Mangalam Organics has become increasingly difficult to track as it doesn’t do con-call and is highly illiquid (made worse by SEBI ASM frameworks) as well. If i recall, it had done large capex few quarters ago. There may be lag between commodity price increase and company earning due to multiple factors e.g. low priced finished goods inventory still in the channel esp. for B2C players, existing price contracts for B2B sales wherein price hike may take few qtrs to come into effect, presence of high cost RM inventory hence subdued margins, loss of market share etc. Most of these reasons may be theoretical as lack of con-calls means these would be our best guesses. Some buying by promoters and impact of capex done in 2022, may indicate positive outlook for the company esp. if camphor prices remain firm. Q1FY25 results too indicate some increase in inventory so their liquidation at increased prices too can give EPS a leg up.

Agree to your points. I have taken position based on macro and technical factors which you mentioned, Brazil is going through sharp downturn and many farmers have left Pine Tree tapping, it will be sometime before it revives. This will keep camphor prices elevated, I am banking on B2C sales which will help margins and promoter buying 4% of the company indicated to me that things may turn in medium term.

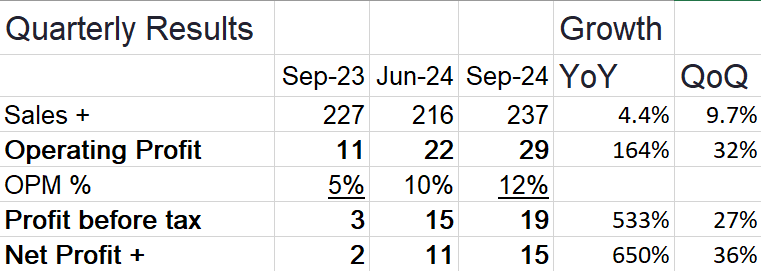

Q2FY25 results [Link]:

- COMMENCEMENT OF COMMERCIAL OPERATIONS OF ORIENTAL AROMATICS & SONS LTD.'S NEW GREENFIELD FACILITY IN MAHAD, MAHARASHTRA.This state-of-the-art manufacturing unit is designed for the manufacturing of the specialty aroma chemical ingredient, Evermoss AB20018. The total capital expenditure for this project is approximately Rs. 160 crore.

Conf. call Summary (Updated on 14-Nov-2024):

-

EBITDA guidance: 10~12%. Being conservative as camphor price pressure yet to abate and 2 new plants need to stabilize and scale up.

- Baroda (Hydrogenation) Plant: Commissioned in July and capacity utilization now at 30%. Will increase contribution with time.

- Mahad (Special Aroma, Greenfield) Facility: Commissioned in Nov.

-

Base business and both the new plants could add 250~300Cr. revenue to the current topline in 2 Yrs. (13~14% CAGR). On the demand side of the 2 divisions (Speciality aroma and F&F), discussion on destocking and reduced demand has come to an end and expect steady demand.

-

H2FY25: Incremental YoY revenue growth of 5~10% for Speciality aroma and F&F division. Camphor being cyclical is still wait and watch. Conversations on commercial transactions for new products from the 2 plants have just started and it is difficult to commit any number.

