Hi mudit - yes, even I believe its a noise. This kind of risk can only be taken care via portfolio diversification. Example was just to compare business model of ajanta pharma vs abbott. If the mentioned risk actually happens Ajanta can handle it better than abbott. Or for that matter any regulatory risk specific to India, generics was just example

1 Like

This was one of the most short term thinking and useless post by me on this thread. Back to the underperformance ![]()

As I gain confidence with business updates, i will look to add in following existing portfolio companies

-

Abbott India - more “information” available on business model with recent video. Yet to connect dots for updated investment thesis if any. Usually my tendency is assuming all the new ‘information’ as investment thesis. To avoid bias, taking more time

-

HCL tech - continue to believe as a business owner i will prefer services + er&d rather than only er & d

-

Hdfc bank - as mentioned earlier, playing uptick in credit cycle by being conservative in selection but being very aggressive in allocation (~ 30% for financials - kotak, bajaj fin and hdfc bank)

At the same time, looking for new ideas in small midcap space having dominant niche with large secular runway for growth

Studying 2 companies -

- Century ply

- Schaeffler India

4 Likes

The key insight from the investor meet and AGM video - which potentially can become my Investment Thesis – is,

Abbott India participates in therapies where they can support across the therapy lifecycle. This helps Abbott India to take lead in therapy shaping, the by-product of which is brand share gain. Therefore ‘Therapy Shaping’ is core to the business model and not the brand share gain

Following slide from AGM, gives gimps on how Abbott India participates across therapy life cycle

Source: Abbott AGM

Thus, the ‘Organic Therapy Shaping’ abilities can become key to for my investment thesis for Abbott India. Their current top 10 brands ( ~ 70% of the revenue) provide good insights whether – They have really taken lead in shaping therapy, or they are introducing brands in already developed therapy. The interesting part of thesis will be – are they in position to shape therapy for next 10 brands

Finally, I believe it will be good to compare what large India generic players are doing and this ‘Therapy Shaping’ is just a management narrative which weakens the foundation of my potential investment thesis

1 Like

These MNC pharma companies launching new products using unlisted entities maybe discussed and beaten to death. That’s a risk nevertheless.

" Companies with MNC parentage trade at a substantial premium to their domestic counterparts. Most of these companies have been listed for many decades and have created huge wealth for the shareholders. But many MNCs operate in India through multiple entities which deprive the listed entity of full range of products and growth opportunities. The risk of that is now becoming increasingly apparent with increasing instances of new products being launched in the unlisted entities - bringing the underlying risks to the fore.

Author: N Balaji Vaidyanath - Crest Wealth Management

(Views are personal and not that of the company)"

Hi Sudhakar

Thanks for pointing out. I am aware of this risk and my risk management technique in this case is right allocation and staggered buying. Abbott india’s risk profile is inferior to Ajanta Pharma in my view and that’s why it will never get same allocation as Ajanta pharma in the portfolio

I am buy and never sell kind of investor (one step ahead of buy and hold ![]() ). I like to invest in businesses which have more longevity in earnings as compared to magnitude of earnings, the business which has less moving parts which improves the decision making. Abbott India fits the bill for me which obviously comes with the risk you highlighted. If this risk plays out, I am asking my portfolio to manage that risk. The second risk mitigation technique is the staggered allocation. I typically build my position over a period of 3 – 4 years. I believe, having these two risk mitigations in place, I can hope to enjoy the benefits of its strength

). I like to invest in businesses which have more longevity in earnings as compared to magnitude of earnings, the business which has less moving parts which improves the decision making. Abbott India fits the bill for me which obviously comes with the risk you highlighted. If this risk plays out, I am asking my portfolio to manage that risk. The second risk mitigation technique is the staggered allocation. I typically build my position over a period of 3 – 4 years. I believe, having these two risk mitigations in place, I can hope to enjoy the benefits of its strength

10 year median PE for Abbott India is 38.2, the current PE is 48.

