P&E: 10.8 cr on a gross carrying value of 239 cr - thats about 5%

Building: 3.57 cr on a carrying value of 147 cr - thats about 2.5%

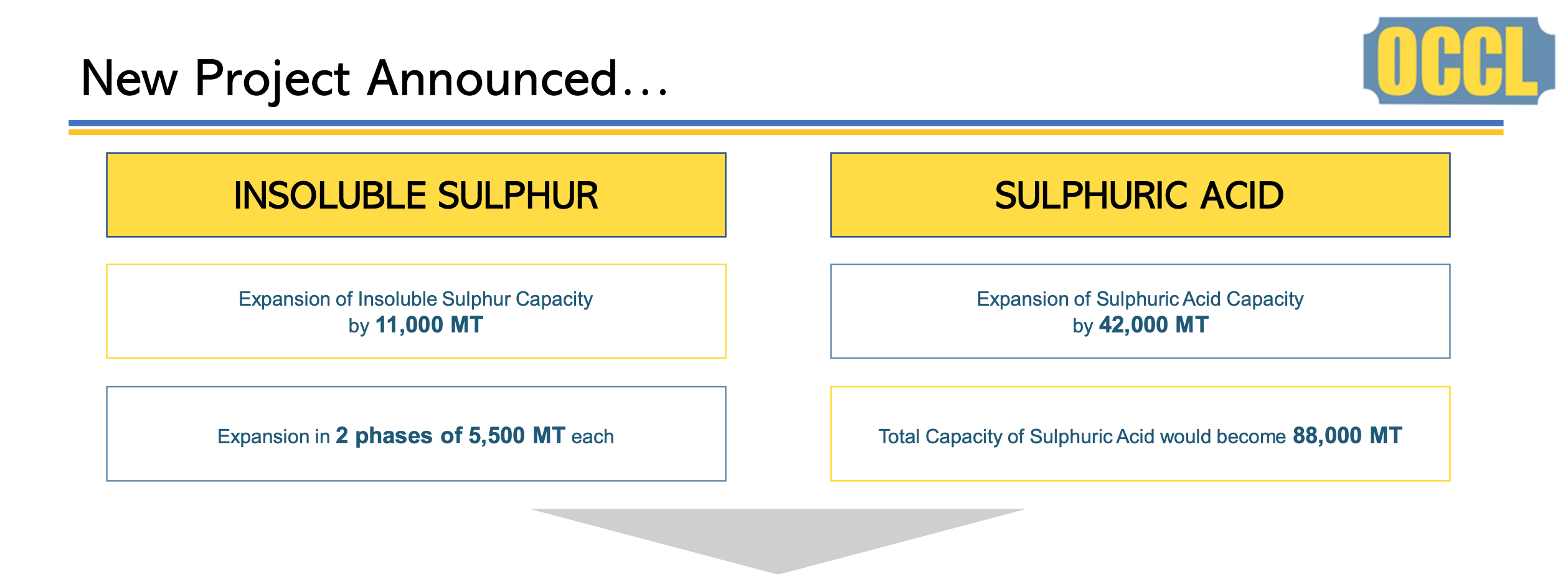

Even after all this capex, they seem to have run out of capacity. Another mega capex announcement of 216 cr in latest investor presentation.

Comment from report:

“There has been a slowdown in tyre production consequent to slow down in the automobile

industry. Multiple factors such as the slowing economic cycle, changing emission norms, like

India’s adoption of BS-VI by 2020, Europe’s ban on diesel cars and the enforcement of safety

norms across the world has resulted in the slowdown”

1 Like

Here are some of the high level fundamentals I gathered mainly from the Annual Reports.

Pricing Power: The company is one of the largest manufacturers of insoluble Sulphur in the world and largest in India. It has many of the major tyre manufacturers of India as its clients. In terms of competition catching up, it seems it is an uphill task because customers have some requirements for norms and certification of the process which takes many many years. OCCL has this on its side and has achieved these certifications and is the go-to company for its customers. So customers do not switch to other suppliers easily. It could be one of the reasons why the company is able to keep its margins strong EBIDTA at 30% and PAT at above 15% for quite sometime, more importantly even in this period of slowdown.

Efficiency:

Not only with process perfection, the company also highlighted that it takes various steps for managing time and waste in manufacturing process, thereby increasing efficiency which is also one of the reasons for high margins.

