Earlier I used to focus more on Fund Manager but now I prefer fund houses with sound processes and which do not depend on star fund manager

1 Like

Similarly for mutual fund policy, origination can be from broking portal or bank branch

Anoop bhaskar is leaving IDFC fund management team, Manish Gunwani is the new head of equity. My investment thesis for IDFC Tax Advantage is ‘‘under review’’

Staying put with Axis LTE. IRR has fallen to 11% from start of investment. My judgment is IRR will bounce back to mid to high teens. I am not sure whether that will be 2023, 24 or 25. ICICI pru value discovery which is topping charts now were in bottom quartile for 4 long years from 2016-2020. Overall my patience levels are very high when it comes to under performance

On the portfolio level, continuing with the same portfolio. Looking to build positions in HDFC bank and HCL tech

Patiently trying to find opportunity where I can hold through multiple cycles and grow with the company. Following are my criteria as explained in the thread above

- Company with proven track record. I am not good at finding transformation from broken franchise to strong franchise rather I will invest when franchise is intact while growth is broken

- Management with proven history of excellent capital allocation

2 Likes

The superior risk profile of Ajanta pharma because of diversified geography presence in branded generics comes at the cost. The margin hit this quarter and last quarter was because of following reasons

- Derivative hedging loss

- Pricing pressure in US and Euro fluctuation

- Freight cost

All these 3 factors are related to non-India business. As per my thesis, this diversified geography model (especially in branded generics) will help Ajanta to mitigate geography specific regulatory risk better and create superior wealth over long term compared to only India focussed branded generic business like Abbott. Therefore I am ready to accept the cost which comes along with it. Abbott’s P&l will always have less moving parts which makes it very attractive but risks comes from nowhere and that is why I am ready to accept margin volatility for some period as long as brand franchise is intact. Therefore I still believe Ajanta pharma deserves better allocation in my portfolio as compared to Abbott

Current Allocation

Ajanta Pharma ~10%

Abbott India ~3 – 4%

Eris Life science – As per my judgment - business model focussing on acquiring brands for growth is less attractive to me as compared to launching brands organically. I am not convinced with capital allocation abilities of Eris’s management

2 Likes

Though Abbott continues to inch its Margin profile upwards every quarter/year, my revised core thesis is solely based on longitivity and not margin expansion mentioned by me in the first comment. Management has promised bottom line growth higher than top line growth in analyst meet and so far they are delivering on it. Having said that, in my long term hold style of investing - margin expansion is of lower priority than maintaining the core franchise

2 Likes

Minda corp is paying ~ 400 Cr for Pricol with Revenue (FY 22) 1500 Cr and EBIDTA Margin ~ 11%, thats around 2600 cr for 100% if they go ahead with hostile takeover

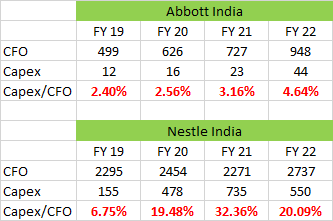

The reason for including Abbott india in the portfolio is the longivity of the business matches with period for which I am willing to hold investment. At the same time, the reason for low allocation is because inferior risk profile as discussed before and low reinvestment rates. Following table gives comparison of reinvestment rate between Abbott Vs Nestle. Low reinvstment can result in below par results over long term. Having said that, Abbott India has done acquestion in the past ( domestic business of piramal ). My approach is here is to keep low allocation and hold long term for any positive risk to play out

2 Likes

Correction - It was Abbott usa and not Abbott india bought Piramal’s business

1 Like

One of the reason, I can never buy Alembic pharma is purely on the qualitative point mentioned above - they try to do too many things in my judgement which draws requirement of higher capex. My style of investing does not favour companies having high capex requirements as it increases the chances of capcital allocation decisions going wrong over a long term. One poor capital allocation decision makes me lose conviction and jump out off business at wrong time

2 days back I complained Reinvestment rate of Abbot India being low ![]()

Having said that I am studyiing Narayana Hrudayala wihch is high capex business ( albiet lesser compared to peers ). I will post my views in some days

1 Like

Request reader to please read above arguement in the context of my invsetment approach which is Concentrated allocation to few ideas where I think I can hold for long term

many roads lead to Rome

1 Like

Precisely the comparison I did couple years back and replaced my Abbott holdings with Nestle. Btw both are good companies. Curious why you are not choosing Nestle at all if willing to pay top valuations for Abbott (Nestle one of highest valued FMCG and Abbott one of highest valued Pharma albeit domestic Pharma).

I feel more than any acquisition, positive surprise lies in any blockbuster drug introduction or marketing leadership in any existing drug in portfolio replacing another leader. This is indeed a positive surprise.

