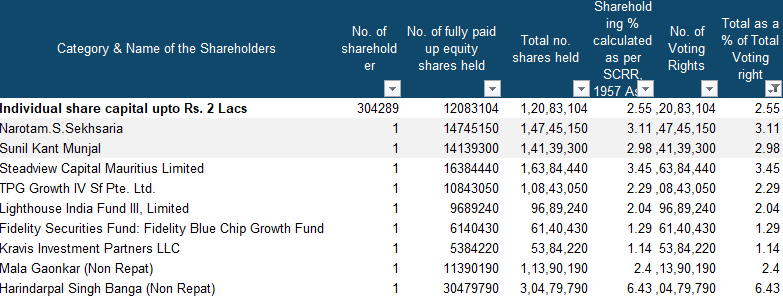

Seeing the current ownership under Non-Institutions, improving the liquidity seems a possible reason. Non-Institutions hold 38.1% of the overall shares. Out of that -

~66% with 9 entities/individuals

~7% with pure retail (Individual share capital up to Rs. 2 Lacs)

The expectation might be that the pure retail ownership would increase due to price reduction after the bonus.

Hi Surender, can you explain how you got the shareholding data in a structured way? Is there a platform which provides such information for every company?

@Surender Thanks for taking the effort and explaining.

IMO, it doesn’t seem to be a red flag as per your explanation. But I can see lots of folks talking (on Twitter) talking this as a negative step by the company.

One possible reason could be, anchor investor lock in period getting over (1 yr since listing), so to improve liquidity, and give them a smoother exit without having a lot of downward pressure on share price.

As I would see, since face value of stock is already Rs,1, there is no other way for promoters to reduce share price (to make it affordable for retail shareholders) than declaring large bonus issue. Also since its relatively new company, it hardly has any “retained earning/reserves” so company will be capitalizing “other equity” which is nothing but securities premium collected during IPO, by converting it into equity, thereby expanding the equity base and (reducing share price). This is my interpretation but I could be wrong.

This is unprecedented in my opinion. But whether it is good or bad, only time will tell.

Discl - I am invested. Position size is less than 1% of my PF.

It’s interesting to note that inspite of FED rate hikes, and miscellaneous badly potent global news, Nykaa hasn’t made fresh lows.

Possibly, because the ones wanting a fast exit already have exited, now there aren’t very many “fast fingers” onboard.

Now on, what the stock price does will depend squarely on GMV growth. And growth, post Covid is highly likely to be good. It has been good for most other consumer facing enterprises.

I have decided to keep adding every quarter, as I see it’s uptrend much like Dmart’s: consistently up, while looking expensive the whole time.

Every time I look at Nykaa and think of scaling up or for that matter at any other retailer (some new IPOs also coming up in Electronics etc.), I hold back and see the stupendous growth of Dmart & Trent and think of rather scaling them up instead…

Nyka is 62,000 cr company today and Trent - Westside, Zudio, Utsa & Star is a 50,000 cr company. Both in fashion, both with hyper growth and excellent management…I would choose bigger allocation to Trent here for a proven track record and better established business model. Would scale up Nykaa but at a much slower pace…I am neither getting it cheap nor is it a small company by any means - It is bigger than what Tata’s well performing decades old retail company…would only bet some part on it not because of the retail aspect but because of the DNA of a new age company…

In this disruptive world of business, maybe that DNA works for this company going ahead…

Disc: Invested in Trent, Dmart & Nykaa hence biased & critical. Not eligible for any recommendations. Post only for academic purposes.

Trent is a different story. We are invested in Dmart and Nykaa for their leadership position in the disruptive way they are positioned, which gives a strong sense that their growth will be sustained.

Trent is a different story. If an investor cannot identify a special thing, then he could asume that the business will face challenges on a regular basis, executional or financial challenges. This will hamper growth. A good management will work around it, but will be hampered nonetheless.

For ex.Trent is heavy on Assets. It’s Sales to Gross Block is around 1. Means, Trent’s growth is directly a function of the money they pour into the buildings and inventory.

And that is alright, I am not saying that it is not a good investment. Trent might be more profitable than Dmart for a retail investor. But, the real fun is in assessing the risk reward ratio.