Last 5 year FCF cagr 50% , stock price cagr - 33%

3 Likes

The third risk management option, I am trying to evaluate is - Can Eris life science + Abbott India be a good partnership. Not yet getting confidence with Eris but actively tracking.

Hi Omkar…if possible kindly share your latest portfolio with weights of stocks…also your mutual.fund portfolio. Thanks

more or less, similar to this. Except I have added around 1.5% more in HDFC Bank

2 Likes

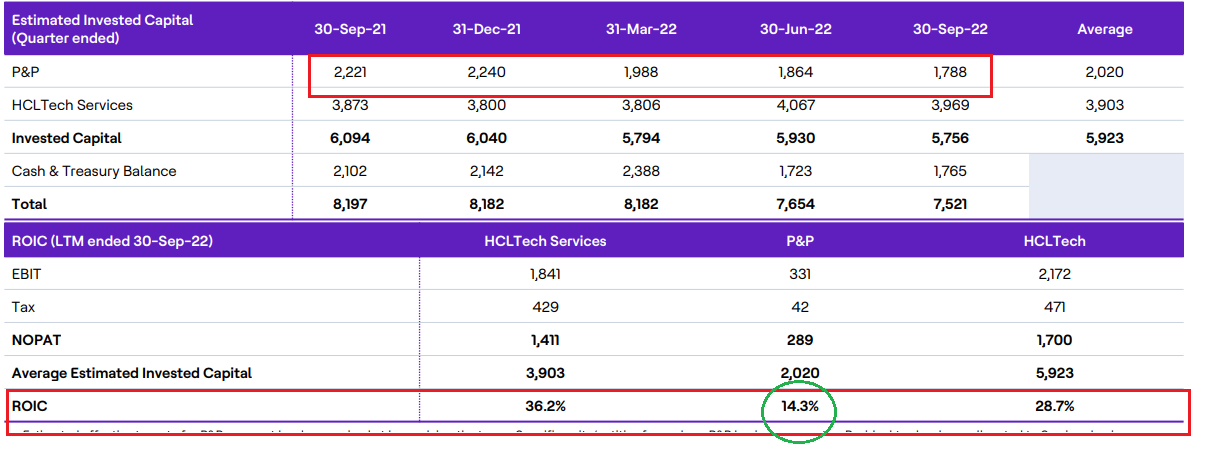

From HCL Q2 ppt, values in million dollars

The reduction in P&P Invested Capital over a period is mainly because of Amortization + some help from rupee depreciation. HCL tech bought product business from IBM in Q3 FY 19 for 1.8 billion USD. It will be interesting to guestimate what will ROIC after 5 years. This can become key part of my investment thesis

As per management in Q2, first time they won large P&P deal because of synergy as they were vendors for IT services with same client. I feel similar sort of synergy is possible between traditional IT services and ER&D business. That is why I prefer Traditional Services + Er&D player rather than niche ER&D player

1 Like

After 1.5 years if posting above thesis, first time there is meaningful progress on the ‘Technology’ side. Though this is the result of work done in last 4/5 years, It will take some time and successful execution to reach to meaningful scale. At this stage I am only changing outlook of my antithesis from No Progress to Progress, but it still remains as a key risk

Suprajit Eng inaugrated its first Electronic Facility Today. Following comments are from Tech Head

Ashutosh, Head of Suprajit Technology Centre said, “Our focus has always been to take products from concept to commercialization. Customers now perceive Suprajit as both capable to execute and willing to invest in complex and future ready products. We are now an extremely lean and frugal manufacturing outfit that is complimented with a highly effective new product design capability”

