Attached monthly bar chart of NTPC shows a possible change in trend from downtrend to uptrend.

All comments put up on the chart.

disc: bought as a technical bet.

Attached monthly bar chart of NTPC shows a possible change in trend from downtrend to uptrend.

All comments put up on the chart.

disc: bought as a technical bet.

Hitesh Bhai,

Just seen the post. Assuming the odds are favourable as per the technical formation and someone wants to buy min 2000 shares. In that case which of the three options are best and why?

Buy 2000 shares with SL as given by you.

Buy 1 lot future October with SL placed at same point.

Buy call option for October or November. Or write Put Option. (Complicated and avoidable for lay investor, in my opinion).

I feel, option 2 is better for persons who have strong conviction on chart formation. If not, then why not?

If yes, then is it advisable to double the bet? And reduce SL by half?

For buying 1 lot you need to pay margin of about Rs. 37K max and keep another Rs. 20 K for SL margin? Whereas buying 2000 NTPC would cost about Rs. 2.86 L based on today’s price.

Just curious to get a detailed response…

Thanks

Aveek,

I dont go into all these complicated calculations.

If I am confident about buying a particular stock I go ahead and buy the amount I wish to allocate for my portfolio. And my buying is in delivery.

Each individual has his own method of doing things so to each his own.

Rep by Kulamani Biswal, Director Finance, N.N.Misra, Director (Operations) and S C Pandey, Director Projects. Key takeaways of con call by Capital mkt;

Adjusted PAT for the quarter ended Sep 2014 declined by 22% to Rs 1805 crore compared to Rs 2304 crore in the corresponding previous period.Regulated equity as end of Sep 2014 stood at Rs 35207.6 crore.

The company has issued NIT for acquisition of strategic stake in coal mines overseas as it feels this is the right time. Sharp fall in bottom-line for the quarter is largely on account of lower incentives as it is now linked to PLF and reduction in marginal contribution.The thermal coal plant PLF for Q2FY15was lower 2.69% points largely an account of scheduled plant maintenance.

The company is well on course to import of 21 million tonne of coal in 2014-15. It has imported coal to the tune of 8.17 MT in H1FY15 compared to 7.5 MT in the corresponding previous period. Further it has already contracted coal imports for about 7 MT and another 5MT is under evaluation. Moreover NIT has been issued for another 5 MT. Since the domestic supply was higher in H1FY15 the imports were pushed back.Under recovery of fixed cost in H1FY15 is lower than that of corresponding previous period. The company will end current fiscal with zero under recovery.

Barh stage II â Not declared commercial yet and it is between synchronization and commercial declaration. The commercial declaration will happen very soon in early Nov 2014.

Mauda â No schedule has been given as per the merit order of rating. It is not an issue this fiscal.Incentive in Q2FY15 was about Rs 40 crore.

Interesting article on Power sector Companies.

Disc: NTPC in watchlist

NTPC is a recent add to my PF because of

(1) recent win of 470MW solar project - they plan to take their renewable portfolio from 17% of the total capacity to ~40% in the next 10 years. PE multiple will expand from current multiple of 7-8 to 14-16 (given low interest rates this should be the multple for any company that offers an perpetual annuity of cash flows)

(2) On track to an EPS of 14 this year, which itself will take the price to 110 if market remains stable

(3) Power demand to keep rising in the next 2 years as impact of global stimuli hits the economies taking discretionary spendings and industrial activity to higher than pre-covid levels (more washing machines / dishwashers, fans, more industrial activity = more power consumption)

These power companies used to trade maybe two times book or more around a decade back and maybe PE of 15 plus…why has derating happened even though EPS has grown just fine? Is it because of slow down of growth or state discom health or something else? What expectation of street was not met that these got derated…I mean what was street expecting of them a decade back? Thanks

PSUs used to have huge scale which was said to be a competitive edge. Over the years they have proven it’s not.

Market expects only the private sector to perform well going ahead.

Well in case of power generator and distribution…they still have same scale competitive edge. Maybe not anymore in petroleum products, oil, telecom etc. For power, there maybe some other reason for derating as practically no private sector exists in power generation comparable to PSUs

markets also expected HDFC bank to have a lot of unsecured loan defaults come October 2020.

This is a contrarian call and already you can see the PE and PB multiple at multi year low (6x and 1x) and not in sync with the growth NTPC has been posting.

