Retail is ever expending business hence you will have large non cash items in balance sheet which is a good sign for turnover growth. E commerce is a most fragile business when it comes to beauty products which is seen in Naayka’s stock price and will be visible in upcoming poor results. What is point if opening offline stores when you siphoned off retailers money claiming only online retailer.

Yes it is interesting to note the share holding pattern presently…

FII and DII have added in last quarter and only the retailer were sellers, promoters have not sold much

There was a time in the Indian market when the FII played with the retailers…

Is the same game now being played by DII and FII both?

Eagerly awaiting this quarters numbers to throw light on growth story still intact or not…

(shareholders data taken from ticker tape app)

2 Likes

In continuation, Guys my apologies if someone feel offended as a valuepickr member I am trying to put my observations on this thread so that everyone invested here can have a relook in their conviction, our ultimate aim to protect capital and find right value of stock.

- Naayka has capital base of 287 cr shares now which i feel is increased to provide liquidity in stock for easy PE exit.

- Margins have dropped to 4% from 13% in Covid era as offline plus online mode started now which will continue

- I saw offline stores in Noida, Gzb, Delhi

- Customer response is not enthusiastic, even sugar doing better right now

- Intense competitive market where MAC, Sugar, Shoppers stop, Sephora, and upcoming reliance will eat up margin or growth will be difficult.

- Current market cap of 38000 cr with EV/EBIDTA ratio of 190 is unsustainable.

- Any poor results ( growth less than 35% atleast) will invite strong distribution

Fair market cap with current margins is no where justified more than 8000 cr which means stock may loose market cap by 75%.

Sorry to be blunt however please keep a close watch.

17 Likes

The debate around Nykaa can be broken up into two parts:

- the business and its management

- the stock valuations

For its business, in my opinion, it is one which has very high competitive dynamics. There are boutique brands and regional brands along with pan-India and international brands in this space. Also, in my limited research, I have found that women tend to experiment with products from different brands.

With the bonus fiasco and aggressive IPO pricing, the management has given out a slightly negative perception to the retail investor community.

December is usually a very good quarter for them and we need to await the results for this quarter to see how well it has done.

On the valuation front, it is way too expensive and given the mediocre business characteristics there will likely come a time when the stock will be in a sideways consolidation for years or fall considerably till it comes to a peer-comparable valuation.

What people often forget is that PE players pay a premium for scarcity. In public markets that is not there. A company needs to show profits, longevity of growth and sustainability of business dynamics to be able to command even 2-standard deviation (+ve) valuations.

If one is investing their own money, it is best not to get enamoured by media hype and narratives (sometimes paid for as surrogate ads) and stick to basic common sense business and valuation principles.

47 Likes

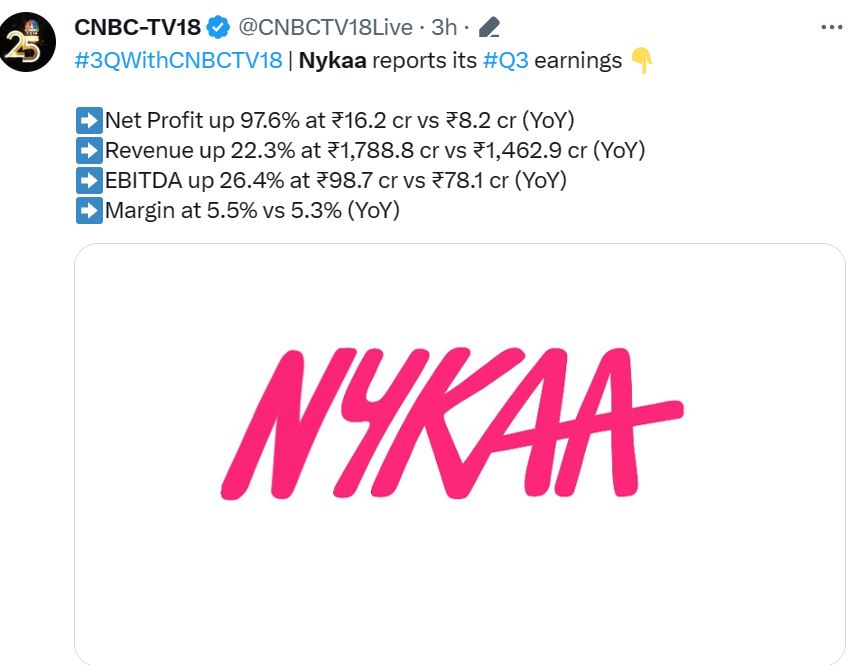

Sales sharply up.

