Today I Entered in Omfurn.

CMP: 73 Rs

Mcap: 60 Cr

P/E: 13.5

OMFURN BUSINESS OVERVIEW:

Omfurn India Limited (OIL) was originally incorporated in the year 1997 as a private limited company; subsequently in June 2017, the constitution was changed to Public Limited and in the same year it was also listed on the NSE Emerge Platform. OIL is engaged in manufacturing of furniture and prefinished wooden doors. The company primarily undertakes turnkey projects for corporate offices, hotels, International schools, prefinished wooden doorframes and shutters & Fire -Resistant doors for real estate developers. The product profile includes executive office furniture, international school furniture, modular office furniture, modular kitchen, bedroom furniture, wooden door & frame etc. Further, the company is ISO 9001:2015, ISO 4001:2015, OHSAS 18001:2007 certified. OIL operates through its manufacturing plant located at Umbergaon, Gujarat and its registered office at Mumbai, Maharashtra.

PRODUCT PROFILE:

a) Executive office furniture

b) International school furniture

c) Modular office furniture

d) Modular kitchen

e) Bedroom furniture

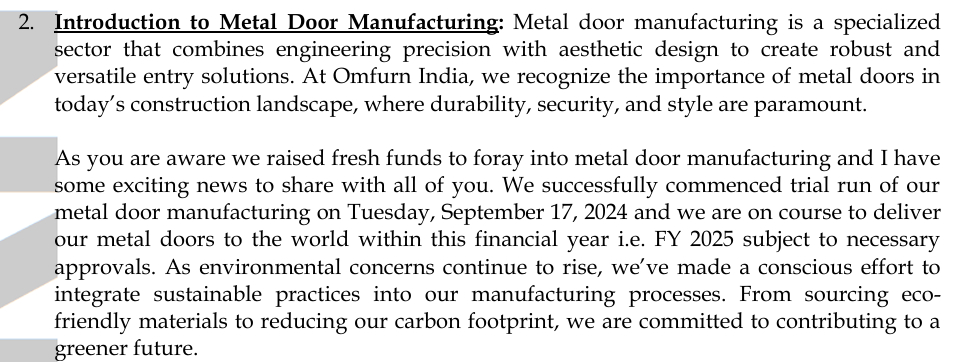

f) Wooden door & frame

INDIAN FURNITURE INDUSTRY:

