About the Company :

Orchid Pharma Ltd., based in Chennai, is a prominent pharmaceutical firm in India. The company specializes in the research, production, and promotion of various bulk actives, formulations, and nutraceuticals. Its global reach extends to over 40 countries through export activities. Orchid Chemicals & Pharmaceuticals Ltd. is a vertically integrated company with a strong presence across the entire pharmaceutical value chain, demonstrating expertise in research, manufacturing, and marketing.

Growth Drivers :

- Integration with Dhanuka Labs through a strategic merger.

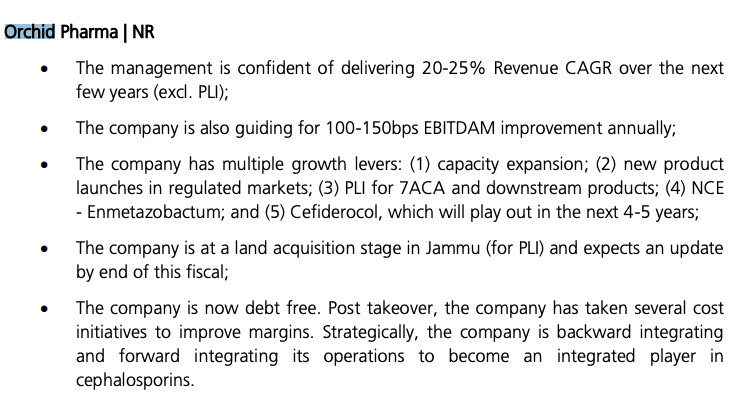

- Anticipating a robust financial performance with a projected 24% CAGR in sales, a 38% CAGR in EBITDA, and 49% CAGR in Profit After Tax (PAT) from 2023 to 2026.

- Launching a New Chemical Entity (NCE) on a global scale.

- Exciting plans for re-entering the US market, signaling a strategic move to expand and strengthen market presence.

Stock P/E Ratio : 58.4

Sales :

FY 23 666 cr

FY 22 560 cr

Net Profit :

FY 23 46.3 cr

FY 22 -1.9 cr

Major Mutual fund holdings :

Quant Small Cap Fund

Nippon India Pharma Fund

Quant Multi Asset Fund

Major FII/FPI holding :

MASSACHUSETTS INSTITUTE OF TECHNOLOGY (4.64%)

Manufacturing blocks -

Sterile APIs - 6 Blocks ( 05 crystalline and 01 Lyophilised blocks )

