So respectfully don’t console oneself.

What needs to be seen is after a decade long growth trajectory now P&L has got derailed and time to see how well market rates/derates this …

3 Likes

What has not changed - As you mentioned correctly, the above points have not changed. Isn’t that an indicator of a stable industry - less prone to disruption and irrational competition.

What has changed - 2 things -

(a) Valuation - 2 years back ppl were paying 2.5-3X revenues for this co. and praising its moat. One was paying first-class price for a not so first-class business at that time. And that lot of investors will not make\make less return in coming years. That’s true not only for OCCL bt many other cos.

(b) The comparative strength of the business : - Part of the reason for derailing P&L, as u said, was that last yr was one of the worst slowdowns of Auto industry. No doubt the company’s revenues fell but they fell less than what has been an average fall of the entire industry. You can get more details regarding this frm Co. conference calls. These sort of things happen to every company over a Business cycle. Only the ones which go thru these sufferings will emerge stronger and thrive.

Another reason for P&L suffering is the planned apex undertaken by the co.

So, if one zooms out and looks the overall picture, the business will have a tough 2-3 yrs. but has reasonably good chance of coming out stronger. Hence, the risk-reward ratio is now more favorable then, say 2-3 years back.

5 Likes

Hey guys I spent some time today understanding OCCL and had questions. Would like to hear from senior members of the group.

-

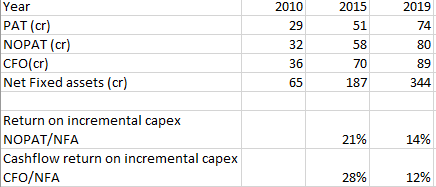

Return on incremental capex. – On standalone basis, net fixed assets grew from 65 cr in 2010 to 344 in 2019 where as NOPAT grew from 32 Cr to 80 cr. If you see the returns on incremental capex between 2010-2015 its 22% (58-32)/(187-65) but it drops down to 14% from 2015 to 2019. I thought I would look at CFO vs NFA and that dropped from 28% to 12% for similar time. My assement is, company is earning less on its incremental capex which is concerning given that company increased its margins in last decade, they also became more dedicated towards IS and reduced other businesses. Is this right?

-

Low Asset turnover – Company has consistently reduced its asset turnover ratio from 2010 to 2019. While the company invested more money into brownfield and greenfield projects, the utilization seems low. One reason this could be possible because it takes 12-18 months to get approval from customers on the new plant and as they are doing the capex every year, there is lag between utilization of those assets.

-

On a side note, company does not provide sales volume information anymore so its tricky to understand their optimum utilization levels

-

Overall, this seems concerning as the company will have to keep on doing capex moving forward and is not earning similar returns on its incremental capex.

Additionally, I was trying to understand maintenance capex. In the image below, if you see the total capex from FY11-FY19 is 385 crore, the incremental sales in the same period are 224 cr (383-159). The net fixed assets increased by 277 crore which seems like a growth capex to me since that is actual increased capacity during this time. Thus, Total capex - incremental NFA = Maintenance capex i.e 385-277 = 109 Cr for last 9 years. Is this the right way to think about it?

I further wanted to extrapolate that over a business cycle that 30% of operating cash flows spent on maintenance = 109/385 = 30% Can I increase it for inflation and assume 30-35% maintenance capex to identify FCF = OCF - 30% of OCP as maintenance capex? This rounds about 70 odd crores of FCF. Note (growth capex is excluded since its part of owner earnings)

Please enlighten me. Thanks

3 Likes

FY20 con-call highlights -

- Single-digit volume de-growth in FY20. 60-65% revenue share from exports.

- 60% domestic market share. No Chinese imports in India, so no anti-dumping benefits.

- As crude has fallen, some customers have asked for a price revision

- 4 crore MTM FX loss in other expense in Q4

- Capex: Brownfield - 150 crores in Phase 1, 65 crores in Phase 2. Both phases can give 150-175 crores of revenue. Each phase adding 5.5k MT. 50 of 150 crores of phase 1 capex done in FY20, remaining 100 in FY21. Phase 2 expansion will depend on the demand situation post Phase 1 is completed. Maintenance capex: 5-7 crores annually.

- Global: Only OCCL putting up capacity globally. 70-75% of global capacity utilization in 2019 (80+ in 2018). Saw some competitive intensity for the year, though global market share is maintained. North America saw some sales in FY20 but should see major sales from FY22 onwards.

