Business Details:

-

About company: Oriana Power is a company that specialises in providing solar energy solutions to industrial and commercial customers.

-

Services & products: We offer low carbon energy solutions by installing on-site solar projects such as rooftop and ground-mounted systems, as well as off-site solar farms i.e. Open access.

-

Business Model: Our business operations are primarily divided into two segments: Capital Expenditure (CAPEX) and Renewable Energy Service Company (RESCO).

-

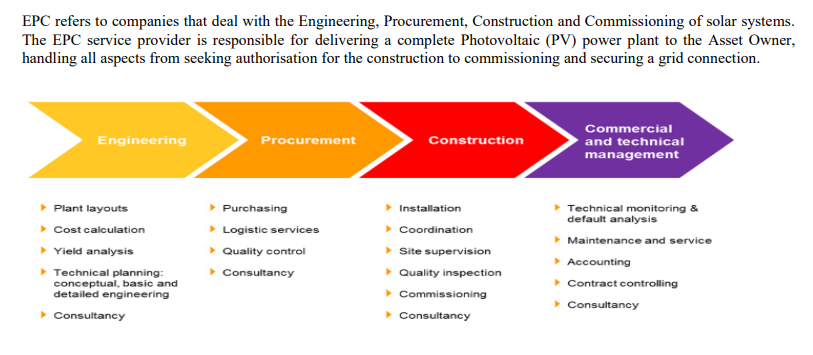

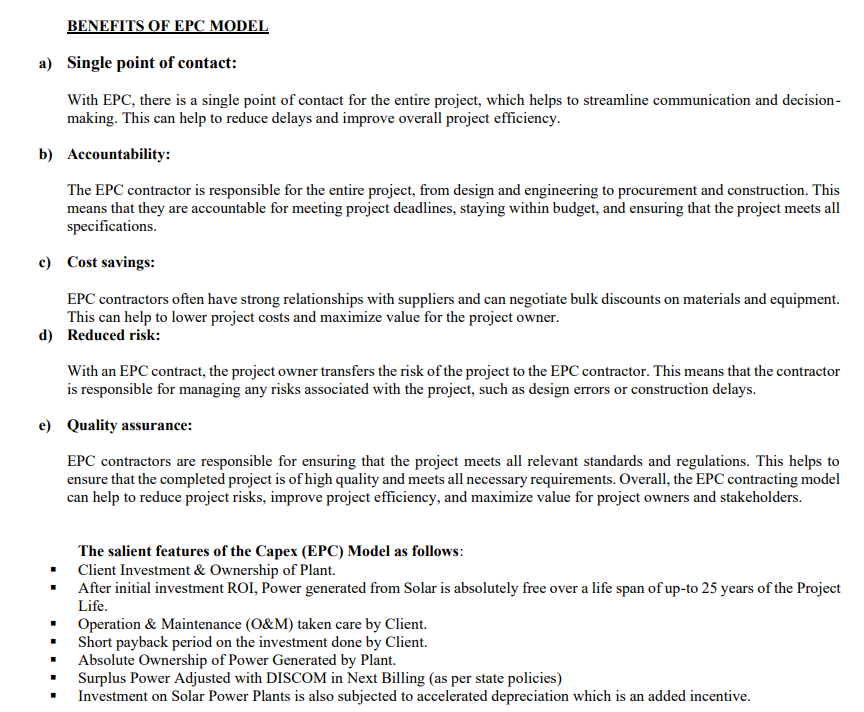

Capex Model: Under the CAPEX model, we offer Engineering, Procurement, construction, and operation of solar projects. In this model, customers invest in the Capital Expenditure on their own & Oriana does Engineering, Procurement, Construction, and Operations on behalf of the client. This model may be executed in various manners such as rooftop and ground-mounted systems, as well as off-site solar farms.

