I also have a minor position in OBL at current levels. Plan to add more on dips. Initially read about it on the value picks blog and bought it after reading the AR. Missed the boat on favourites like Kajaria and Cera. Mgmt seems to have integrated Bell quickly and for reasons that you have mentioned above this looks promising to me as well.

I have been getting good inputs from couple of good investors. However, I’m quite concerned on the low ROEs over last many years and the highlycompetitivenature of the industry. Everyone is trying to search for next Kajaria in this area but soon all the cos are trying to replicate what Kajaria did to get better than industry returns.

Would be great to hear your thoughts on the margin picture etc.

I had been excited when they had Orient ceramics had announced buying Bell ceramics as the combined capacity was the highest amongst the ceramics players. But had exitted as the stock never went anywhere.

Subash, I saw only about 150000 to 20000 of volume in last few days (Moneycontrol.com), while the float is about 4000000. I dont know much about technincals, does it meanaccumulation?

There have recently been some changes in the balance sheet of this company. Also post the merger with Bell ceramics, it seems to be in interesting position at the moment. I have made a small write up on the same

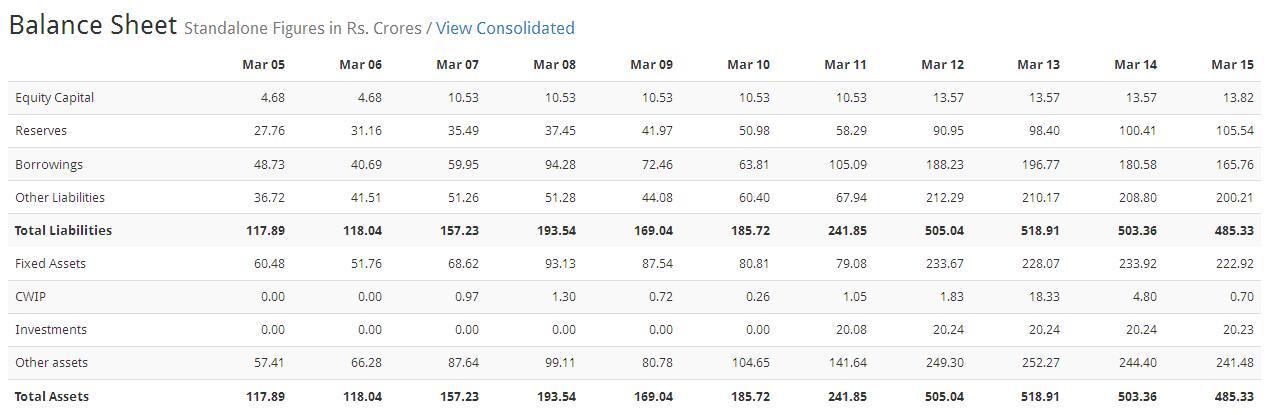

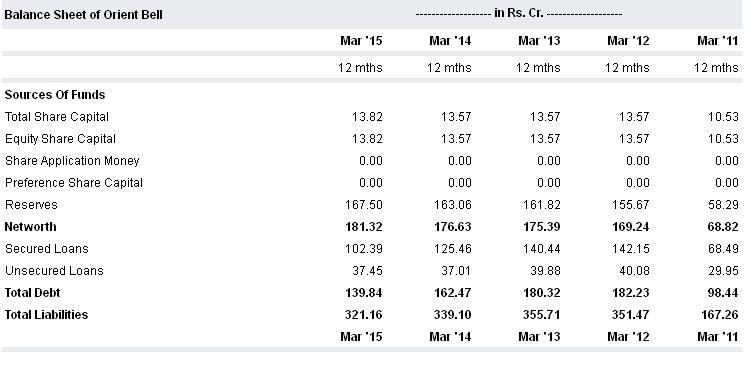

Orient Bell manufactures Ceramic tiles. It has the second largest in-house capacity of 24 msm. It bought Bell ceramics a couple of years ago. This acquisition increased the company’s debt dramatically.

• Market cap = 160cr.