- Future outlook, demand, growth guidance can only be made in the H2.

9 Likes

Hey guys - here are some thoughts, please share your comments on below questions -

- Low Asset turnover –

| 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Sales | 126 | 159 | 218 | 225 | 262 | 283 | 271 | 297 | 324 | 383 |

| Net Fixed Assets | 65 | 68 | 141 | 188 | 193 | 188 | 183 | 306 | 308 | 344 |

| Asset turnover ratio | 2.39 | 2.09 | 1.37 | 1.37 | 1.48 | 1.46 | 1.22 | 1.05 | 1.17 |

Asset turnover ratio has been decreasing and its below 1 on consolidated basis. OCCL has to constantly invest in increasing capacities to meet market demands and the overall utilization of these assets seems low or decreasing. The company increased its capacity from 15,000MT To 40,000MT from 2012 to 2020. They do not provide volume details anymore, but my research shows they must be utilizing 80-85% of their plant capacity and constant expansion drags the overall utilization level and affects asset turnover ratio. What I am concerned about is that for every $1 of sales they have to invest $1 in assets. Is my understanding, right? What other reasons could there be? How does this affect their return on capital?

1.1. Return on incremental assets –

On standalone basis, net fixed assets grew from 68 cr in 2011 to 344 cr in 2019 whereas CFO grew from 29 Cr to 89 cr. ( I prefer using CFO than PAT here) If you see the returns on incremental assets between 2011-2015 its 34% but it drops down to 12% from 2015 to 2019. My assessment is – OCCL is earning less on its incremental assets which is concerning given that company increased its margins in last decade. What inference should I take from this

| Year | 2011 | 2015 | 2019 |

|---|---|---|---|

| PAT (cr) | 37 | 51 | 74 |

| CFO (cr) | 29 | 70 | 89 |

| Net Fixed assets (cr) | 68 | 187 | 344 |

| Cashflow return on incremental assets CFO/NFA | 34% | 12% |

Side note – Interestingly, return on capital has not been impacted which is confusing. Shown below.

2.Return on invested capital – Owner’s earnings approach.

I read about calculating ROIC from NOPAT approach vs Owner’s earnings and I liked owner’s earnings approach much more suitable since thats actual cash coming out of the business.

Owner’s earnings are calculated by subtracting OCF – Maintenance capex. In calculation below I assumed 15% maintenance capex as management clarified in conference calls that their maintenance capex is in single digits and I have been conservative.

Invested capital is sum of short term and long-term debt plus equity minus excess cash. Table above shows that management has been conservative and is keeping cash at hand for bad times. Thus, my ROIC has been around 16-17% on avg. Thoughts?

1 Like

OCCL :

Sales CAGR for 1 year, 2 year average are in single digits at 6-7% and 3-year average is at 4%. (This is mostly because FY2019 sales had negative growth and back to positive in FY20). This is because the company already has 60% domestic share and the only way to grow is to expand internationally. They have a 10% international share in insoluble sulphur and as in the concall, they are investing in the capacity and sales increase can be seen from FY22 on-wards. So the promise of the company is future sales

Promoter holds 51.7% in the firm and they seem to believe in the story of the company as they increased their stake.

SSGR of the company is at 10% and so all the capex can be funded without taking on additional debt. NPM at 16%, low depreciation at 6%, low dividend payout ratio at 18% and high asset turnover at 121% drive the SSGR. NPM is unlikely to change in future as this is a monopoly business. The asset turnover used to be 50% higher a few years back, and it will be interesting to see if it gets back to those levels. ROCE could greatly improve if the asset turnover increases.

Company has 0 debt which is very good as all the capex is funded by its performance as the SSGR indicates. 13% of the market cap is actually cash & eq. So the company is cash rich. Based on an interest coverage ratio of 3, a prudent banker would give a loan of 351 Crores, which is almost half the market cap of the company. The company also has 100 crores of cash. These two make up 451 crores. So the company could be a target for a leveraged buyout in future.

No accounting red flags as the PAT is getting converted to cash, cash in the company is generating good interest income, CWIP/Gross block is low, inventory turnover and debtor days are similar across the years.

Company generates good FCF and EV/FCF is very cheap. High margin of safety as the company is likely to give 10%+ CAGR over 10 years as long as P/E at end of 10 years is 10 and earnings growth > 10% during this period. There is room for both P/E expansion and Earnings growth in the stock

Disc: Invested. Have 171 stocks at a price of 695.