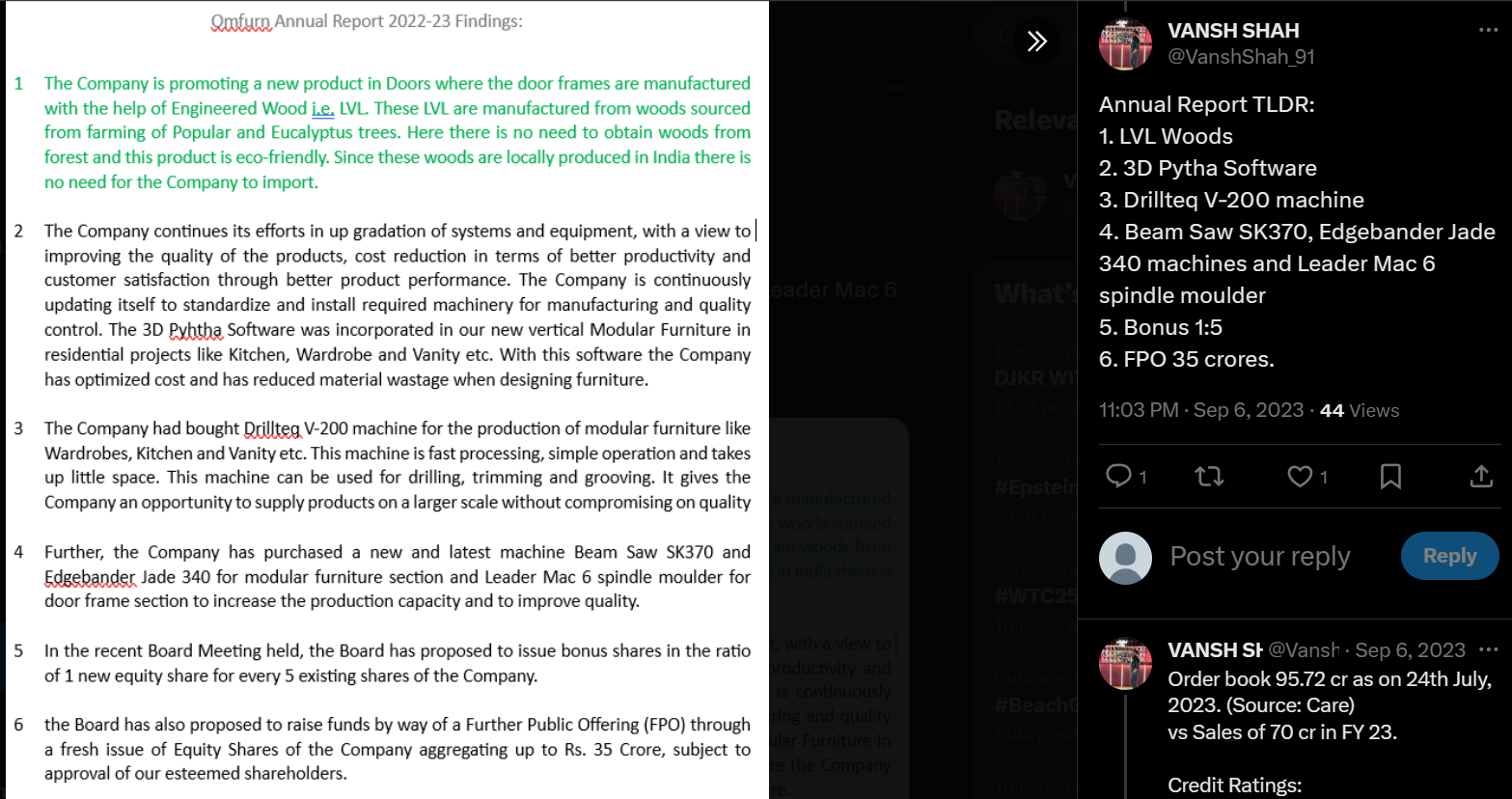

The India Furniture market size reached US$ 21.4 Billion in 2022. Looking forward, IMARC Group expects the market to reach US$ 41.4 Billion by 2028, exhibiting a growth rate (CAGR) of 11.6% during 2023-2028.

Financial Performances:

Things attracted me to invest in this business:

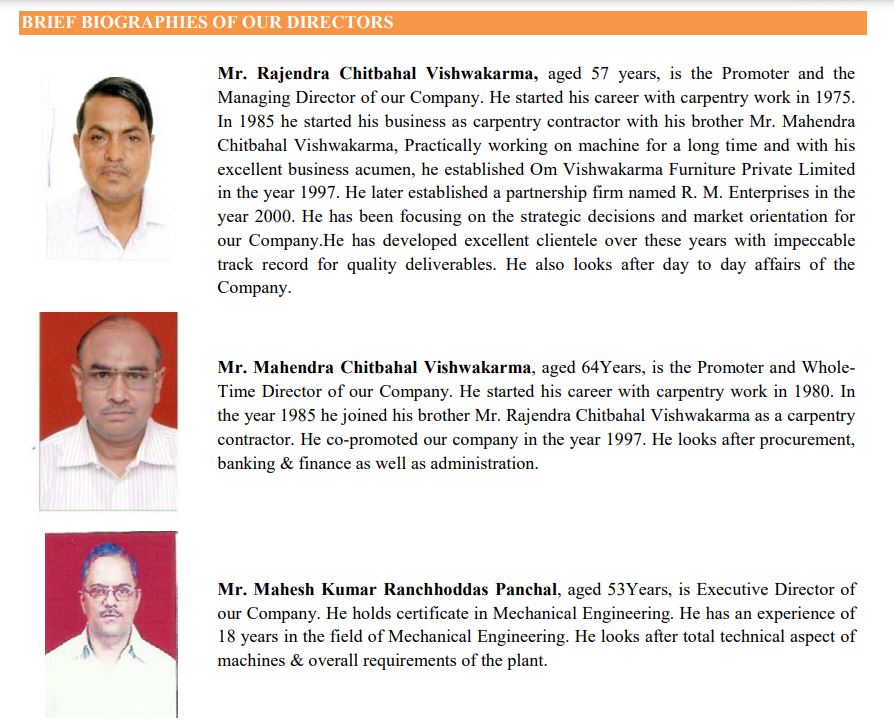

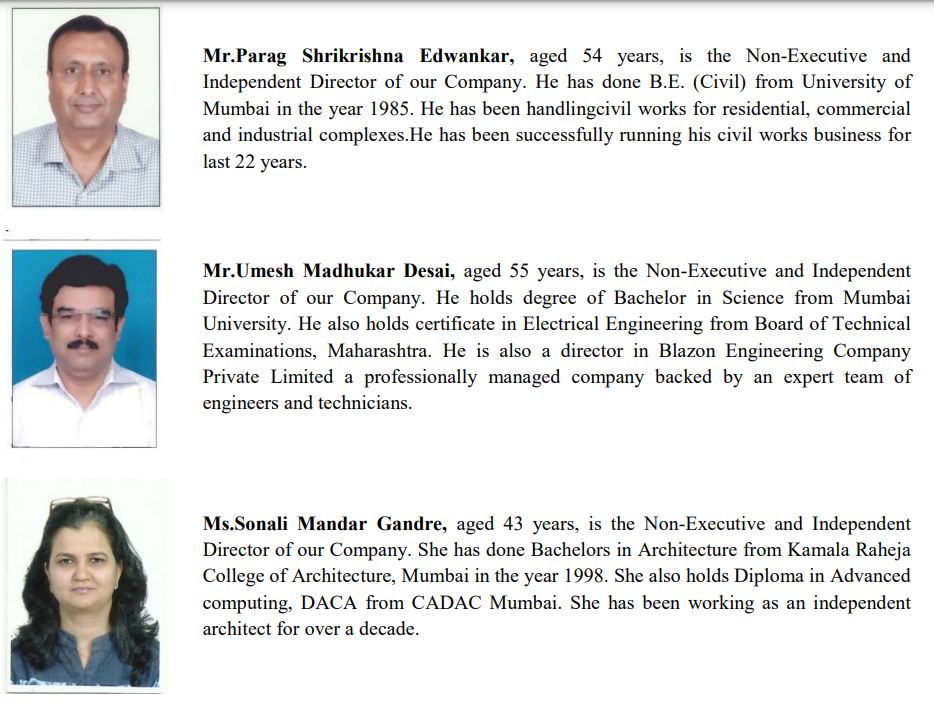

- Experienced Promoters

- Established Presence: Existence since 1997 shows it’s a genuine business not like many SMEs born in last 5 years to make money out IPO mania.