From Q4 FY-21 transcript -June 19 2021 https://www.ntpc.co.in/transcripts/10183/ntpcfy21concalltranscript

=============

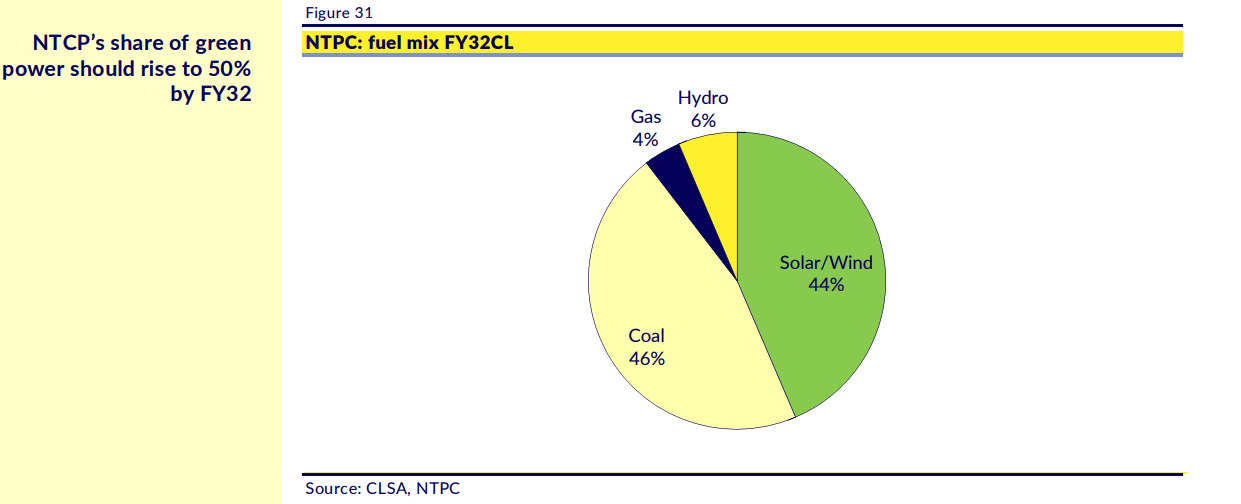

"With these, the commercial capacity of NTPC has become 51725 MW on standalone basis and 64490 MW for the Group as on 31 March 2021.

NTPC group, being a leader in the Power Sector, has strong commitment towards Renewable Energy and would be targeting RE capacity of 60 GW by FY32"

So, growing towards a 50:50 RE capacity. Sounds serious

“A MoU was signed between DVC and NTPC Renewable Energy Limited for setting up of Floating Solar PV Park and projects in the reservoirs under the command areas of DVC in Jharkhand and West Bengal.”

Not sure of capacity…

"NVVN has signed a MoU with South Delhi Municipal Corporation (SDMC) for implementing roof top solar project(s) and 20 MW ground mounted solar project along with charging infrastructure development.

CIL NTPC Urja Pvt. Limited (CNUPL) bagged its first assignment of project coordination for setting up a 50 MW Solar Power Project in Nigahi Coal Mine of Northern Coalfields Limited (NCL). It is a major step towards Green Energy by two major PSUs, NTPC and CIL, joining hands, to create such projects utilizing CIL’s vacant land and NTPC’s expertise. NTPC will act as Project Management Consultant for this solar project.

On RE:

“The installed capacity today is 1365 MW and the capacity under construction is 3019 MW. All of these have PPAs except 125 MW”

===================

Looks like serious moves already happening on RE side and with GOI planning for high targets in RE, this looks like a good opportunity to me…?

Need expert inputs on whether there are risks.

Disc: not invested. Have been avoiding as Coal/pollutor. Now evaluating expecting a serious focus in RE

hey @ChetP

Do you still hold a bullish view on NTPC?

This is my thesis.

Invested a year ago @90 for:

But a year later,

So hence planning to book out gradually, would love to know your thoughts

I have exited recently for making room to tackle US & EU recession. the stock was great at 90-95 Rs but i am constantly looking for doublers in my pf and this one has 30% left on the table.

Hello friends,

This is my first time on this board. I have not studied NTPC fundamentally. This is an attempt to analyze NTPC technically. Honestly on fundamental basis PSU stocks don’t make a lot of sense since they are generally run with greater good in mind rather than making Q-o-Q profits.

