Camphor & Allied Products Ltd. ---- A Case-Study of a Silent Management, Apt in Execution.

Camphor & Allied Products Ltd. (CAP) is a perfect case-study of how an otherwise efficient, ethical and proactive management on business front can keep executing one step after another in the long term interest of the business and therefore shareholders of the company and still remain silent as far as communication with investors/shareholders is concerned.

Why I term it as a Silent Management — in company’s ARs that you read, in AGMs when you interact with them, forget painting any rosy picture, but, they even don’t highlight strongly the strengths and strong positioning of the company in each of its operational segment and infact proactively bring down your expectations in case you try to draw any high assumptions and correct your facts on each of their business segments.

This Silence is :

Despite company’s strong positioning in each of its operational segment —

2nd Largest Indian-origin player after SH Kelkar & overall 6th Largest player in niche Indian F&F Blends segment

counting elite names in its clientle like Godrej, Nirma, Dabur, Bajaj, KeoKarpin, MTR, Pfizer, Abbott, Wockhardt, Wyeth, etc. It is a key supplier of F&F blends to leading Indian brands like Godrej No.1 & Cinthol soaps, Bajaj Almond Drops Hair Oil, Nirma Washing Powder, Mediker Shampoo, etc.,

4th Largest Indian player in F&F Ingredients (Aroma Chemicals) space after Privi, Eternis & Anthea group counting in its clintle key names like IFF, Givaudan, Firmenich, Symrise, SH Kelkar & Agan Aroma, etc.,

Largest Indian player in Pharmaceutical-grade Synthetic Camphor & 3rd Largest player in overall Indian Camphor segment after Saptagir & Mangalam Organics

counting in its clientle key names like P&G, Jhonson & Jhonson, Novartis, JB Chemicals, Association Forum Auditorias (AFA), PZ Cusson, etc.. It satisfies 80 % of the camphor requirement for P&G’s most popular ‘Vicks’ brand.