• Average operating cash flow (4 years) = 50cr

• Promoter holding = 74%

• Working capital number has reduced 95cr. to 77cr in 4 years

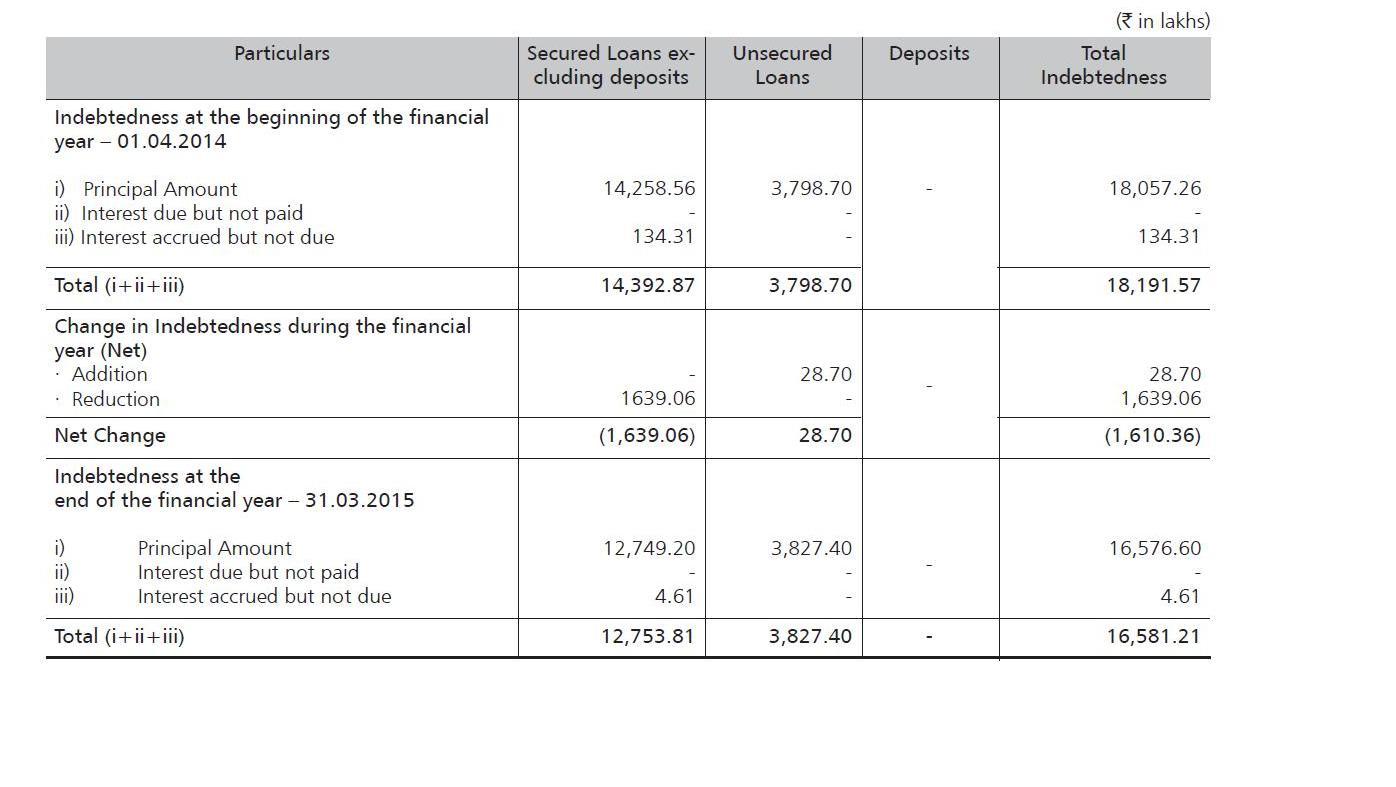

• Debt has reduced from 182cr. to 139cr. in 4 years

Positives

Moving up the value chain - The company is planning to open ‘Orient Bell’ stores and become a branded player.

The acquisition has dramatically increased its distribution network. As of now it has 4500 dealers, 120 specialized stores and 25 depots

Profits have been subdued as the company is investing heavily in re-branding, store opening and re paying its debt

OBL plans to selectively outsource manufacturing and increase its focus on advertising. This will be done for the high value digital and vitrified tiles

Company has applied for 4 patents

Trend from unorganized to organized (Moved from 60% unorganized to 50% unorganized in last 3 years)

Crisil has marginally improved its debt ratings to BBB+ stable. IN fact OBL plans to repay its majority long term debt in 2 years

In the last quarter sales volume has increased by 11%, which shows a fundamental demand

Negatives

Demand affected by construction activities

Competition from imports = But China consumes most of what it produces domestically. Also OBL is heavily investing in point of sale advertising, strong sales force and new designs

orient bell will derive much more benefit from falling crude as they use LPG for manufacturing at Bangalore(Rural) plant and LPG cost has come down much more than RLNG

Reducing debt and reduction of interest rate .

JV/ outsourcing model if successful can reduce future capex requirements

Concerns :

with slowdown in real estate activity , business growth may slow down.

Kunal, yes the real estate slowdown is a concern. But just look at the market cap and compare it to the other ceramic players. If it continues with 50cr profit and pays down most of its debt, there could be a significant re-rating here. With its distribution power, this is no small company.

Two bonuses are the JV model and the branding. If any of these bear fruit, we could see significant changes in the ROCE of this company.

Even without this, sales have grown at 20% cagr over a 10 year period. Also the company has for the first time started to communicate in the form of Investor presentations. A subtle sign, maybe? And in 2015 the company promoters have bought back shares around the value of 1cr. Not significant, but already the promoter holding is close to the limit of 75%

akshay let me disclose first ,i hold orient bell but it is less than 5% of my portfolio. so let me clarify i am bullish b’cos of cheapness and some other factors mentioned above but we have to be realistic when we evaluate stocks we hold.