Again, a quarter with no loss is cash. Still a Great business, valuation I don’t know for sure.

Interesting development by Reliance launching Tira (Omnichannel online/offline cosmetic retailer)

2 Likes

Nykaa did amazing capex last quarter. It includes:-

- Retail expansion (+43% YoY in-store area)

- Warehouses (+79% YoY in warehouse capacity)

- Office space (+68 YoY in office space)

However, 1st & 2nd are likely to be paused for the next 12-18 months.

They are also really keen on optimizing their margins. Either by decreasing marketing and advertising spending or scaling up their eB2B business.

5 Likes

Can someone please share the contract manufacturers list for nykaa. thanks

Note on Nyka

NYKA (Mcap – Rs. 43,318 Cr)

Summary

Nykaa’s leading position drives self-reinforcing flywheels, which further bolster strong network effects. The brand affinity it has cultivated with consumers draws them to engage on Nykaa’s platform. As consumer traffic increases, so does the number of transactions on its platform. With more consumers and transactions, there is a growing imperative for more brands and sellers to associate with Nykaa, thereby expanding the choices available to consumers. Leveraging its brand strength, the company has successfully added and will continue to add more lifestyle verticals and adjacencies on its platforms, thereby expectedly increasing its consumer base. The experience flywheel further accelerates the transaction flywheel: more consumer data leads to better analytics, resulting in higher engagement and a superior experience. This, in turn, fosters the creation of more content, which further enhances consumer experience and drives transactions.

Background

In the beauty industry, Indian women previously faced challenges such as limited options and lack of convenience. Recognizing this gap in 2012, Falguni Nayar, a former senior managing director at Kotak Mahindra Capital Company launched Nykaa, an online beauty retailer that revolutionized the market for Indian women. It sells cosmetics, wellness, and fashion products through its websites, apps, and 141 physical stores in India. In 2020, Nykaa launched two new businesses: Nykaa Pro, a professional beauty services platform, and Nykaa Fashion, a fashion e-commerce platform.

Nyka’s revenue segments

-

Beauty and Personal Care (BPC) (85% of revenue)- Nykaa operates with an inventory-driven business model for the BPC category. This means that Nykaa purchases products directly from manufacturers and stores them in its own warehouses. By doing so, Nykaa can maintain control over the quality and availability of its products. Additionally, Nykaa implements an omnichannel marketing strategy, engaging with customers through various channels such as its website, mobile app, social media platforms, offline stores, and events. This multi-channel approach enhances Nykaa’s reach and allows for greater customer engagement.

-

Nyka fashion (8% of revenue) – In 2018 Nykaa launched its curated marketplace for apparels, jewellery, footwears etc. It is building up its fashion business with similar principals it used to build its BPC business: (1) strong focus on merchandising, brand assortment and exclusivity, (2) focusing on premiumization and upselling as opposed to discount-led tactics adopted by competitors.

Others ((7% of revenue) -

Nyka e-B2B - Since India BPC market may increase substantially, 41-50% consumption is expected from unorganized trade. The current distribution system, which caters to the unorganized part of the market, has a few inefficiencies such as fragmented distribution, poor credit coverage, uneven playing field (large brand dominating newer brands) etc. Nykaa plans to leverage and disrupt this via technology through its eB2B platform Superstore. Nykaa aims to buy directly from the brand, bypass middlemen (distributors/wholesalers) and directly supply to retailers.

-

NykaaMan - Nykaa launched NykaaMan mobile application/website in FY21, thus customizing models and experience for men, as also spiking education/awareness among men on grooming/personal care product use.

Industry

•A recent report by JM Financials indicates a shift towards higher BPC spending, with 16% / 14% of consumers spending Rs. 10,000-20,000 / >20,000 respectively, as compared to 8% / 6% a few years ago. The share of consumers spending < INR 2,000 has contracted from 43% to 21% now, validating the argument suggested by Nykaa that Indian per capita beauty shopping is expected to rise sharply.

•Higher skincare and haircare expenses now indicate premiumization. Also, when it’s about skin and hair, people become loyal to brands compared to when using makeup.

•Large young population driving consumption: India has the largest Generation Z and millennial population globally. According to the UN Population Division estimates for 2019, approximately 375 million Indians are Generation Z (10-24 years of age) and approximately 333 million Indians are millennials (25-39 years of age), forming approximately 51% of the Indian population. Both groups are considered India’s biggest spenders, a trend likely to increase further as they enter their prime earning and spending years.