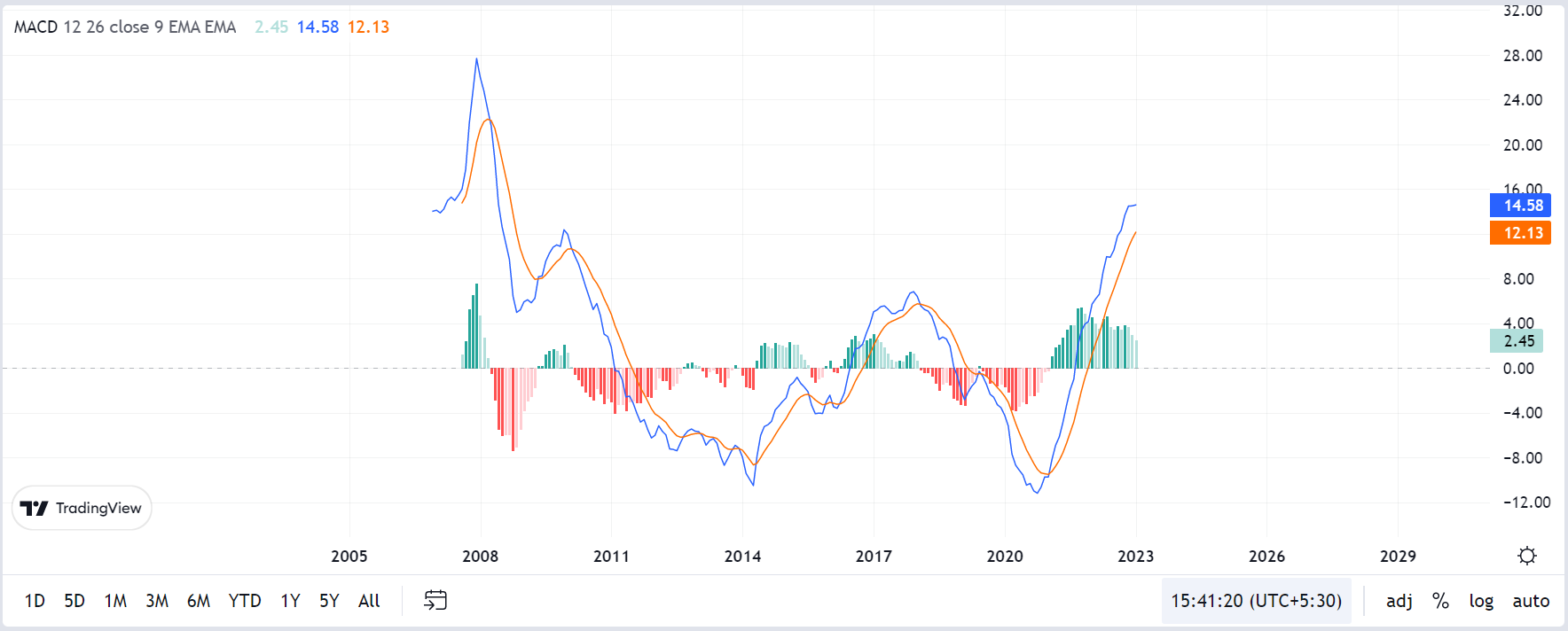

This is how NTPC monthly chart with volumes looks

The monthly MACD is also in positive cross over for long time

Even the monthly RSI is @ 63 (bullish momentum) and showing all right intent

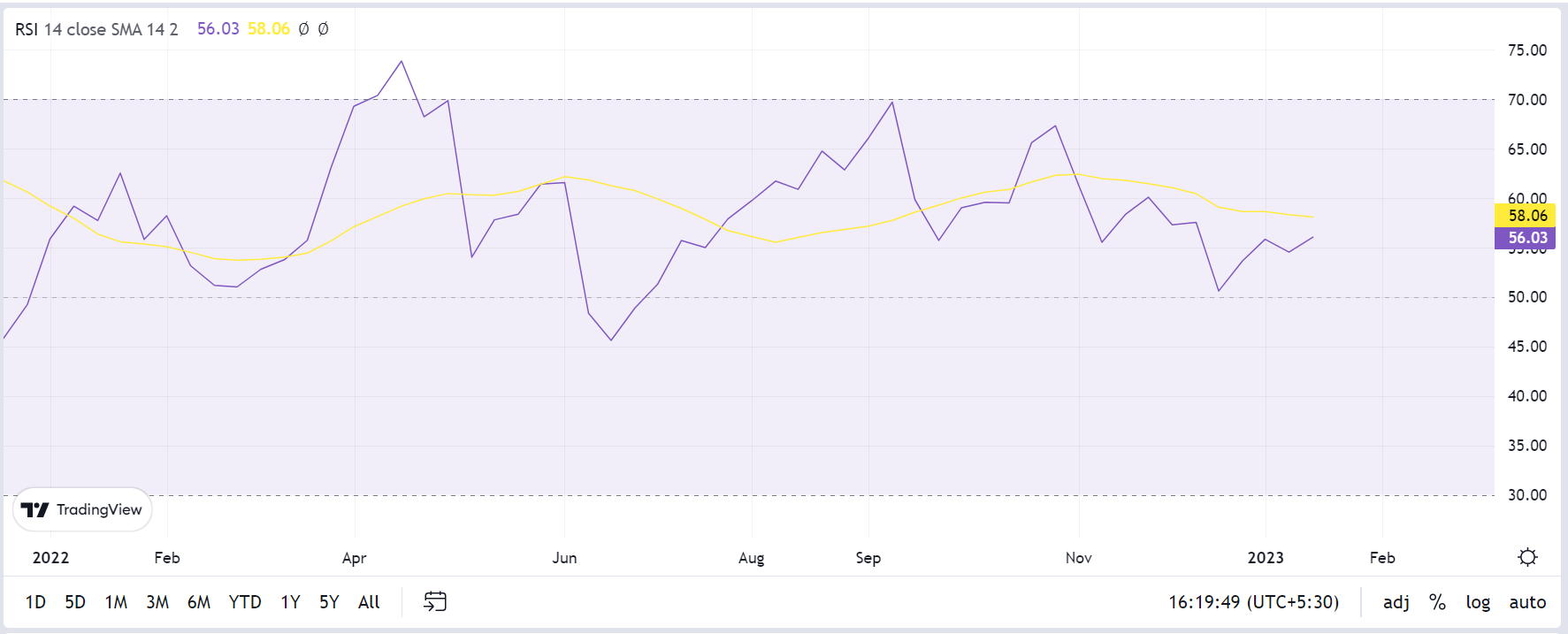

Weekly RSI needs 1-2 good weeks to get into bullish momentum zone

Very recently the 50Mon EMA has given a PCO with 200Mon EMA, and 100Mon EMA is on its way to do so. Difference is very small

INR 183-184 seems to be a mental resistance level for this scrip which it only briefly tested in Nov’ 22 after 12 years. It seems like a shakeout is happening before it breaks and crosses next mental barrier of INR 200/-. However, there is no guarantee that break-out will happen at so & so date/month.

I am going to keep a close watch on this stock for sure.

Disclaimer - I don’t own this stock and I am not a registered stock adviser, so do your own research and don’t believe me blindly