50 cr. profit i dont know how did u get that figure . it is at best OP and u must deduct interest and taxes. ( u may count dep. and PAT for interest repayment)

real estate slow down is valid concern as u pointed out.

20% sales growth was due to acquisition of bell ceramic and they diluted equity for same and had taken debt and still paying large part of EBIT towards interest charges for same.(with hindsight we can say that if they did not acquire bell and had JV/outsourcing as kajaria did they would be in much better shape )

I am talking about the more important number here, operating cash flow here and not net profit. The number ranges from 45cr. to 55cr in the last 4 years

Yes you are right about the acquisition part. But lets take the sales numbers before acquisition. 111cr in 2005 to 291cr in 2011. This equates to a cagr of 15% over 7 years, which is a reasonable rate of growth right?

I personally think the acquisition was not a sensible one back in time. Yes they did dilute and did increase debt. But you can also see some advantages. Distribution and branding opportunities to name a couple.

Just look at the balance sheet post acquisition. Debt, working capital and cash positions have improved in the last 4 years.

btw just got an update that they have launched a new website: www.oblcorp.com.

akshay cant understand approach of taking operating cash flow to value business with debt. in this way all GMR , GVK, Lanco , Relaince Power and JP would be invesment candidate in 2011-12 . when a business is debt funded, cost of fund must be considered as normal expense.

my case was business growth was less than 20% which u say was 15% on lower base and when business environment was more conducive now we cant extrapolate same rate in future

i am posting here balance sheet (screener.in snapshot), cant find anything extraordinary. Debt reduction from fy12 is from 188 cr. to 165 cr. that is not so great when u have no rise in net block which was 233 cr. in fy12 and it is 223 cr. debtor days have been steady at 45 days since last 3 -4 years .

Finally do you have any projections of sales growth and EBIDTA and PAT . would like to see your expectations.

Kunal, You can’t compare this case with the names you mentioned unless they use that cashflow to reduce debt. After the debt reduces, the cash flow remains (and hopefully grows, if its a growing business)…Lets fast forward a bit…Just assume, the 50cr cash is used to pay down down only. After about 3 years, what remains is a business valued at 170cr earning 50cr of cash with no debt, on a recurring basis…If future business remains debt funded, or the debt increases further - this may not hold true…Which means we need to re-analyse the business model and figure why they need so much debt (not making it a good business to be in)…

I am not saying 15% was on a lower base…15% was before the acquisition

With regards to the balance sheet, the numbers mentioned are not present on the snapshot you have provided. Please see moneycontrol.com or any other website which has separate sections for overall debt, working capital and cash…You will find the trends over there…Please include FY15 numbers too…For example debt has reduced from 180cr to 139cr

akshay my point is that 50 cr. of operating profit will not go in to debt repayment. u have interest of 20 cr. that u have to pay . and income tax on PBT and u have maintenance capex . i am being very liberal here because i am not even talking about depreciation here.

again sales growth is not 20% even after acquisition sales rose from 546 cr (fy12 ) to 693 cr.(fy15) it is at best a 10% growth and anyone will agree that last 3-5 years environment was much better that current one.

Finally it is difference of opinions that make market . i am holding shares and want them to move up but i like to have reality check of business which i own so i can sell them at right time.

just posting a recommendation on Orient Bells from Financial Express.

Orient Bell

CMP 165

The company is into manufacturing of non-Vitrified and Vitrified tiles as well as sanitary products. The company acquired and merged with Bell Ceramics in December 2010. Post this merger, the company has emerged as the only one in the industry to have plants in North, West and South of India. The merger has been a good opportunity and will enable the company to grow inorganically at a much faster pace.

Investment Rationale

Strong government thrust: The government’s thrust on improving sanitation system in India has provided a new growth opportunity to the Indian sanitary ware and ceramic tiles industry. According to ‘India Sanitary Ware Market Forecast & Opportunities, 2017’, in the coming years India will witness huge improvements in the sanitation level. The industry is already growing at a fast clip and it has huge potential due to under-penetration. The industry is likely to witness high growth for at least the next 20 years before it saturates. Over 60% of the Indian population does not have proper bathrooms and toilets, and in the remaining 40%, the share of the organized industry is negligible. Implementation of GST is likely to provide a major fillip to the earnings potential of organized players like Orient Bell.

Disclosure : Not invested as of now/ Planning to invest on this stock,

EBITDA Margin on sales has reduced to 7.6% for 9M of current year. There seems to be pressure on margin despite claim of moving up in value chain. Sales through JV also reduced by 5.2% during 9M of current year as compared to corresponding period of last year. Business model of the company is still not giving good results.

Further, AR 2017 shows some small related party transactions in form of loans which shows lack of professionalism. Are such transactions were done to cover any mismatch in cash flow.

)

)