I don’t think it should have that a big impact, my rationale behind this is that market is currently looking at the short term perspective which isn’t good as business is not back to pre-covid levels yet.

Despite that, I find it strange that company is undervalued when many stocks are on a bullish run in other industries which too haven’t recovered properly.

Is there some other backstory to this which is overshadowing the numbers?

On the cyclicity front, there are two factors at play - the raw material prices and the prices of the product itself. Both impact the margin severely and both often happen together.

Typically in the upcycle, a lot of players increase capacity and this leads to overcapacity in the sector as a whole, which puts a lot of pressure on product price when supply increases.

We may be at the top of the cycle at the moment but the stock market always discounts a cycle turn in advance (and in anticipation). But NR Agarwal’s strategy of moving towards higher margin packaging paper and the already discounted valuations to peers does offer a lot of margin of safety. The growth in profits going forward is what the market is seriously doscounting

At one stage I really liked the company but the corporate governance has been a huge issue.

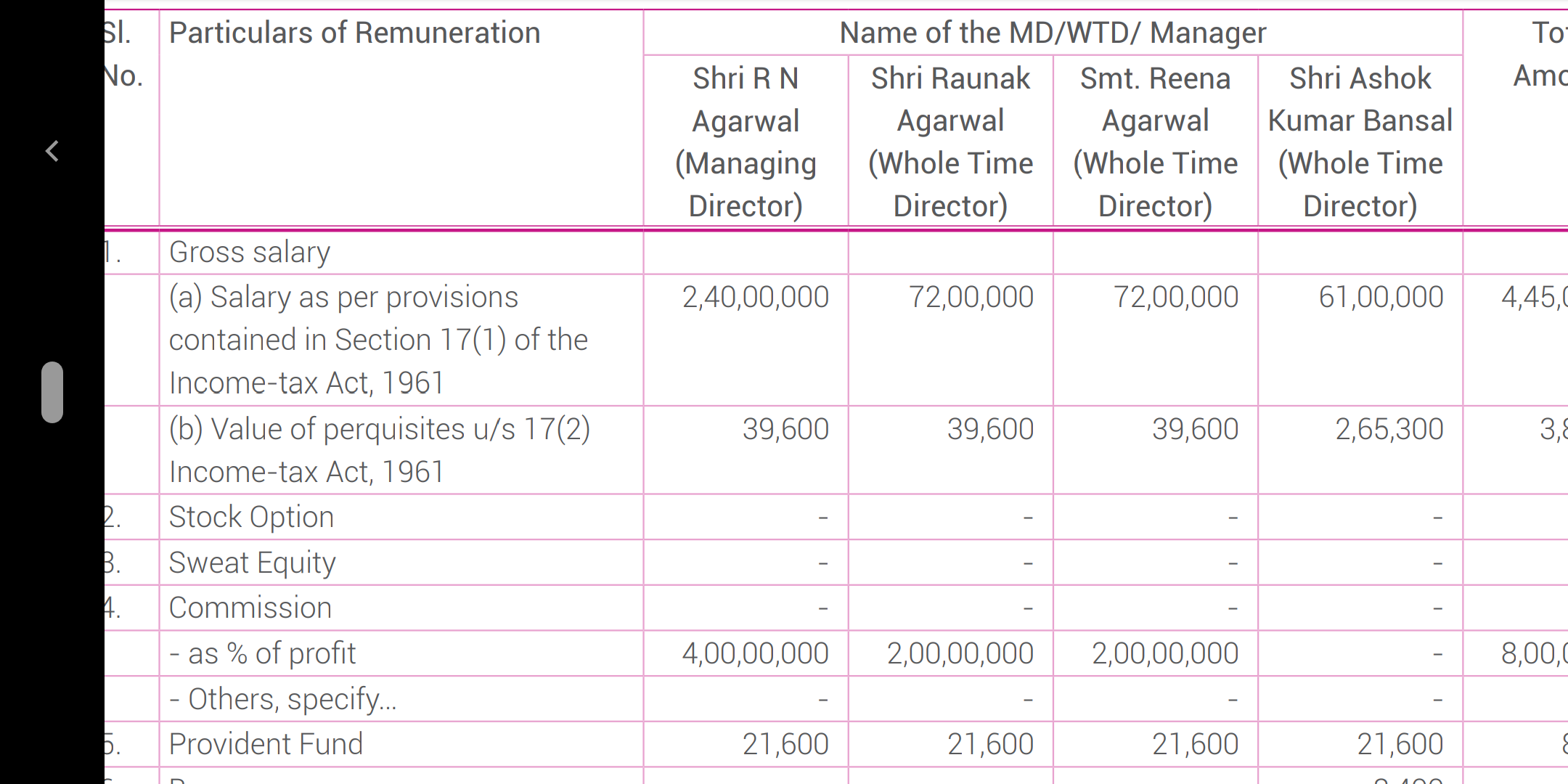

The salary drawn by the promoter and his wife and son have been a big drawback for me. They can easily hire a very good professional at a much lower salary.