Oral APIs - 07 blocks

Intermediates - 05 blocks

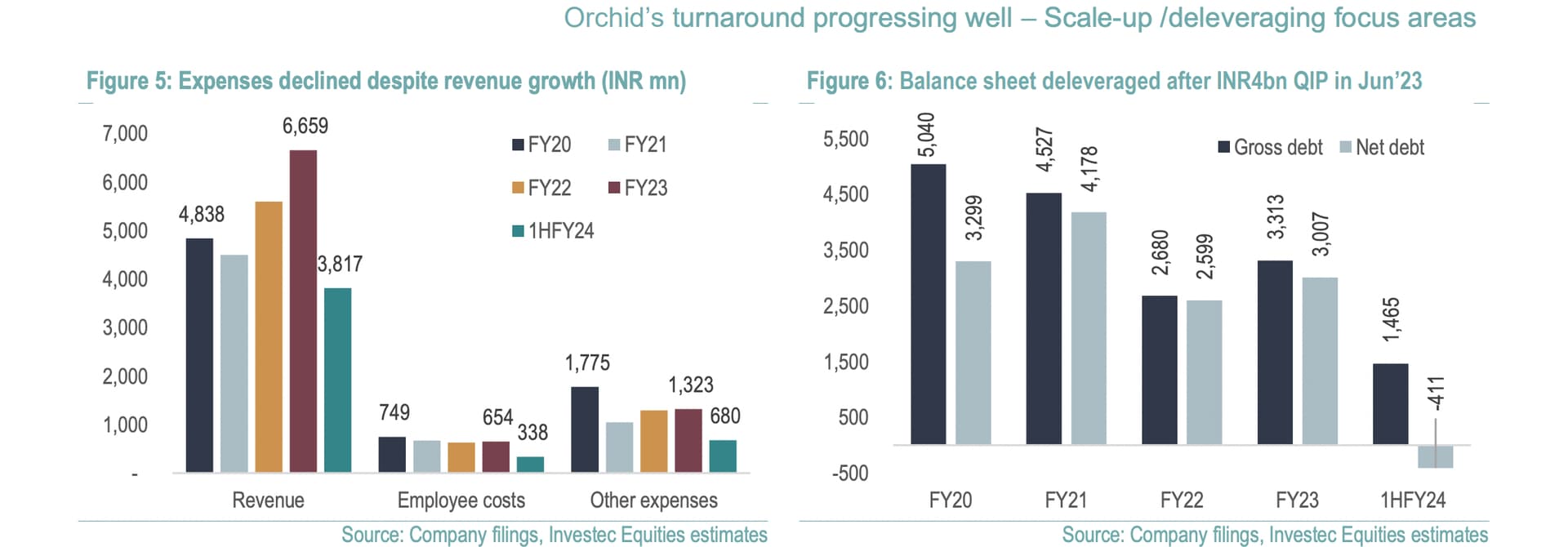

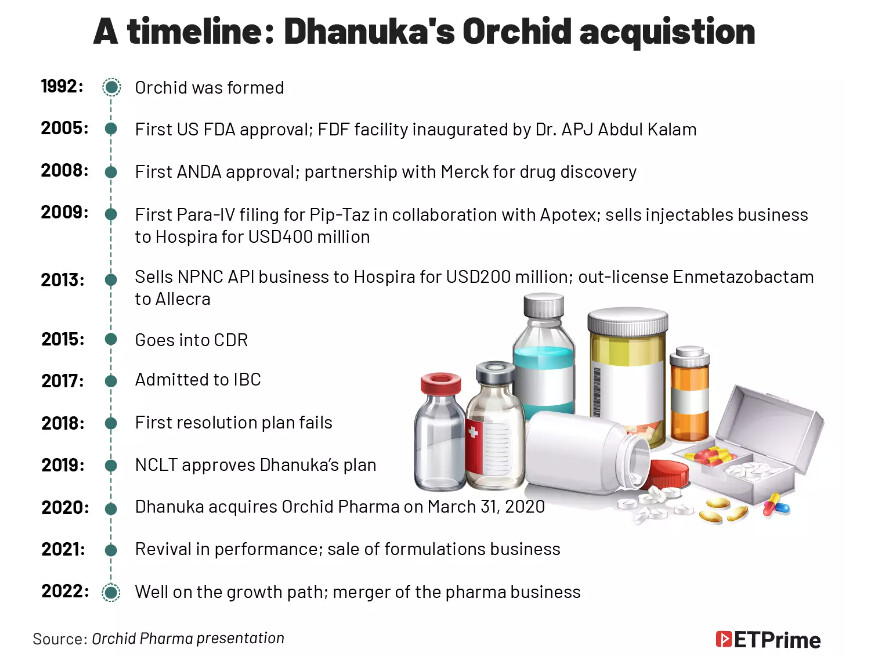

Orchid Pharma (Orchid) is a prominent supplier of cephalosporin APIs, and its recent revitalization under new ownership by Dhanuka has been remarkable, achieving a significant reduction in debt and a threefold increase in Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) within just three years.

Contention is that Orchid is now primed for a growth trajectory driven by:

i) enhanced utilization of its expanded capacities, currently at 75%;

ii) the potential advantages stemming from the Production Linked Incentive (PLI) program for a crucial starting material (7ACA), expected to amplify sales and promote backward integration.; and

iii) the timely implementation of innovative projects, including two with limited competition

Key Risks:

-

Execution Risks: The successful and timely implementation of these initiatives poses a significant risk.

-

Litigation Risks: The introduction of Sterile Abbreviated New Drug Applications (ANDA’s) in the US market hinges on a positive outcome in ongoing legal proceedings.

-

Pricing Risks: Unfavorable shifts in API prices due to changes in competitive dynamics or alterations in supply and demand could present challenges.