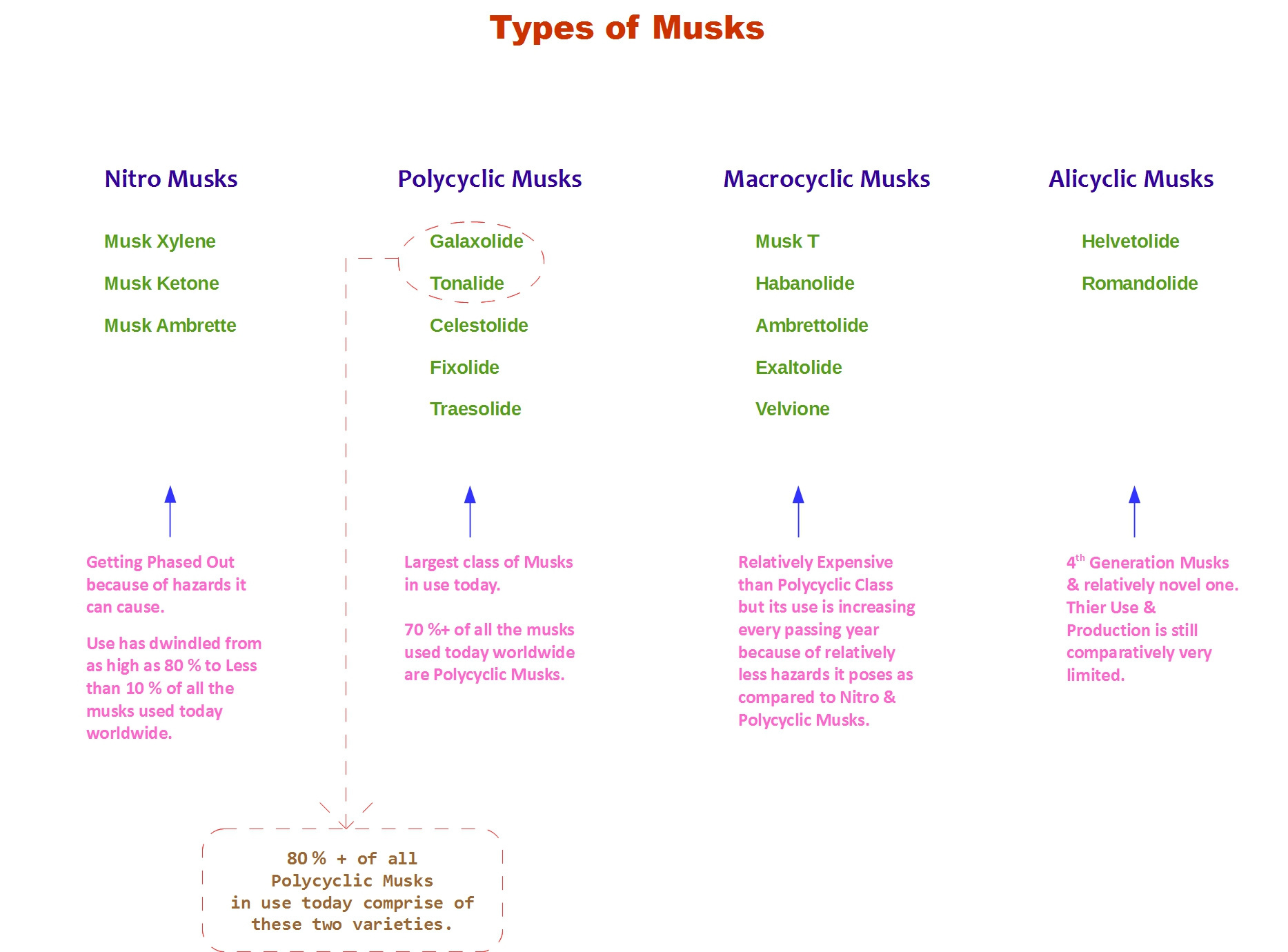

Largest player in Musk – key F&F Ingredient – segment from India enjoying ~30 % Global Marketshare of Galaxolide Musk – the most popular musk in use today worldwide.

This Silence is :

Despite majority of the operational segments having history of good profitability —

78 % of the Revenue enjoys 11 Years’ History of lowest Indicative Gross Margin of 41 % and highest Indicative Gross Margin of 52 %,

13 Years’ Average Consolidated EBITDA Margin at 10.62 %,

13 Years’ Consolidated EBITDA to Operating Cash Flow genration % at 40.5 %

This Silence is :

Despite the current New Promoters running company’s operations most efficiently as compared to that run by Old Management :

8 Years’ (FY09-FY16) Average EBITDA Margin of 10.94 % under New Management

v/s

8 Years’ (FY01-FY08) Average EBITDA Margin of 4.81 % under Old Management, and

16 Years’ (FY93-FY08) Average EBITDA Margin of 7.86 % under Old Management

Improvement in EBITDA margin is despite Macros not in favour of New Management wherein :

8 Years’ (FY09-FY16) Average Gross Margin was 31.89 % under New Management

v/s

8 Years’ (FY01-FY08) Average Gross Margin of 37.66 % under Old Management, and

13 Years’ (FY96-FY08) Average Gross Margin of 38.08 % under Old Management

8 Years’ (FY09-FY16) Revenue CAGR of 16.33 % under New Management

v/s

8 Years’ (FY01-FY08) Revenue CAGR of 4.38 % under Old Management, and

16 Years’ (FY93-FY08) Revenue CAGR of 2.91 % under Old Management

8 Years’ (FY09-FY16) Average RoE = 12.95 % & Average RoCE = 13.06 % under New Management

v/s

8 Years’ (FY01-FY08) Average RoE = 3.94 % & Average RoCE = 3.49 % under Old Management, and

16 Years’ (FY93-FY08) Average RoE = 6.69 % & Average RoCE = 10.03 % under Old Management

Now, this is called the Silent Execution. And the effect is, CAP, on a post-merger, fully expanded equity capital basis currently trading at TTM :

EV/EBITDA = 10.90x

EV/Sales = 1.44x

P/E = 15.98x

P/BV = 2.26

So, now, let me give a brief background as well as story as I see unfolding for the company :

Company Background & History :

– Incorporated in 1961, CAP is one of the pioneers in terpene chemistry in India. It was the first company to set-up a Synthetic Camphor plant in India in 1964 with technology from Dupont, USA.