-

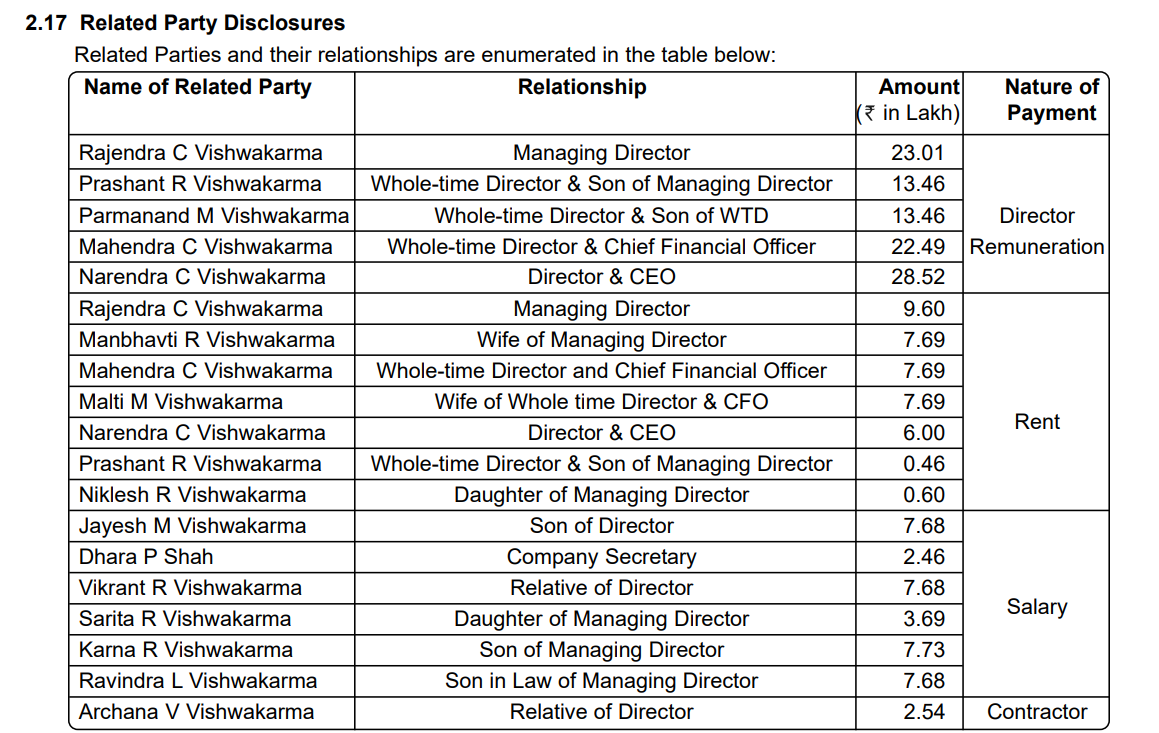

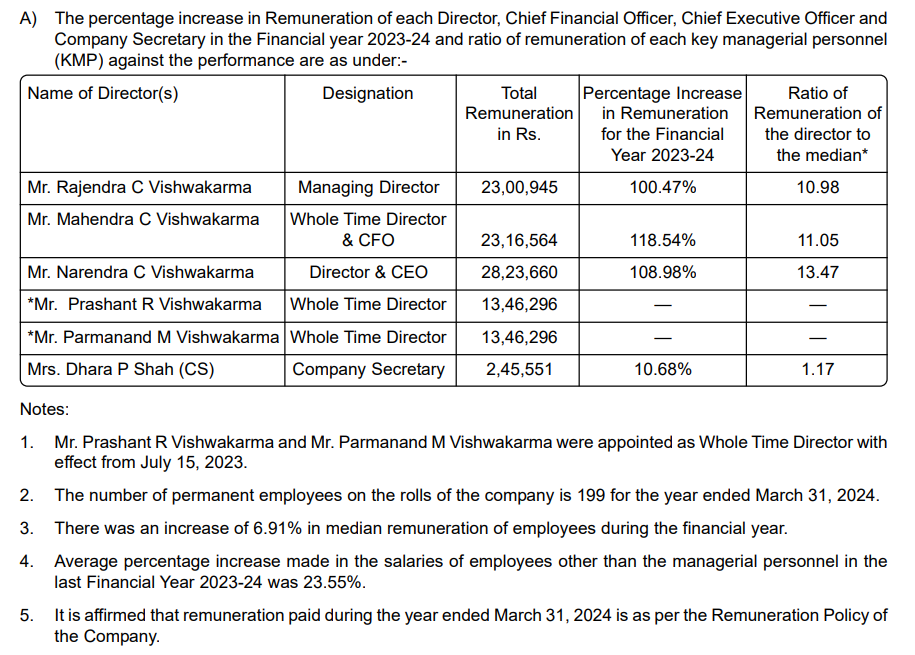

Credit Rating: It’s a rated company, Rating available since 2014 – (Way before IPO)

As per CARE there are total 50 million SMEs in India and out of these only 5% are rated.

https://www.youtube.com/watch?v=l93mEsCkkOA

Why only 5% SMEs are rated ? They don’t want to open up their balance sheets to the world, truth is most of them won’t be able to compete if they start paying taxes.

This again shows these guys operate at the top of integrity level, they preferred to operate in white in the most unorganized sector of all.