It is only an early indicator that when there are big profiys the promoter will take some route to transfer them to his kitty.

One learning from the past. Greedy promoter + great company = very bad investment

The promoters of almost all of the small cap family owned companies pay high salaries to themselves. This by itself is not a red flag. In my opinion, it is much better to take high salaries than to siphon funds off the company illegally.

Besides, even after paying high salaries, the return ratios are excellent.

Another point that I was thinking for undervaluation could be that company lacks a sustainable economic moat. I read somewhere that when a stock goes on a bull run, it usually accounts for the growth potential that can be observed in a 3-5 year landscape.

Dividend paid: 1.36 crores

Salary + comission to the family(father mother and son) other than other perks and benefits which need deeper digging is 12 crore plus.

Will they pay the shareholders their due in the future or will the payout ratio be the same?

I think investors looking to invest in businesses with a moat should stay away from this Company and any paper company for that matter. The industry offers a purely commodity based product whose input prices fluctuate a lot and buyers really don’t care about what brand of paper they’re using.

The investment in this stock has to driven by the valuation and growth (if any) expectations. My reverse DCF assumes that the Company needs to grow at 3.3% for 10 yrs and then terminally grow at 0.5% while taking a starting FCF value of 72 crores based on average of last 3 FY’s FCF. This discounted back at a hurdle rate of 16% to give me something close to today’s price.

If you believe in these numbers then I think it’s worth looking deeper into, which I am going to do.

How does that make sense? The company is selling for 340 crores. And you are taking a starting FCF of 72 crores. That is a 5 times free cash flow valuation.

I ran the same numbers and it seems like at this valuation, the market is expecting a negative growth rate.

@Pavandeep_Singh he’s taking a starting FCF of 72 crore (like an estimate for the this year). Thats reasonably accurate.

I am factoring in a growth rate of much more that 3.3% over 10 years and thats why tis seems very undervalued to me. That said, it is possible that the near term growth may be negative with the cycle turning, but that seems to be factored in by the market already

Surprisingly decent results from the company for the June Quarter. Was expecting a net loss & little to no revenues at all considering their regular plant shutdown announcements. Now I’m quite sure that the market is mis-pricing the business. It’s just a matter of time before this mis-pricing gets corrected. Will just have to wait it out.

Very surprising indeed. Plant shutdown is one thing, but who is buying? Writing and printing must be completely wiped out in this quarter. I wish they would give the segmental break up.

Also, is anyone tracking whats hapening wiht the other paper stocks? Is there any chance of consolidation in the industry?

Message from the Chairman and MD in the Annual report. I appreciate the clarity.

“The message that I wish to communicate to our stakeholders is that there will be a decline in our revenues and profits during the current year. However, N R Agarwal will continue to remain profitable on account of a broad-based business model. The Company will protect the integrity of its Balance Sheet and its competitiveness till the time demand revives and the Company is better placed to enhance value for its stakeholders once more.”

Just completed my analysis on the Company last night so posting my report and model here. Please do take a look and feel free to share your view or point out errors.N R Agarwal Inds.pdf (940.3 KB) NR Agarwal_Model.xlsx (117.5 KB)

For a company with ROCE’s in excess of 32% and D/E being 0.3 - Market is valuing the company unbelievably low with P/E of less than 4 and Mcap / FCF of just 5. And this low valuation has been right from 2018 onwards.

The EPS and EBITDA margins have been pretty decent in last few years.

Is there some risk which market perceives or is it just the fact that the paper sector has lost favor with the market.

Experts pls guide to any factors / view points on this case of extreme low valuation.

All paper stocks are trading at very low multiples. Paper stocks in the age of Tech are obviously not going to be valued by the market. There are only numbers and no glamour to back it up.

On the other hand the market could be rightly assuming a turn in the paper cycle and things could get ugly for a lot of companies as they might not even turn a profit on the bottom line. However that has only happened for one year out of 11 in its history.

For me this is more of a heads I win, tails I don’t lose much kind of idea.

