That’s probably not your dmat account but your broker trading account which is suggesting the added price as 0 as there were no purchase transaction done via the trading account for those bonus shares…Dmat account would simply show the number of shares held…

2 Likes

Nykaa Pink Friday Sale delivers 75% growth, recording 8 lakh orders, that is over 400 orders every minute on Day 1.

2 Likes

This is nothing short of impressive. However, market participants cannot see beyond the established narrative that is fueled by the quick and sharp drop in price.

I intend to add at the swing low of 160. The bearish narrative that has caught on, can atleast grant me this.

I have tried to compare, but cannot find a peer to Nykaa in BPC. Others are doing bits here and there, but nothing close to what Nykaa is doing IN BPC. I have been told, JIO and Amazon are competition, but I dont think so. The numbers tell a different story.

Valuation seems decent to me, for a company that can grow at 30% (which is because it is the undisputed leader).

I might be off by 20 odd % valuation wise, but no one can really be sure. I dont want to miss a great opportunity, which i believe it is, for the fear of buying expensive.

4 Likes

Everyone seems to be worried about the exit of PE and VC funds. These are the prominent foreign investors buying their shares:

Norwegian Government Pension Fund Global

Canada Pension Plan Investment Board

Morgan Stanley Asia Singapore Pte

Societe Generale

Citigroup Global Markets Mauritius Private Limited

Hermes Investment Funds Public Limited Company

Ontario Teachers Pension Fund

BNP Paribas Fund

HSBC Funds

Goldman Sachs (Singapore) Pte

International Monetary Fund

Bofa Securities Europe Sa (Bank of America)

Rest of the shares are being absorbed by domestic mutual funds and retail investors.

4 Likes

Samit Vartak of Sage One has given his opinion about Nykaa’s valuation in a Morningstsr Interview:

Have you invested in any of the Initial Public Offer (IPOs) which were listed in the recent bull run?

We have not found the valuations attractive. We liked Nykaa (FSN E-Commerce Ventures). We didn’t like the business models of the remaining tech IPOs. Most of them are loss-making and we don’t know when they will turn profitable.

If we are expecting 25% growth from an already existing listed player then we would expect 30% growth from Nykaa. That means you need to generate 3x in the next three years. We arrived at a fair value of Rs. 1.2 lakh crore market cap three years down the line. But this was the valuation of Nykaa when IPO came out. If we have to make 3x, the entry point has to be at Rs 40,000 crore market cap. So we did not invest in Nykaa. We would like to participate in such businesses but valuations have been a concern. You rarely find good valuations in an IPO.

11 Likes

I don’t think I deleted it, although I do delete some of my post which I feel are not contributing to the flow.

That post was flagged by forum members and deleted by the admin. I think sometimes the admin delete posts thinking that the author is promoting the stock. I guess, it’s alright.

In that post I said how nykaa is getting publicity from the issue of bonus shares. And publicity is good.

Devaki responded with the accusation.

I am no expert in corporate gov, so I chose to make a note of it. And be on a look out for any such untowardly actions.

3 Likes

Being a very few of the profitable Ecommerce firms, Nykaa was talk of the town at the time of IPO.

Like many other investors, I too wanted to own this profitable tech business.

The brilliant listing, the big guns minting money, I waited for my first buy and started following the firm closely.

Quick 10-11 months after listing, and near to the uplifting of lock in period, Nykaa bonus/split startes to make the noise.

Like many others I too found it to be a gimmicky move to uplift the sleeping giant, move the share price up and give a profitable exit to pre IPO investors.

I ignored and decided not to invest in the firm for shirt to mid term and stopped following the business.

And then today morning, I happened to go through the latest video from Think School YouTube channel and got aware about the ethical but not in good taste tactics from the company and here it is.

Suppose you owe 1 share of Nykaa at 1125 At IPO price , and plan to sell on 14th Nov at the price of 210

(Most of the pre Ipo investors wanted to do that after the 1 year lock in period)

Now see what happens if you exited your IPO holding on 14th Nov

So that 1 share of Nykaa has split into 6 shares of Nykaa each worth 210

5 bonus shares , 1 existing share.

