Also, if you go further ahead in slides, you can see Capital Markets business has PBT of 231 Cr out of 348 Cr of total PBT which means 66% of total PBT is highly cyclical. Add to this there are 20-30% cyclical elements in Nuvama Wealth, Nuvama Private and asset management business as well which are growing good in these good times and can moderate or de grow in bad times, so 70%+ PBT would be cyclical for Nuvama. This explains the constrained earnings multiple despite overall scorching growth.

On similar point raised by one analyst, management did say that they are doing upfront investments in wealth and asset businesses on RM side specifically and there is lag between revenue and investments in these businesses. The RM productivity can increase significantly in 2-3 years which would bring the cost to income down and blended cost to income target is 60% in 2-3 years. This would help offset some of the cyclicality in the business.

Todays volume makes up close to 18% of the total shares count, however, media news confirms Edelweiss cleaning out sale of 8.5 stake, which was expected, so where is the other 10% sale coming from, any info? considering most of the holding is with institutions , it will be good to know.

Edelweiss Financial Services through its two affiliates – Ecap Equities Ltd and Edel Finance Company Ltd – offloaded a total of 25.50 lakh shares or 7.14 per cent stake, collectively, in Mumbai-based Nuvama Wealth Management, as per the bulk deal data on the NSE.

The shares were sold in the price range of Rs 6,854.15-6,941.30 apiece, taking the combined value to Rs 1,759.44 crore.

Meanwhile, Kotak Mutual Fund acquired 2.71 lakh shares, amounting to a 0.8 per cent stake in Nuvama Wealth Management. The shares were picked up at an average price of Rs 6,851 per piece.

This took the deal value to Rs 185.78 crore.

Entry price is subjective…my understanding from the above video is…currently nuvama has 23% Annuity product and 51% is related to Capital Markets. So, I’m guessing a reduced growth rates in the upcoming Two to three Quarters. Reasons being

The base has changed, earlier this year the base revenue was small Hence we observed more than 100 % growth, but may be not now.

After recent F&O changes, the value of Options trading from 5-6 Trillion has come down to 2-2.5 Trillion, So this might has an impact, but not as much as brokers like Angel One, 5 Paisa and IIFL securities etc…

Even though, Market has not corrected much, it’s in sideways since last two months, So the growth in AUM is key monitorable item.

With this background I’m waiting for next two Quarters results to understand the impact of Capital Markets on Nuvama to start a new entry.

Disc: Had a small position.

two key factors which is still yet to kick in for PAT can be Foreign clients who want to invest in India, More and more FII clients addition along with NRI’s and Alternate asset management profits in coming quarters which is still at very small base for Nuvama, more and more white money is added to economy due to digital India should help in real estate sector thru alternate investments.

Also income tax reduction as recently speculated in recent headlines for next budget should compensate any capital tax hikes.

Motilal Oswal’s detailed report on Financials – Thematic: Indian Capital Market – A golden era!. As per Motilal Oswal Nuvama has 25% upside. Let’s see the results next week on 3rd Jan 25.

After doing a basic common sense check, seems the financial pandits are right on wealth and asset management business overall.

Below are the assets under management by worlds largest asset managers. Only BackRock manages $10 Trillion, which is 3 times Indian GDP. By the way link to Blackrock’s India Fund is here.

Considering the above numbers, India being a very under penetrated market, wealth management being a sunrise industry, seems Nuvama along with other wealth managers have a good runway ahead.

"SEBI clarified that while Motilal Oswal and Nuvama Wealth Management facilitated Big Client trades, no evidence of wrongdoing was found against them. The SCN stated: “The trades of the Big Client undertaken through Nuvama and Motilal matched with trades of FRs. However, no evidence implicating these trading members in the alleged fraud has been discovered.”

as compared to peers, i think nuvama results are far better. despite having higher exposure to the capital market, QoQ decline in revenue and PAT is very less. margin expansion is going on. future quarters may be challengin for them but improvement in margin can lead to compensate declines in numbers.

valuation is more lucrative as dividend yield is 2.67%

dis. invested

Hi. Generally want to understand cycle duration for capital market companies.

how long does a bear market last before bull run again. and do they do even better, like higher revenues than previous bull run.

asking because i really like the 80 and 60rs dividend nuvama paid me last 2 quarters : ) so was wondering if i should buy more shares. very new to investing so would really appreciate some insights.

What will be the stable/long-term opm% for nuvama wealth. Current margins are 50%+ and it might not sustain for long, given the inherent cyclicality of model

Disc: Invested

Dubai operations: Currently operating with three Relationship Managers (RMs), generating revenue but not yet profitable. Aiming to break even in 6-9 months and double RM count in 12 months.

Singapore operations: Still in planning stages, facing a highly competitive market.

Lending business recalibration:

Borrowed 800 crore, which was repaid but likely resulted in a 20-30 crore increase in interest costs compared to Q2.

Relationship Manager (RM) growth and productivity

Total RMs: 1237, with 359 added in the last 12 months and 35 in Q3.

New RMs take about a year to break even, with significant contribution starting after 3 years.

Less than 40% of RMs have less than 1 year of experience, barely contributing (1X

revenue).

RM productivity increases from 1X to 4X to 6X as they move from 1 year to 3 years to 5 years of experience.

Relationship Managers (RMs) at Nuvama earn through a combination of fixed and variable income. The variable component is tied to the platform’s offerings, with Nuvama’s full-service platform providing multiple avenues for RMs to generate revenue. This structure incentivizes RMs to leverage the diverse services available to clients.Attrition among RMs is primarily observed in non-performing categories. High-performing RMs tend to stay with the company due to the time required to build revenue streams on a new platform

Asset Management division:

Not yet profitable, expected to break even in 8-12 months when reaching around 20,000 crore in assets under management (AUM).

Lending business characteristics:

Size around 5,000 crore, offering products like Loans against Securities and ESOP funding.

Lower Return on Equity (ROE) of about 20% due to lack of leverage.

Asset Management,

Nuvama’s division is expected to break even in 8-12 months when it reaches an AUM of around 20,000 crore

Lending business:

Size: Approximately 5,000 crore

Products: Loans against Securities and ESOP funding

MTM (Mark-to-Market): Around 50%

ROE: 20%, lower due to lack of leverage

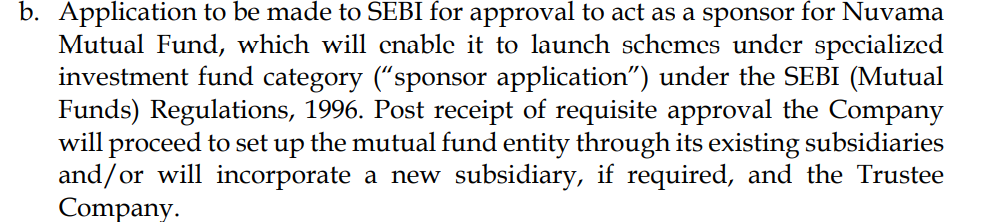

Nuvama has applied for mutual funds, focusing on special funds with a minimum ticket size of 10 lakh, which will enable them to work on long-short type funds.

The “One Nuvama” strategy aims to create synergies across services. Clients can enter through one service and become clients of others. For example, a client using asset services or pre-IPO services may later become a private wealth clien.

AUM growth is projected at around 25%, assuming steady market conditions.

360 One WAM (formerly IIFL Wealth Management) is the big daddy in the field. Bigger and, as per a friend who has availed their services, very high calibre in terms of the wealth management professionals they have got.