Thanks for the detailed answers. Appreciate it !

I understand the +ves with this co., their guided growth, operating leverage benefits and all.

However, the key is to understand risks that lurk ahead if one chooses to invest at the current price.

I am still wondering:

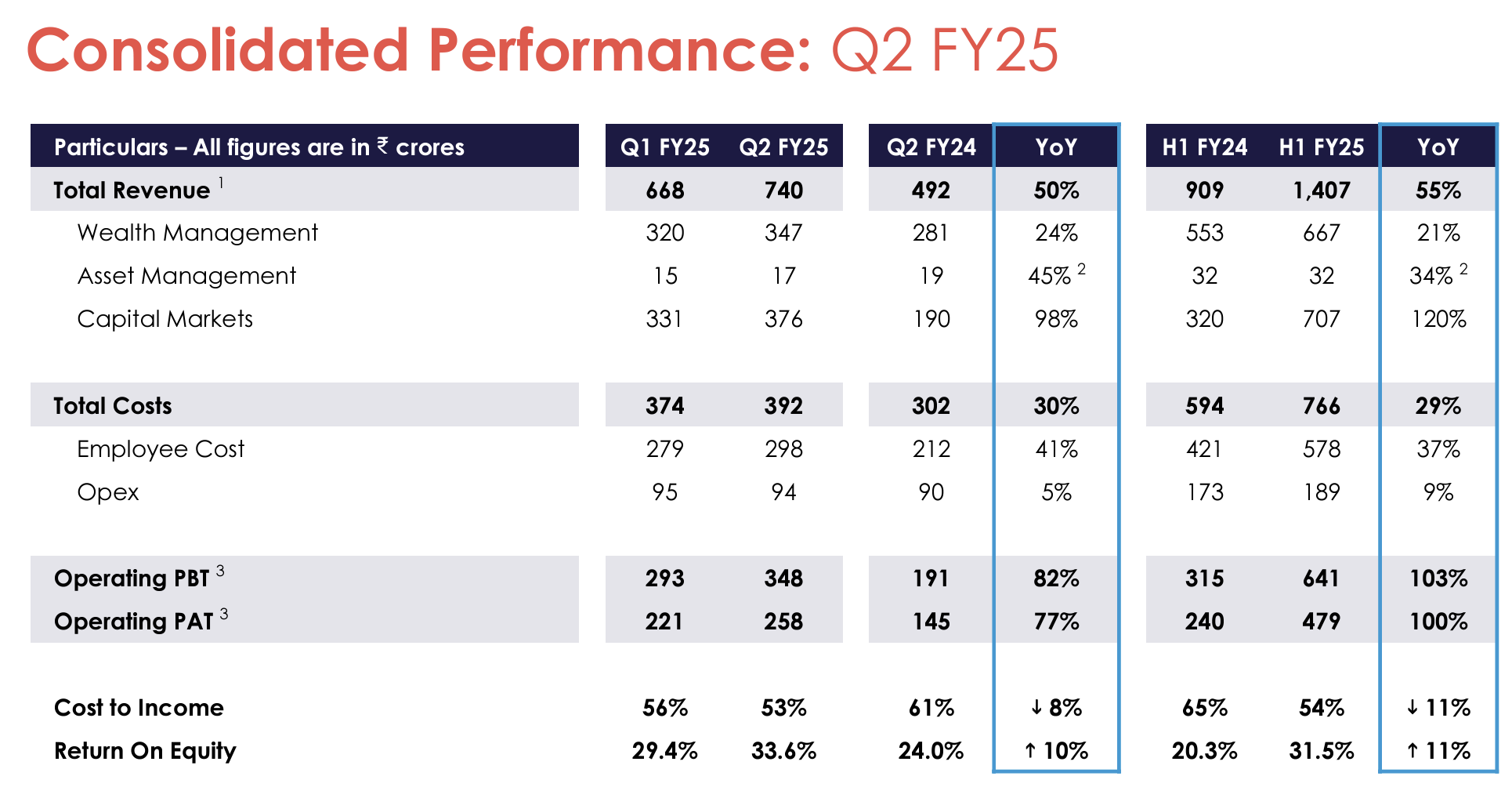

Even if you give out loan against shares to clients, you are earning a +ve net income NIM on the same. That should get reflected in cash flow from operations sooner or later. CFO = “Cash collected from customers” - “Cash paid to suppliers”

Look at it that way (rather than working from Net income & making adjustments)

And the “WC items” you mention, it cannot keep on ballooning every year in a way that you have -ve CFOs every year for the last 5 years while +ve on EBITDA and PAT.