11 Likes

Hi All,

I have compiled my research on OCCL on my blog. Oriental Carbon and Chemicals Limited – Coffee with Abhishek

( PS - Not trying to promote but share compiled information)

Key Investment Rationale

OCCL is one of the top 4 producers of Insoluble Sulphur (IS) where only 4 players hold 90% market share globally. Demand for Insoluble Sulphur is dependent on the production of rubber or tyres which is related to the auto industry and replacement tyre market. Demand for tyre through Auto OEM’s consist only 30% of the industry and 70% is a replacement market which keeps the demand stable. The tyre industry is expected to grow at 3-4% over the next decade and there are no structural changes that would affect the manufacturing of tyre or rubber. Use of IS has increased due to shift from bias tyres to radial tyres. India still has large growth potential for radial tyres in the Commercial Vehicle segment as only 50% of the industry has adopted to radial tyres. While the industry is growing at a smaller rate, OCCL enjoys high barriers to entry with competitive advantages that allow them to maintain significant operating margins. OCCL has prudent management that has consistently innovated in higher grades of IS as per customer demand.

At current capacity with optimum utilization, OCCL generates 90 crores of owner’s earnings after maintenance capex. At 11% discount rate, it should command a minimum market cap of 900 crores i.e. 850 crores for OCCL and 30 crores for its subsidiary Schrader Duncan with no growth in future. Assuming a mediocre growth of 5-7% starting FY 2022, brings intrinsic value at 1300 Rs/share on DCF basis. Thus, current market cap of 700 crore provides enough margin of safety and downside protection for such a high quality, low uncertainty and low risk business.

Covid19 Update

Management has clarified that FY2021 has been negatively impacted due to auto slow down and expect the sales to drop by 25%, profits to drop by 50% for Q2FY21 at least. They are optimistic about demand picking up in Q3FY21. The first phase of the latest expansion has been delayed its commissioning to Q1FY2022 from Q4FY2021.

Conference call Q1FY2021

Risk

Eastman chemicals USA controls the Insoluble Sulphur pricing. Any change in the pricing can affect OCCL’s margins and return on capital. Secondly, Chinese players have not come to global market due to their lack of innovation and product inconsistency. They can drop prices to grab market share which can affect overall margins for the industry.

Here’s my Investment Checklist -

May 1 2020 - Morningstar report on Eastman Chemicals -

https://drive.google.com/file/d/1d4CA1YA-XVB5S_6U6y9ay8ktqgp-hSrP/view

I have access to Morningstar premium so feel free to ask me for any reports you might want.

Here are questions I am trying to find out

- Does management have most of their net worth in the company?

- Does Eastman actually hold 70% market share? A lot of Indian brokerage reports say so but if you go to eastman’s annual report they don’t really share lot of information about their Insoluble sulphur business. I wonder if there is an analyst report that claims so?

- I have access to morningstar reports on Eastman chemicals and even they don’t mention Eastman’s global market share and the advantage they might have. The only thing they started writing about is Crystex - the IS material since 2018 because Eastman found a cheaper way to produce it and has a commercial patent for the next 10 years.

- Morningstar report claims there are tyre regulations starting FY 2021 that Eastman will benefit from. Other than F1 Race regulations, I couldn’t find any material on this. Do you have any idea?

From Morningstar report =

"While Eastman sells a diverse portfolio of chemicals that have a wide range of end uses, we see a couple of trends that should benefit its competitive advantage over the next several years. Eastman’s best-in-class portfolio of tire additives should benefit from more stringent tire regulations that take effect in 2021. These regulations require tire manufacturers to reduce rolling resistance in order to increase fuel efficiency. They also require a minimum amount of wet grip and maximum level of external rolling noise. Eastman’s continual innovation of its Crystex and Impera brands allows the company to charge a premium as its newest patented products allow tire manufacturers to meet the pending regulations in all three areas. "

Feel free to reach out

6 Likes

I am working on a financial model but summing up my research here -

- Attractive Primary Market . OCCL is the 3rd largest producer of Insoluble Sulphur (IS), key ingredient in vehicle tyres out of 4 global players. 30% of OCCL’s revenue comes from India and 70% from Europe, Africa, and North America.