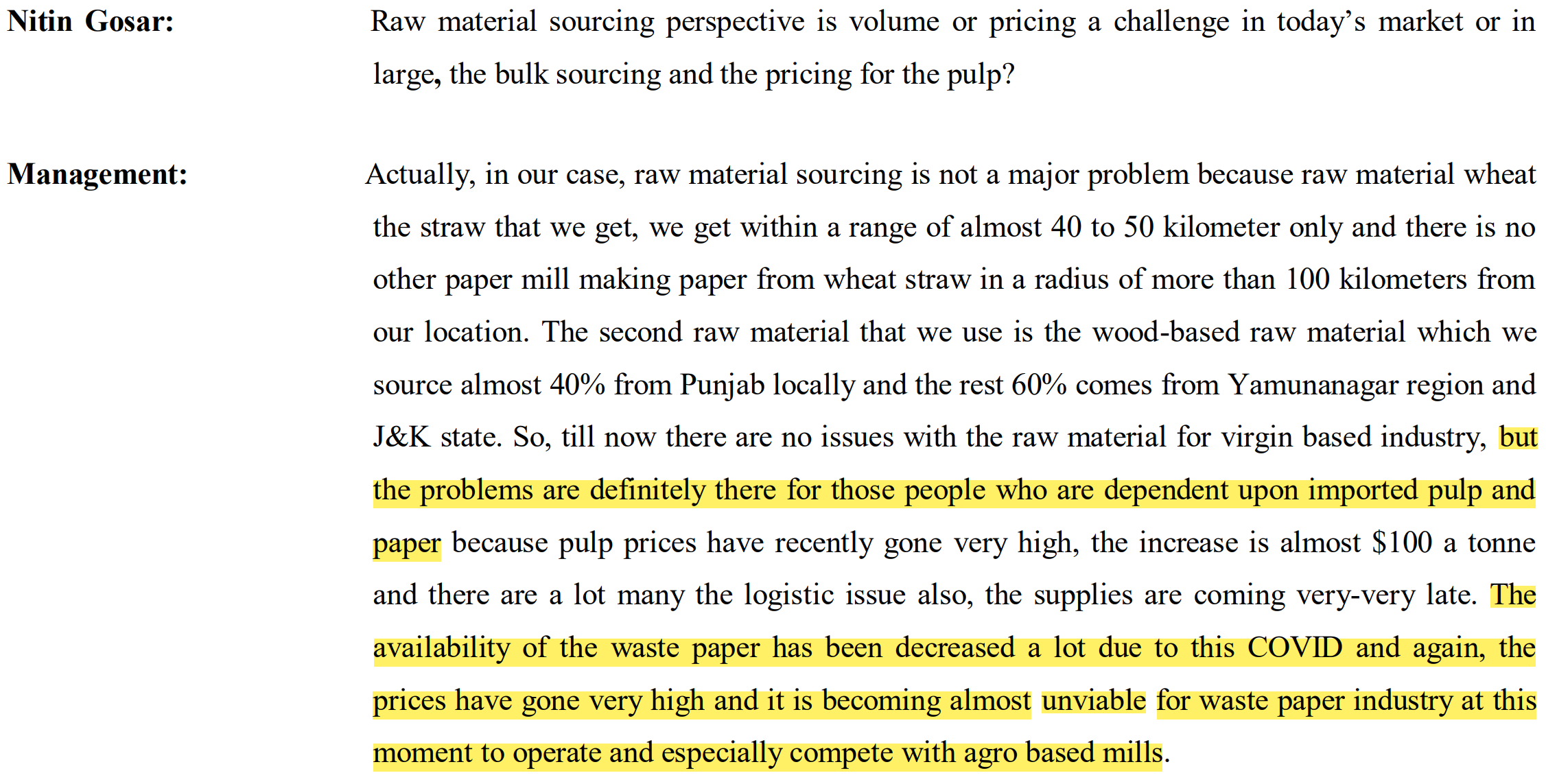

I have been tracking another paper manufacturer - Satia Industries. Not invested, just started tracking. In their earnings call of Q2/FY21, there was a question about the price of raw materials. Since NRAIN uses waste paper, I thought this info might be useful here…

The management claims to have factored in fluctuations in raw material prices and availability to a certail extent. Quoting from Note 41 of their anual report for FY 20:

"The Company is affected by the price volatility of certain commodities. Its operating activities require the ongoing manufacture of paper and paper boards and therefore require a continuous supply of raw materials i.e. waste paper, chemicals, coal etc. being the major input used in the manufacturing. Due to the signifcantly increased volatility of the price of waste paper and coal the Company had entered into various purchase contracts for these material for which there is an active market. The Company’s management has developed and enacted a risk management strategy regarding commodity price risk and its mitigation.

The Company partly mitigated the risk of price volatility by entering into the contract for the purchase of these material and further the Company increases prices of its products as and when appropriate to minimize the impact of increase in raw material prices."