2 Likes

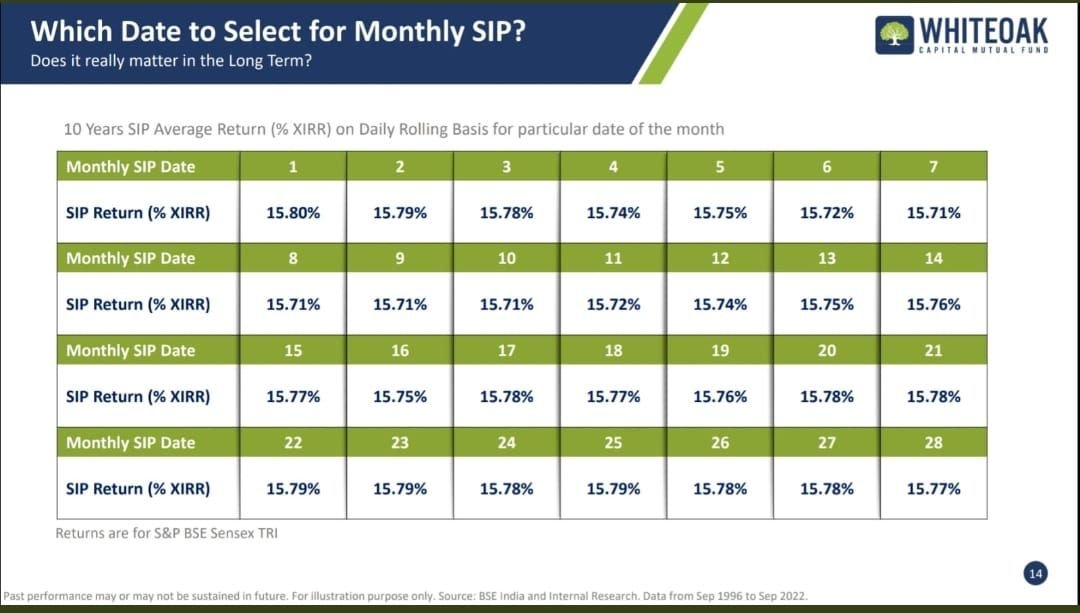

Last 3 years of SIP IRR of two mutual funds in my portfolio

IDFC Tax advantage - (small, mid cap 50%, value tilt) - 30.03%

Axis long term equity - (Large cap, growth quality) - 12.7%

Allocation of Axis : IDFC :: 3 : 2

IRR AT a MF portfolio level ~ 20%

3 years back in 2019, it was an exactly opposite situation. Even with knowledge of cycle, it was very hard to believe and have conviction especially when 5-year IRR is in single digit.