- Impending Industry Growth . Use of IS has increased due to shifting from bias tyres to radial tyres and India still has large growth potential for radial tyres in the Commercial Vehicle (CV) segment. Only 50% of the CV industry has adopted to radial tyres.

- Sustainable Competitive Advantages . OCCL enjoys high barriers to entry with competitive advantages that allow them to maintain significant operating margins. The company produces higher-grade IS than Chinese competitors.

- Valuation Upside . I value OCCL on a DCF basis using an 11% discount rate which yields intrinsic value of 1200 Rs/share vs current share price of 800 Rs/share. The price target of 1200 Rs/share implies capital appreciation of 50% plus a dividend yield of 2% for a total implied return on 52%.

10 Likes

Oriental Carbon.xlsx (343.8 KB)

Attached Financial model inspired from Michale Maubossin’s book Expectation investing. Here’s the supporting.

Covid 19 Effect

OCCL’s sales and ebit would drop by 30% in FY21 with sales going back to optimization levels by FY 22. The company is expanding its capacity from 34,000MT to 45,000 MT which is likely to come online by FY 23 which is good enough time to get 7-10% sales growth and for the market to recover

The consensus estimate is sales growth of 5%, EBIT margin - 28% that brings Mkt cap at of 773 crores over a 12-year forecast till in March 31 for OCCL as a standalone entity. Add 30 cr market cap of Subsidiary for valuation of 800 cr market cap which is the current valuation

Sales growth and Margin expansion are the two Turbo triggers that will expand shareholder value for OCCL. Sales growth from 5% to 14% can bring valuation to 1214 whereas operating margins will have to grow from 28% to 41% to get a similar valuation for constant sales growth of 5%. Operating margins will increase with sales growth due to economies of scale and operating leverage.

One of the most likely scenarios that can result is sales growth of 7-8% and operating margins of 33% that would result in a valuation of 1050 Cr.

Leading indicators of Sales growth are new capacities added by tire companies

Sales growth will come from OCCL tapping into new markets, adding new plants.

OCCL currently supplies in 21 countries and to 40 customers. New geographies may have same customers so its new plants that are getting added.

Reviewing expansion plans of major tyre companies will help us understand when the demand will come back,

| Sales Growth | Sales | EBIT | Subsidiary | Standalone | OCCL Value | |

|---|---|---|---|---|---|---|

| 0% | 25% | 30 | 674 | 704 | ||

| 5% | 28% | 30 | 773 | 803 | ||

| 14% | 30% | 30 | 1184 | 1214 | ||

| Operating Margin Growth | Sales | EBIT | Subsidiary | Standalone | OCCL Value | |

| 5% | 24% | 30 | 678 | 708 | ||

| 5% | 28% | 30 | 773 | 803 | ||

| 5% | 41% | 30 | 1189 | 1219 | ||

| Possible Range of outcomes | Sales | EBIT | Subsidiary | Standalone | OCCL Value | Probability |

| 5% | 28% | 30 | 773 | 803 | 15% | |

| 7% | 33% | 30 | 1005 | 1035 | 50% | |

| 10% | 33% | 30 | 1133 | 1163 | 30% | |

| 14% | 33% | 30 | 1350 | 1380 | 5% |

Some weekend research here –

-

EV Trend , EV Market is expected to grow at 21% CAGR from 3b units to 27b units by 2030 – Source- https://www.marketsandmarkets.com/Market-Reports/electric-vehicle-market-209371461.html

-

Faster wear out , Due to high torque required, EV tires wear out 30% faster than conventional tyres. Source - Pirelli Showcases Performance Tires Built for Electric Cars.

-

Faster wear out – Avg tire runs 50,000 miles vs EV tires run out after 20-30,000 miles. Read comments for realistic picture. https://solarchargeddriving.com/2018/08/26/premature-tire-wear-appears-to-be-biggest-maintenance-issue-for-electric-cars/

-

Watch this video - Do Tyres wear out faster on a EV ? - YouTube

-

Tire makers are prepared, While tyre technology is changing, tyre manufacturer will install these in the auto’s that are being sold and gradually all the tyres will be replaced by EV specialized tyres that are lighter and has low rolling resistance and is able to carry extra weight of the EV batteries in the cars. Goodyear EfficientGrip Performance with Electric Drive Technology - YouTube

-

Change of complete market – Miles driven vs Quality of tyre – There will always be a trade off as conventional tyres will reduce range of miles driven for EV vehicles, so people will buy specialized tyres which are lighter but expensive to keep higher mileage range. Higher mileage range tyres will have low total miles driven 20-30k miles as said above.