Paying out Dividends are essential if you are engaged in a business that throws out a lot of cash. It is to ensure that Shareholders trust your numbers.

I mentioned Anand Rathi because they have grown at 25%+ cagr and have the same future guidance also, while also maintaining a great dividend payout.

(360 WAM is much difficult to project & analyze because they house a lot of things inside: AIFs, Funds & what not. So i dont look at that)

Becoming a 1 stop solution (aka full service provider) is a good thing. But, does’nt offer much benefit in the sense you think that a particular customer will get everything done by Nuvama only. Because the HNI customer will pick the most price efficient vendor for the service he desires. This is financial services after all. (The same thing happens in IT services where the customer follows a multi-vendor strategy. Nobody likes to depend for everything on just 1)

*The major concern for me is: Are their P&L numbers genuine or inflated?

If the mgmt. can answer why the CFOs are consistently hugely negative & when can we expect to see +ve numbers there, that will help.

Agreed, I think the cash flow statement in the annual report that will be published now will be of better help to get to know the specifics. Also, loaning out is a part of core operations so it gets added back to the cash flow from the PnL statement itself. Agreed that the CFO can’t be negative consistently. But I would like you to compare this with 360 instead of Anand Rathi as there not exactly peers to peers.

But I will delve deeper into this to get to know the specifics of the whole cash flow!

When I said growth over dividends, that was just my personal opinion Nuvama will/should come with a dividend policy by Q1 fy25. If not, it should be brought but since they have mentioned it I think it’s fair to wait and see.

So the thing is, HNIs and UHNIs are very sticky. I have been studying deeper and the persistence ratio for UHNIs is high 90s and for HNIs is low 90s. and that’s really good. Which makes me believe the services aren’t as price elastic as we might assume. Moreover, they are more likely to pick their asset manager because of their assets easily being used as collateral. You dont lose out on customers very easily here.

To add to above, if i remember correctly in one of the concall they did mention that client retention is 99% or above and the ones lost is also generally those who wind up their operations in India and permanently move abroad.

Nuvama’s MD and CEO Mr. Ashish Kehair did an interview where he discussed Nuvama and the industry

Here are my notes on the same:

Industry

GDP growth leading to increase in equity and real estate value is leading to prosperity and this prosperity is not just in the top tier cities.

Adding financilisation to this, he believes it is a structural trend which is just beginning.

Banks have led the way worldwide in wealth management but India still has a lot of credit needs which leaves this white space for asset management/ wealth management companies like Nuvama.

How long can this structural trend persist? the geographical reach is increasing and it will keep increasing as GDP per capita increases. Moreover, size of assets/ wealth is focused on top 2 tiers. When GDP per capita reaches 10,000 then the bottom of the pyramid too become attractive. so it will increase in terms of location and also bottom pyramid

Promising areas: Jaipur, Udaipur, Coimbatore, Varanasi etc. HNIs can be found here

huge demand supply gap.

Business

focus is on wealth management while the rest accompany them

If equities grow by 15%, these guys can grow at 20% due to inflows and some investments in debt.

Wealth management have the highest degree of separation from capital markets in this proxy to capital markets businesses.

Growth strategy: You need to launch a few products to fill a few gaps. This is not the biggest priority but what matters is sourcing the right manufacturing. Moreover, you need RMs to grow but they become more productive as assets of these HNIs keep growing by compounding. so same client and same RM but higher AUM.

RM: 120-125 in Nuvama private. 1200 in Nuvama in wealth. Add 20-25% every year and a little more on wealth side. Possible of imagining 12,000 RMs as India is 20 years behind India and these are the numbers they operate

the only variable cost is producer cost, while most is fixed or semi fixed in nature.

Aims to reach 59-60% Cost to income ratio in 2-3 years.