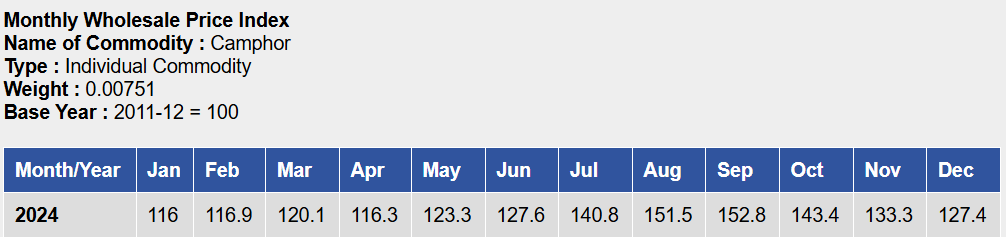

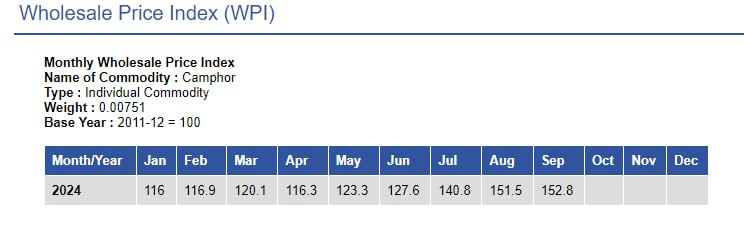

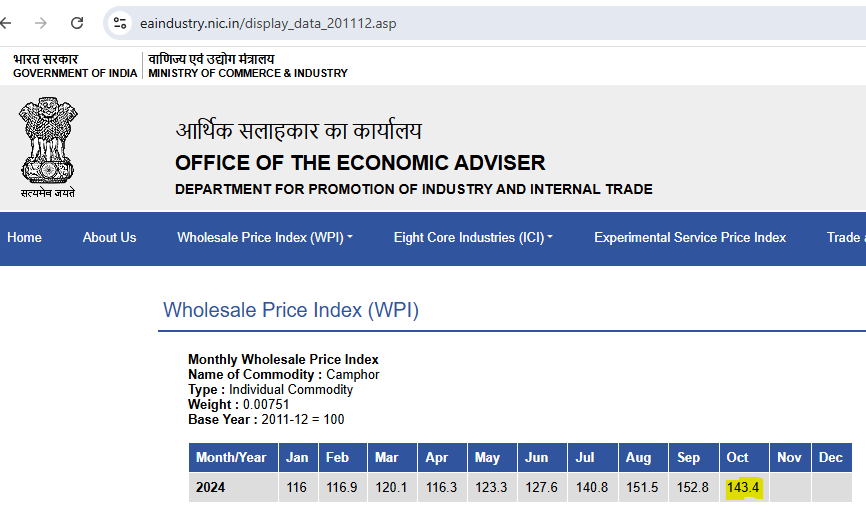

Camphor’s Wholesale price falls in the month of Oct compared to months of Jul and Aug:

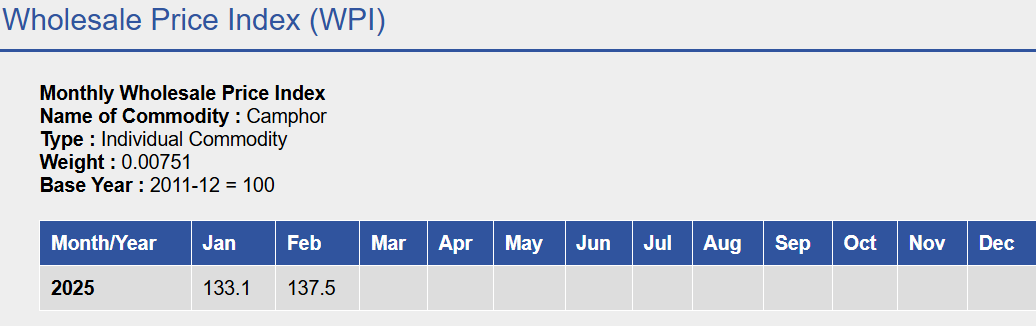

November this camphor WPI is 133.3 , downward and price unstable. Seems guidance will be correct. Ebidta margin will remain closer to the management conservative numbers

