- Company is consistently performing.

- Promoter has recently released pledged shares.

- Debt has reduced in last quarter.

- At 430, its lucrative now.

Any comments please

Its running out of its capacity. No volume growth visibility.

IRR report on NRAIL. Ongoing Capex shd yield improved revenues from FY19 onwards.

1 Like

@hitesh2710 Sir ur views on this company is appreciated. Rising ROE, ROCE, Cash flow, PAT margin, Reducing D/E. A potential candidate for good returns considering Paper sector tailwinds?

2 Likes

Why this stock is continously going down having low PE & favourable tail wind.I can’t understand

I am also searching, not getting any negative news, but share price keep falling from 500 level to 360 level, I got following two news from ratestar, may be expecting less sales due to this, I am not sure.

NR Agarwal Industries has temporarily shut down operations of its Unit 5 for a period of 15 days with effect from November 11, 2018 for the purpose of annual maintenance.

NR Agarwal Industries has temporarily shut down operations of its Unit 2 for a period of 30 days with effect from November 25, 2018 for the purpose of annual maintenance.

Paper prices have corrected 4% recently. In a cyclical stock, the PE will look cheap at the peak of the cycle. Not sure if it is peak margins for paper. But if paper prices remain soft , you should expect selling in the stock. I am not giving a recommendation here. just sharing my thoughts.

1 Like

NR_Q3_2019.pdf (876.0 KB)

Flat results

Q3FY19 results are good given the backdrop of maintenance shut down of Unit II and Unit V for 30 days and 15 days respectively.

Discl: Invested

3 Likes

Q4FY19 results depressed. Though the revenue has increased by 9.8% and 15.36% for Y-O-Y & Q-O-Q respectively, but due to increase in cost of Material (17.23%), Employee benefit Expenses (73%), Other expenses (16.75%)on Y-O-Y basis, profit before Tax has dented by 27.33% Y-O-Y .Equally Q-O-Q profit also has declined 30.85%. Paper Industry fortunes are in declining trend.

Disc: Invested and no transaction for the past 60 days.

1 Like

Little shocking numbers for me as well.

Raw material and employees expenses as %ge of sales are very high this qtr. Also, they paid 37% tax. All these led to suppressed bottom line.

Also gross block increased by more than 10%. Further they did some technology upgradation in recent times. These should yield good results in future.

Management should focus less on news print papers and focus more in kraft papers.

Disc- invested & will continue to hold. 7% of PF. No transaction in last 3 months.

1 Like

So this stock is available at a PE of 3.x with a 30%+ Roce and reducing debt. Something’s not adding up?

2 Likes

It seems to be a clear case of mis-pricing by Mr. Market. The company has been consistently churning out good numbers for the past many years…& as far as I can tell, the business is run exceptionally well and the accounting standards are at par with the best in the industry. Ticks all the boxes: Good Business, Excellent Management, Exceptionally low valuations. The only question is…when will the market realise all this (hopefully soon).

Disc- Invested recently (17% of portfolio)

@ArunValoor is that the case though? Or is it that we are at the peak of the paper cycle and thats why we have low PEs and high earnings? Though the earnings for NRA have been consistently good even though this is more or less a cyclical industry.

Have you been tracking the demand and supply situation for NRA’s products? If yes, please do share some insights

We are at peak cycle for paper manufacturers. Good last 3-4 years. Cycles cant last upto 5 years. But even we normalise the spread to 10-15 year median, valuations are reasomable. So chance of decent gains in this sector, as some consolidation and anti-import sentiment.

1 Like

Segment breakup: 46.3% from writing & printing paper AND 45.2% from packaging boards. There’s definitely a risk of the cycle turning…& the results for the June qtr’s going to be pathetic (I have no doubts about that). But, I’m quite confident about the management & their ability to pivot at critical junctures. Mr. R N Agarwal has already proven this a couple of times. They’ve already indicated that that over the next few years, the packaging paper and boards (PPB) segment is going to grow the fastest and they’re foraying into packaging in a big way (They already sell to FMCG bigwigs indirectly). If they’re able to make that pivot successfully, it’ll be a sight to watch. Also, even when we compare the valuation of NRAIL with its direct competitors, the valuations still don’t make any sense. There seems to be a good margin of safety. #GameOfProbability

2 Likes

Agree, the margin of safety from a medium to long term is definitely there at these valuations. What I’m not able to wrap my head around is why has this mispricing lasted so long? The cash flows are great, return ratios are stellar, profits are increasing and debt is low. Plus the’ve added capacity, more efficient technology and are also moving away from low margin products like newsprint paper. And most of all the management is credible. And still the market has not latched on for quite a while.