The RR in these disruptors is good, once they get their footing. I mean no debt, no cash burning and leadership position. Nykaa and Dmart have these features. Therefore, I feel they won’t find any roadblocks for many years. And I want to see that in every quarterly report.

Nykaa is a little more special, because it is NOT ONLY disrupting and aggregating the established flow of revenues in BPC. But, also has tailwinds, in that, the demand, the TAM for BPC is increasing due to urbanization general increase in Per Capita income.

Some other investments I have made offer a good RR, but they are just a play on PE or demand reviving, like Muthoot.

Just curious to know how DMART and Nykaa are disruptors.

DMART manages inventory well which is best of its all competitors but that is not disruption.

What does Nykaa does very well? It sells things online at competitive prices. This is also not disruption as you can find those things at Nykaa’s competitiors.

Neither of these two companies are disruptors.

When Amazon bought whole foods almost every one thought it will become market leader and will displace already present competitors. Nothing such has happened.

Is any Indian company really a disruptor even when many are claiming?

Thank you

Disclosure: these are my only views and I can be wrong.

Similar points and my similar thoughts towards them…Trent is today where Nykaa would be sometime later in terms of physical presence and physical retail significance

No retailer can ignore physical channel

Trent on other hand has a beautiful gap to fill in terms of digital…the group knows it and already in action.

Rest all lies in DNA and execution and I trust both, so far…

Disc. Same as above. Invested & biased. Not eligible for any advice

At Price to Sales of 15x and EV/EBITDA of 293, no matter the growth and management quality (both look good) it should take some time to make money in this stock. Trent is equally expensive (given the current business size and business dynamics) and we shouldn’t look for high returns there either.

In both cases, the risk seems higher than the reward and Nykaa is even riskier given that business model is still evolving and the market cap is already that of an established giant.

Disclosure- Tracking position in Nykaa for learning perspective, no position in Trent.

1800 PE is misleading. Was too for Idfcfirst, the darling of retailers.

Nykaa isn’t focussing on profits, but on capturing market share. It’s re-investing the proceeds in future growth. And aggressively so. But, only enough to not burn cash, particularly after getting listed.

I have done the calculation/estimation. If done correctly, Nykaa at 30% growth is cheaper than HuL one year forward, which has 9% growth.

A company trading with 4000 cr topline and market cap of 62000 cr, P/B is 49, OPM 4% dont know how valuations are justified. Reliance retail is planning agressive for offline stores, Naayka business model will fail once offline business is scaled up, may remain at this price for long long time or will go down. Shoppers stop, Arvind , AB Fashion, even go fashion is better than this.

@jamit05 I agree with you on this. Nykaa is a growth company and it is using its profitability to fuel its growth. A 40-50% growth on topline and a similar margin will justify the stock price as long as this is met.

Once the top line reaches a higher level, operating leverage will kick in and margins should expand. This (winning market share) is the only way Nykaa can survive. Once the company reaches a significant market share, it’s a no-brainer that it will reduce its spending.

Just to give you context Zscaler (NSE: ZS) a company in the cyber security domain works in a similar way. The company is a leader in cloud security but uses the excess cash to capture the market share.

Nykaa enters into a strategic partnership with Apparel Group to setup an omni-channel, multi branded beauty retail operation business in the countries that are part of the Gulf Cooperation Council (GCC) namely the Kingdom of Bahrain, State of Kuwait, Sultanate of Oman, State of Qatar, Kingdom of Saudi Arabia and the United Arab Emirates (UAE) through an entity to be incorporated in the Abu Dhabi Global Market in which FSN International will hold 55% stake and balance 45% will be held by Apparel as on the Closing Date, in accordance with the terms of the Agreement.

This is the first pivot for the company to work towards a global retail brand in the Beauty and Personal care market

Waiting for the quarterly earnings. Since the drop in price is nice, I will add more qty only if the numbers are good. Provided, I don’t detect any major negative structural change.

My expectation is to see atleast a 5% growth in GMV and revenues. And minimal cash burning.

There have been mixed news/opinions I have come across regarding lock in period for Nykaa IPO shares. Some say that lockin for Anchor investors are about to end in Nov 22 while others mention its already ended because Nykaa is heavily promoter owned.

Anyone having clear understanding of whether lockin for Anchor investors have ended already or about to end in Nov?