-

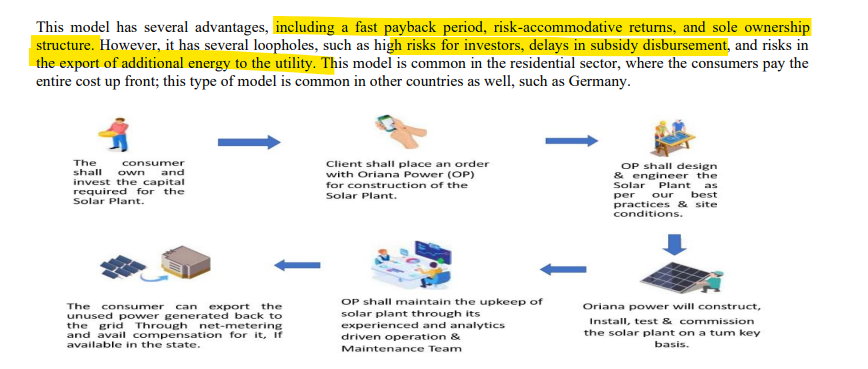

Benefits of Capex Model: The consumer is responsible for the risks associated with the operation, management, and maintenance of the system. Often the consumer finances this through bank funding. The owner can apply for the capital subsidy provided through the CFA (Central Financial Assistance) and additional subsidies provided by the respective state governments. However, in this model, the owner has the maximum risk.

-

Realisation on setting up 1 MW solar plant: Based on below comes around 4 crores/MW.

- Cost of electricity under capex: Cost of Unit electricity is approx. less INR 2.0 for over 25 years,huge cost savings adjusted for the initial investment of setting up the plant.

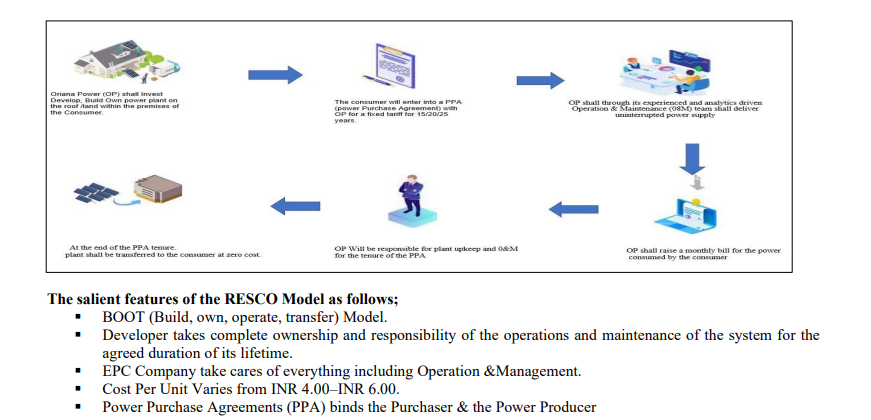

- Under the RESCO model also known as the OPEX model or BOOT (Build, own, operate, transfer), we operate through our 17 (seventeen subsidiaries). Our subsidiaries provide solar energy solutions on a BOOT (Build, own, operate, transfer) model basis, allowing our customers to enjoy the benefits of solar energy without the upfront investment. All the Investment, Commissioning and maintenance are done at our end and in lieu of that our company sells power to the end consumer through a Power Purchase agreement generally agreed for 25 years. This Business gives us Annuity income post recovery of Initial investment. However, the challenge is mobilising low-cost capital for meeting the requirements of system deployment.

Capex or cost involved : 4.5 cr for 1 MW of solar plant.

