Anchor Investors(who were allocated shares in IPO Anchor book) lock in ended last year…pre-IPO investors( investors who already were holding shares prior the IPO) will be able to sell after one year of listing which is Nov 10, 2022…

3 Likes

Thanks, is this rule for Pre IPO investors (including Promoters) for all IPOs or only PE backed IPOs? Nykaa, unlike few other new age companies which listed recently, is significantly Promoter owned…does that make any difference in how Anchor investor lock in and Pre IPO investor lockin is treated? Thanks

1 Like

For the benefit of my fellow investors:

Lock-In for Pre-Ipo shares used to be 1 year, in December 2021 SEBI decided to reduce the time period from 1 year to 6 months.

What are pre IPO shares?

PreIPO shares are those purchased by investors before the company going for an IPO.

Who are these Investors ?

They might be VC funds,HNIs ,Angel Investors, PreIPO AIF funds etc who might have stayed invested from quite some time.

Why will they sell?

Problem for PreIPO investors is liquidity, they might have invested long back at prices, fraction to what they are today.

When given a chance many might look to exit, even at IPO prices they might be sitting on massive Mark to market gains.

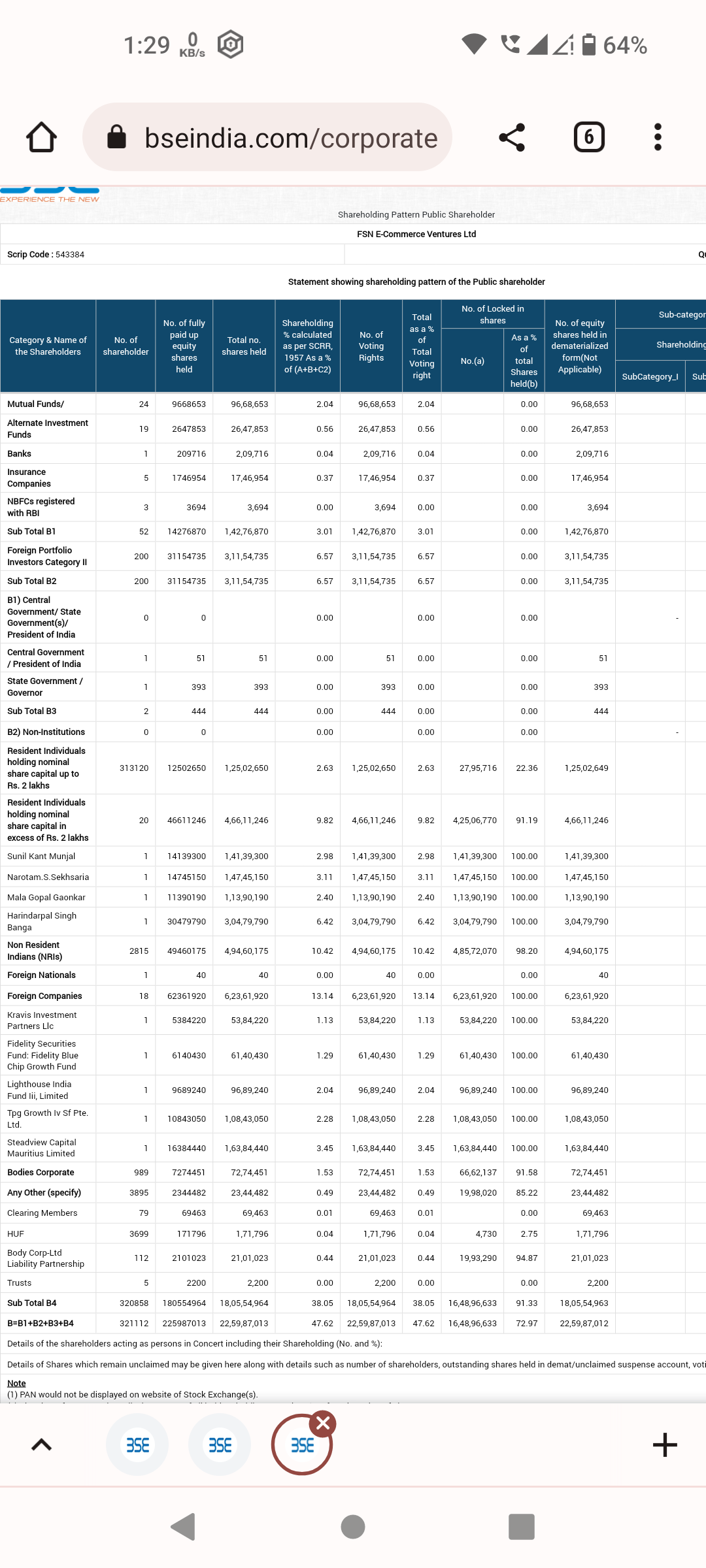

To understand the exact quantum in this case, check the shareholding pattern:

73% of the public shareholding is lockedin, i.e 16.5cr shares worth about 18kcr

6 Likes

Thanks Appreciate your inputs here!