– Established in 1974, in huge 40 acre land at Baroda, Malti-Chem Research Centre signifies company’s prime focus on R&D.

– In 1999, company ventured into manufacture of specialty F&F Ingredients (Aroma Chemicals) via in-house developed technology developed at its own R&D Centre.

– In 2009, change of promoters/management took place wherein CAP was acquired from then promoters – Dalal Family by current promoters – Bodani Family via their flagship company Oriental Aromatics Ltd.

– In 2013, by using the expertise and reach of new promoters, company undertook a major expansion of its F&F Ingredients’ manufacturing capacity to the tune of 155 % (1.5x) and ventured into production of Galaxolide Musk with Technology & product-Marketing support from Agan Aroma, an Israel based company pioneer in Aroma Chemical industry. It set-up one of the world’s most advanced Polycyclic Musk manufacturing plant and captured ~30 % of the global marketshare of Galaxolide Musk within a span of just 3 years.

– In 2014, company inked a long-term manufacturing and supply agreement with International Flavors & Fragrances Inc. (IFF) – 3rd Largest player in Global F&F industry enjoying 12.50 % marketshare of world F&F market – to manufacture and supply Fragrance Ingredients’ Intermediates and Finished Products.

– In 2015, company acquired certain indentiified assets & liabilities of Arofine Group (Arofine+Vaishnavi) — a group incorporated in 1976 with 4 state-of-the-art specialty F&F Ingredients’ manufacturing plants in Dombivali & Ambernath, Maharashtra for a consideration of INR 17.50. cr. Arofine Group was an existing supplier to leading global F&F companies like IFF, Givaudan & Symrise and had expertise to manufacture ~200 high value specialty F&F Ingredients. Two key promoters of Arofine Group joined CAP as CEO & R&D Head of newly formed Specialty Chemical Division.

– In 2016, company undertook an expansion in F&F Ingredients manufacturing capacity to the tune of 18 % (to be commissioned in Q1FY18) at a cost of INR 40 cr.. Expansion is into high value specialty F&F Ingredients (inline with that manufactured by Arofine Group) space – used majorly by MNCs in premium FMCG products’ & Fine Fragrances.