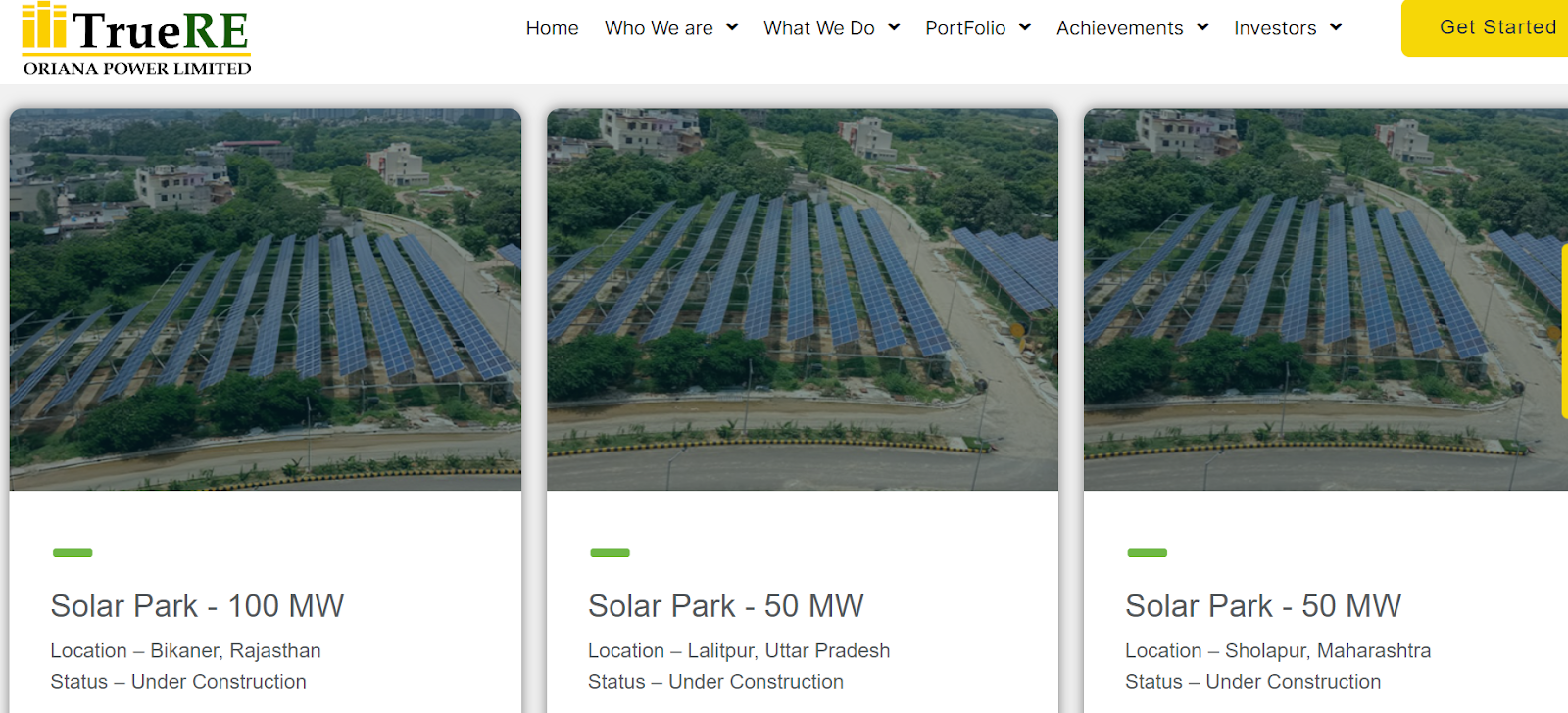

- Deliveries: Under the Capex Model, it has delivered projects with capacity exceeding 100MWp .

- Orders in pipeline as stated by company during IPO filing:Our continuous efforts for our development and expansion can also been justified by the list of projects which are in hand or are in the pipeline of its execution, or where our company has been duly empanelled, to name few:

We had an EPC project portfolio of more than 80 MW across India and Africa which combined 4+ MW of projects under floating solar, 13+ MW projects in ground-mounted and 55 MW+ projects in rooftop.

- Order wins since listing: Total Now, Orianapower declared that this year they did 350 cr of revenues so in H2 they did 290 cr of sales vs 60 cr in H1.

Orderbook was 900 cr+ on 1st march 2024 and with today’s order of 325 cr, it should stand at close to 1235+ cr.