Why? What is it that the market is seeing that we are not?

3 Likes

Company has temporarily shut down Unit 2 (Writing and Printing) due to lack of orders.

Not looking good.

3 Likes

Hello,

I have been reading VP a lot lately. Amazing forum. Thanks @Ansh_Gupta for introducing me to this wonderful platform.

I am very new to value investing and this is my first analysis of a company. Please help me out if I go wrong/vague somewhere.

This is my take on the company:-

Company Background-

- · 27 years old company, family run paper manufacturing business. 5 units across Gujarat. Promoter- Mr R. N. Agarwal.

- · Business Type- Mainly B2B, Recently entered B2C with copier paper

- · Product portfolio-

-

- Writing and Printing Paper- 46%

-

- Duplex Board- 45%

-

- Newsprint- 9%

- · 5 units:

-

- Unit 1- 8000 TPM (Duplex Board)

-

- Unit 2- 5500 TPM (W&P Paper)

-

- Unit 3- 3500 TPM (Duplex Board)

-

- Unit 4- 3500 TPM (Duplex Board)

-

- Unit 5- 9000 TPM (W&P Paper)

- Sales: 85% Domestic, 15% export

- Overall capacity- 3,54,000 TPA

Elevator Pitch-

· 27 yr old paper company, mainly B2B, cyclical, good numbers for the past 3 years.

· Pricing wise seems undervalued w.r.t. industry and market

· Growth potential and capex plans to increase capacity, plans for becoming debt free

· Company moving towards more profitable product segments and exiting declining newspaper industry

-

Positives-

o Long term growth potential due to undervaluation and increasing demand of paper as a packaging substitute.

o Recent increase in promoter shareholding -

Immediate negative triggers include

o Increase in other current liabilities (Don’t know what the liabilities are and what will be the impact on the company)

o Covid-19 demand slowdown

o Raw Materials cycle turning around

Industry Trends-

- Growing demand of paper. Domestic paper demand grew at a CAGR of 6.3% from 2008 to 2018 owing to rising literacy rates, ecommerce book, reduced demand of single use plastic for packaging.

- Under penetrated market as compared to developed countries. FY 18-19 AR mentions per-capita consumption around 13 kgs in India as compared to a global average of 57 kgs.

- Capital intensive industry, making it difficult for new players to enter in this sector.

- Cyclical industry, raw material price fluctuations are difficult to pass on to the customers hence company bears the load.

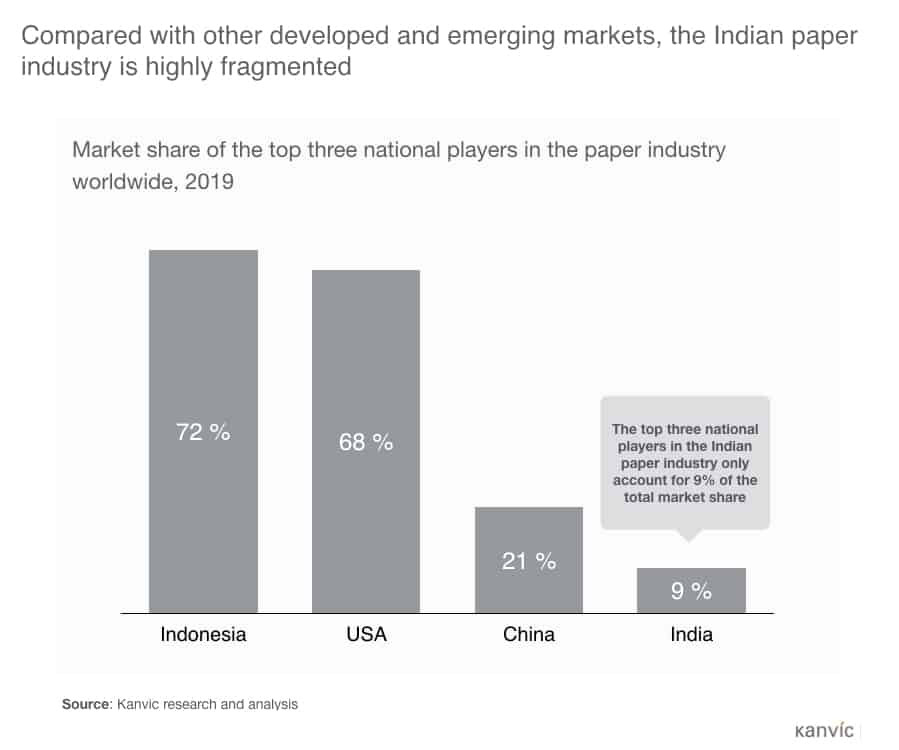

- Paper industry is expected to enter a consolidation phase. Don’t know how this will turn out but found this fact very interesting. Larger moat, cyclical nature can lead to consolidation and emergence of few top players instead of a segmented industry. (Source- Kanvic)

Business Attractiveness (Qualitative)-

-

- Recent switch from Newsprint to Writing and Printing paper. Moving away from fading newspaper segment towards a growing product segment.

