Motilal Oswal bought Ola in a lot of funds. In my last post, I made a mistake. They have bought at 54-55 levels.

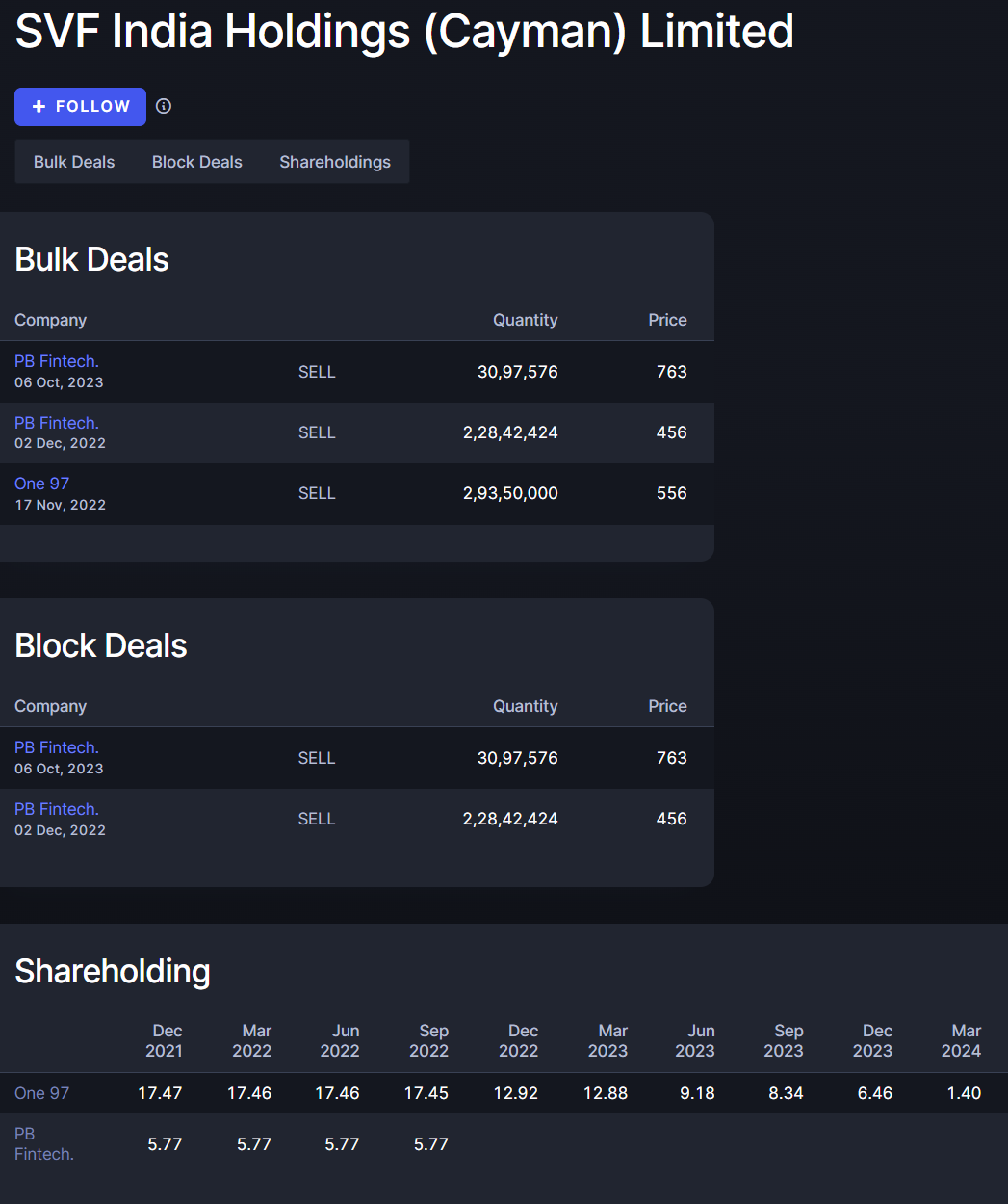

On the other hand, Softbank has sold 2%+ shares of company(out of 17% it had) over 15 July to 2 September. This seems to be normal profit booking. However, there is no guarantee that this selling is over. In short term this might make people jittery. However, FII exiting and being replaced by DII has been the theme over last few years across the market.

SoftBank Eternal exits. This is very likely the beginning of selling. If Ola’s sales volumes pick up, all of it will get absorbed. Eternal is already up 3x since then, I know comparison is irrelevant, just highlighting how buying and selling is a non-issue as long as the company’s performance keeps improving.

Have you read the auditor’s report? I have. Here is the relevant portion.