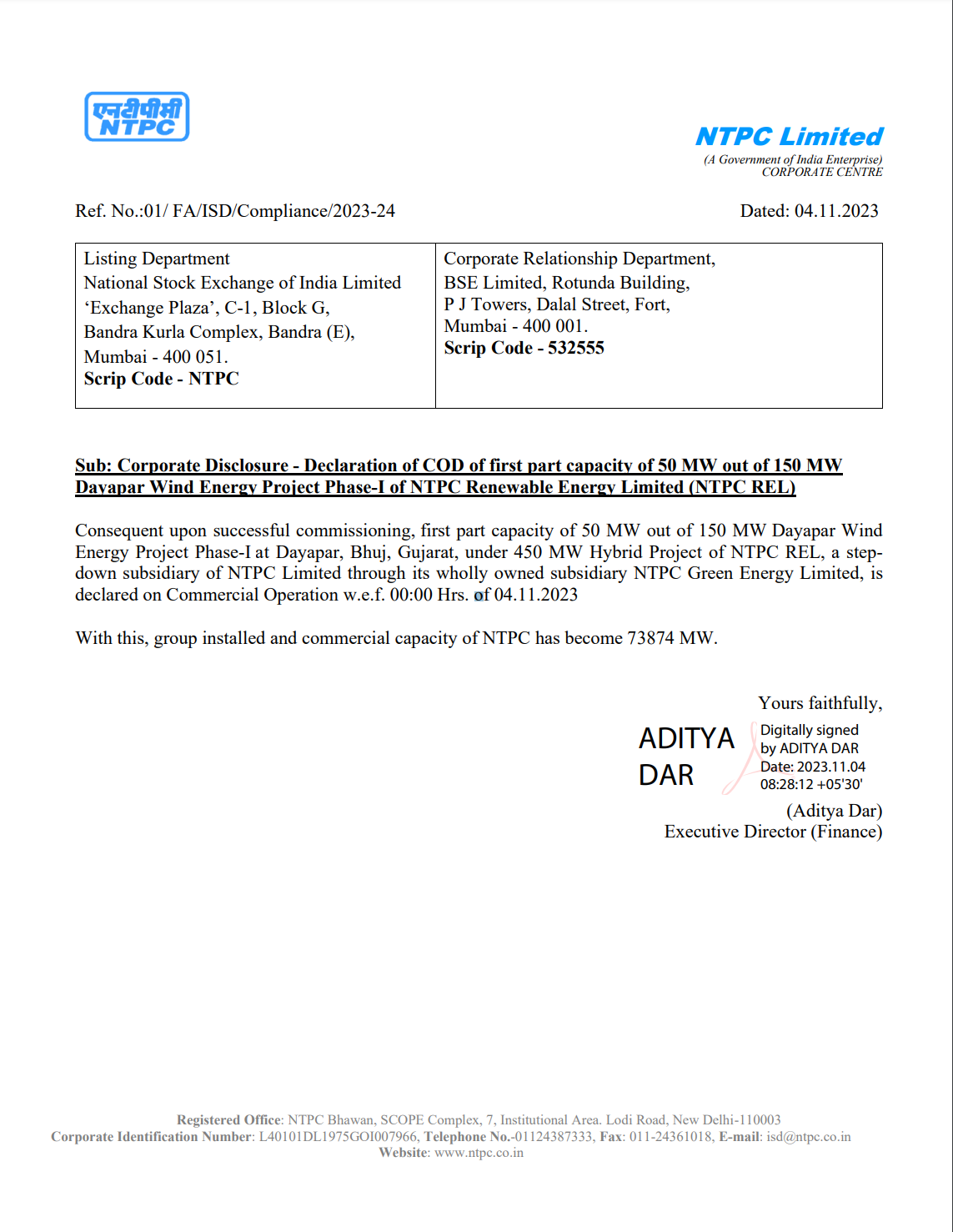

NTPC Limited, has announced that the first part of its 150 MW Dayapar Wind Energy Project Phase-I, located in Bhuj, Gujarat, is now officially operational as of November 4, 2023. This project is under the umbrella of NTPC Renewable Energy Limited, which is a subsidiary of NTPC Limited. As a result of this successful commissioning, NTPC’s total installed and commercial capacity has increased to 73,874 MW.

https://www.financialexpress.com/market/ipo-news-ntpc-to-list-green-arm-ngel-3379302/lite/

To meet the growing demand, the government has announced to continue relying on coal with nearly 80 GW of new coal-fired capacity planned by 2030

