Ola slips to fifth

4 Likes

Ola has indeed slipped to 5th. Apart from that it looks from the data that the GST cut on ICE vehicles has dented EV industry as a whole. Ola’s transition to own cells may have taken more time than expected. That is the only explanation I can think off. I would track closely for at least 1-2 more quarters before forming an opinion on the trajectory of the company.

As of now it looks like they won’t be able to break into EBIDTA positive territory in Q2. They can do so in Q3 due to festive demand and even can continue in Q4. But it is the non festive season when we shall see if the demand has truly increased or not. As more Roadsters are used, people will become aware of the product. Service will be of utmost importance now.

Ola is planning to launch service guarantee in December. I visited a showroom recently. Demand is constant, and I was told that even for battery or motors, the replacement comes within 1-2 weeks. They give a spare battery or new vehicle till that time.

For this FY, I see sales to be below 3 lakh vehicles - somewhere around 2.8 to 2.9 lakhs. I will be surprised if they breach that. Next FY, can be EBIDTA positive for auto business though.

To determine consolidated EBIDTA positive timeline and PAT positive timeline will be very difficult with so many moving parts. Let us first wait for the 5GWh capacity to come online in Gigafactory.

5 Likes

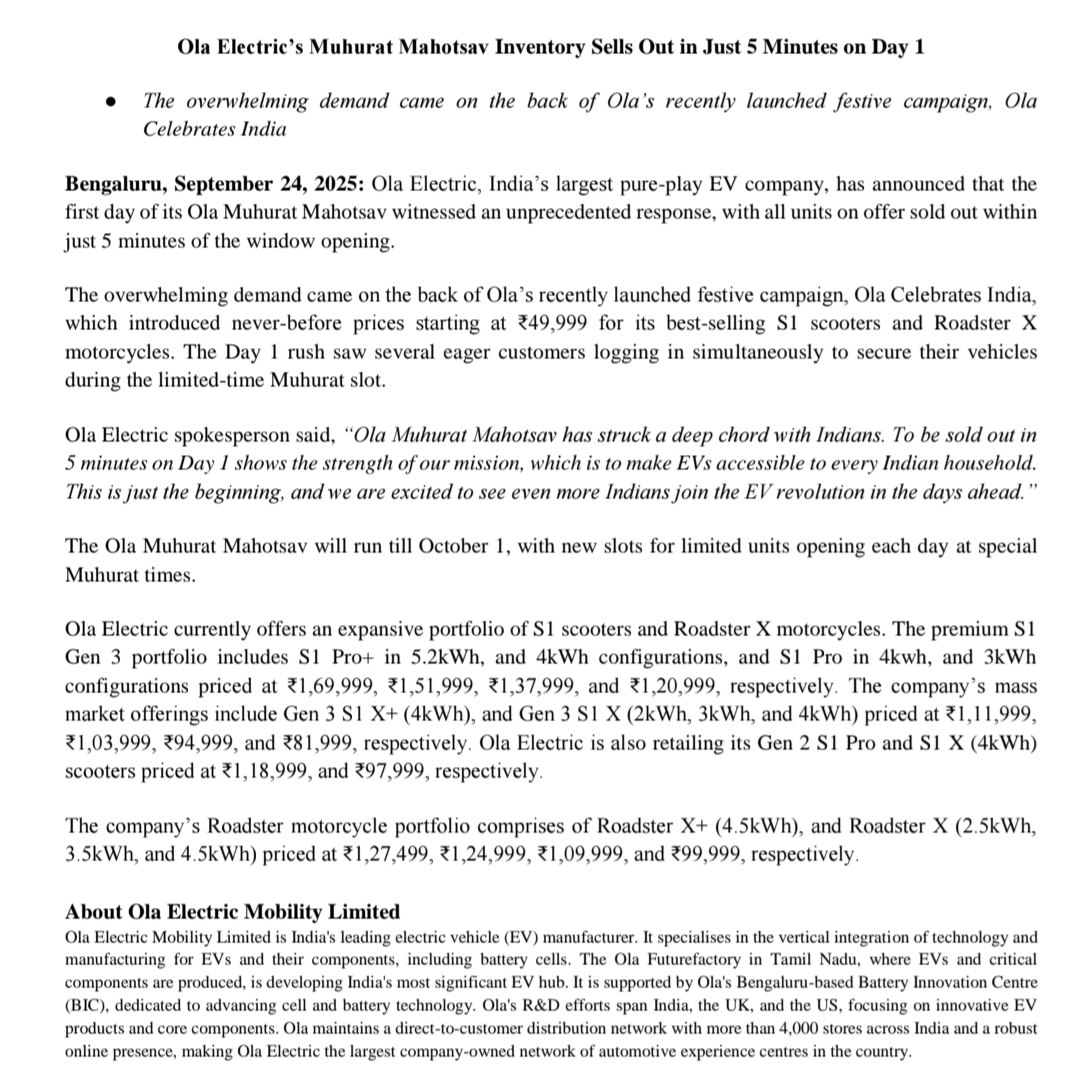

Why so much of discounts given on products of the company in the name of OLA celebrates India Campaign with the introduction to Mahurat Mahotsav? I mean the discounts are to the tune of 30-35%. Is the company clearing inventories? Or it simply is selling at heavy discounts out of desperation to increase sales (sales data is dismal for the company as it has slipped to 5th spot from 3rd)?

Are other e2w makers also offering comparable discounts?

2 Likes

A few things have happened since I last posted here. Let us first discuss the discounts, then the sales and then the announcement of 30 Sept, 2025.