For Pre IPO, is there any metric like 1 month before IPO is considered for lockin or even if some of these investors invested 10 years before IPO is also locked in as PreIPO?

Is this rule for all companies IPO or is linked to some kind of shareholding pattern priori to/post IPO like say Promoter/PE percentages etc.?

Thats huge no doubt but same should be case for every IPO like even for TCS or Dmart when they happened?

So, huge MTM gains must be present for huge magnitude of investors compared to mcap even for these firms but only the recent IPOs are falling…so gain is not reason for selling, its something else…maybe future potential of these companies compared to irrational IPO?

Is there no regulation to monitor this as this means the IPO done for retail public was at a price set for them to loose?

Disc: View only for academic purposes. I can be completely wrong in all my assessments.

All Pre IPO shares will stay locked in and the period of lock-in is different for different type of stakeholders, 6 months is the least.

Most of these new age tech companies are Angel Investors,venture backed… they have large base of LPs invested at various traches of funding & large number of early employees who built the company in lieu of ESOPS unlike companies like Dmart which is promoter funded.

It’s not an apple to apple comparison.

To understand the quantum of MTM gains for PreIPO shareholders one can look at DRHPs. This is reflected in the Capital structure section where issue prices and dilution metrics are disclosed. - will not be 100% accurate but close( since secondary txns are not reflected)

Issue pricing is always subjective, events like these usually create temporary voltaility… if the underlying intrinsic value holds for the stock, it should bounce back at some point or other.

Disclosure: No holdings.

8 Likes

Some article on nyka, Paytm, PB, delhivery, etc lock in period.

Deepak Shenoy of Capital Mind did a thread on the lockin period of Nykaa and others.

Thanks again for explaining so beautifully. Last thought that comes to mind for now regarding this is…Nykaa is also largely a Promoter owned company - before as well as after IPO…unlike many other New age companies…and also there are many traditional business which get listed with much much less Promoter stake as compared to Nykaa…but they do not witness the fall Nykaa is witnessing near lockin period…makes me think what should be root cause -

- IPO Pricing/Narrative and/or

- Lack of Profitability/doubt on business model and/or

- Promoter Ownership - kind of gets ruled out in case of Nykaa…infact its much better than many traditional businesses and/or

- Type of Investors involved - I think this may also have some weight on current situation as Angel/PE/Venture investors are more in New age businesses as compared to traditional. So type of investor is very important during lock in.

Elaborating point 4, I see that in case of Nykaa, unlike other new age firms, at least they do not have a single large PE…they seem to have healthy mix. Also, some well known individuals are also invested as top investors…Now is that a good thing or bad, I do not know…

views welcome!

Disc: Same as above

2 Likes

Combination of factors, I feel.

Rs 87,000-crore worth shares of new-age companies Nykaa, Policybazaar, Paytm and Delhivery due for lock-in expiry in November.

- Moneycontrol

This could be the leading cause.

Looking at the decimation, I am praying that nothing has gone wrong fundamentally. I am relieved to see the whole bunch of newly listed co fall.

Results are due soon.

General consumer sentiment is phenom. I am expecting a big growth in GMV.

In heart of heart, I am wishing this stock remains down and out for long, so that I can SIP enough.

4 Likes

CTO has resigned

Nykaa hits a new low today

— Sonia Shenoy (@_soniashenoy) October 28, 2022

stock down 6% now

-CTO sanjay suri resigns

-lock in period for pre ipo investors to expire on nov 10

-stock down 53% in 2022 so far

-stock now down 13% from IPO issue price of 1125rs

1 Like

In April 2018, nykaa was less than half a unicorn. But in Nov 2021 IPO it was valued at over 1 lakh crore. Even Ashneer Grover, the Shark Tank India evaluator and bharatpe co-founder, got his image screwed for nykaa but his money is safe now.

1 Like

Nykaa IPO valuation was Rs 53,204 Cr. It has fallen just 12.5% from IPO price.

Nykaa did 574Cr sales in 2018 and did 2441Cr sales in 2021. Business is still growing and profitability can change sentiments although the extent of fall due to selling can’t be predicted. So it’s better to wait for consolidation to occur before averaging down.