Tricky part is only that 1 share is applicable for long term capital gain/loss, in this case loss and rest of the 5 shares are bonus shares and come under STCG

So LTCL = 210 - 1125 = -915

And rest of the freshly gained bonus shares come into short term capital gains(This complete holding is considered as bonus holding, so complete holding coming under profits)

So STCG = 5*210 = 1050

15%of 1050 = 157.5

So net short term profit = 1050-157.5 = 892.5

So total amount that would come to your account after selling 6 shares on 14th Nov.

210 from 1 existing share

892.5 from 5 bonus shares

Total amount that you own = 1102.5

So the net loss if sold on 14th Nov after taxes = 1125-1102.5 = 22.5

Now think about the pre IPO investors and many such big investors that get locked in for 1 year post IPO.

Basically Nykaa tried to stop them from selling post lockin period by this ethical but “not to be taken in good taste” tactics but they failed, many of the existing pre ipo investors still went ahead with selling the Nykaa shares.

Post this Nykaa’s reputation has surely gone for a toss.

P. S. : Not following the business any more, not invested.

Sources : Think school YouTube channel (latest video)

10 Likes

Sharing the video link as well - How Nykaa’s Genius Financial Strategy Backfired? : Nykaa Business case study - YouTube

Quite detailed and nice explanation

1 Like

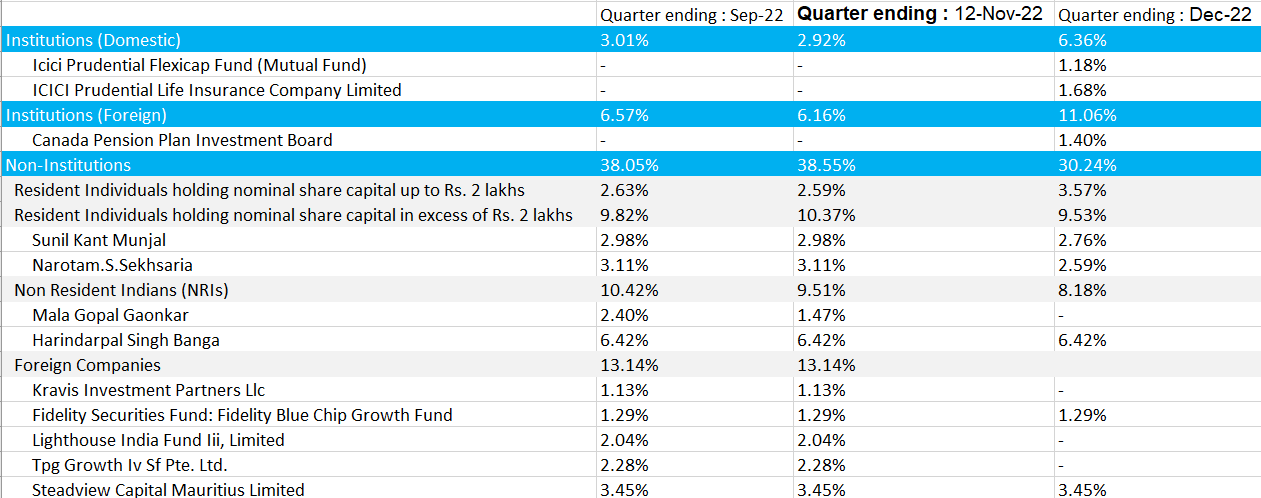

Inferences from BSE shareholding filings of Sep-22 and Dec-22

Overall Equity Shares- 285 Cr.

Non-promoter holding Shares- 136 Cr.

- In Sep-22 filing, concentrated positions (with Big Hands/Pre-IPO investors or Early Investors) had 80 Cr shares, rough approximation per my understanding.

- In Dec-22 filing, concentrated positions have reshuffled in below manner:

- 26 Cr were sold. 4 parties holding 86% of these shares completely exited. Bought by retail, MF and Insurance companies

- 22 Cr are still with parties that sold partially, contributing to the above mentioned sale ( might be participating in the ongoing sale)

- 32 Cr shares maintained status quo. In this, 56% is with one name.