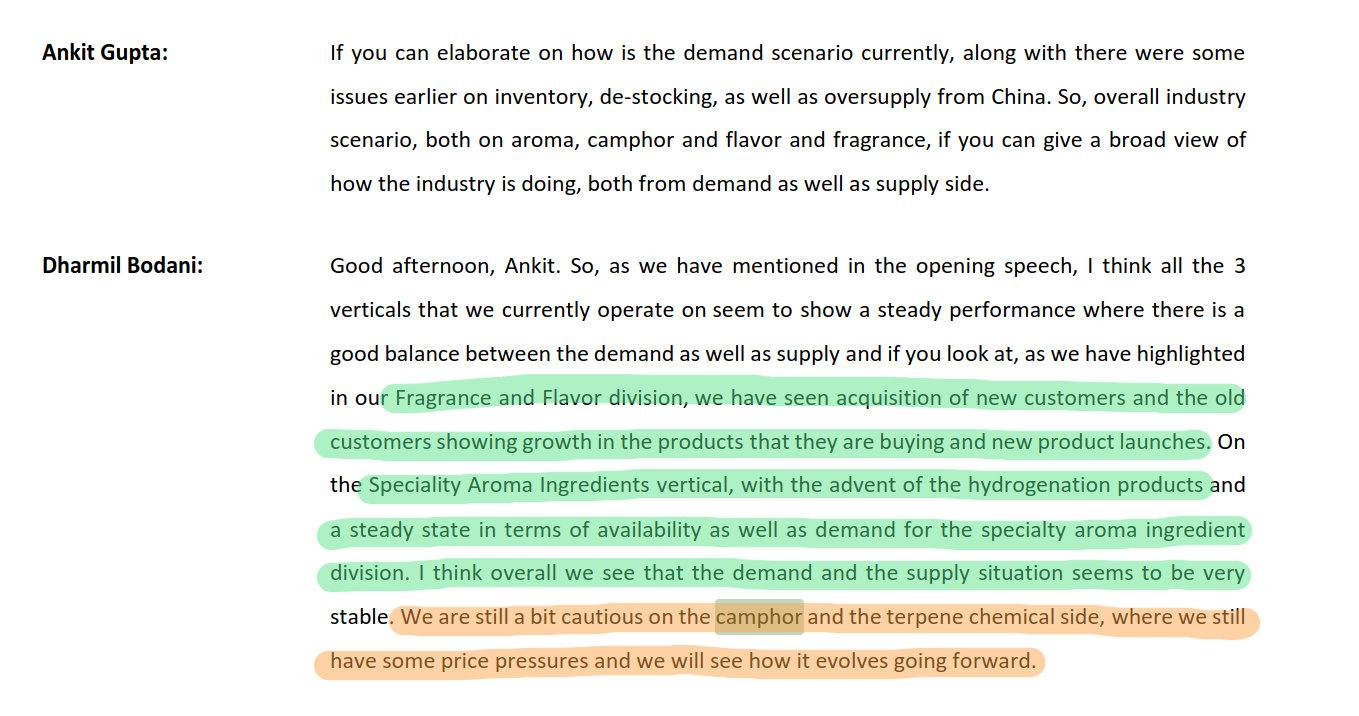

Flavours & Fragrance and Aroma chemicals segment seems to be doing well. Camphor - Management was bit cautious. Looks like the cycle has not fully turned around.

Does this math work?

Current PE ~24

Sales ~900 Cr, PAT ~40 Cr

OAL is expected to add 250-300 Cr in 2y (base + capex) at 10-12% EBIDTA (let’s take 11%)

FY27 Sales ~900+250 = 1150 Cr

EBIDTA ~ 125 Cr

Assume increasing trend, Net (Other income - dep - interest) ~ 45 Cr

PBT ~80 Cr

PAT (30% tax) ~ 57 Cr

If PE remains same ~24, Price potential = (57x24)/(40x24) ~ 1.4x

40% in 2 years at SAME PE as today does look good at today’s valuations.

Ofcourse, we do not know how PAT% and PE would look like 2 years from now. Could go either way.

Disc: Planning to invest.

The only thing you didn’t consider as risk is camphor prices. They are very volatile and its very hard to predict what would be next quarter.For analysis of valuation don’t use p/e as earnings are not stable use another metric to value business, like in steel we value using p/b which is also type of commodity.