Growth

If the auto sector picks up, (irrespective of the EV boom or ICE continuing to stay, Tyres aren’t going away) and company could gain in revenue as well as the stock may enjoy re-rating, it is currently trading at a very low PE (13). On the other hand, company has made clear its intentions to grow markets other than India (China/US). It’s vision is to be present in every tyre manufactured in the world!

What is not to like in such a company? Is this a value stock which is undervalued right now?

Would be glad if folks here could highlight what could go wrong for OCCL in terms of business in the next 5 years…

Disclosure: Invested

2 Likes

As per the current quarter eps ,PE will be 15.5

So looks appropriately priced and may correct to Pe of around 12

Main thing here will be opportunity cost as not sure how long the auto slowdown will last

Tracking and looking for entry point

1 Like

I agree with your points that the business is very well managed and efficiently run.

Coming to your point on things to watch for the next five years? I think you have already highlighted one of the main thing to watch. Under the growth subsection, you started with

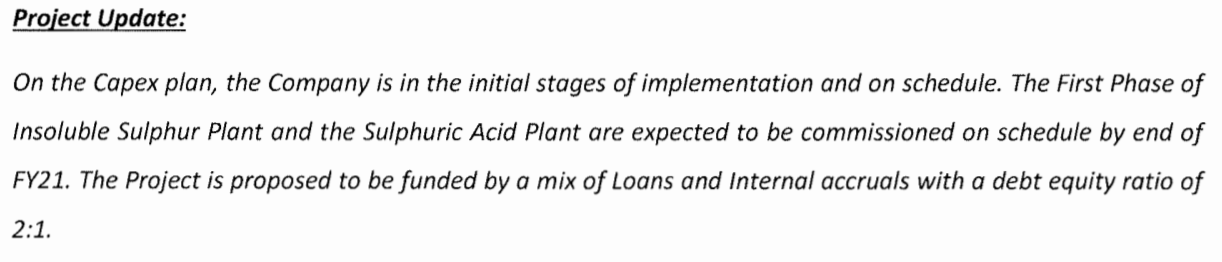

This is the thing that one should focus IMO. The “If” is we need to see. The company is already undergoing a capacity expansion. The management said that the expansion project is on schedule, which is a good thing.

But it will pay off only if the slowdown is over by the time the project is finished. If the sales does not pick up by that time, the situation can turn bad.

Moreover, the chinese player China sunshine (https://www.chinasunsine.com) in IS market has announced a very big capex and claims to have more than 1000 customers (total customers, not necessarily IS customers). Although the quality and efficiency of this manufacturer needs to be verified, they might give tough competition to OCCL in expansion in China, which is the biggest market for IS.

Given all the challenges, I think OCCL is a very strong player with good management behind it. However, IMO continuous monitoring of these developments is necessary in order to maintain a healthy portfolio.

Comments/thoughts welcome.

2 Likes

On sunshine competition mgmt said currently sunshine catering mostly to the Chinese demand. Not giving much competition to outside china as per latest concal

Agree, they are exporting 30% of all the products (if I am not missing anything). My point was the same, this could create competition in expansion in China.

1 Like

I agree here that the auto sector pick up may be a big If. But also think that it is also sector without which economic growth would still be muted and it is in the Govts interest to revive growth, specifically for a country/market like India. So I believe we will see growth pick up in the coming 5 years. Therefore I would like take a bet that OCCL will gain in India mainly from sales pick up because of recovery in auto sector. Additionally management has been saying that they also expect sales to revive because of radialization of tyres, this is yet to be seen.

One important point also mentioned by the management in the Annual Reports is that they are inherently very conservative and only after evaluating that their investment in Capex really makes sense. they decide to pursue the expansion project. Below paragraph in the Annual Report 2019 gives me some confidence

Never over-leverage

At OCCL, we believe that to finish first, we need to first finish. This clarity is largely influenced by the quantum of debt on our books. In a business where only a handful of global companies possess specialised manufacturing technology, there can always be the temptation to mobilise large debt, invest in substantial capacity and engage in an aggressive pricing strategy to carve out a larger market share. This is a temptation that we have avoided. We believe that large debt on our books could influence our strategic thinking away from the values we have cherished – of remaining a focused quality- and knowledge-driven player in addition to protecting Balance Sheet integrity.Expand incrementally

At OCCL, we address a global market that is annually growing in the modest single-digits. To expand aggressively in this market could disturb market stability or leave us with large unutilised capacity until market growth caught up with our installed base. We believe that steady growth has been the safest tested response until now with expenditure that can be largely addressed through our accruals. This does not compel us to disturb our commitment to deliver quality products and services that could, in turn, affect our brand potential does not stretch our managerial bandwidth in a business with a premium on the availability of specialised professionals. This marathon-like approach (as opposed to a sprint) has helped to sustain the business in this past and we expect to sustain this approach across the future.