Competitive advantages

•Omni-Channel Strategy: Building a more resilient distribution network that will allow for potential hyperlocal delivery. Nykaa leverages its omni-channel database of consumers to select store locations, design brand and assortment mix, direct traffic to its stores, plan offline beauty events and marketing campaigns, and create an experiential-based, educational, and personalized shopping experience.

•Deep Brand (Supplier) Relationships: Nykaa engages with brands and provides them end-to-end services, Nykaa has helped premium brands develop miniature versions of their hero SKUs to drive product trials and acquire mass-market consumers, who over time would migrate to the full-size SKUs. This has enabled Nykaa to also get exclusive brands into India. Nykaa has been successful in giving the luxury brands a platform where their aspirational status could be maintained. Shipments to consumers for such products are also packed in premium packaging to enhance the luxury shopping experience for consumers.70% of business for luxury brands comes from online channel.

•Clear Thought Through Business Model: Showing that the company is not lethargic and even if new entrants come, it will keep climbing up the ladder and stay ahead of them. A few examples are: Premium brands are focused on maintaining their premium positioning and do not wish to be listed alongside mass brands on horizontal platforms. To counter this, Nykaa has created a special Luxe platform for high-end brands and to provide a better customer experience. Also, Nykaa launched the Nyka Man app, even though more than 50% of the product would overlap, but just to focus on customer experience (75% of the customers of Nykaa Man were not shopping in the main app).

•Inventory-Based Model: Nykaa has gained trust in an era where not-so-trusted sellers on Flipkart and Amazon were cheating by selling products like duplicate Maybelline kajal. Nykaa came in, took responsibility for inventory, and became an actual online D2C beauty platform. The inventory-based model ensures authenticity. The proliferation of counterfeit products is one of the challenges in the BPC market globally.

•Exclusive Brands and Private Label: Exclusive partnerships help increase customer loyalty and stickiness, while private label helps increase margins. Nykaa’s data related to customer preferences, choices, and price points helps it to acquire and launch brands and products that can immediately achieve product-market fit. These brands now account for 11.2/12.1% of GMV in BPC/fashion respectively.

•Not into a Discounting Game: Discounts on the platform are not Nykaa-funded and are usually brand-funded, resulting in better profitability for the company. Luxury brands usually do not like discounting given the desirability around these brands, thus creating a win-win situation for Nykaa and the brand. Contribution to GMV of BPC from existing buyers has increased from 66% in FY20 to 78% in FY23, indicating trust and loyalty factor and not discounting factor. The good part of Nykaa’s journey is that it was not built on the positioning of discounts or low prices. Amidst a crowded e-commerce market, it tried to differentiate itself by: (1) strong vertical focus, (2) positioning it as a platform of premium beauty brands, and (3) robust consumer engagement, including a network of (social media) influencers.

Risks

•Heightened competition might raise customer acquisition costs. Nykaa’s competitors include various online marketplaces, retailers with physical stores, and brands adopting a direct-to-consumer approach, which effectively bypasses third-party platforms like Nykaa in the distribution and sales process. In the Fashion business competition comes from well-established players such as Myntra. (Myntra infused Rs. 42bn over FY21-22 to further its growth story; Reliance Retail has invested Rs. 118.4bn towards tech stack building for all its online platform businesses and category building)

•Launch of Tira: There will be an initial consumer churn as some customers will try Tira as well. Whether the new venture, Tira, can retain all these customers will depend on the consumer experience it provides. A situation could arise where a player like Reliance with deep pockets starts offering EMI options on beauty purchases.

•There are too many moving parts to fully understand (marketing expense, brands giving discount, fashion business etc.) making valuation uncertain.