“In our opinion, except for the possible effects of the material weakness described below in the Basis for Qualified Opinion section of our report on the achievement of the objectives of the control criteria in respect of one of the wholly owned subsidiary company, the Holding Company and such companies incorporated in India which are its subsidiary companies has maintained, in all material respects, adequate internal financial controls with reference to consolidated financial statements and such internal financial controls with reference to consolidated financial statements were operating effectively as of 31 March 2025, based on the internal financial controls with reference to financial statements criteria established by such companies considering the essential components of such internal controls stated in the Guidance Note on Audit of Internal Financial Controls Over Financial Reporting issued by the Institute of Chartered Accountants of India (the “Guidance Note”). We have considered the material weakness identified and reported below in determining the nature, timing, and extent of audit tests applied in our audit of the consolidated financial statements of the Group as at 31 March 2025, and the such material weakness does not affect our opinion on the consolidated financial statements.”

Now, what it may change is inventory-related numbers (stock, cost of materials, changes in inventory). And how significant is this?

From a technical point of view, it is there but practically speaking, this is a very low amount. That does not mean they should not rectify it. However, media has used terms like “crisis”, “Lack of financial control sweeps across Ola Electric” very irresponsibly in this case.

Now please tell me how could this " significantly affect the revenue/profit figure"? This is related to inventory and balance sheet, does not even touch revenue in any manner.

Both authors carried the same piece on Bhavish missing board meetings, few days ago.

The coverage feels biased, amplifying minor issues purely for the sake of headlines.

That’s not the only pattern with the news agencies or their reporters but also with social media, there was nothing shared while the stock corrected from 55 to 40, but as soon aa the stock moved above 55, i started seeing videos of service issues and showrooms filled with inventories cropped up on social media (reddit/Instagram). This is not to say ola doesn’t have these issues on a smaller scale but the timing is very suspicious.

I agree with you. I have been tracking Ola since its IPO. Every negative event, small or big, gets amplified in the media. I also noticed that some big names in auto reviews like Autocar, Powerdrift etc do not review Ola bikes. I suspect this is because of the strong hold Bajaj, Hero and TVS have on them. Yes there are service issues with Ola, but so do the auto giants. Why don’t they review the latest products from Ola? It’s a significant improvement over the previous generation, but I guess these review sites do not want to upset the biggies.

I feel all these big names are scared of Ola, and they should be.

Disc: Invested avg price 60.

As per Mint’s article, In dec quarter inventory was Rs 369.5 Cr against submission to bank at Rs 344.2 Cr. Similarly, Inventory was Rs 1186.9 Cr against submitted to Yes bank at Rs 1220.8 Cr.

Above 2 items are part of current assets and only benefit one gets by inflating the number is higher WC limits. In above data points, submitted number to bank in one instance is lower by 25 Cr and in other incidence it is Rs 35 Cr higher. With standard 25% margin, one may loose benefit of Rs 18 Cr and other place it would be benefit of Rs 26 Cr. If intent is to inflate number to avail higher limits from bank, then why would they show lower at one place. Secondly, is it worth doing all this to get some 20-25 Cr??

In recent AGM, approval is obtained for utilization of part of the money (Rs 5500 Cr) raised in IPO towards following:

R&D - 1049 cr

Organic growth initiatives - Rs 901 Cr

Debt repayment - Rs 395 Cr

General Corp Purpose - 248 cr

With access to these many funds, I seriously doubt any malintent and at best it may be reporting lapses which can be easily addressed. These difference in amount also happens when someone takes record from shop floor on provisional basis while in actual audit after detailed verifications, some differences appear.

It appears to be more of a case of some ego/other clashes between the corporate and auditor rather actual issue of corporate governance.

An auditor’s job is to report; it’s our job to interpret. Clearly, incentives are at play here, this feels like unnecessary headline hunting aimed at maligning the company’s reputation, nothing else.

My only Qs- to all the people, who r saying, a section of media is against Ola, that’s why negative news kept on coming..1st come out of Investment bias..next Ola always in the news ? Why Ather / TVS/Bajaj/Hero not in news ? Do we need to understand, all r paying the media..?

Why Ola mgmt is not correcting internal processes ?

The biggest concern for me in Ola, is People and Process..In terms of Ppl..everyone outside Ola knows, Environment is so toxic..how many people senior ppl left ? Why there is no such allegations against others ?

2nd What Ola is doing to address Process issues ? this is not the 1st time, Feb data was a disaster..why Mgmt is not being proactive ? Do rivals preventing them?

Why Investors need to face a mini bomb blast every 2-3 months ?

A good , leave alone the great part, is not born , unless , Process, Org./People, Tech issues r handled..Just headline mgmt will not help..PayTM learnt the hard way..Hope Ola Mgmt does quickly…

Thanks for the question. Ola is targeted because it is the category creator and biggest threat to other companies’. Ather has been doing this for 12 years. Bajaj, Hero and TVS had models years before Ola was born. Ola disrupted all of them.