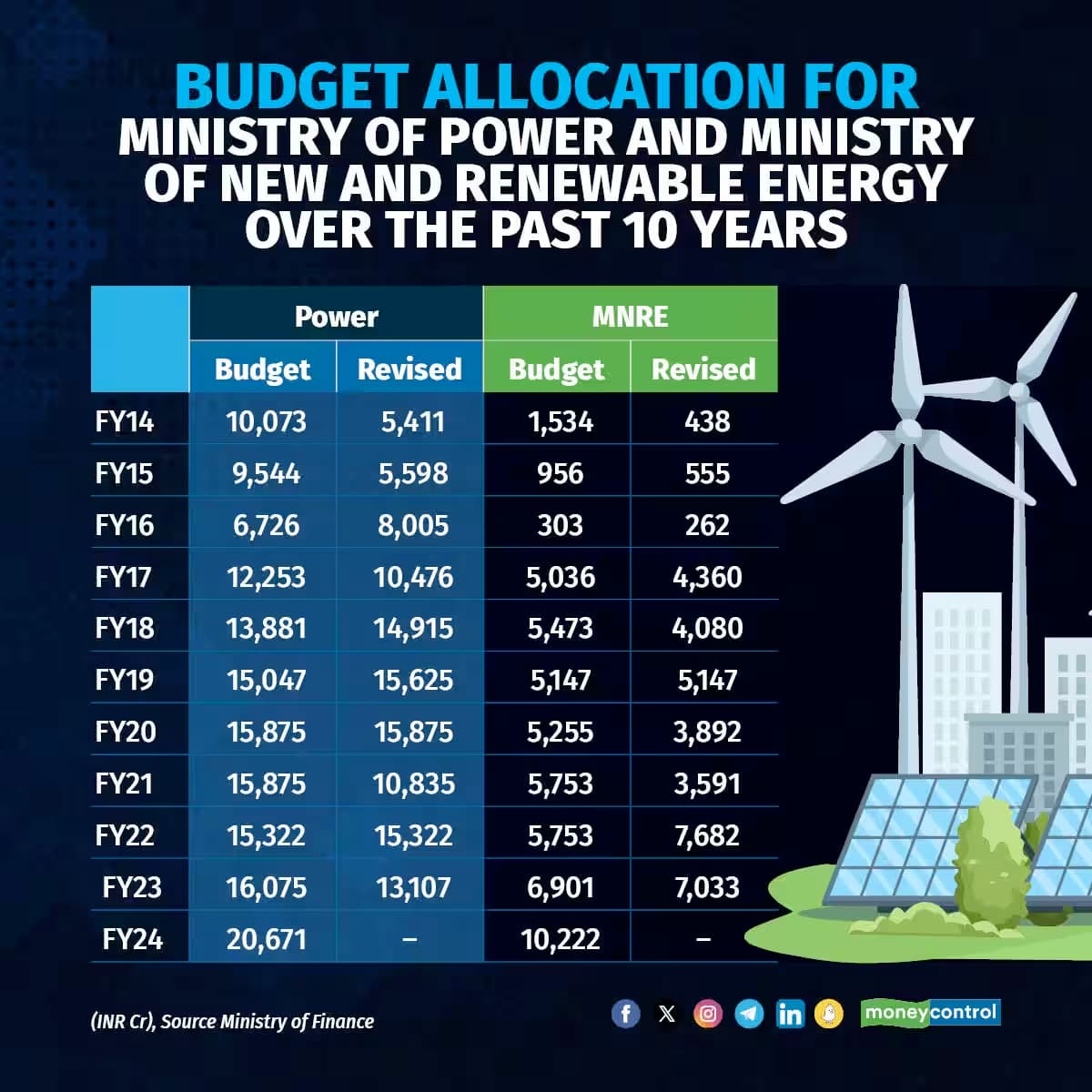

Scaling up renewable energy: The allocation to the new and renewable energy sector increased 99 percent to Rs 10,222 crore in 2023 from Rs 956 crore in 2014-15. Between 2013-14 and now, India’s installed pure renewable energy capacity (excluding hydropower) has almost quadrupled to reach 132 GW from 28 GW in 2013-14.

National Green Hydrogen Mission (NGHM): Since renewable energy alone would not be enough to meet India’s energy needs, the central government has attempted to get into new energy sources such as green hydrogen. The Union Cabinet approved the NGHM on January 4, 2023, with an initial outlay of Rs 19,744 crore, including Rs 17,490 crore for incentives. The government’s aim to produce at least 5 MMT of green hydrogen annually by 2030 under the NGHM would require 60-100 GW electrolyser capacity and 125 GW renewable energy.

India’s power sector is regulated by the CERC with an availability-based earnings model (fixed RoE on power generation assets) and, thus, the regulated tariff model provides strong earnings visibility for power-generation companies.

Additionally, with improved coal stocks at thermal power plants, plant availability factor (PAF) has improved and, thus, we expect fixed cost under-recoveries to decline for power companies.

Quick notes on some terms:

PLF - Plant load factors (PLFs)

A cost-plus basis is a way of charging for a product or service where the price includes the cost of production or service plus a profit

discl: Invested from lower level. not a buy sell recommendation.

plesse do your own assessment before buy sell.