– Also, in 2016, promoters decided to merge their only flagship company – Oriental Aromatics Ltd. – with CAP in lieu of increasing their stake in merged listed entity from current 57.66 % to 74.16 %. NOC from stock exchanges is already received and application filed in Bombay High Court on 26th October 2016 – all formalities expected to get completed by Q4FY17.

– Incorporated in 1973, F&F Blends business (which is to be merged with CAP) enjoys second largest Indian-origin player status in Indian F&F Blends segment after SH Kelkar and overall sixth largest player status in Indian F&F Blends space after MNCs Givaudan, IFF, Firmenich & Symrise.

– F&F Blends business of CAP has sustained its positioning amidst onslaught of rising presence of MNCs in Indian F&F space as also emergence of numerous small private players over last 10 years which saw many Indian players getting wiped out completely and loose considerable market-share.

Industry Details :

Attached is a pdf file giving almost all the details of Industry of operation of CAP from varied angles. Contents of the file are :

Industry_Details.pdf (355.1 KB)

CAP – Revenue Breakup

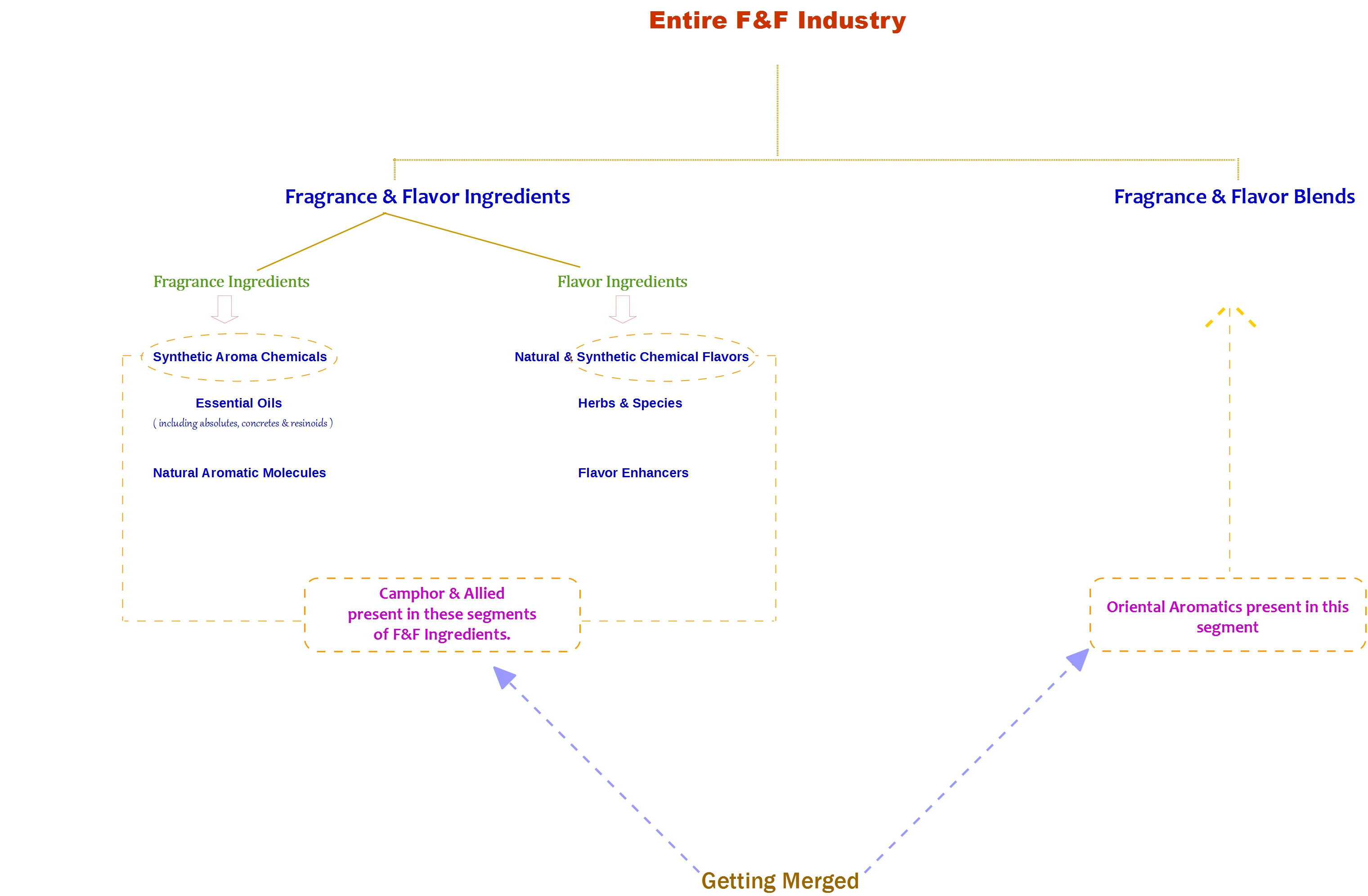

Entire F&F Industry Breakup – Key Segments

Entire Industry Cycle – Key Players in each Segment,

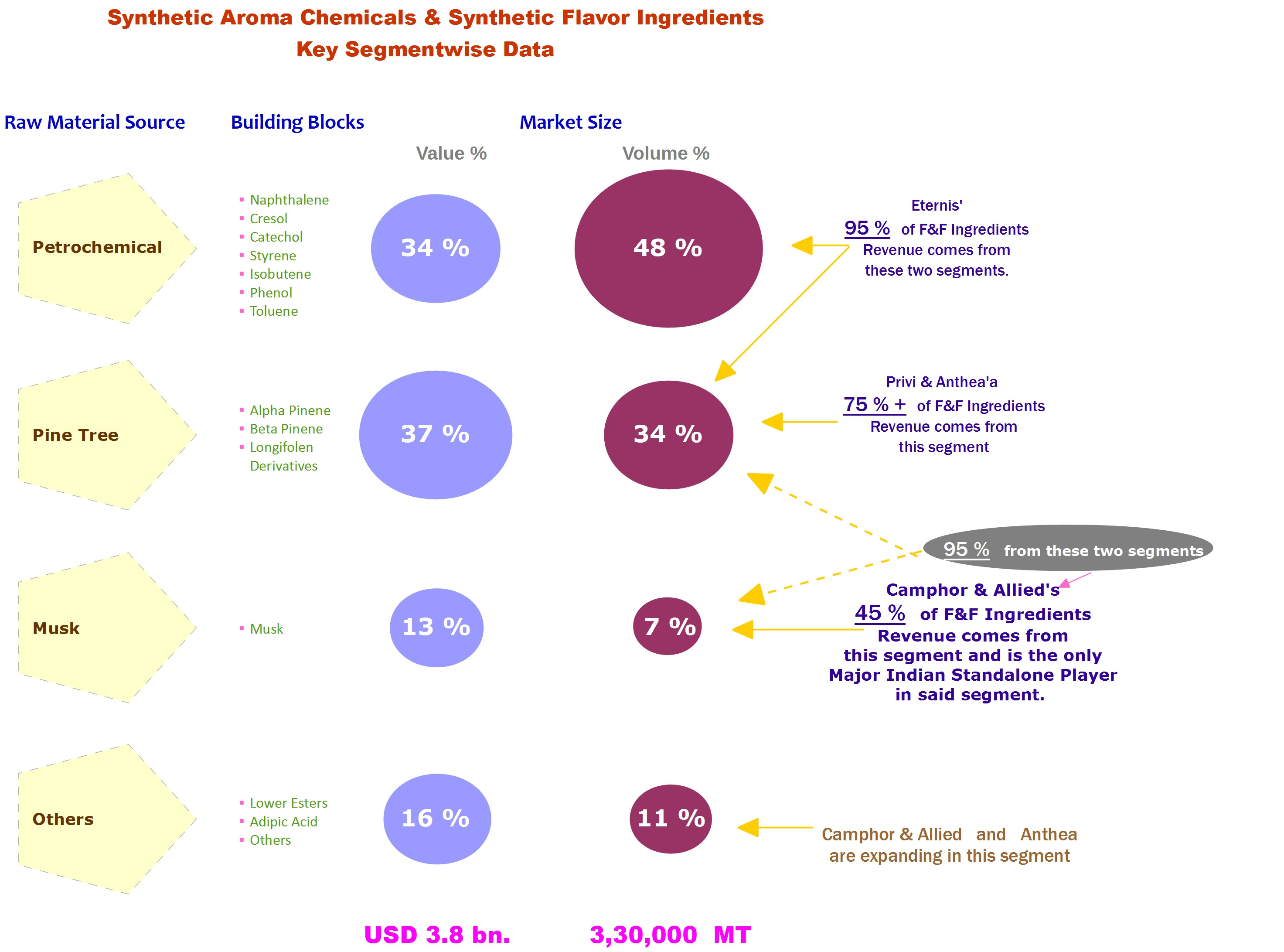

Synthetic Aroma Chemicals & Flavor Ingredients – Volume/Value % wise breakup according to RM Sources