-

Regulatory Risks:

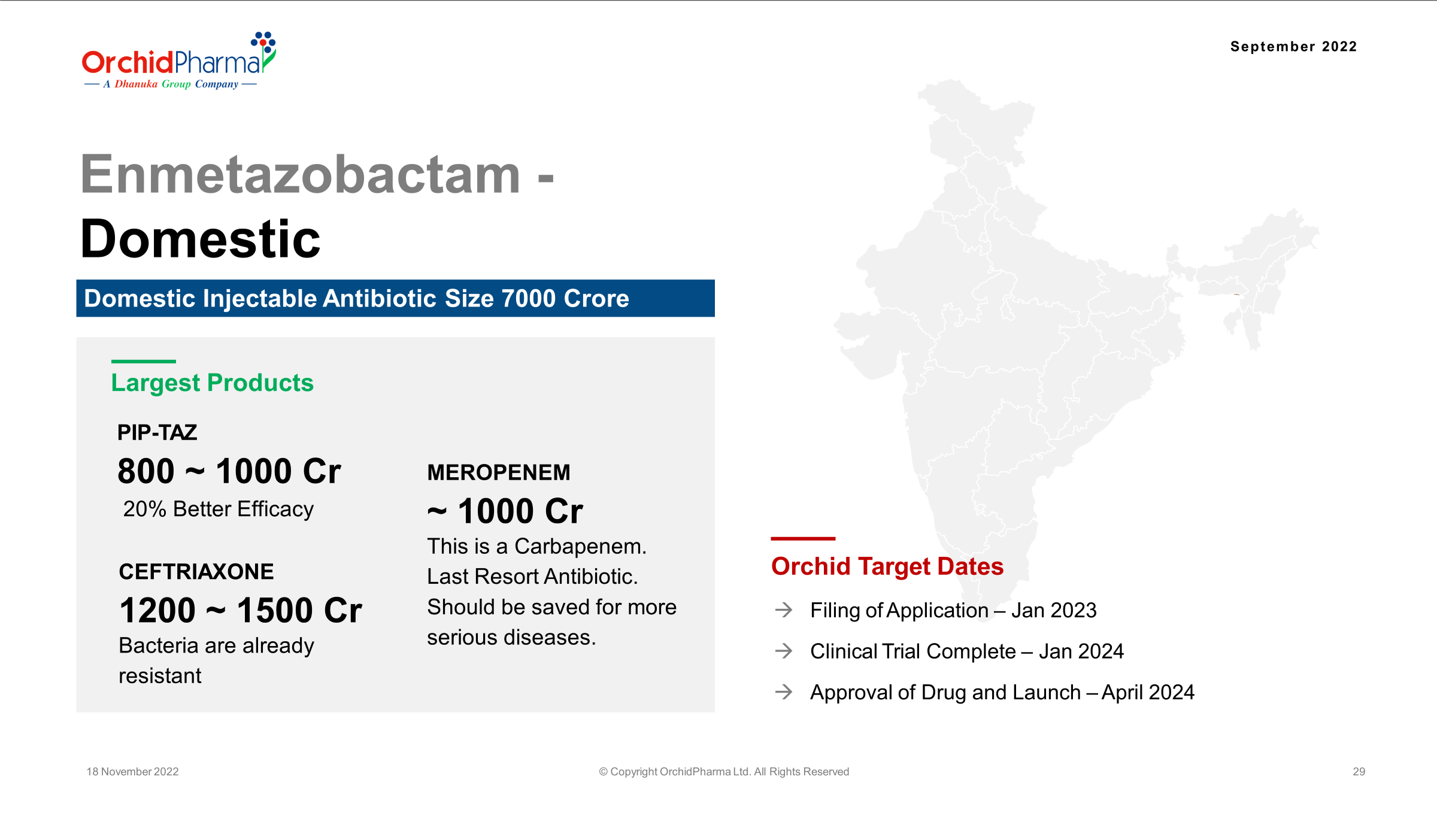

a. ORCP Novel NCE (Enmetazobactam): As Enmetazobactam awaits approval from global regulatory bodies, an adverse regulatory decision could impact our projected outcomes.

b. GMP Compliance: ORCP’s substantial exposure to regulated markets necessitates the maintenance of its manufacturing facility in compliance with current Good Manufacturing Practice (cGMP) for the continuity of supplies and successful new launches.

Here is a brief analysis on a company I am interested in. Would love to hear about your views on the same.

Disclosure: Invested nominal amount for tracking purposes.