I think looking at one year’s revenue generated by the RESCO capacity is not entirely right thing to do because these are annuity projects which usually have PPA agreements spanning across 25 years. So the revenue contribution has to be looked from that POV.

1 Like

Hi Pratik,

While these assets have long useful lives, they must ideally generate enough annual revenue - and consequently operating profit - to earn a return on capital that is higher than the project’s cost of capital. Obviously, it is understandable that this may not be achievable in the first year or two after commissioning owing to stabilisation issues. But the revenue from this segment seems too long way off to say with any confidence that it will happen in future.

2 Likes

Very bullish guidance in the investor call. 1000 Cr rev in FY25, 2500 Cr rev in FY26 and an aspirational goal of PAT in FY28 = Rev in FY25.

The last bit seems aggressive to me but FY27 onwards with the BESS and GH2 businesses kicking into gear could lead to explosive growth.

Disc - Invested.

5 Likes

How Oriana Power is different than “GENSOL ENGINEERING”? Can someone throw light in this comparison? (Do Research for intresting insights)

Gensol Eng Seems Cheaper-Better-less risky

Solar Green hydrogen Emobility BESS power developments projects.

GENSOL ENG seems to have it all.

GENSOL Seems More promising

Disc- invested

My Entry price is 1849

I am invested in both - Gensol & Oriana. Gensol was the earlier investment and my thinking was similar to yours. Now, I realize that with these 2, execution is the key as they are very aggressive companies targetting/promising the moon and operate in new futuristic sectors. So potential seems huge, but how well they execute and sustain is crucial. Having said that, 2 differences are

- Oriana operates in related sectors only, while Gensol’s diversification into multiple areas including EV manufacturing/leasing and transactions with promoter held Blusmart makes Investors a bit wary

- Oriana operates/plans in Green Hydrogen sector, Gensol is only in the Green part. The Hydrogen (electrolyzer) part will be done by their sister concern Matrix gas. (again another promoter held entity)

2 Likes

Company clarified “As an EPC and IPP player without reliance on international markets or policies, we are uniquely insulated from external shocks. Oriana is well-hedged against potential impacts from international policy changes. Oriana is well-positioned to take advantage of increased solar module manufacturing capabilities of India”

6 Likes

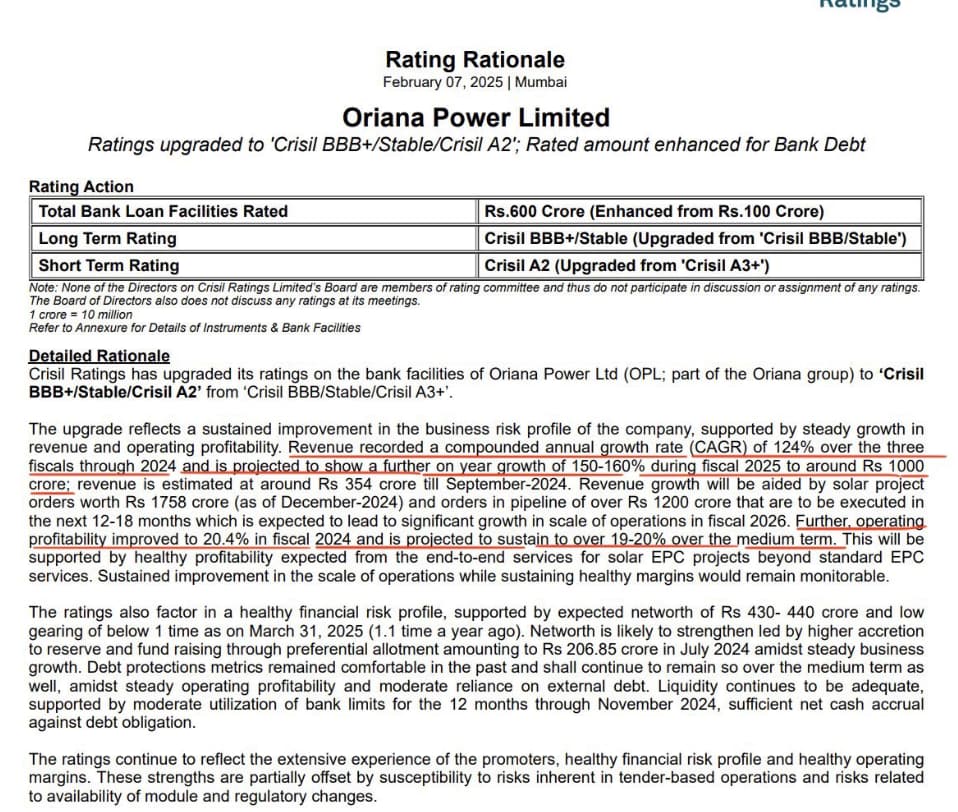

Oriana rating upgrade. As per this FY25 revenue of 1000 cr at 15% profit margin also FY25 PAT can be 150 cr. At current market cap of 3k cr i.e FYWD FY25PE of 20

2 Likes

I have just started researching this business and listened to H1 call.

Everything about the business looks good. Great Order book, seems to be well executed, etc. On the outset, looks to be generating cash but need to further research that.

However, Has anyone done research on the promoters? Appreciate your inputs.

- Concall Qs moderated by someone seems to be strange.

- Half the time Promoter presented, they seem to keep talking about thier integrity, pedigree and like how they are engineers and now they will be great in finance as well, etc. Shareholders get 3 great promoters running the business, complement each other, etc → I maybe completely wrong but felt like they were over doing it.

And yes, its a small company so probably could not get DIIs but don’t see good HNI investors as well, except for Prashant Jain and he reduce the stake recently.

3 Likes

point 5…

I know they made strategic partnership with spill waters for hydrogen theme

Sometime around they have done one EPC for CBG plant…

Only Concern is do they have complete understanding business for CBG or they are outsourcing it

1 Like

As they are still small company may be they are projecting as much positive as possible to increase confidence of the investors I don’t see that much of this as red flag as long they are delivering on numbers

Only issue I see with Oriana now is they are not posting any orders since 3 months but they keep saying next year targets are on track

Just need to see how this turns out

2 Likes

How should we interpret this? What could be the potential impact on all players esp. Oriana?

The said warning letter alleges violation of

Regulation 167(6) of the SEBI (Issue of Capital and

Disclosure Requirements) Regulations, 2018

ORIANA_10032025183815_Update_OPL_100325.pdf (2.5 MB)

1 Like