About the company

Nuvama Wealth Management is a recently listed business which was emerged from Edelweiss group of India. Currently, the promoter is PAG, which is an asian investment company with more than 55 billion dollars AUM.

3 business segments

- Wealth Management: Company operates as Nuvama Private and Nuvama Wealth. Nuvama Private serves Ultra High Networth Clients and is among top 2 pvt. players.Nuvama Wealth serves affluent HNIs.

- Asset Management

- Capital Market Services

Nuvama Wealth Management has clients asset worth 247,000 crores as of 31st March 2024

Cap

Asset Management have an AUM of about 7000 crores

Capital market which mainly constitutes of Client assets for cleaning and custody are at around 91,000 crores.

This was a very small brief on the business

Here is my thesis on the business and below that are the notes on all the Concalls. It will provide a good understanding of the business and what interests me here

4 Likes

Disc: Invested and biased

First

why is it a proxy to Affluent India?

India is witnessing multiple opportunities which are empowering the country. One of the key opportunity which was highlighted by Goldman Sachs as well is the rise of Affluent of India.

the income or the number of individuals with a set amount of income is rising which allows them to look beyond daily needs. It allows them to spend on wants and invest for a better future.

Nuvama is rightly placed because the key market it caters to is HNI and UHNI. Moreover, its increasing emphasis on Asset Management makes it the right fit to play the bet on rising income levels.

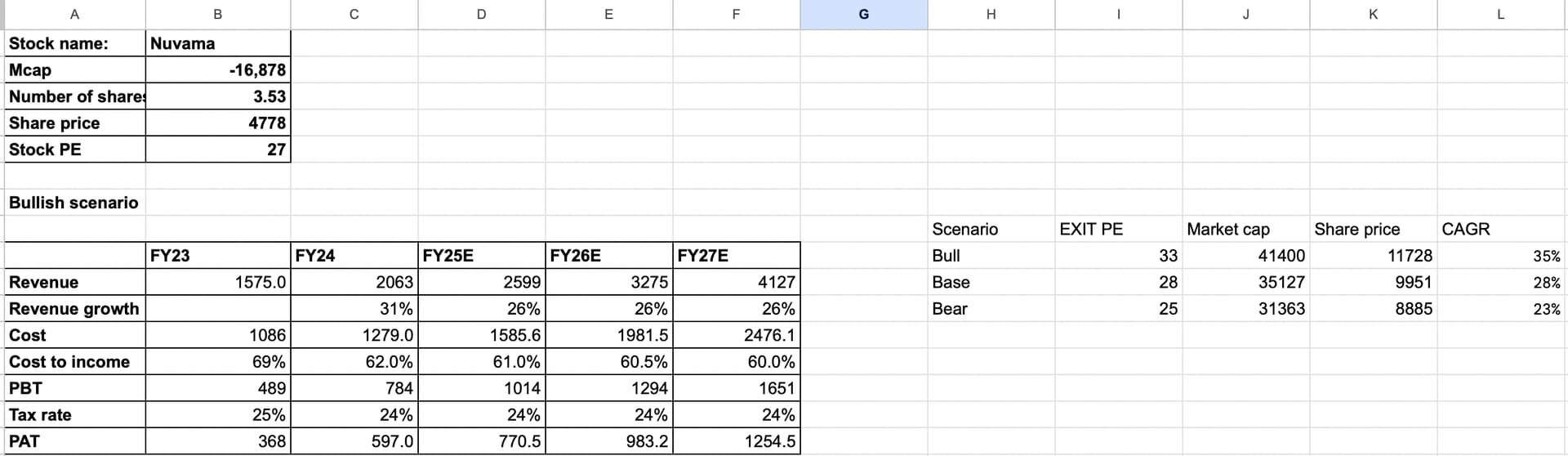

Thesis

The financial model works a bit differently here. High emphasis is placed on Cost to income by the management and the statements issued by them show the same. and it makes it very simple to understand the key aspects of the business and also highlight the operating leverage at play.

Sales growth

Firstly, Increasing RM or relationship manager is basically the capacity expansion of a wealth management company. Currently, they are at around 1200 RMs and aim to make it 2000 in the next three years. This means a CAGR of 18.5% . Additionally, the revenue growth should outpace the growth in RMs as productivity increases. The second segment, Capital market too is expected to grow at around 2-2.25x in 3-5 years. A big driver of growth will be the asset management as the goal is to make the current AUM of 7000 7-8x in the next 5 years. Operating leverage will kick in as well. Hence, I feel like the growth assumed is moderate to conservative as there are a lot of levers of growth.

Cost to income

Nuvama is aiming to become a tech platform and one a stop solution. the Opex cost of the business will not be much in the coming years as the cost is already done before. The only cost that will rise steadily is staff costs as RMs are hired. Thus, Operating leverage will kick in as the variable costs are employee costs and their benefits.

The management has guided for Cost to income of 60% over the next three years, however it could be lumpy because that depends on the pace of hiring so keep that in mind.

Tax rate assumed is 24-25% as indicated in the past 2 FYs.

Anti thesis pointers

- Although I believe the story is structural, some of its elements of business are cyclical in nature and hence can lead to problems in revenue growth. For example, Capital markets which includes IB is highly cyclical and should be looked at with caution.

- a big part of their capital market revenue is Custody and clearing business: it. is dependent on the volumes of contracts traded by big hedge funds and such companies. Volumes increase during a bull market so during a bear market, revenue and volume will go down.

- Nuvama Private caters to ULTRA HNIs who benefit a lot from IPOs and Real estate. Again, these are cyclical in nature

One thing to understand in operating leverage is if revenues do not grow, operating deleverage can. take place which is a possibility here so the PAT can fall drastically.