In nutshell, I infer that:

- Insurance companies find value due to their long term horizon.

- Big Hands who are in rush to exit will do so irrespective of tax incident created due to Bonus share or ongoing price fall.

- Base formation shall start in Q1FY24.

Disc: Invested

2 Likes

Just remembering what i said 15 months ago, truth has started revealing. Naayka has lost 70% market Capitalization and shoppers stop has gained 150%. Stock will find its real value over a period of time and markets are supreme.

3 Likes

Things are unfolding now at Naayka, still lot of PE lined up for exit, now the real performance and operations will be analysed by markets, still valuations are in bubble territory.

1 Like

Would be interesting to know if he’s considering Nykaa now?

Current mcap is 36k cr and it is currently at under 7x FY23E sales.

Sounds cheap given the fact it is growing the topline at 35%+.

Not too concerned about profits at this stage since the unit economics are strong.

2 Likes

Valuation matrix for retail companies is based on EV/EBIDTA level, compare naayka EV/EBIDTA with existing retail like AB fashion, Arvind, shoppers and trent. All have hybrid model with online and offline mode. Brand comparison will take Naayka last in the table hence moat is very weak. Too me its still too expensive and avoidable bet

The problem with nykaa as I understand is it has a good business model.it is placed at the better end of the value chain where the retailer/distributor often can command higher premiums and customer retention to further cross sell products. Where it has failed is aligning minority investors interests with the company. Market has punished it for that and rightfully so.

Personally I feel its a very long battle to see nykaa became shareholder friendly.

Disclaimer: was invited. No transaction done in last 30 days

3 Likes

Why do you feel it will be long battle?

Hi- What’s the basis for this conclusion? I understand that bonus trick caused a lot of narrative around this topic. However, the same primarily caused a heavy tax burden on 9 entities/individuals.

In recent times (bonus issue transition period - Sep to Dec), few of these 9 entities/individuals (Pre-IPO investors) were on a selling spree whereas minority shareholders in the category of Institutions (Domestic and Foreign) and retail (Resident Individuals holding nominal share capital up to Rs. 2 lakhs) were buying and increased their holding. Hence, I infer that bonus triggered sale was a moment of joy for most of the minority shareholders.

Data for reference:

1 Like

I don’t see anything that the management has done which is untowardly.

IPO was mainly to strengthen the business. It wasnt an FPO, like mapmyindia etc were.

Only way the early investors are going to get an exit, without whom the business won’t be standing, is by selling in open market. profiting are the terms of investment.

Management tried to reduce this flow by doing the Bonus. Did nothing to damage the new investors.

Media creates “sansani” for myriads of reasons/vested interests.

Amidst the volatility, stock has crashed. Buisness, however, is still pristine. GMV growth 30% +

Without posting a losing quarter.

6 Likes

How will brand comparison take Nykaa last in the table? If at all, it has superior brands, superior customer engagement, and higher quality of customers (going by the average order value).

1 Like

This works for a Debt provider, interest coverage by x times of EBITDA. Equity investor could expect to benefit only from a sustainable Net Profit .

Offline businesses ,which you named, have real expenses after EBITDA - Interest Cost for leasing at the prime locations, Depreciation Cost to continue maintaining pristine physical outlets. Hence, their NP is erratic while B/S is heavy. In turn, ROE remains anemic. I expect that Nykaa will keep these costs under control and achieve respectable ROE in the long run.

1 Like

First of all business must have a moat to generate ROE, you need to understand the retail business first before concluding longterm ROE, Naayka is a new kid on the block, will face huge challenges going forward, risk reward ratio is still very low, it has to reach a market cap of 6000-8000 cr where business can be analysed again. EBIDTA generated by ABFRL is 2200 cr, Arvind Fashion is 450 cr, Shoppers stop is 700 cr, Naayka will not achieve this even in next 10 years.