The discounts first. Muhurat Discounts are likely to be very few in number. I have seen perhaps 1-2 people who claimed to get at such discunts in social media. In my estimation, it is on less than 50 vehicles per day. This gives them 2 advantages. first, the free publicity. Second, phone numbers of people who try to book. Then the sales channels start calling these people for demo etc. However, the expectation of discount also makes people to defer their purchase. So, not sure of overall impact. LEt us see.

Then the issues of sales. In September, we had shraddh paksh. So half of September did not lead to any significant sales for any company. Then there was the GST cut announcement for ICE vehicles. So, EVs were sort of discouraged by the govt. This is seen in sales of all EV companies. On a combined basis, less 2w EVs were sold by the top 5 companies in September than in either July or August. I suspect the rains also played a part. In fact, only yesterday did some companies sell more than 2000 vehicles in 1 day(during last month). Ola is specially hit in sales though. On a monthly basis, it is at number 4 and on a quarterly basis on number 4. Although on a quarterly basis, the difference between Ola, Ather and Bajaj is within 2000. TVS is undisputed leader for now.

Ola had a target of EBIDTA positive quarter for which it needed to sell 75000 vehicles in these 3 months. That has not been achieved and they missed by quite a bit i.e. around 17k! I estimate Q2 sales to be 57-58k. They sold less vehicles in Q2 than in Q1, but except Hero and Ather, the other 3 too have sold less in Q2.

The reasons for lower sales of Ola could be multiple. I can see the regular posts about service quality, even in Roadsters which are supposed to be new Gen 3 products. This has obviously led to erosion of public trust in company.

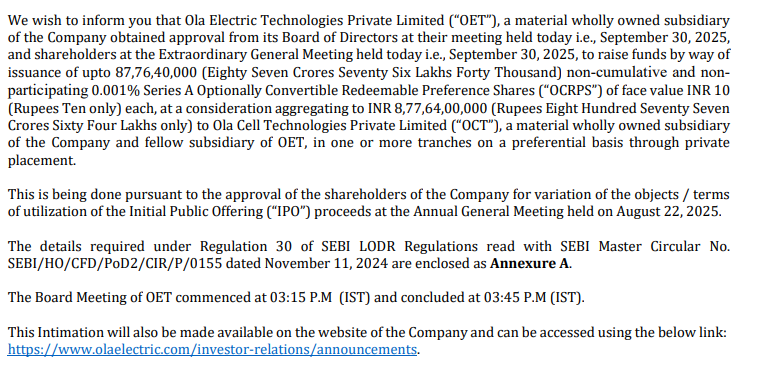

Now coming to third issue of the fund raise announcement. The operating part is this :

