OBL reported strong set of nos. for the 2nd quarter led by 22% volume growth & 6% value growth.Their investor ppt has excellent details:

The concall ended recently.Some highlights:

→ Continue to see robust demand,ASP is moving up on a monthly basis.30-35% of ASP improvement is on account of price increase rest is higher value tiles.

→ Some years back players at Morbi had got together and indulged in undercutting the market.Most of this was due to non-compliance with tax regulations resulting in lower cost.However,the situation is the polar opposite now & mgt doesn’t see organised players losing ground at all.See no risk of them coming back in the market even with export issues.

→ Company continues to have 90% own manufacturing+JVs,while only 10% is outsourced.The decision on this is taken based on the make of tiles being sold and in demand.

→ Feel Indian tile market is huge and don’t intend to diversify into ancillaries.Export market will fetch low margins if outsourced from Morbi and company has no intention to focus much on that market with own mfg.

→ Added 128 channel partners in Q2.Brand spends have gone up by 2x vs. last year.

→ Opened 23 new OBTBs,shut down 12 poorly performing ones.Thus,net addition of 11.Demand is strong leading to blistering pace of opening.

→ Company continues to improve cost efficiency but major delta in margins will come with higher topline.With current capacities,company can do 200 cr. kind of quarterly run-rate with own mfg.

→ H2 is always better than H1 and even Q2 is one of the leaner quarters.While management has given no concrete guidance,Q3/Q4 being strong quarters looks highly likely(ex- of Covid)

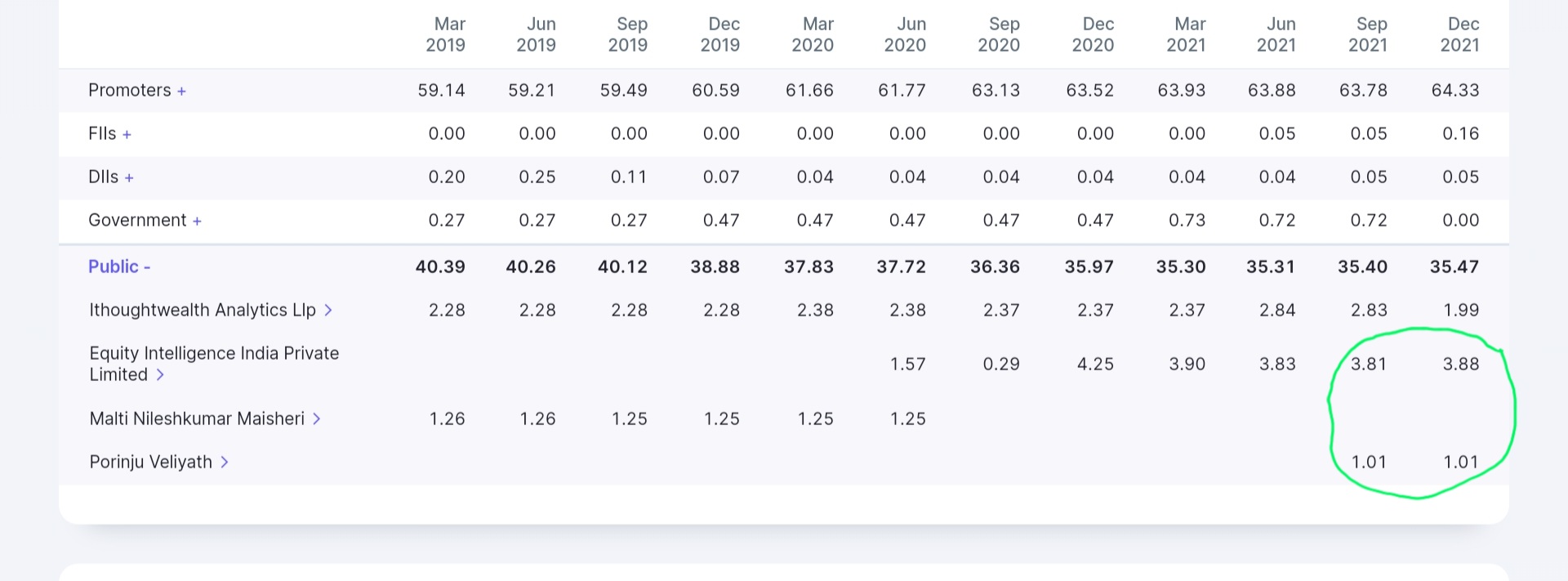

Overall,the management continues to execute well with focus on improving product mix and being cognizant of working capital.Given the scope to improve margins I feel stock looks very good here.8 cr. PAT in a lean quarter should only inch higher in coming quarters.At a marketcap of ~500 cr. and net cash B/S this continues to be one of the cheapest organized tile plays.In Q2,there was a lot of small,small promoter buying as well.

Disc.: Invested.Views are biased.

- Orientbell Tiles")