-20MW Coal India Jharkhand ( 138Cr)

-7MW cement Co Rajasthan(34.3Cr)

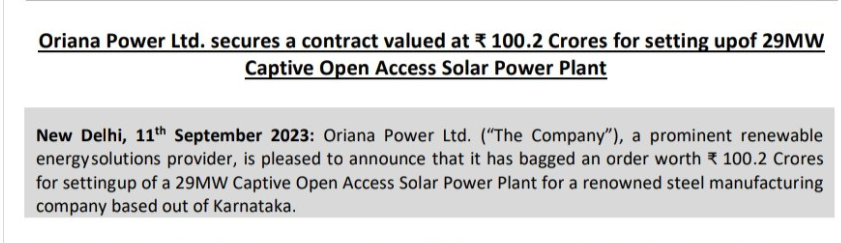

-29MW Steel Co karnataka(100cr)

-7.4MW ( 4 orders in up,Delhi, Rajasthan)

-They are getting into CBG including the recent one for 56 crores.

-

100 Cr. order win for 29 MW solar EPC work @3.44 crore/MW.

-

-200MW order under implementation (RHP)

- Clients under Capex Model:

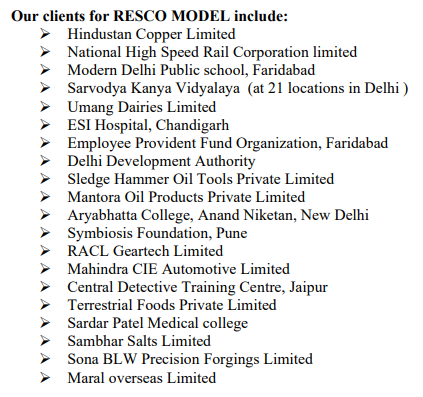

- Clients under Resco Model:

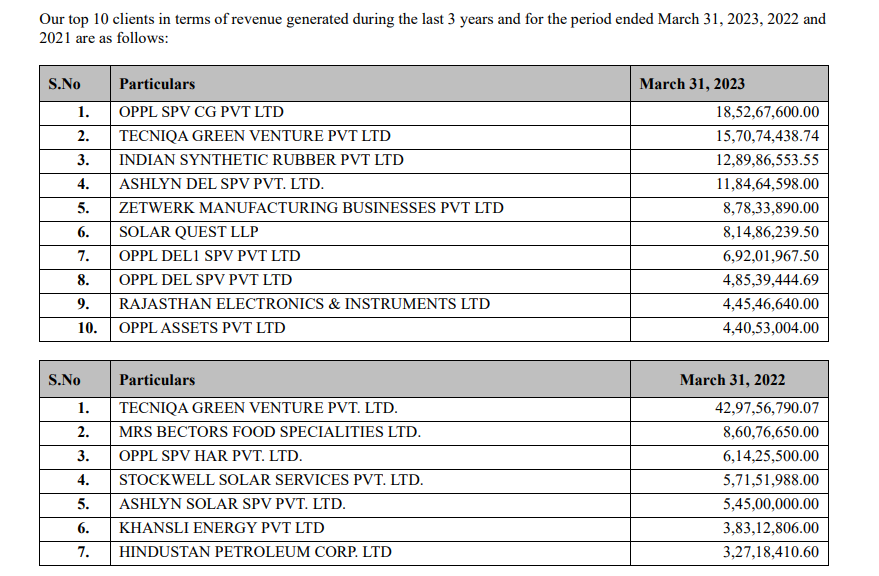

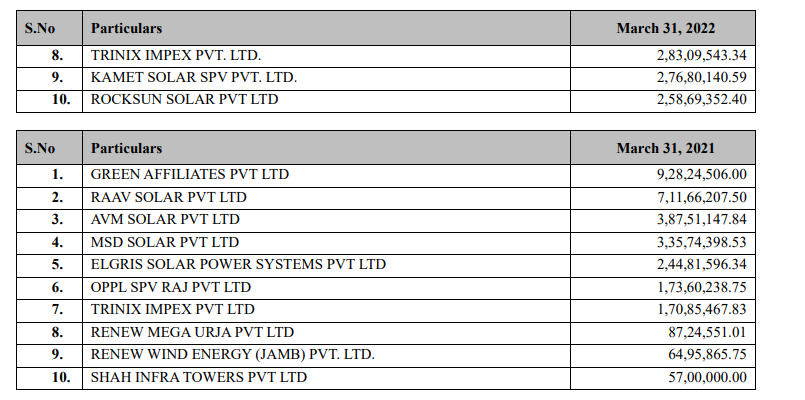

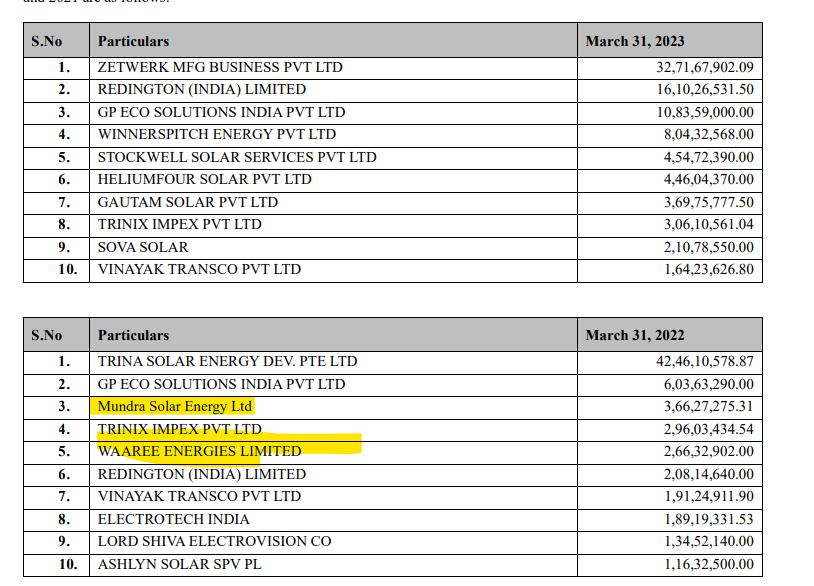

- Revenues from clients:

- Top Suppliers:

- BOS costs for solar projects:

-

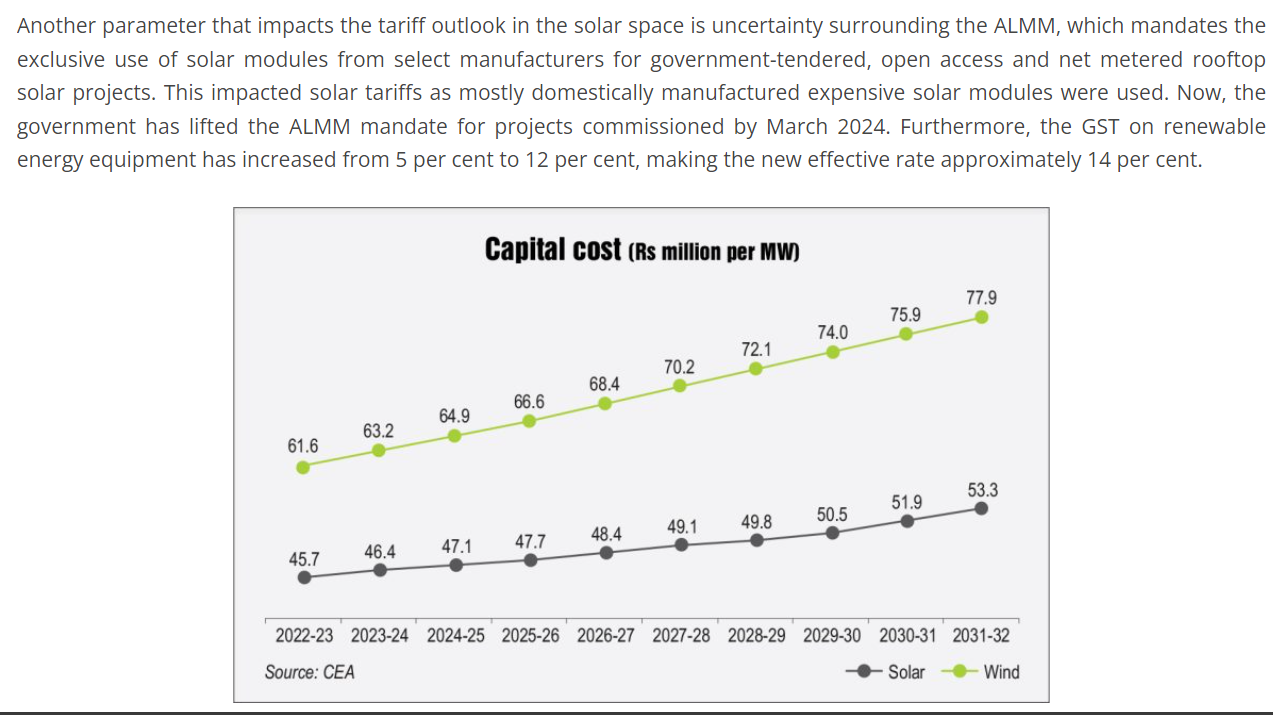

Raw materials Impact: At present, it imports 60–70% of its solar panels from China. Though solar panel prices in China has plummeted, ORIANA will not reap any benefits of this decline as any price fluctuation is passed on to the end-consumer. Imports may decline to 30–40% once ALMM regulations are implemented from April 2024.

-

Awards and recognition:

Growth:

- Opportunities: At Oriana, we are committed to continuous growth and exploration of new opportunities. In 2019, we expanded our service portfolio to include floating solar installations, demonstrating our dedication to innovation and development. We are also close to exploring new avenues like Energy storage and Green Hydrogen.

- CBG segment: They have ventured into the Compressed biogas segment with recent wins of 56 crores orders.

- Hydrogen electrolyzers & reverse electrolysis: Its planning to manufacture both hydrogen electrolyzers (electrolysis) and fuel cells (reverse electrolysis) in the hydrogen value chain.They will also provide hydrogen projects EPC services just like solar EPC.

Profitability:

- Margins : Both WAREERTL and ORIANA have guided at a sustainable EBITDA margin of ~17%. Any price fluctuation in solar panel prices is passed on to end-consumers while executing end-to-end EPC solar projects in India. Thus, shielding the profitability of EPC players.

- Guidance: As Per guidance, trying to use IPO proceeds of 60 crores to develop 100 MW over next 2 yrs. Per guidance, 470 crores potential.

- FY 25 revenue: With the latest order of 325 cr, it should stand at close to 1225+ cr.

- 1800+ crores of revenue target for next 2 years with a 18% margin but key risk is execution.

Industry Tailwind:

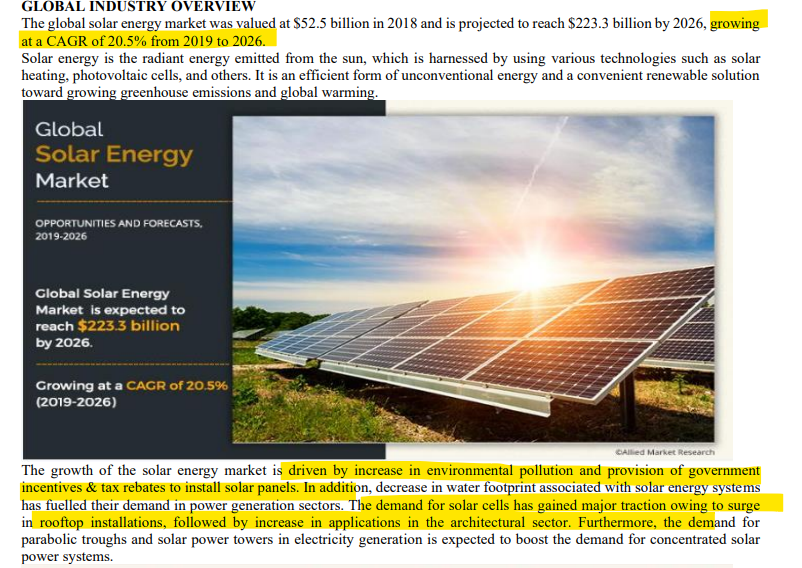

1. Global Industry:

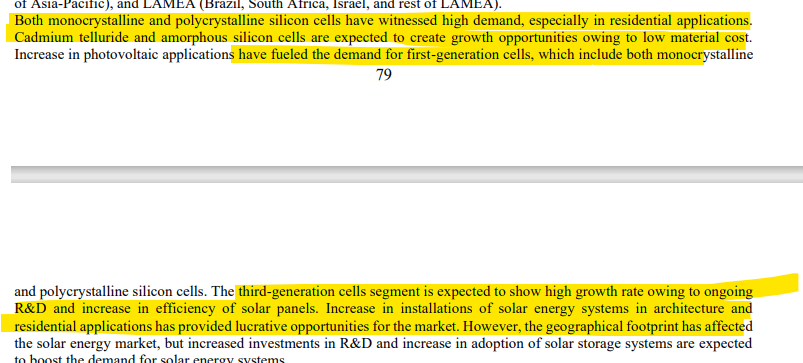

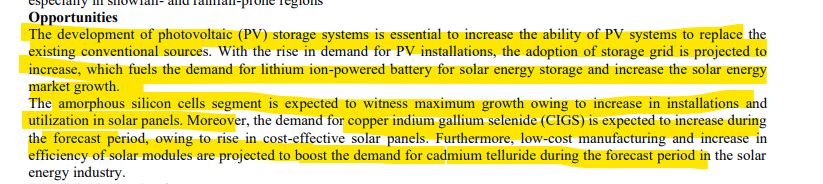

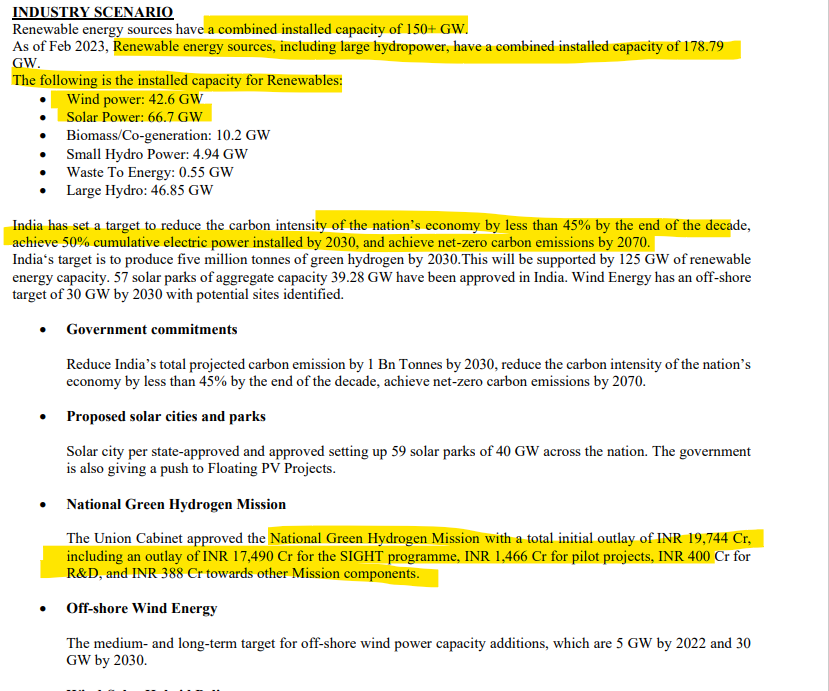

- Solar Industry in India:

- Energy demand and to be self reliant:

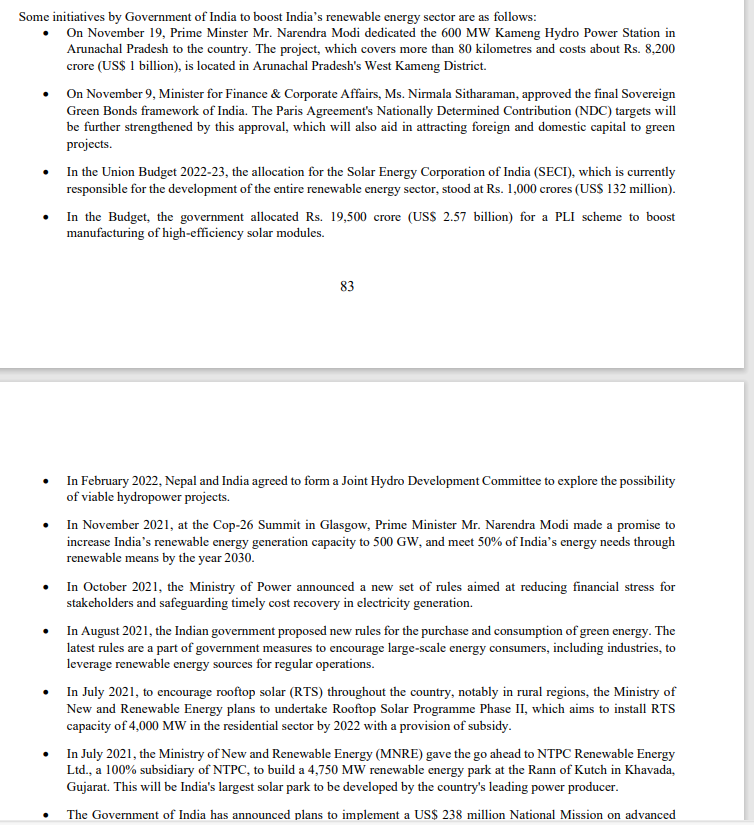

- Government initiatives:

Competitive Advantages and Intensity:

- Capabilities and experience:

- Innovation tech : BESS (Battery Energy Storage System): Adapting to the growing reliance on renewable energy sources.

Hybrid Systems: Combining solar, wind, and battery technologies for reliable and sustainable energy.

Risks:

- Our Company has given Corporate Guarantees of ₹ 7,437.00 Lakh in respect to the loan taken by its subsidiaries and associate companies. We cannot assure that there will be no default done by our subsidiaries in the future.

- We may be unable to accurately estimate costs under fixed-price EPC contracts, fail to maintain the quality and performance guarantees under our EPC contracts, we may experience delays in completing the construction of solar power projects, which may increase our construction costs and working capital requirements and thus may have a material adverse effect on our financial condition, cash flow and results of operations.

- Orders in our order book may be delayed, modified or canceled and letters of intent may be withdrawn or may not translate to confirmed orders, which may have a material adverse effect on our business, results of operations and financial condition.

- Risk due to ALMM as cost escalates:

Management:

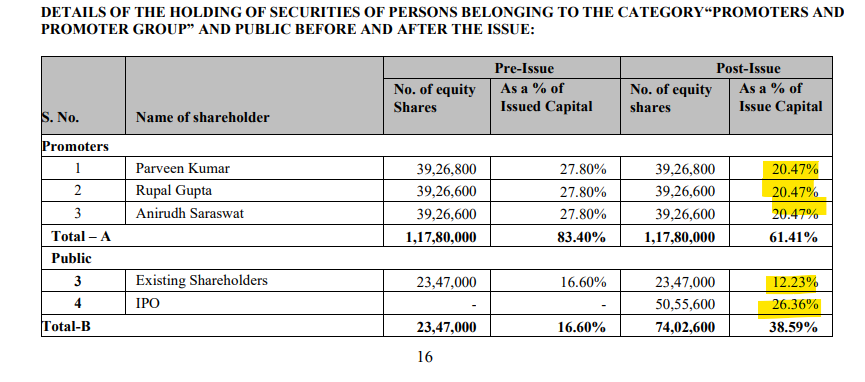

- Shareholding pattern:

Financials:

- Revenues over the previous years:

Disclaimer: Invested and biased, DYDD.