This transfers Rs. 877 crores from the Cell company(Gigafactory) to EV company(Futurefactory). This is as per the decision in AGM on 22 Aug, which allowed variation in IPO terms and allowed taking out 1227.xx crores from Cell to EV company. This means they do not need expansion of Gigafactory capacity from 5GWh for a few years. This is a sensible thing to do specially as the cell yields as of now are in 60s. Until and unless we have cell yields in mid 80s, it should not be run even at 5 GWh capacity. That will leak a lot of money. The yield improvement from here can take 2-3 years or even more if we go by Tesla example. It is better to spend on EV design and more importantly service in the meanwhile. I suspected some financial difficulties too as early last month, they fired 1000 people. Hopefully, this money will help them to get back on track.

Now, what are my expectations in future? I think October will be a good month for all companies due to Diwali. Even today and tomorrow they can sell a lot of vehicles. If we have to watch, we must focus on November month. That will be a normal month and also give us some idea of where the money is being used by then. If there is service improvement, we shall see that by December. The number of vehicles outside service centers should reduce substantially. In my town, Ola has improved the services over last few months. I have heard similar reports from some other places. They do need an operations guy, a COO, for uniform service experience, training of mechanics etc. I will judge them after December on this front because they have promised 3rd party mechanics and doubling hyperservice centers by then. Let us see.

Disc: Invested. No transactions in last few weeks. Biased.

7 Likes

In my opinion giving so much discounts for mass producers is never a good thing for the business specially when price point is not the issue but SERVICE. Instead they should provide more info on the status and improvements in the service call management and closure. That would give them more positive brand image and boost sales by boosting confidence of future buyers. As you have highlighted too, the heavy discounts would just defer sales by buyers in anticipation of being lucky in getting e2w on discount or may be in worst case customer even move to other OEM after getting frustrated by not getting discount as atleast other OEMs are selling at uniform prices and he won’t feel like he missed the bus.

Also regarding the sales of roadsters, i live in a metro city and haven’t seen roadster on road yet and it has been 3 months since company launched it.

The dropping sales specifically is not encouraging either as even Ather is having more sales (which sell at a premium compared to OLA).

All in all, most positive things seem like a noise for now until company comes up with something concrete on ground.

Dis. - invested but may exit given an opportunity.

2 Likes

Can you please share the exchange filing saying 5000 sold in 5 min on discount? I have not seen any such filing and I track very closely. There is no single day with 5000 or even 2000 sales even. So this is your misreading of something. Roadsters came to most stores just 5-7 days ago. Not even 5000 total sales as of now in the country.

As for Ather, one factor for recent bump in sales is BaaS, same as in Hero. That is lower price per unit. You can get Ather Rizta at 75k today with BaaS. So, not at premium.

3 Likes

Sorry i must have misread the data and have edited my response. The disclosure said about whole units for discount sale being sold in 5 minutes.

Regarding the sales increase in Ather and Hero due to baas. It is just that battery is provided separately on rental or purchase basis separately from e2w purchase. How that helps in increase in sales? Battery is the one of the costliest part in an e2w and the buyer will surely add it’s price while considering a buy. And 75k plus battery will make it premium price compared to OLA.

1 Like

Cashflows are important to individuals as to companies. With BaaS, I get to own vehicle today at 75k in comparison to 1.5L, I am likely to go with 75k option. The running cost would still be same as or lower than an ICE vehicle. It also insulates me from battery issues, which is the number 1 fear of many buyers.