But IMO feel very very hard to know, track, predict or understand the possibility of such surprises…

Would be good to know your thoughts on above and also on Why not a Nestle…

Thanks

Hi

I must admit Abbott India is the weakest link in my portfolio. No other investment idea in the portfolio, I want to restrict allocation below 3-4% - that itself explains the dilemma. Therefore my argument/reasons are not solid. Please take note of that

Following are the reasons

- Generally I think branded generics have do better in high inflationary environments compared to FMCG companies

- In my view, there is no further scope for Nestle in improving working capital further. CFO increased from 2052 cr to 2737 cr only from 2018 to 2022. Abbott has room to crush WC further in my view. CFO for abbott improved from 150-200 Cr to 948 cr from 2018 to 2022. Next 5 years, I dont think this will improve at same rate but in my view has some room for improvement

- Earnings profile will be similar I feel, having said that Nestle’s volume growth in recent quarter has been very strong

- In both cased I believe, starting valuations are rich and therefore in best case returns will mirror earnings growth.

I am sitting on the fence and looking for options. Following are current options

- Bump up Ajanta’s allocation to 15% by selling Abbott – priority 1

- Replace Abbott India with something else – Priority 2. Current candidate – Narayana Hrudayalaya

- Maintain 3-4% allocation in abbott – Priority 3

1 Like

Ajanta pharma keeps repeating sensible capital allocation

- Invest in branded generic business more and more. Focussing on what they have rather than announcing fancy new projects

- Careful about US generic investments. No more capex in US generic focussed manufacturing. Careful consideration to US generic R&D. Calibrating US generic pipeline

- Return whatever left to shareholder via buyback or dividend

- No flashy future targets

- Maintaining ROEs even in difficult quarter

All these points give me conviction to hold even at very high allocation despite having 0 knowledge about brands/ future launches/ market size etc.

My belief is if they keep repeating above steps for next 10 years, it will create descent wealth to shareholders.

2 Likes

I believe it’s not the current / historic capital allocation that matters but future incremental invested capital matters. I would like to stick with managements which are sensible and that’s why future incremental invested capital will be deployed ‘’sensibly’’

Since being sensible is a behavioural trait. ‘Past’ track record gives enough opportunity to judge if management will deploy cash sensibly in future as well. It further increases the predictability if cash is being deployed in existing strategy which is successful so far. In this case odds are in your favour to judge the success of future capital deployments

1 Like

What makes investing exciting is that there are multiple ways of making money and there are multiple lenses looking at the same industry. Investor’ investment thesis will depend on through what ‘lens’ investor is critically observing the industry and the best part is - multiple investment theses can be correct as investing is not a zero sum game. Unfortunately this point is lost in many discussions

One of the lens to critically analyse auto ancillary business is Gross Margin profile which many of my colleagues on VP use and I absolutely think it is correct

Although my lens does not consider Gross Margin as the most important factor. The reason for that is the key KPI in auto ancillary business is QCDD - Quality, cost, development and the delivery. In my view gross margin does not capture the ‘delivery’ part of QCDD but EBIDTA margins capture that and therefore rather than starting thesis from Gross Margin, I would take QCDD as the starting point

Suprajit engineering with its presence of plants across - americas, europe, india and china scores very high marks as a partner in a global supply chain in the cable business. And according to my judgement Global presence makes integration in global supply chain lot better than just export heavy global business

This global expansion Suprajit achieved by being the King of low gross margin business like mechanical cables and buying their competitors cheaply across the world. In my judgment this will not be possible for the high gross margin business because that business will always sell for top dollar

Views welcome!

More thoughts on above point - high gross margin is the key KPI only if company wants to grow within india for medium to long term as ‘delivery’ kpi in qcdd is not as important as global business in india centric model