Who Manufactures & Why ??,

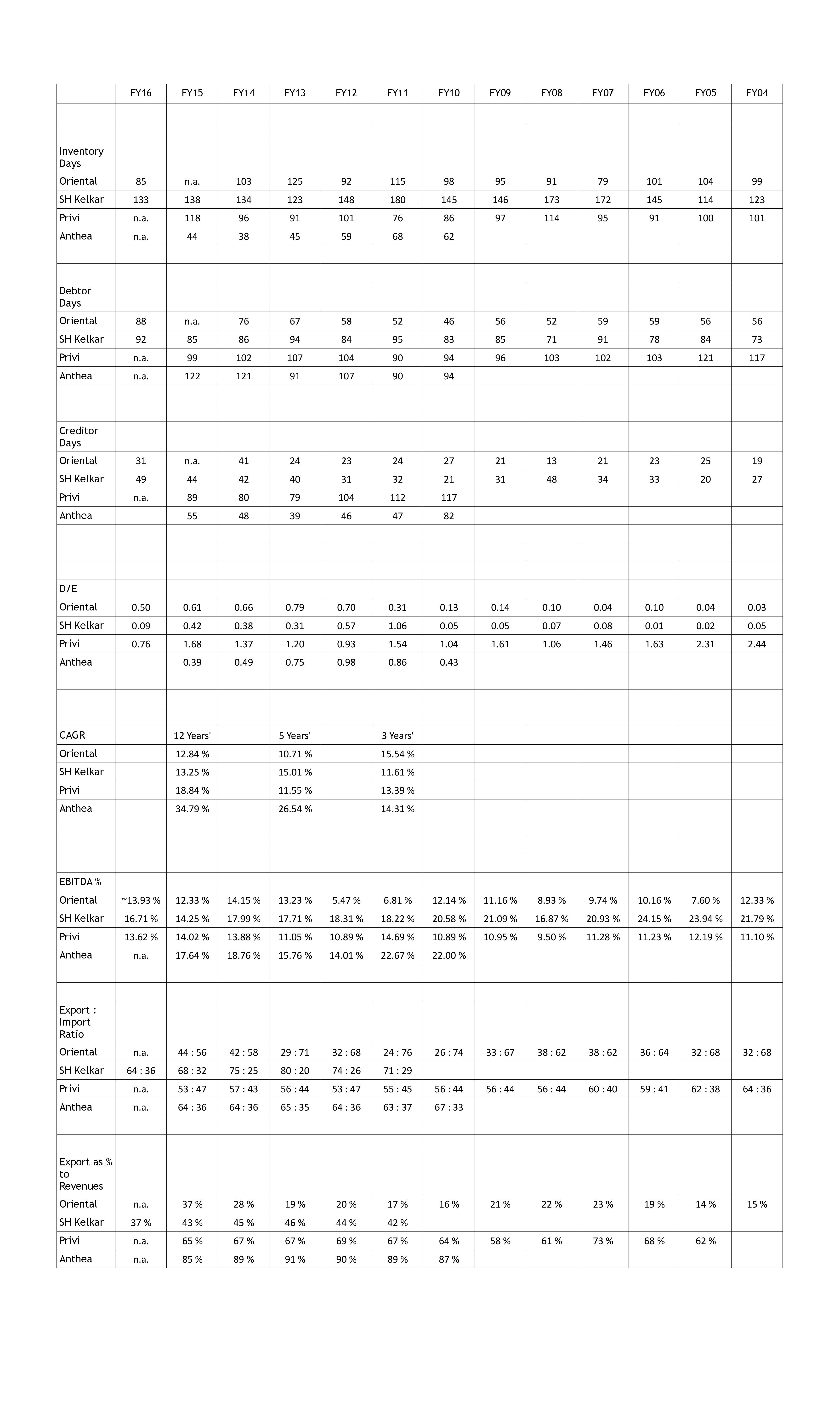

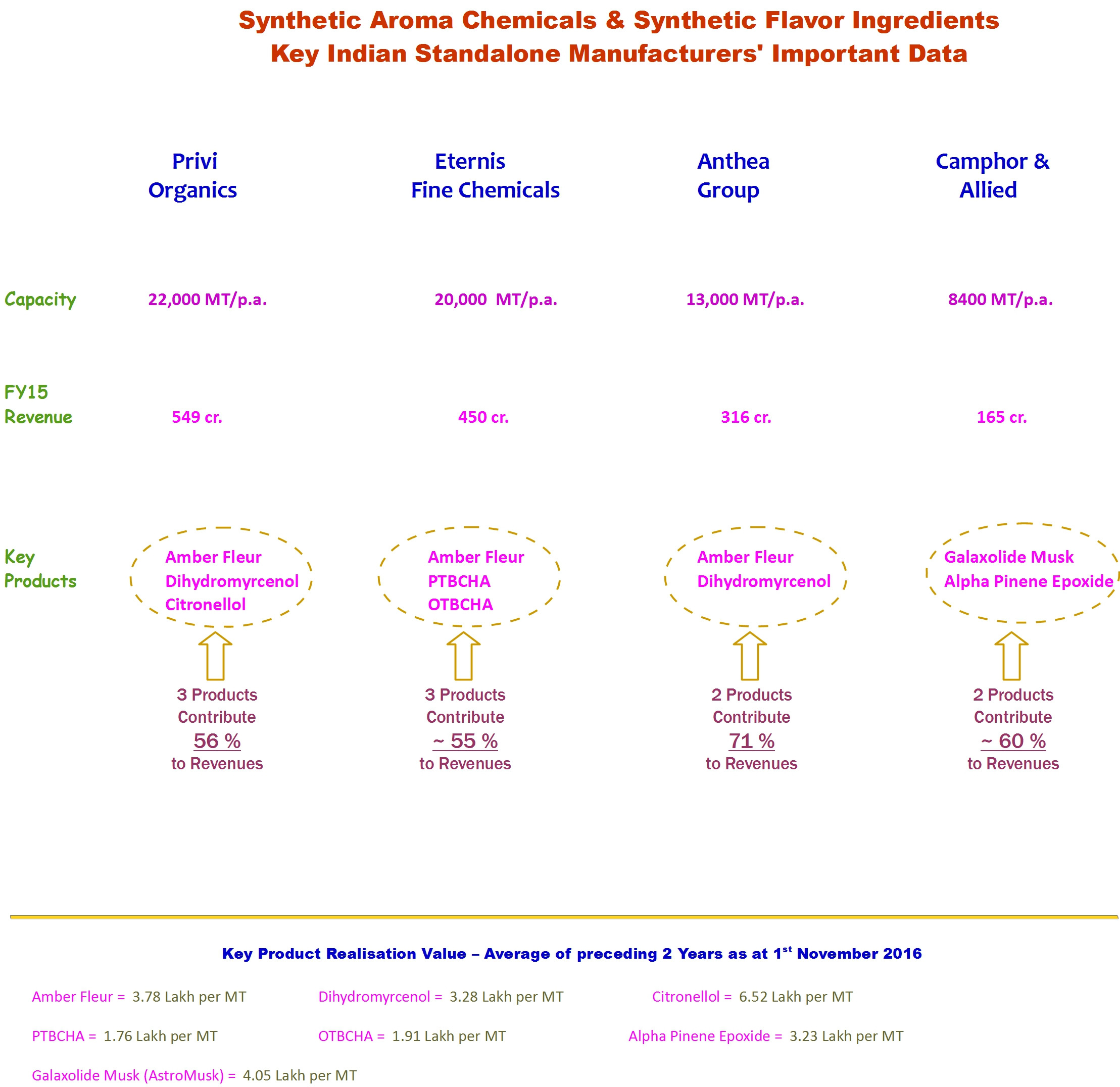

Key Standalone Manufacturers Important Data (Privi, Eternis, Anthea, CAP)

Musks – What They Are & Their Importance to Fragrance,

Types of Musks,

Positioning in Musks Segment of CAP,

F&F Blends Industry – Why Clients are so Sticky ??