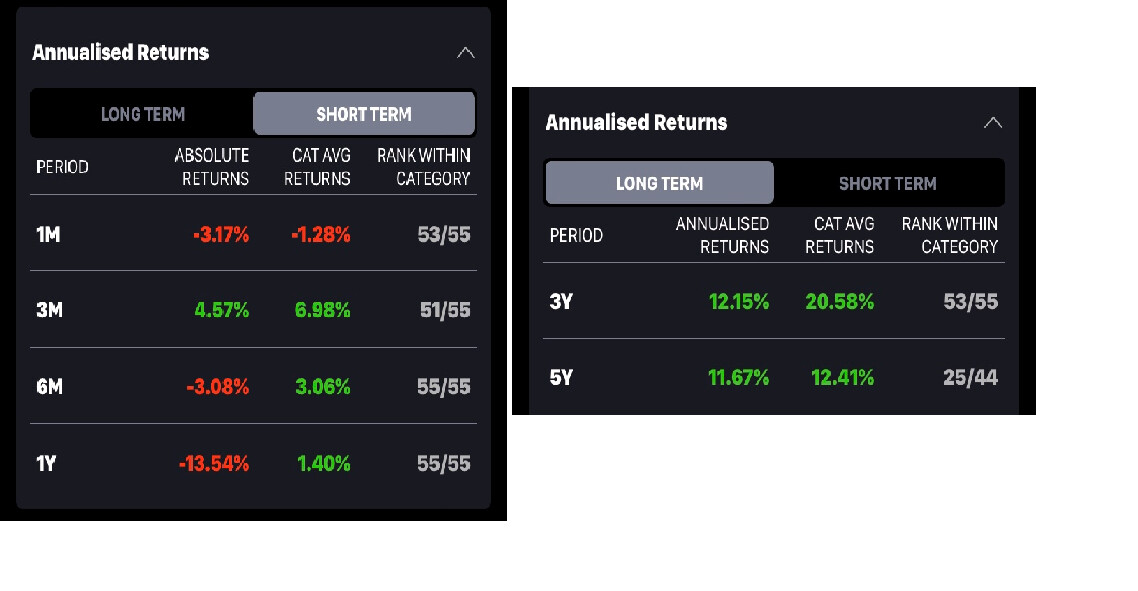

Following is the Axis Long Term equity’s current performance snapshot . Looking at it, it is hard to believe for me today (even with successful execution of buy and hold with IDFC) that next 3 years will be any different

2 Likes

I do remember many colleagues vouching for Axis MF 3 year back or so…they were mostly the ones who look for recent 3-5 years history and in trend MF…

Correct me if I am wrong, the point you want to make is that all MF houses go through cycles of out and underperformance and in long term in its real sense, it would not make much difference be it Axis or SBI or HDFC?

2 Likes

Could be due to Axis front running scam. Even before the MF bought, the managers bought and also tipped off others there by increasing the entry price for Axis MF.

In the recent PPFAS unitholder meet, Rajiv Thakkar gave following reason for not owning Asset Management companies and Insurance companies directly but through holding companies via investments in Axis Bank, ICICI Bank, MOFSL and Bajaj Holdings

‘‘In value chain there are two large players which capture the value. In the asset management business - asset management companies and the distributors. In the insurance business - insurance companies and agents. When investor owns a parent company, she gets to participate on both the sides’’

I wanted to think on the same lines when I wrote down reasoning above but what Rajiv Thakkar said is simple, sharp and shows his thought clarity. My reasoning shows brain fog

2 Likes

Curious how one can participate in agents value/profits via the parent Axis etc. same goes for distributors in an AMC. Parent value depends on only the value of either it’s subsidiaries or sum of parts (not literally but the synergy)…and here agents and/or distributors do not come under sum of parts…

On the contrary, with Parent, we get to participate in the risk of the other part of business as well…just a perspective…

There is positive as well as negative side of diversification…if we know what and why we are doing, like your case, both diversification or concentration should be fine…

Hi

Axis, Motilal and Marcellus are all underperforming at the same time. Do you think this points to something larger than just Axis AMC specific issues?

I have personally invested in AXIS Mutual Funds. I was a bit worried about the underperformance of these funds, so I decided to go deeper and check the performance of the individual stocks owned by the AMC. So I noticed only few schemes underperformed like the Focused 25 Fund while small cap and midcap funds were giving better than index returns. Stocks in Focused 25 like pidilite, Bajaj Twins and Diagnostic stocks which contribute to majority of the holdings are considerably down. The reasons are macro economic situations or overvaluation in the last 2 years are being rationalized by the market.

We need to understand that all Fund Managers have their own Investing Model, which tend to perform differently in different market conditions. So personally I trust the Fund Manager and not the return in the short term.

2 Likes

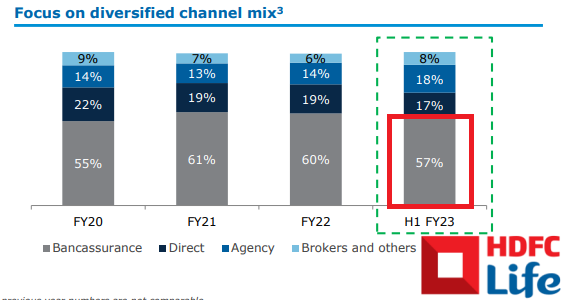

Hi

I think he is referring to bancassurance channel which might be selling policies for other insurance companies as well (outside parent) as per tie up