Aiming to set up an office in Dubai. One big advantage is channelizing NRI funds as Indian assets get attractive and near the 5 trillion dollar mark. When a country crosses 5 trillion dollars, India will become a mainstream. Another advantage of setting up office in Dubai is that UHNIs can have a leg outside of India as well. This won’t be a large meaningful contributor for a few years because its just one office.

Growth levers: geographical expansion, increasing RM, increasing products. they have a well built product platform and they wil keep adding. Asset management will also contribute in the future which is loss making currently. They have an AMC as well. Profitability growth will come from operating leverage.

one of the most value adding as it enables financial independence

Lock in will end on September so we can expect supply coming in.

20% AUM growth is visible seeing the state of country

As your ratio of New to OLD RM comes down, degree of operating leverage keeps increasing as experiences RMs increase productivity.

During the year, they launched a

commercial real estate fund through

the 50:50 Joint venture entity with

Cushman and Wakefield as partner… Do you have any Idea how exactly this type of deal

works??

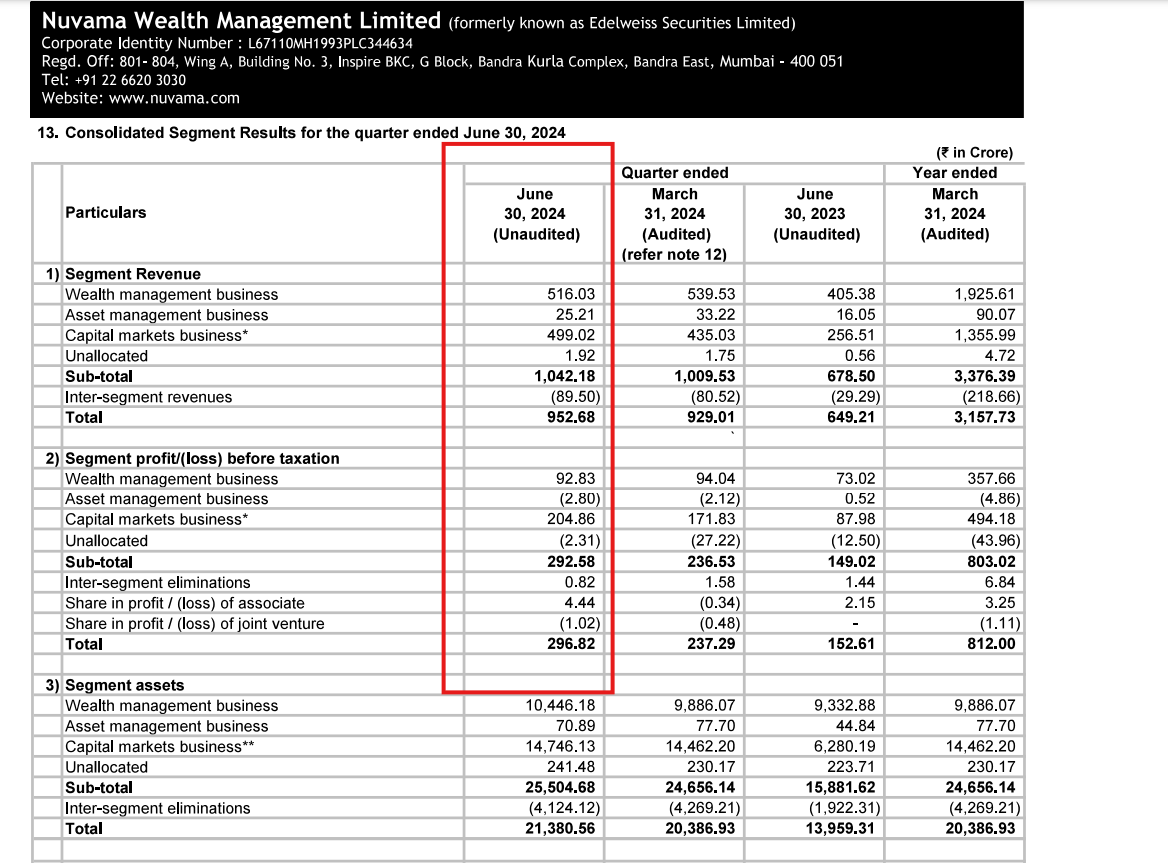

With this spike in capital markets contribution in recent quarters its getting difficult to have a peer to peer comparison on valuation with the likes of 360 ONE, Anand Rathi etc. The question is whether there is a possibility of derating?

