Decent Q4 numbers.

1 Like

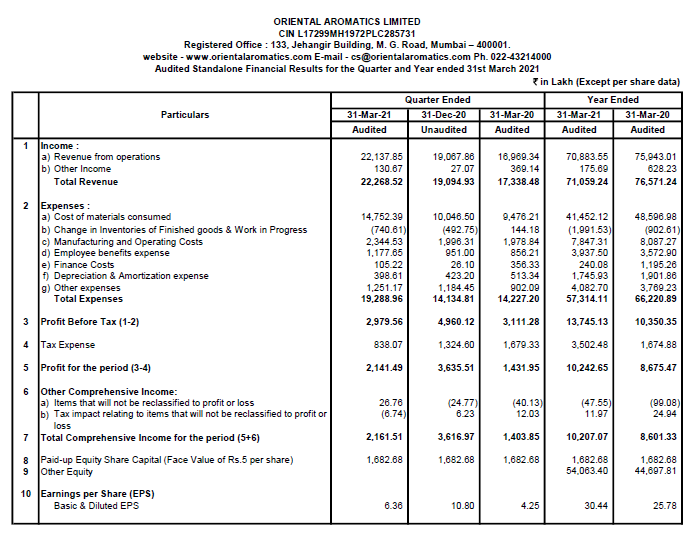

Seems poor results to me as margins have really come down. Management commentary would be important.

Management had already clarified in several previous concalls that 17-18% OPM is sustainable.

1 Like

From AR 2021, provision for bad debts has increased 3 fold - from 27 to 95, legal & prof expenses have grown by 200 Crs, sales promotion expenses have gone down from 105 to 67, Inventory has increased while write down of inventory (reflected in raw material consumption) has increased because of aging, liquidation and realizable value. These seem to be concerning given that industry is a slow grower and companies are price-takers - any insights?

Privi Speciality Chemicals is also able to maintain margins of 17%. How does Oriental compare? Both companies focus on aroma speciality chemicals

5 Likes

And how come you say that this business is price takers? Does it controlled by any tariff norms under any board? Can you please tell me.

Flavor and Fragrance Sector Analysis_ E…pdf (2.2 MB)

Refer attached overview of the sector. It talks about slow growing industry and pricing power

3 Likes

Last 11 yrs cummulative PAT=400 cr around

Last 11 yrs cummulative CFO=300 cr

I think about 25% CFO is stuck in reveivables

Last few yrs receivables

receivables as % of sales

2021=26.65%

2020=20%

2019=21%

2018=26%

2017=22%

2016=22%

2015=22%

Inventory as % of sales

2021=32%

2020=21%

2019=27%

2018=26%

2017=25%

2016=20%

2015=23%

Form 2010 to 2020

cPAT=298cr

cCFO=281cr

There is sudden jump in receivables in 2021 and 2018.

There is sudden jump in inventory in 2021.

5 Likes

Does anyone have link to investor meet held yesterday?

Disc: Invested

1 Like

http://www.orientalaromatics.com/corporate-announcements/ErnPresSep21.pdf

pdf of investor presentation

Q3FY22 Results - https://www.bseindia.com/xml-data/corpfiling/AttachLive/e56e0f52-cb1f-42b0-9aeb-a7b631672691.pdf

- Cost of materials consumed as a % of expenses is ~81% which is generally in the 60s range hence a sharp decline in margins and profits.

- Revenue is more or less the same which was expected as 1) no new plant was ready to give additional sales in Q3 and 2) high capacity utilize. of almost all facilities.

Overall, not a good set of numbers.

Disc. - Invested

3 Likes

OAL has got the EC for their Greenfield project expansion at Mahad.

As per earlier con calls, this was supposed to be attained in Q3FY21 but got delayed due to COVID and whatnot.

About the Mahad CAPEX -

- Investment of ~200-250 crores. Will be a combination of certain Turpene chemicals and certain standalone plants for single products.

- A camphor unit will also be set up in Mahad, which gives geographical de-risking for camphor.