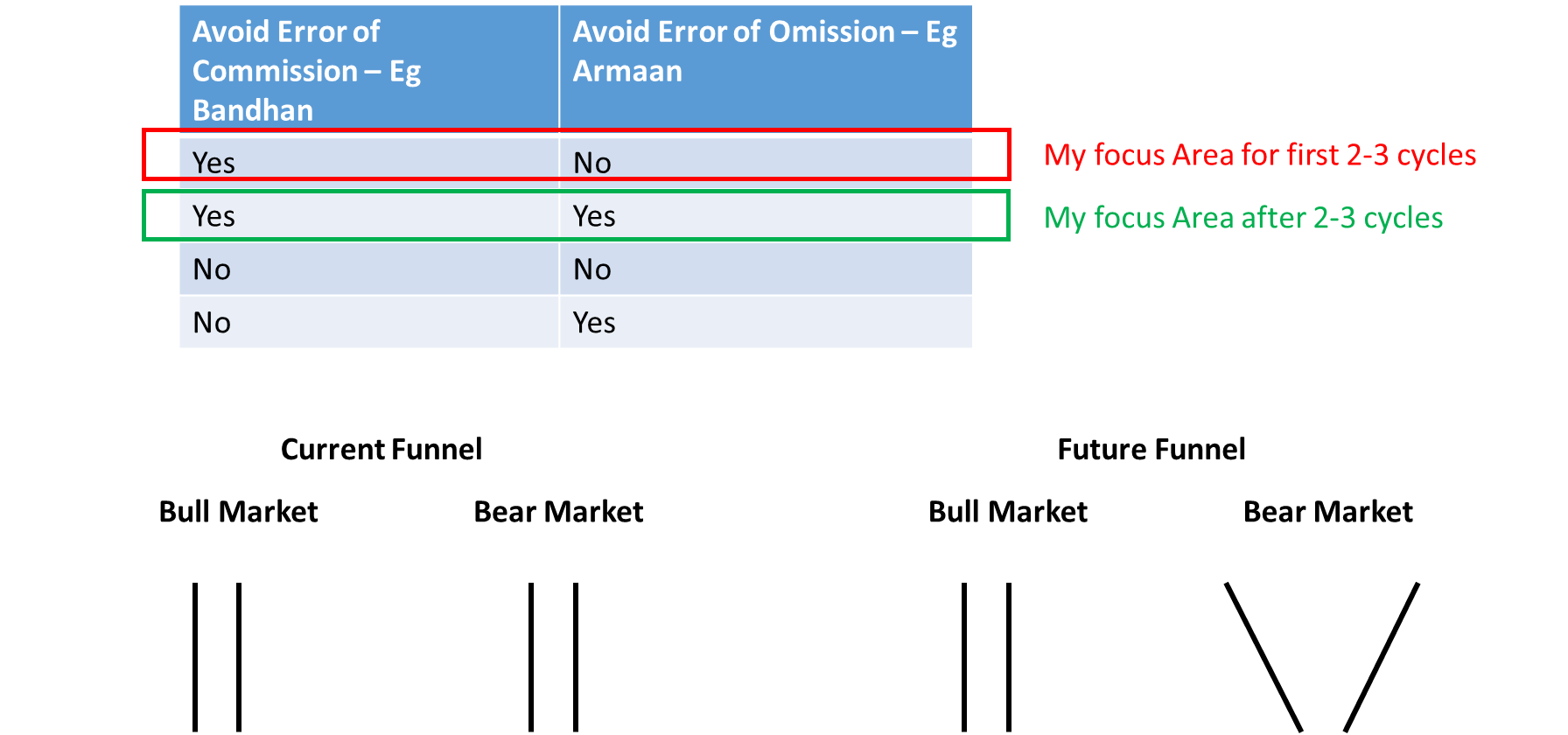

I avoided bhandan but I missed other winners in MFI ![]() Thats I beleive very ordinary outcome and not worth of ‘‘Maine Bola Tha!’’

Thats I beleive very ordinary outcome and not worth of ‘‘Maine Bola Tha!’’

One of the key drawback of my current framework is the ‘narrow’ width at the top. I let go far too many ideas ( mostly also because I am not a good stock picker) But at present, I don’t lose sleep over errors of omissions. Given that I have concentrated style, My belief is if I avoid mishaps, few good decisions over long term will generate alpha

But I am willing to change to broaden my funnel by removing ’10 year track record criteria’. Following are my thoughts

This only looks good in diagrams, execution is the key

5 Likes

On contrary, I think this is a sign of maturity, level thinking and brightens chances of long term success.

Ability to cut the crap and focus on limited names and avoid FOMO, persistent need of momentum (when that’s not your forte) and unnecessary diversification is what differentiates the Men from the Boys…

If I think back -

- In my portfolio of around 30-40 stocks, I would have been much better off had I invested in only my top 10 and cut the rest crap.

- That rest crap has few 5-10 baggers but not worth it considering low allocation & other misses which drags down everything, blocks existing and fights for incremental capital.

- Over last 3-5 years, if I had invested only in my top 3 picks, I would have hit the home run.

So, the need for me is exactly opposite to what you feel is yours. I think I would be better off making my funnel closer to what it is yours today i.e. Narrow! Cheers!

4 Likes

Reader will notice how my opinion about Abbott india keeps changing. This hasn’t happen for any other portfolio company in last 2 years since the beginning of this thread. Partly because I have lesser conviction and at the same time price is still holding up in spite of my negative views.

Following is the trail before telling you the latest change in opinion

First mention -

Taken position first time during Jun 21

On the fence, not sure about increasing allocation. Jan - 22

Turned positive because of quarterly updates and price action - feb 22

Justifying valuation. Positive mood may 22

Turned neutral/less bullish July 22

**Suddenly turned positive after analyst meeting oct 22 **

Turned slightly bearish feb 23

Turned more bearish in feb 23

1 Like

Most recently I have again turned slightly bullish. I will post my latest narrative soon on Abbott. I am also excited with upcoming Mankind pharma ipo. I have written off Eris because I am not convinced with management’s capital allocation abilities. I might sell tracking position soon. That’s a first ‘Sell’ or trim since the start of this thread

3 Likes