Its fair question, management claims their equity market revenue is more of a synergetic subset of complimenting service to the same set of clients in wealth management. Also, its worth listening to this interview especially from 6.30 min. Worth listening to their earnings calls as well. The management sounds very rounded.

Wealth Management profit and revenue did not grow this quarter, mostly likely its due to addition of new 67 RM’s and investment’s in Dubai office, while AUM has grown 10% + QOQ., family offices have grown from 3600 to 3850. which is good enough sign of scaling.

I know revenue to AUM should not be looked at in a linearity. But in about 2 years where AUM grew 30-40% CAGR, where is the incremental ARR?

On a positive note, I hope the WM revenue can jump exponentially in the coming quarters, looking at how revenue recognition has been falling behind the exceptional AUM growth.

If am not wrong and I am not sure how exactly revenue recognition works against AUM, but there was a change in accounting standards recently, I think they had made some comments regarding this in earlier con calls.

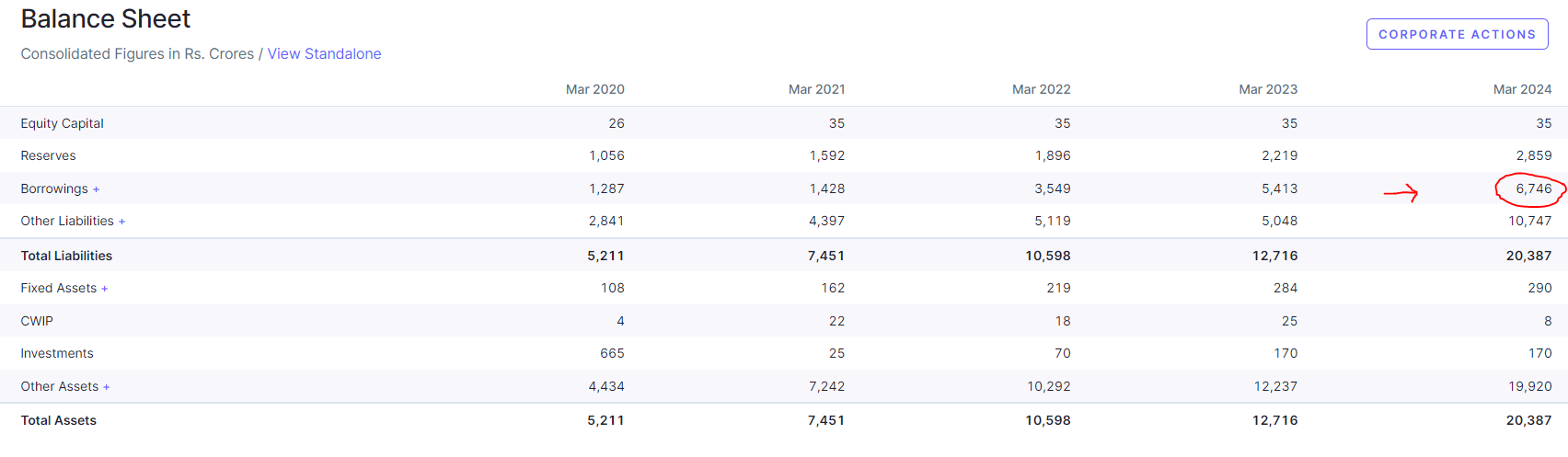

Hi Guys, I am studying this company. I got stuck at borrowing parameter. Can anyone help me to understand, having such big borrowing 6,746 is it concerning? Or I am missing something ?

This is not borrowing in the traditional sense where a company would borrow to buy PP&E and put up a plant.

The debt you are referring to is essentially financing the margin trading/loan against securities business of the Cap Markets/WM business which you can see appears on the asset side of the balance sheet.

Most of the debt is market-linked - so you are essentially earning a spread by lending out at slightly higher than you are borrowing. And it is collateralized.

It is a source of income, but not the primary business - it serves to complement the core Cap Markets/WM business.