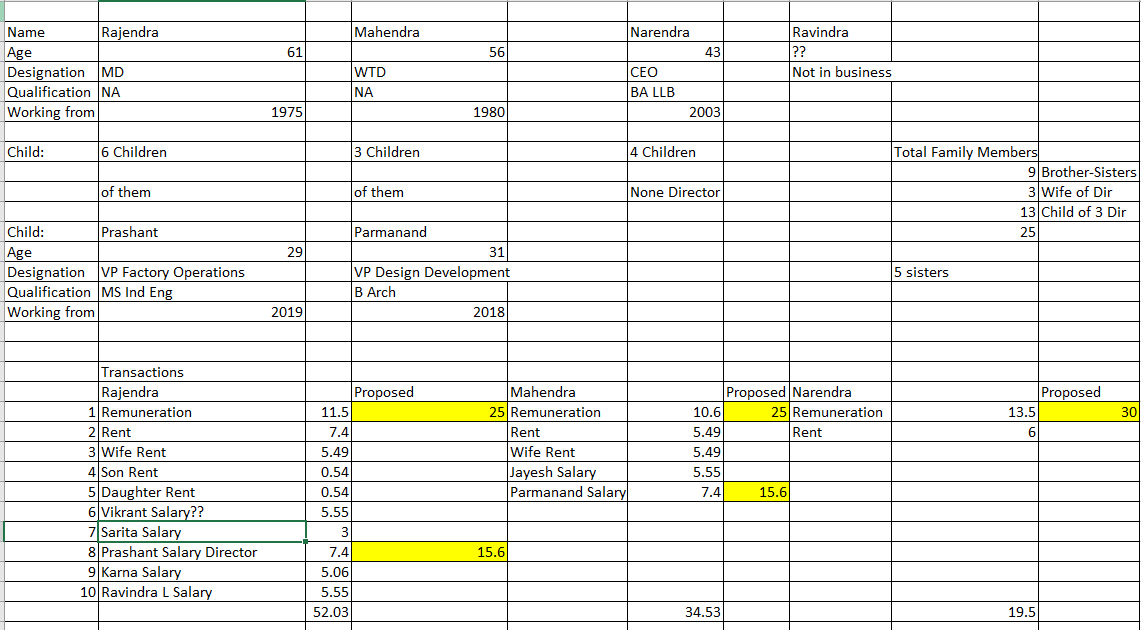

4) Strong Clients Base. Their key Clients are:

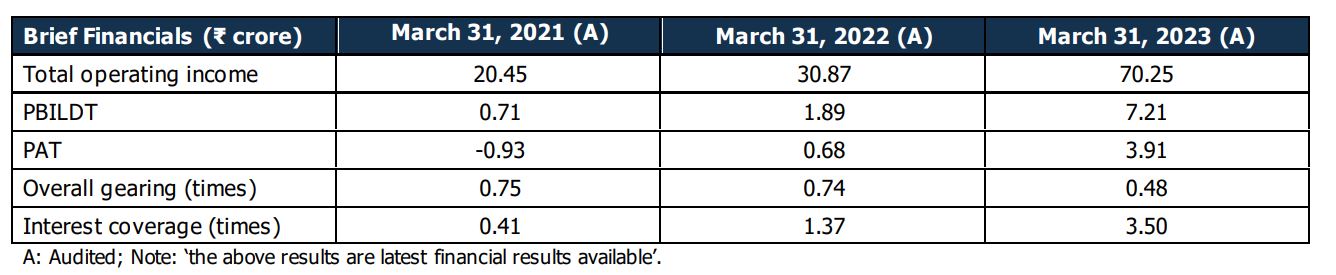

- Their revenue is 90Cr which is greater than M. Cap of 60 Cr.

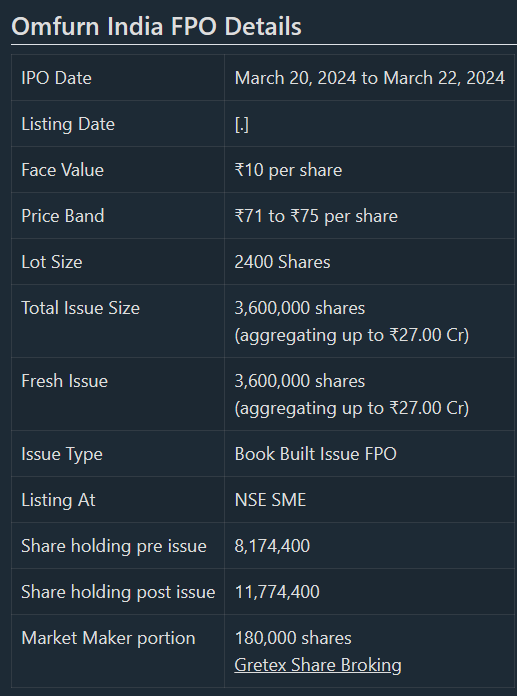

Highly Under valued. it’s a Microcap company shares are available only in lots sizes (2400) No’s

Conclusion:

Omfurn India Limited emerges as a promising investment opportunity. Its long-standing presence, experienced leadership, creditworthiness, and robust financials contribute to a compelling investment case. The company’s alignment with the growth trajectory of the Indian furniture industry further enhances its potential for value appreciation. However, investors should conduct thorough due diligence and stay attuned to industry trends for informed decision-making.