- It will be a zero liquid discharge plant from day one

- As per the management, all technology, ordering of machines and background work has been done, so I believe the plant should get completed in or before Q4FY22.

Disc. - Invested

6 Likes

Any specifi reasons why company is 15% up a day?

Anyone tracking this?

There is an overcapacity for Indian domestic market for camphor. Since camphor and related business comprises ~30% of OAL, it has moved to a wait and watch position.

2 Likes

Anyone tracking OAL fundamentally and sees an opportunity?? Please comment

I recently bought it my thesis on it is their net fix is increased from 270 to 443 they normally get net fixed turn over of 3 which makes a sale of 1329

Took 15 percentage as a margin finally doing all the thing got 120 of net profit as per my target I can give 3-4 year for cycle to play took forward exit pe of 25 it can give 18 to 25 percentage of return , second it also gives a technical entry to. plz share your thoughts

4 Likes

@Mahesh Shah, a good exploration and walk through of Flavours and Fragrance @ Camphor & Allied products. I have had the patience (Hero Honda’s Punch line- Fill it and Forget it) to stay with the company right from IPO, when the greens stripes etc were predominantly decorated on the white paper in share certificates which are still available with me at my residence (temporarily I am abroad on a visit). I recall CAP was involved in producing natural products from MInt like - Mentha Oil, Menthol, and (maybe some derivatives like Cornmint Oil, Menthone, and Menthyl Acetate) apart from extracting turpentine oils etc (not forgetting Camphor made organically from Natural products).; until it was given competition from the industries which produced Mint flavours and products artificially. Organic chemistry and organic produce have a competition always ( Viz Mangalam Organics

Ltd since 1981); and the AR’s of CAP cited constraints to support their dismal performance, and cover denial of say - Dividends.

Since I was never impressed with performance of Mangalam Organics Ltd most of times, never considered switching.

Q1FY25 results update and personal opinion:

- Growth in revenue and profitability on a YoY basis.

- Slight improvement in profitability on a QoQ basis.

- Q2 and Q3 results of FY25 should also be substantially better since management has guided OPM of 10~12% for FY25 whereas FY24 OPMs for these quarters were in single digit.

- Topline should show better growth in the Q3 and Q4 as a multi-product Hydrogenation Plant at Vadodara, Gujarat commenced on 30th July, 2024 and trial runs are on at the single dedicated Specialty Aroma Chemical plant at Mahad,Maharashtra.

- If camphor pricing improves in the next 3 quarters, OPM might surprise on the upside as that division contributes one-third to the revenue and has been breaking even at the EBITDA level.

Q1FY25 Conf Call Summary [09-Aug-2024]:

- Camphor pricing improved along with rise in the RM prices

- Holding to earlier EBITDA guidance: 10~12% for FY25. Confident to meet EBITDA guidance for the next 2 quarters along with top line growth. Q4 view shall be possible around Q3 period.

- Expect revenue growth in H2FY25 as the Hydrogenation facility [Vadodara, Gujarat] shall contribute from Q3 and speciality chemical facility [Mahad,Maharashtra] will contribute in H2FY25 to the topline. Intend to run the new plants to full capacity and stabilize in 3~4 quarters after they start. Incremental depreciation from these facilities will be 8~10Cr.

- In the near term, plan to reduce debt further and utilize the capex done till now before planning for any more capex.

- Peak revenue possible at current prices and capacity: 1200 Cr.

Disc: Invested.

10 Likes

Peak debt of 280 cr mentioned for this year by management

80cr term loan and rest would be working capital supported by inventories

Looks like a very good turnaround bet with their camphor division seeing revival of demand due to festive season coming and also for the quality of their camphor.

Disc : Invested

4 Likes

Camphor prices maintain their upward trajectory even in August. Disc: Have positions and transacted during last 30 days

9 Likes

Hi Saket, are you tracking mangalam organics? Camphor prices are on uptrend since this year and B2C is in effect since some time back but Q1FY25 nos are nothing to cheer about, why would this be? Any thoughts on this? thanks