Ola is planning the same but in the lower price points in Gig range. Should be done with other models too. With 4000 touchpoints, Ola is actually best positioned for this.

3 Likes

I think baas is just a temp route to expand the market.no way companies can pay for batteries when mass adoption starts.

No, even the govt is going to promote BaaS, but more so in larger 4 wheelers. I think BaaS makes sense for consumer in an environment where battery failure is a risk. I personally would prefer to take a BaaS vehicle. It would be substantially cheaper than an ICE vehicle and the running cost will be equal to a petrol 2W. It is win-win. When mass adoption happens, expect the batteries to be standardised and swappable with other brands, just like you can for normal inverter, car or scooter batteries in ICE vehicles. In such a case, battery companies would make a lot of money on BaaS as production costs would progressively come down with scale but BaaS costs would be anchored to whatever they are now plus they ensure smoother cash flows over many-many years. For Ola Cell Technologies, it could be a very good proposition though it is in a distant future as of now.

For consumer it is best for companies it is a disaster.lets say a battery costs 33 percent in a scooty.to sell ten lakh vehicles company would have to spend 3300 crores to fund batteries.

Of course, but look at the returns. Let us say everyday trip is 40km/vehicle, which should be the average. This is 50 rupees per day in battery leasing. Over the year, it is 18000+. They recover the cost in 2 years which is 50% return! So, calculating at 3300 crores, they are earning 1800 crore per year. Any bank would fund it. I would fund this if they dilute equity.

In Bangalore, most of the Gig workers ( Q-com delivery agents) use Yulu bikes (no DL and helmet required to ride these E2W). And in the last 2 years or more they have the battery swap stations operating in many places. It needs just a small shop. I also see Honda battery swap stations operating in a nearby HP petrol bunk. No idea who uses these Honda batteries. So BaaS may not be a temp route.

Excellent points. In addition to this, the fuel top up time will be equal or less than filling up ICE (petrol, diesel, LPG, CNG) vehicles.

1 Like

Pessimism has come again in Ola Electric share. September sales have already been discussed above. October sales for first week seem to be decent, at least in comparison to September. As of now, Ola stands at number 4. Only the results will tell if this ranking holds for sales revenue too.

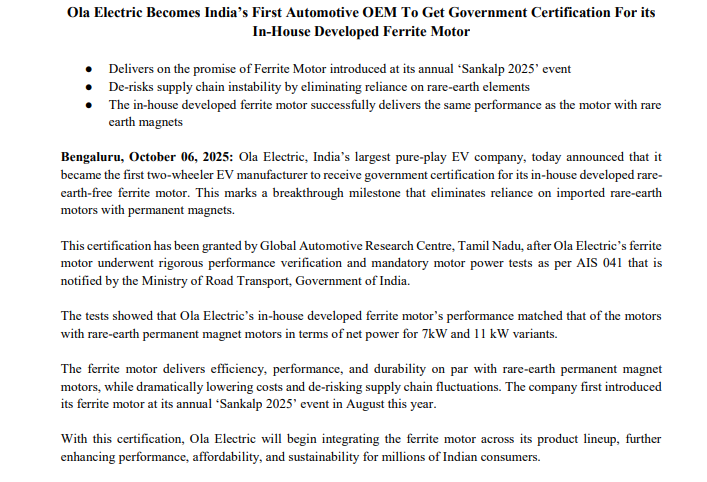

Today Ola told that their ferrite motor has been approved by the govt.

This will take some time for homologation with various models and then into commercial production, but will certainly reduce costs for the company and reduce significantly. This is a significant technological milestone. To my knowledge, apart from Ola, Sona and Ather have also almost developed Heavy Rare Earth Free motors, but they are not ferrite ones, but light rare earth based motors. Those are not yet ready for production too.

The benefits of these motors will flow only after 3-4 quarters as homologation and PLI certification is received.