It would definitely be interesting to watch OCCL’s progress in China and US markets in the coming years. I plan to watch this and increase/decrease allocation to this stock in my portfolio.

Disclosure: Invested

5 Likes

In the concal management said they are not seeing any traction in china market and competition over there very high,so they are not seeing any potential over there.

And on USA market management seeing good traction and getting good orders and by fy21 they are aiming to reach the market share in USA equal to global market share.

1 Like

Q3 Concall notes:

Q3 Revenue 81.9 <- 96.1

Q3 EBITDA 24.8 <- 36.1

Q3 PAT 16 <- 20

Q3 EBITDA Margin 30.3%

Q3 PAT Margin 9.5%

9M Revenue 264.7 <- 289.4

9M EBITDA 79.5 <- 96.9

9M PAT 54.4 <- 54.7

9M EBITDA Margin 30%

9M PAT Margin 20.6%

Capital work in progress -> 30Cr

Long Term Debt -> 90Cr

Short Term Debt -> 30Cr

Cash -> 120Cr

Q. Progress in USA and China?

China → No traction, extremely competitive

USA → Good prospect, supplies increasing

Targeted 1 year to get Market share = global market share, in USA.

Domestic → Our market share increase, but market down.

Q. Capacity increase globally in last two years:

OCCL - 5000T,

Estman - 40000T, Shikoku 10000T

OCCL - 5000T new capacity end of year.

On track with OCCL capacity plan.

Globally total cpacity 300,000T. utilization below 80%

Q. General engineering product revenue stable but PBT number is Fluctuating? 26L, 2C, 76C

Due to non operational reasons. Take 4Cr as run rate

Q. Effective tax rate

OCCL → 17-17.5 % MAT

Subsidiary 0% tax

Q. On Competition in India Possibility lose market share?

No, we are working hard to increase market share

Q. Capital Allocation:

Very prudent on capital use, risk weighted returned on capital

Insure earn best returns.

No plan, to go into products unrelated to sulphur.

Q. Replacement Cost for Green Field 4700T plan

estimates of capex of 800Cr+

Q. New client in last quarter

Yes

Q. Impact on Tyre Capex?

Continuing, No fresh capacity expansion

Q. Duncan Engg strategy?

No growth seen because of slowdown. Positive on company, continue to do better

Q. China Sunshine

Confirmed, don’t have 4th guy that supplies to global market.

Sunshine have got good traction within China. Does not really affect us.

- Sulphur price down last year. 9 Cr revenue down on account of sulfuric acid.

Margin down because of sulfuric acid - Volume of export is suffered more, than domestic.

- Anticipating pricing pressure

- No adverse impact on contribution

- By end of 2020, early 2021, Capacity 40000T, after that will take call for next capex.

- Current Expansion is at Dharuhera plant.

- Started selling new product to 1-2 customer.

- Cost saving will come from Q2-FY20. This is priority for us.

- Tyre production 10% down.

- Next year (once Capex is done) is better time to discuss the next buyback or special dividend

15 Likes

Going forward, I don’t see OCCL considerably outpacing the industry growth which will most likely be 5-6% at best. This is a good stock for inflation beating returns. But, considering the length of the runway, returns in mid to high teens won’t come

Disclosure

Not invested

1 Like

OCCL has provided a couple of disclosures to BSE. These disclosures say

- Increase in borrowing powers of the Board of Directors pursuant to Section 180(1)© of the Companies Act, 2013

- Authorizing the Board of Directors to create/modify charge on the Company’s movable and immovable properties, pursuant to Section 180(1)(a) of the Act, for securing its borrowings

Can someone please explain what does this mean for the investors? What are these resolutions about?

1 Like

Probably due to Company’s act provisions that requires board resolution in order for BoD to take more debt than earlier limits for the Capex.

2 Likes

My concern is how can the cumulative CFO be so much greater than the cumulative PAT? As the money collected in reflected in the CFO, so how can they collect more money than they have reported? Am i missing something?

Depreciation, decreasing working capital requirements could be the reason.

1 Like

Company has been talking about penetrating in the North American market since last 3 years, do we have any clue how is the market share they have gained there or how much additional revenue its generated from the new markets which it has been exploring?