Now for toxic environment, it is there in every company. Show me one where it is absent. After the IPO, some people will always leave. The high performing people like Kripa, Mekkat etc were there and still are there. Those are adding value. Ola also had lot of staff in showrooms, who always have a high attrition rate.

After Feb data, Ola took registration in-house. For this, they will answer in next earning call. Management has done extraordinary things and will likely continue to do. A few teething troubles are expected. Investors should expect a lot of volatility, but also a lot of value creation over next few years in my opinion.

Thanks.

Disc : Invested at 41-42 level and tracking closely.

Taking from your analysis done above “FY29 should have EPS of about 2-3 rupees and FY30 around 5 rupees. This is when next phase of expansion should begin. But even at an EPS of 3 rupees in FY30(I prefer to be positively surprised), and a PE of 20-25, it should be 60-75 rupees fair value.”

So if your conservative estimate is for 60 - 75 rupees value in 2030 , is not the current price, with the run up, get fully valued at 62 odd, discounted for time.

At the time you did the analysis maybe the price was around 40 , but given the sharp up move would you still rate it as “safety of principal” in the long run with a conservative outlook ?

As I said in my previous post, it won’t be long before you get a quick-commerce like experience in service.

It will be a game changer; let’s see the execution.

Personally I would like Ola to scale up this (Ola Electric Scooter Service At Home, Pickup - Quite Straightforward) , most vehicles have minor issue of software, sensor ,loosening of parts etc. which can be easily fixed with such kind of service. Customers can book slots and get vehicles serviced at home.

Hi, I would put the PE a little higher, maybe around 35-40, as it should be growing quite briskly at that time. It can do a Zomato too, but I hope it doesn’t though(slow and steady is what I prefer). But let us take 60-75 in 2030.

This is for the 2W+3W (the auto business). Depending upon capacity of battery plant created, I would add about half a billion dollar market cap for every 5 GWh installed. Assume it is 2 bn, which is 16000 crores and in terms of share price, another Rs. 40. I expect a car would be in the works but not contributing anything significant at the time, maybe not even released. So yes, conservatively I would value it at 100-120 in 2030. That should be about 15% CAGR from here(if taken as 120). I don’t know if this appeals to many people. I bought at 40-42 levels and from there I hoped to get 25% a year. The recent move surprised me, although I had done my complete allocation by then.

I’m no expert at valuations, but the way I look at Ola Electric is through relative comparison. Valuations are always relative in nature, there are variables beyond our scope to predict, and no one truly knows what the future holds. For now, Ather trades at 20,000 crore market cap and Ola at a 26,000 crore market cap. To me, the market is assigning almost the same valuation to both companies, while completely ignoring the bike vertical(whose TAM is far larger than scooters), completely ignoring the battery vertical, completely ignoring deep vertical integration, and completely ignoring the platform mindset.

So, I ask myself: if I start factoring in all those elements, what downside and upside could I have from these levels? For me, Ather’s valuation acts as a lower bound for Ola. On the upside, if I add in all the possibilities, Ola should trade at 2–3x Ather’s market cap.

Obviously, if Ather’s valuation falls by 50%, Ola’s projections would fall as well, and vice versa.

This is just a mental model not any financial model, Please don’t ask for math, but that’s how I look at it.

I think this business definitely has potential , but predicting how things will shape up has many degrees of speculation and things could go south just as well.

For me, this would fall in the bucket of high potential , with many unknowable unknowns - and with that unpredictably, allocating or not allocating capital is more tricky than other businesses.

Great work. My take on these kind of bets is Promoter pedigree and their risk appetite along with passion for doing something spectacular. TAM as you rightly pointed out is huge. Nothing else has worked for OLA so far. Taking a call into its future is purely a gut call based on personal assessment. Number crunching etc is purely a mathematical exercise akin to shooting in the dark. Logically, the stock has been butchered to 40 levels, sales figure is still decent despite customer service noise and keeping above mentioned factors in mind OLA can be a risky but worth a shot.

GST cut on ICE vehicles could lower overall demand or may show no growth over next year

Increase competition from legacy players which is reflecting in vaahan data where its sales now stand at 4th position with incumbent like ather taking over its position.

Continous discounting reflects low demand compared to its peers and no pricing power.

The new bike doesnt look promising.

Promoter pledging.

Unnecessary press releases recently showcasing 1 million production and not sales number.

battery cell division yet to be commercialized.

Bad repuation in the market given previous service delivery concerns comparatively Ather is gaining word of mouth publicity in the masses.

Disc- Exited recently given headwinds , i may be wrong :)