Ola has also started integrating Bharat cells in the Roadster X+ bikes. However, even there the company will lose money as of now. The wait for 80% yield continues. As soon as these two things align, we could see the number of vehicle sold required to reach profitability fall significantly. I asked ChatGPT and it says even 12-15k would be break even if these two things happen. That would be fantastic, though I think 20k per month is a more reasonable number.

The battery business on the other hand would continue to leak money for a while. Bhavish said it would require 5 GWh production to break even. I assume it is at 85% yield. I think we still are 2-3 years away for that.

Disc : Invested. No transactions in last few weeks. Biased.

11 Likes

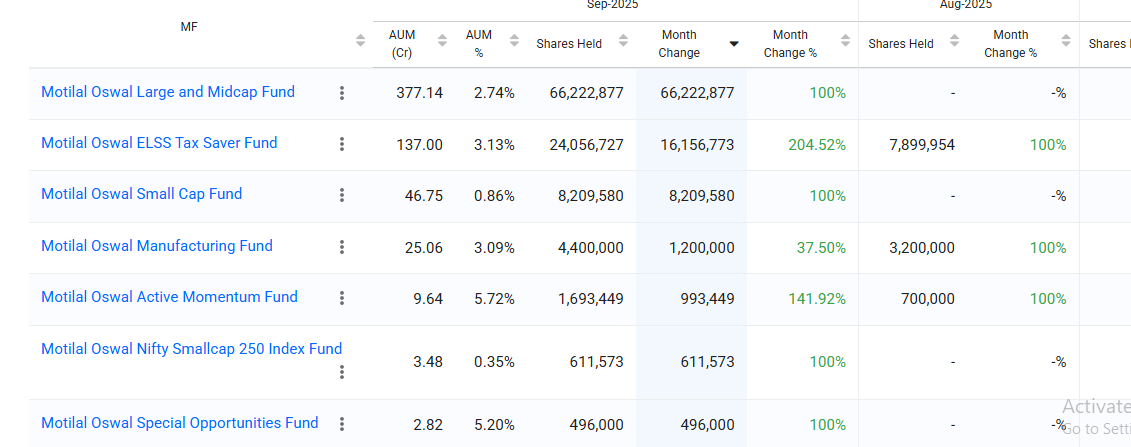

Helios Mutual fund sold off about 23% of their position in Ola Electric in September, I assume in early September. Currently they have 66 crores odd shares in their Flexicap fund.

However, Motilal Oswal has increased its stake multiple times and now owns more than 2.5% of the company. That is more than 550 crores of shares across its Large and Midcap, ELSS, Smallcap, Manufacturing etc funds.

Will be interesting to see if other DIIs also accumulated during this downmove when the share was in T2T. Also worth seeing if Softbank has sold more of their stake.

5 Likes

No relief of negative news for Ola electric.

Disc: Invested.

3 Likes

Very strong conviction from Motilal, glad to see that. Risk reward definitely looks favourable now, hope company delivers on its promises now to rebuild its credibility - key triggers to watch out:

- Near term triggers - Roadster volumes uptick and PLI linked incentives to further improve margins

- Long term triggers “Tech driven growth/margins” - Indigenous Cell tech and ferrite magnets to cut costs and reduce dependency

Tech can drive significant moat, but execution is key now to regain some lost ground

Disclaimer: Invested as High risk/return play

Lost market share may not be regained easily, but they can turn profitable with even a 15M% share. That is the main thing.

Another trigger is a new products after the Roadster series is stablised. Last year, they spent significant money on developing a 3-wheeler. At some point they have to release it. My guess is Q426 or Q127.That will add to revenues pretty quickly as it is likely to be the least expensive in a very price sensitive market. The competititve price will come from own battery.

3 Likes

And hopefully Bhavish pushes these 3 wheelers using Ola cabs.

If you want to know science behind Ola’s battery pack and what makes them affordable, light weight and scalable.

3 Likes