5 Likes

It is tough to predict price movements. Chart patterns simply show the current direction which can be changed by a fundamental news.

Folks find Nykaa expensive looking at PE. Let’s put that into perspective:

One year fwd Cmp/Sales is 9.5 (how? currently it’s 13.38 plugging in 40% growth is sales gives 9.5) this is lower than Hindustan Unilever’s

I don’t know if I should be comparing the two, cuz one is growing at 10% and other at 30-40%… But they do seem like cousins

1 Like

If the growth so far continues, what you say about valuations may be accepted, but I don’t think comparing Nykaa with HUL is correct, as HUL is present in many categories including food, which makes it a diversified business, not to mention the brands which are household names, the decades of its existence, the reasonable and relative secular growth it can have over the coming years, dividend, FCF, and other reasons.

Just saying, as I have no intention of investing as of now, but I am a little interested in the business.

1 Like

What is competition?

Same stuff being sold by many. Price wars. Over supply… Well, that won’t happen here.

Reason: Nykaa sells brands, not commodity. Brands hv pricing power, great margins.

Here, the race is about accessibility. And Nykaa has the first movers advantage. Once people get attached to brand, the relationship tends to stick. Everytime a person wants a BPC product she will assuredly touch Nykaa… that’s a given.

This tech enabled business is what I am counting on.

And like a friend suggested @deevee, once Nykaa is in our mobiles, homes, what all it can sell … Makeup, clothes, health, shoes… List is endless. But, these are all possibilities, and that is what we are doing here investing in possibilities. Investing in the future.

I am unsure about valuation, some say 60K Cr is expensive, and I feel a decade down the line 6L CR is possible. 10x in 10years is my game play here. Therefore, not commenting on the fall (or the upper circuit)

Glad to see a pivot formation at 1000, which is where I wish to add.

6 Likes

Things which are overvalued can remain overvalued for long long time, naayka can’t have exclusive partnership rightnow due to very low scale and zero presence in offline , valuation matrix will change once model is mixed with online/offline as margins will go down. Its a long long road lot of optimism built in price and these kind of situations result in disappointments in a high probabilistic scenario.

I am bullish on offline retail and that has paid hefty dividends, ABFRL, Shoppers stop and recently arvind fashion.

2 Likes

Sorry for curbing your enthusiasm and optimism, but having seen you from the days of not investing citing valuations or uncertainty, to the days of investing in Nykaa with high optimistic views, I want to say this.

What is a brand in the context of BPC? Is a brand a matter of feeling or does it also have a skin component attached it, do all brands suit all skins, all bodies? How long will it take Nykaa to sell only its own brands? What moat does it actually have, that no matter how big the new entrants are, how large the reach is for the existent players, that Nykaa’s moat is impenetrable like Apple?

Bata’s sales have grown 4% in the last 10 years, while Relaxo had a growth of 12%. I am sure Bata was perhaps one of the very few brands in the segment, if not the top brand back in the day. So I am not too sure even if a company with the backing of PE, builds brands which can capture the entire market, with no competitor in sight, more so when the market is fragmented with other popular brands and local brands in the segments, that you say Nykaa can enter - clothes, shoes etc.

Not that you don’t know about these, I am sure you do, but just saying.

Also, since you are bullish and wanted to know how to value Nykaa and now you are talking about brands, I would suggest you to study the growth of Apple, particularly since the time it has built a global name, may be after the first iPhone release, and has been growing the name ever since, which I think even Buffett acknowledged and bought a stake, and the only brand that comes to mind right away.

Not invested, and if I get convinced from any perspective, I will have a position.

6 Likes

Results

39% YoY Sales growth

200% YoY EPS growth

2 Likes

39% YoY growth is good.

They are doing something right.

The question that I have unanswered is, what might be their net margins. Are they spending a crazy amount to achieve such growth. Are they dishing freebies, like PayTM? They have good gross margins, but that is not enough information.

YoY 75% increase in employee expense and 33% increase in advertisements. That is forward looking expense, to fuel future growth.

Am not looking at EPS as long as it isnt negative, and the company isnt burning cash. That is where I draw the line for these new age stocks.

6 Likes

Indeed its good, Dmart also did 36% jump…lets wait for Trent. If I m not wrong Trent last Q jump was more than this…one aspect could be that Dmart & Trent have more offline presence & hence opening up would result in greater growth…a 5-10 year CAGR for these three will show good picture…Other listed retailers I am neither comparing nor concerned as they are not in same league as per me.

Disc: Invested in all 3 hence biased. Not eligible for any recommendations

3 Likes