Financials and Valuations

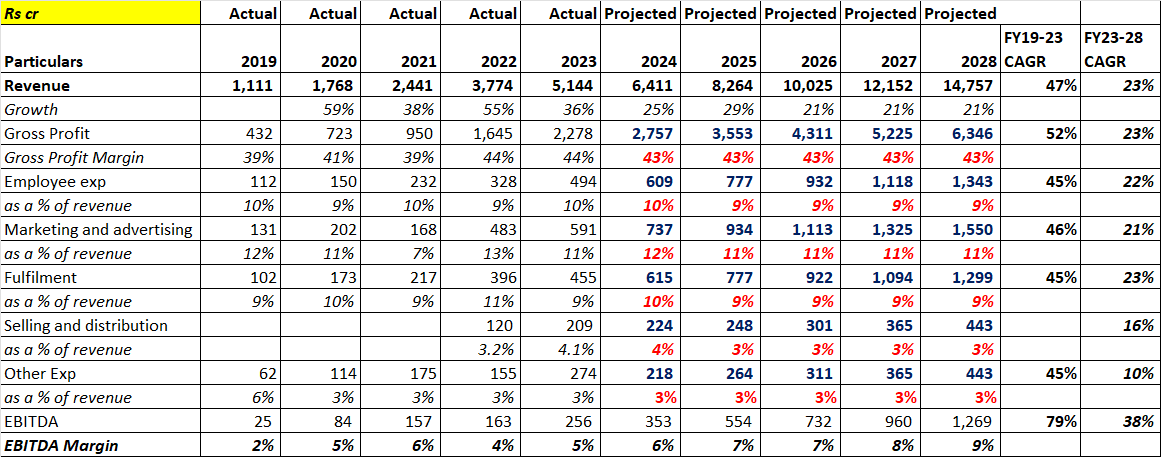

•In the past 4 years (2019-2023), Nykaa’s revenue has grown at a CAGR of 47% and EBITDA at a CAGR of 79%. According to a few assumptions that I have made (mentioned in the attached Excel), Nykaa’s revenue is expected to grow at a CAGR of 23% and EBITDA at 38% for the next five years.

•The current EV/EBITDA, based on 2024 earnings, is 125 and EV/Sales is 7. There is no similar business to Nykaa in the listed space. Businesses like HUL trade at a higher price-to-sales ratio (10.3), as their sales track record is proven, and they are cheaper in terms of EV/EBITDA (35.1), having already established their business profitability over the years. On the other hand, businesses like PB Fintech and Zomato trade at a higher EV/EBITDA (>250) compared to Nykaa. These businesses have not yet turned profitable. Markets like India have high growth, low penetration, increasing disposable income, and valuations here can’t be compared to valuations that a US-based company gets, because over there the markets have slower growth. In my opinion, Nykaa is an investible business once its dominance is proven over competitors with a few KPIs that need to be tracked regularly.

Conclusion

Nykaa has emerged as a prominent contender in India’s e-commerce industry. Through cultivating a robust online and offline presence, delivering personalized customer experiences, and offering a wide range of products, Nykaa has successfully set itself apart from competitors and established its leadership in the Indian beauty and wellness market. Beyond its business achievements, Nykaa’s triumph extends to its unwavering dedication to innovation, expanding business verticals in similar domains, and maintaining a focus on profitability.

The huge addressable and growing market in fashion and BPC segments will continue to drive revenue growth. Additionally, leveraging private labels will aid in expanding EBITDA margins. In my opinion, while marketing strategies can be replicated, discounts offered, and channels copied by competitors, certain aspects such as customer comfort with the platform, loyalty, and trust associated with Nykaa, particularly due to its non-focus on pricing alone, along with private label offerings and exclusive tie-ups, cannot be easily disrupted.

Moreover, Nykaa’s commitment to continuous growth through expanding into similar business segments adds further resilience to its competitive position.

6 Likes

what is the reason of tax rate 50 from 31 in q1 also in previous year q1 .

Two important business models I learnt recently from Nykaa :

- Creating demand through customer education where the intent to purchase a product in already visible:

Eg. Indian customers are increasingly focused on improving their lifestyles. For instance, when it comes to skincare routines, understanding which products to use based on skin type, how to use them, and when to use them is crucial. However, many people feel confused about product choices, leading to delays or neglect in using beauty products. Nykaa, a market leader in the organized beauty retail sector, has taken proactive steps to educate customers. They engage influencers, organize virtual and physical demo sessions, and implement other initiatives to guide customers effectively, eventually leading to higher sales.

- Should we educate the customer for free?

In Adam Grant’s book “Give and Take,” he highlights an intriguing concept: for eg. when a person or platform provides free education/goods/services, recipients often feel obligated. This psychological tendency increases the likelihood that they’ll return and make a purchase from the same platform/vendor/company which inturn results into higher revenue.

Notably, India remains an underpenetrated market for beauty product consumption. Currently, India’s per capita beauty product consumption stands at $15 annually, significantly lower than the $250 per person per annum in developed markets like UK and USA. However, with the increasing participation of women in the workforce, there is substantial potential for a significant surge in demand within this space.

2 Likes