Indian F&F Blends Market – A 10 Years’ Perspective --,

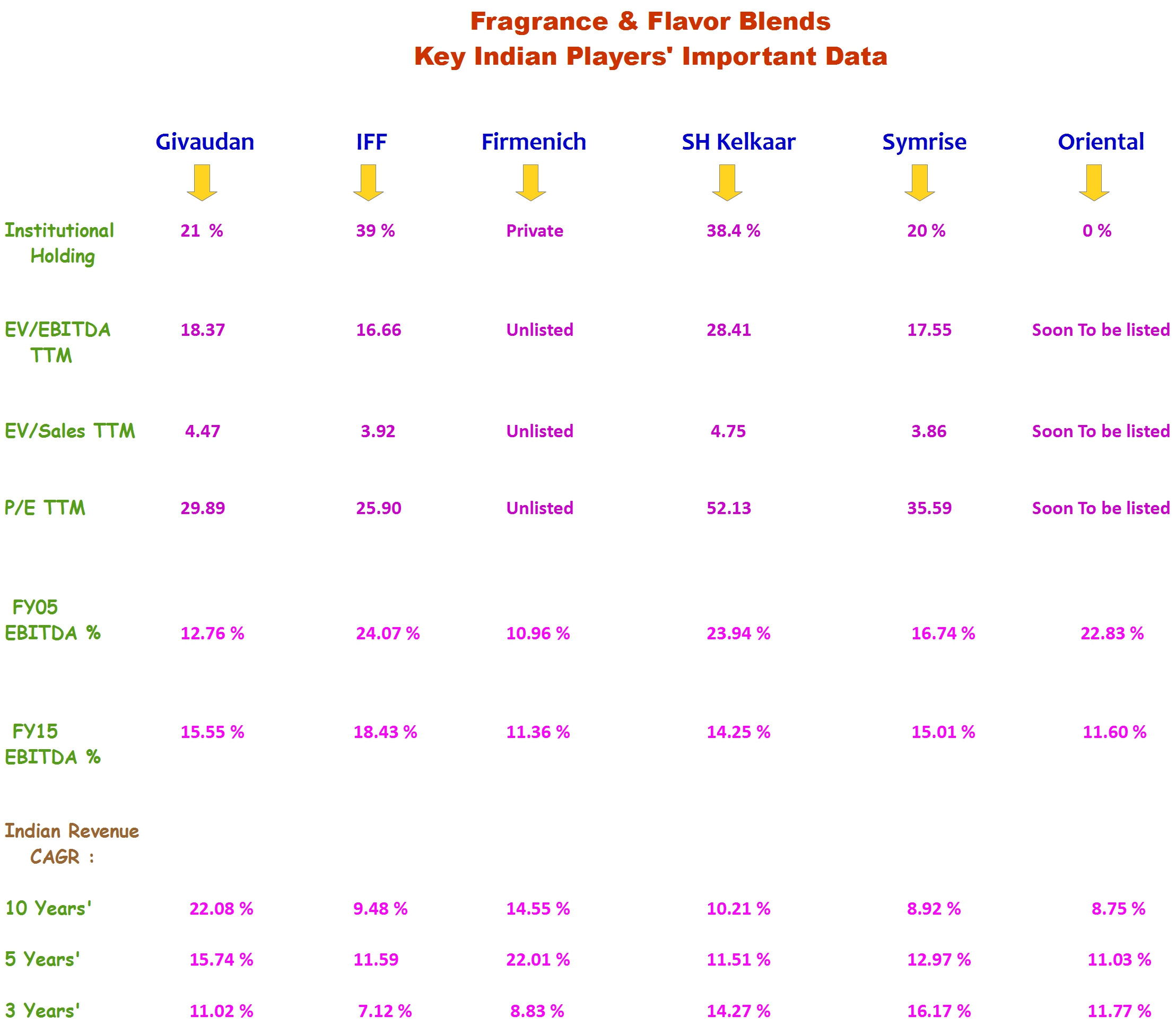

Key Indian Players’ Important Data (Givaudan, IFF, Firmenich, SH Kelkar, Symrise, Oriental),

F&F Blends Industry – Bariers to Entry,

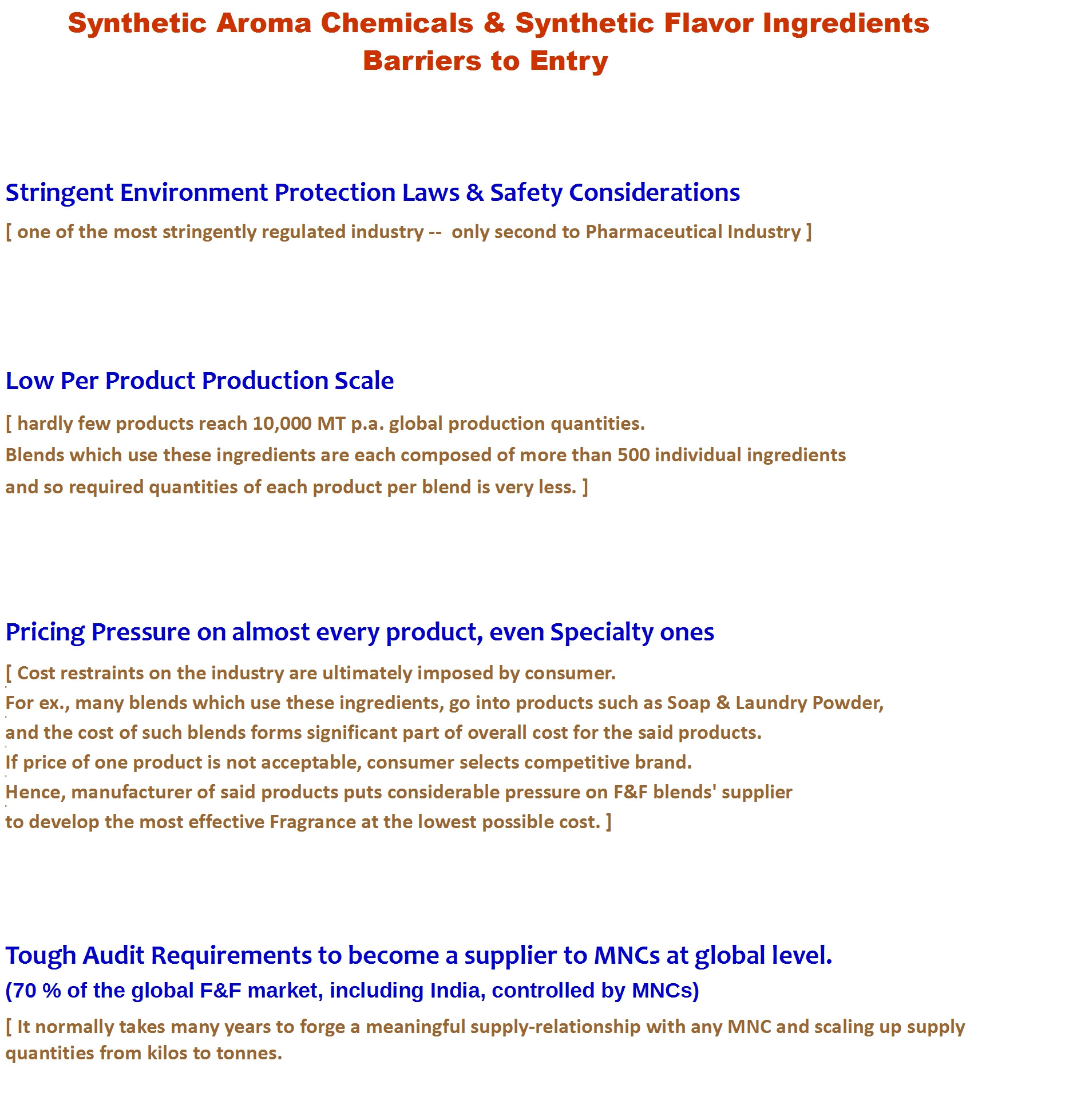

Synthetic Aroma Chemcials & Flavor Ingredients — Barriers to Entry,

CAP – Aroma Chemcials Factsheet,

CAP – F&F Blends Factsheet,

CAP – Synthetic Camphor Factsheet,

Key Indian Players’ Important Data (Managalam, Saptagir, Kanchi & CAP)

Some important excerpts from above pdf file are attached below for ready reference :