-

Noise reduction – One of the benefits of EV vehicles is they don’t make noise, but conventional tyres do, so people will buy EV specialized tyres to reduce noise than avg for passenger vehicles at least. Guess what, noise cancelling tyres will be expensive

-

Higher range tyres → Expensive The website below shows tyres for EV vehicles. While they provide 50,000-mile range. They are all above $140 range where as I bought a tyre for my Toyota Camry for $76 that has same mile range.Discount Tire | Tires and Wheels for Sale | Online & In-Person

-

Nokian – A UK based company claims that electric vehicle tyres don’t wear out as claimed but if you watch this honest video at 4.58 min. She went through 1 set of tyres for 48,000 miles only and apparently the cost was $410 per tire. How Much It's Cost To Run Our 2017 Chevrolet Bolt EV So Far! - YouTube

Source - Electric vehicles are changing the future of auto maintenance – TechCrunch.

Insoluble Sulphur – My guestimate shows that if tires are going to wear out 30% faster, the current tire demand will also grow by 30%. Current outlook on major reports is 4-5% globally and 7-9% in India. Thus, I believe Tyre market would grow around 8-10% which would boost demand for IS as well.

PS – I actually think the growth will be even more but still not able to collect verifiable data.

14 Likes

Hi

Their recent results are not that bad looking into current market condition.And being a supplier to the Auto industry they are facing double whammy of intense slowdown and Corona effect.

Their Profit before exceptional item stood at 24 crore(March 31st 2020) compared to 27.5 crore(March 31st 2019).

However management is having a cautious stance for the Q2 due to the pandemic.They are expecting the revenue to go down in the range of 25 to 30% and PBT to be reduced to 50% comparing to the last quarter.

They have couple of positives in their faviour

1-> Rupee depreciation

2-> curbs on imports of certain pneumatic tyres. Which will drive more domestic production and in turn demand for IS will increase.

Disc:Not invested as of Now.

Thanks,

Deb

1 Like

Nice Analysis.

Can you please also look at any potential disruption due to AIRLESS TYRES which may have an impact on replacement market or may be the chemical mix required to produce it … Just wondering !!!

3 Likes

Hi,

Does this airless tyres require insoluble Sulphur for its manufacturing??

Thanks,

Deb

Components :

Research article on Non pneumatic tyres are made especially by Michelin

Concept of Non Pneumatic was started by NASA for space rovers

Polymer is the main ingredient

NONPNEUMATIC TYRE

Non-pneumatic tyre (NPT), or Airless tyres, are tyre that is not supported by air pressure. Airless tyre generally

have higher rolling friction and provide much less suspension than similarly shaped and sized pneumatic tyres.

Other problems for airless tyre include dissipating the heat buildup that occurs when they are driven.

Airless tyre is often filled with compressed polymers (plastic), rather than air. Resilient Technologies and WisconsinMadison’s a company specializing in Polymer Engineering and design are creating a “non-pneumatic tyre” (no air required) which is basically a round polymeric honeycomb wrapped with a thick, black tread and that will support the weight of add on armor, survive an IED attack, and the tyres are expected to maintain a speed of 75 mph for 60 miles with 10% damage to the honey comb structure. Honeycomb structure is designed to support the load placed on the tyre, dissipate heat and offset some of these issues. The patent-pending design mimics the precise; six sided cell pattern found in a honeycomb and best duplicates the “ride feel” of pneumatic tyres, according to the developers. The goal was to reduce the variation in the stiffness of the tyre, to make it transmit loads uniformly and become more homogenous, and the best design, as nature gives it to us, is really the honeycomb.

Will it come to India soon? No - this is just a concept implementation is too far from now (even tesla uses normal tyres down the line polymers industry may have good future)

Thanks for this @Tauqeer

Note : Michelin has announced that by 2024 they will be entering into the market for airless tyre similarly Bridgestone have also come up with similar airless concept using rubber threads.

9 Likes

Latest Results

2 Likes

I have looked into this. Airless tires are not feasible for commercial usage and would not become a large part of the overall pie. The commercial usage of these tires won’t come until 2024. Refer to google news. The ride quality of such tires is questionable as it affects suspension.