However, The management aims to keep a 75-80% of earning from Asset Management and Wealth Management which I believe are structural stories with elements of shallow cyclicality. If they succeed in doing this: rerating is possible and the worry of being cyclical goes away.

16 Likes

The stock seems to be in a stage 2 with support from 50 ema.

2 Likes

what will be impact on its price if any regulation regarding F&O comes?

Not much. The reason I find it a structural trend is because its key focus is in wealth and asset management. Both will not be affected by F&O in any way.

However, in capital market it deals with funds and houses that trade in F&O

So any regulation against F&O should hamper this area of revenue! But I expect the problem to be minimal and even less as the other areas grow!

4 Likes

why is the debt in Nuvama so much ? and do you expect the possiblity of Demerger of buisness in the future ?

It seems entering in stage 3, right?

@Mudit.Kushalvardhan I’m not a technical analyst, but as per the stage analysis knowledge that I have it does look like stage 3. I can be completely wrong as well.

Did Nuvama release a Draft Red Herring Prospectus (DRHP)? If so, where is it made available?

1 Like

@Mudit.Kushalvardhan @fuzzhead It’s at 50EMA right now. On what bases does it look stage 3 to you? Calling it a stage 3 is way too premature. It’s at stage 2 acc to me.

2 Likes

Agree that it has not entered into fullfledged stage 3 and also not breached 30 week EMA…But its down by almost 15% from its recent peak and also from April start till now , almost 2 months it has been flat and going down. It has breached 10 week EMA from last 2 weeks and slope of 10 week EMA and 20 week EMA has been flat. Its not an ideal condition to enter into. But those who have already invested from lower levels, they have to watch for next 2-3 weeks to see if it consolidates or moves higher…

2 Likes

I dont think it’s in stage 3. It looks like stage 2 is still intact with a routine correction.

check out the weekly and daily charts. The trend line I have drawn are intact and haven’t been broken yet

Moreover, the fundamentals and the guidance look bullish and I dont think there is much to worry about.

A concern could be that margins might suppressed due to faster increase of staff costs in the coming quarter.I personally think that should lead to some consolidation at best but lets see its just a guess.

Technical analysis fails when we try to be precise. If my trend line is at 100 and it goes to 99 that does not mean it’s a bearish trend now. It is best when used to understand the general trend of the theme or stock and atm Nuvama seems to be in the same trend.

7 Likes

looking at a 15% correction in an absolute term is unfair. Barring the EMA discussion because I do not use them, a 15% correction in business like Nuvama is fine because how rapid the price fluctuates. If a reliance were to fall 15%, I would be worried but not a business that has nearly tripled in the past year.

4 Likes

if I am not mistaken, borrowing isn’t exactly a loan. Nuvama allows such stuff for their clients and gives them funds or parks funds. Its a very small area of business and is only done to fill the gap

On the demerger thing, I think that’s very speculative and we cant predict it.

4 Likes

what do you think about JIO-Blackrock entering wealth Management segment… how much time it may take for them to be on par with Nuvama ??

A MOAT that Nuvama has/ is developing is that it’s a one stop shop for its clients. it’s doing everything they want.

Let me give an example,

I want to go public, I will contact Nuvama for their IB team to get listed

After getting some money post IPO, I have liquid funds available.

I am more likely to contact Nuvama for their wealth management because I already have a relationship with them.

Its a circle, they have been and are filling gaps of this whole process.

However, Reliance has a lot of cash and can disrupt any field. All we can do is wait and watch. However, I am of the belief that this industry will have multiple winners and will not be a winner takes all.

Only time will telll.

12 Likes

yes, they have said the flywheel effect will start as scaling will happen… like you said and may be like in US there may be many winners.

3 Likes

Hey! Great questions let me try answering them

-

One major component is Loan advances. around 1300 crores is in loan advances. Remove that and it’s already positive. Secondly, If I am not wrong, You need to park cash as requirements in different segments of business. This goes under wc items. I would say compare this with 360 ONE WAM as these are the most similar. Also in the earning calls, you can notice analysts and promoters discussing dividend policy because they generate a lot of cash. Its not a point of worry(according to me)

-

Dividend policy is set to come by next quarter. they have mentioned that in their earnings call. However, the thing is Nuvama is investing and guiding for the Highest growth of all. they are aiming to double RMs in 3-5 years and AMC 5x in 4-5 years( low base so easy to do this but good growth rates) So honestly I would rather prefer cashing going into these growth engines rather than dividends.Personal opinion though so it won’t change anything and dividend policy will be announced soon.

-

NIMs is 5-5.2% in general but was 4.7% in Q4. Most of the loans are to existing clients and it is given on the collateral of the assets that their clients have under AUM of Nuvama so its 100% protected.

They haven’t commented on the gearing ratio, however 360 ONE said they are fine till 4x. That could give a potential idea

-

Two answers to this. First, Nuvama aims to be a one stop solution so a client need not go anywhere. A promoters lists it business via Nuvama’s IB and then gives the proceeds as an HNI or UHNI for wealth management. When cash is needed, they use these assets against collateral and get that. Holistically, it’s a good model. even they mentioned they dont chase growth or anything but its an added service as a full circle kind of a thing

However, AMC and wealth management are the high ROE ones and the least cyclical of all. so they are aiming to focus on that and if you observe their share of profit has continuously increased and will continue doing so! their growth rates far exceed other segments

hope this helps, if you have doubts or if I got something wrong, let me know and I will try delving deeper.

Moreover, I am working on an article covering the wealth management space so I will cover these ideas in detail.

I will share the article here later for business analysis

15 Likes

Loan against Securities is completely protected against collateral. This is the only firm with complete solution for a full cycle. That is the reason perhaps their family offices clients are growing at higher rate.

2 Likes