Disclosure:invested from higher levels

Could you share your metrics for investing? I agree it is difficult to predict camphor prices, hopefully it will be on the better side atleast once in the next 2 years, or say 3 years - still looks like a decent bet.

My thesis was there was some part of margin expansion happening in business

if camphor prices become stable it will help in operating leverage

So what multiple do you use to value it? How would you know the value is rightfully or over priced?

I use technical analysis for these business

SH Kelkar managements claims that the raw material prices have increased and the Q3FY25 results allude to the same. Gross margins got hit by ~4%.

Oriental Aromatics - management says that they are seeing price increase in some but not a sudden hike. At the RM basket level they say that prices are more or less stable.

Can anyone tracking Oriental help how to interpret this ? Can this be related to product mix ? Both of them supply to most of the domestic FMCG players.

I think F&F players don’t have any pricing power. They are the mercy of FMCG players. Most of the contracts are for 6 -12 months. Any sudden inflation in RM, they will take hit at the GM/OPM and NPM.

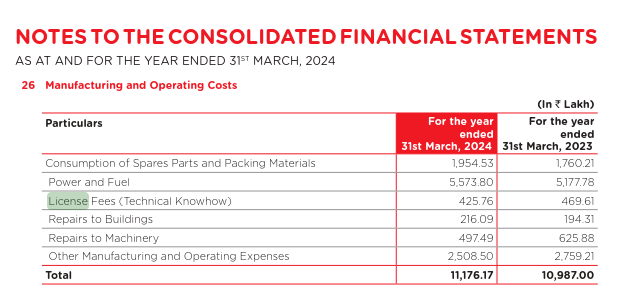

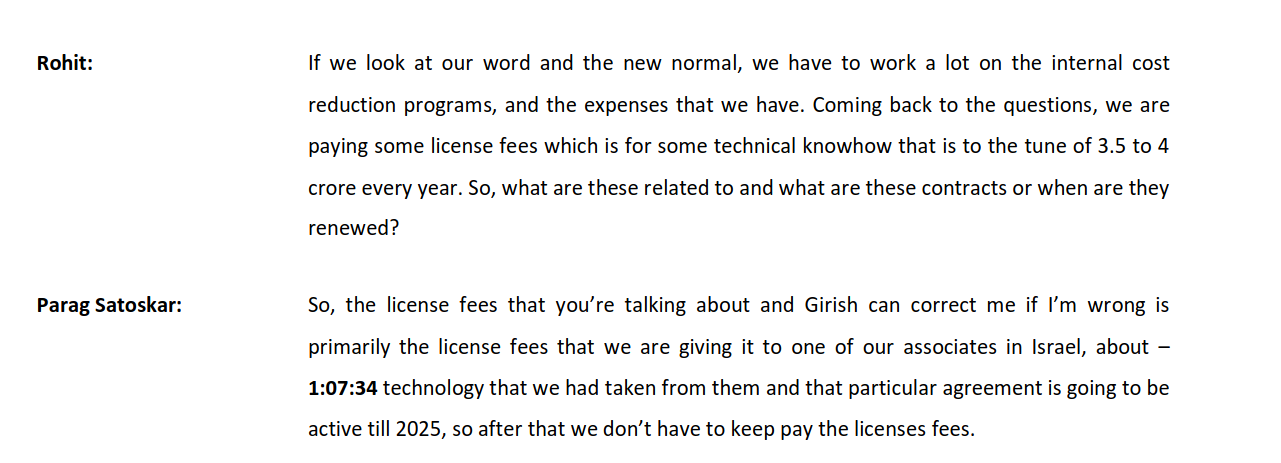

OAL - Looks like ~4Cr of license fee will not be there from FY26 onwards.

Nice coverage on OAL - Oriental Aromatics Ltd Share Analysis: Is This Stock Set to Surge?