Company Details :

Attached is a pdf file giving almost all the key details of company’s businesses from varied angles. Contents of the file are :

COmpany_Details.pdf (182.1 KB)

**Positioning of the Company in Each Segment **

CAGR figures of all the peers of each segment,

16 Years’ Indicative Gross Margin of Key Business Segments,

Strategy Adopted by the Management for Each Segment,

12 Years’ EBITDA & GM % of SH Kelkar v/s Oriental Aromatics,

Land Asset Value & Replacement Cost Analysis,

SOTP Valuation,

** Genuine, Ethical & Efficient Management**

Now, after referring to above two pdfs, some questions, which as an investor I ask myself :

– Won’t this forward integration in F&F Blends space make CAP one of the strongest player, as also, the only second player in the listed space (after SH Kelkar) via which one can have exposure to growing niche F&F Industry ??

In recently presented paper (September’2016) at one of the most popular international F&F event in Italy, --‘Fragranze’–, Indian fragrance market alone is expected to grow at a CAGR of 11.94 % over next 5 years and is the centre of attraction of all International players. SH Kelkar has already given a guidance to grow its revenues over next few years at a CAGR of 15 %.

Top 10 players in Indian F&F Blends space are Givaudan, IFF, Firmenich, SH Kelkar, Symrise, CAP (via Oriental), Mane, Aarav, Goldfield & Ultra International – exactly in the same given order with Givaudan being No. 1 player and Ultra International being No. 10 player. Out of these, Givaudan, IFF, Firmenich, Symrise & Mane are MNCs.

– Isn’t CAP, with its forward integrated business approach better than standalone Aroma Chemical players like Privi Organics which have a backward integrated business approach and are ultimately dependent on players like CAP (Blends business) for growth ??

– Isn’t CAP the only play available which offers a balanced exposure to both the high growing segments of F&F Industry – viz., F&F Blends as well as F&F Ingredients — SH Kelkar offers exposure to growth opportunities of F&F Blends space as its F&F Ingredients business (via PFW Aroma) is not a focus area atall whereas Fairchem Specialities (Privi Organics) offers exposure to growth opportunities of F&F Ingredients space (aroma chemicals) with no presence in Blends Formulation.

– Won’t inhouse manufacturing capability of 60 % of RM used make CAP’s blends business much more efficient and will give its clientle much more confidence in it than others. Infact, even SH Kelkar lacks such capability and post Baroda expansion, CAP will likely be the only Indian player which will have such capability. This is not to say that CAP will become superior to SH Kelkar, not atall,-- SH Kelkar has a robust R&D Infra and set-up which no peer can compete with for years to come (in F&F Blends space). However, after SH Kelkar, CAP will be the second best choice for any clientle and with these capabilities, CAP can expect to pitch for contracts directly in competition with SH Kelkar.

– Won’t the Gross Margin of Blends business will significantly improve because of internal procurement of majority of RM.

– Tie-up with IFF has so far not contributed meaningfully to CAP financials – so, aren’t Arofine acquisition as well as commissioning of Baroda-expanded capacities the building blocks for this tie-up to start bearing fruits from FY18 onwards ??

– Company has so far refrained from any sort of equity dilution over last 16 years – whether its old management or new one — infact, it is interesting to note that even new promoters’ family have never diluted equity in lifetime of their flagship company Oriental Aromatics Ltd. despite many ups and downs of the industry . So, will the rise in promoter holding to 74.16 % (from current 57.66 %) post merger will act as an incentive to dilute equity going ahead.

– Won’t 74.16 % holding change the silent approach of the management and make them more proactive as far as IR communications goes.

– Won’t the extremely successful listing and widespread institutional participation of the only other big Indian peer – SH Kelkar — prompt the management to have proactive talk with institutional investors and therefore improve on IR disclosures.

There are also some questions that arise on risk side :

– What if tommorow Galaxolide Musk is banned ?

– Current demonetisation is surely going to have some sort of impact on Q4FY17 financials (Q3FY17 might not be that impacted as there is usually 30-40 days lag period) since majority of clientle will be getting impacted. However, players like SH Kelkar and CAP will be better placed as they have clientle diversified across all industries ranging from Soap Manufacturers to Agarbatthi Manufacturers to Perfume Manufacturers to Ready-to-Eat Manufacturers.

– Mr. Trump becoming president – will he completely ban imports (a wild guess) and therefore one of the prime market for Aroma Chemicals might be in trouble. However, here too, SH Kelkar & CAP will be least impacted relative to all other peers because of their extremely low exports. SHK & CAP exports as % to sales is at 37 % v/s peers’ 65-70 %.

– Only Listed on BSE & Illiquid nature of company’s stock.

Discl. - Invested in Camphor & Allied Products Ltd. Bought in last 30 days.

Note :- This is part of a general discussion and is not a Buy/Sell/Hold recommendation of any kind. Here, Factual Statistics regarding varied sectors like Aroma Chemicals, Flavors & Fragrance & Camphor are presented and discussed and in no way this should be considered or interpreted as recommendation or advice of any kind. This discussion is to be used only for further analysis purpose of each of the segment discussed and not otherwise.