-

- Company according to FY 18-19 Annual report expects to be debt-free by 2023-24. (Might get changed/extended due to Covid-19 impact). Long term borrowing reducing every year.

-

- Company focused on increasing operational efficiency (see numbers below) to gain competitive moat.

-

- Company planning to expand the Duplex Board segment from 1,80,000 TPA to 3,30,000 TPA (+ 83%) by 2022-23. (Rationale Given- “ High demand in western region, plastic ban, growing export demand)

Business Attractiveness (Quantitative)-

Trends-

| 5 yrs | 3 yrs | 1 yr | |

|---|---|---|---|

| Sales Growth | 14% | 10% | 6.60% |

| PAT Growth | 33% | 23% | |

| OPM | 13% | 14.30% | 15.40% |

| P/E Ratio | 4.91 | 4.64 | 3.30 |

Sales growth has been stagnant, however Operating margins have improved over the years. Still okayish. Company is planning to increase capacity over the next few years.

Operational Performance-

| 2018 | 2019 | 2020 | |

|---|---|---|---|

| EPS | 53 | 56 | 69 |

| RoCE | 27% | 27% | 33% |

| RoE | 41.13% | 30.30% | 27.88% |

| RoA | 13% | 12% | 13% |

| Current Ratio | 1.12 | 1.31 | 1 |

| D/E Ratio | 1.32 | 0.95 | 0.41 |

| Operating Cash Flow | 104.12 | 112.18 | 191.45 |

| Free Cash Flow | 54.48 | 22.53 | 114.49 |

| Gross Margin | 41% | 41% | 44% |

| OPM | 13% | 14% | 15% |

| NPM | 7.58% | 7.18% | 8.31% |

· EPS is increasing steadily

· RoCE is good (>25%)

· ROE is good

· Current Ratio is reducing which is not a good sign. (If someone can shed some more light here not able to understand this properly)

· D/E ratio reducing steadily

· Healthy cash flow

· Net profit margin unchanged but positive

Valuation-

| Market Cap (in cr) | 386.08 |

|---|---|

| P/BV | 0.92 |

| P/E | 3.31 |

| Industry P/E | 10.87 |

| EV/EBDITA | 2.43 |

Performed a quick DCF. Presenting the results below

| 3 yr Avg FCF | 54 |

|---|---|

| FCF Growth rate for first 5 years | 6.6% |

| FCF Growth rate for last 5 years | 5.0% |

| Terminal Growth Rate | 3.0% |

| Discount Rate | 12.0% |

| Year | Cash flow | NPV |

|---|---|---|

| 1 | 57.6 | 51.4 |

| 2 | 61.4 | 48.9 |

| 3 | 65.4 | 46.6 |

| 4 | 69.7 | 44.3 |

| 5 | 74.3 | 42.2 |

| 6 | 78.0 | 39.5 |

| 7 | 82.0 | 37.1 |

| 8 | 86.0 | 34.8 |

| 9 | 90.4 | 32.6 |

| 10 | 94.9 | 30.5 |

| Terminal Year | 10.0 | |

| Terminal Value | 1085.7 | |

| PV of Terminal Value | 349.6 |

| Total PV of cash flow | 757.4 |

|---|---|

| Total Debt | 173.0 |

| Cash & Cash Balance | 5.7 |

| Net Debt | 167.3 |

| Share Capital | 17.02 crores |

| Face Value (INR) | 10.0 |

| Number of Shares | 17020000.0 |

| Intrinsic Share Price | 346.7 |

| Margin of Safety | 30% |

| Lower Intrinsic value | 242.71 |

| Upper Intrinsic value | 450.75 |

Taking a 30% margin of safety, this stock still seems undervalued.

(This is my first DCF, please let me know how I can improve DCF analysis)

Competition-

| Name | Mkt Cap (in cr) | P/E | ROE | EV/EBIDTA |

|---|---|---|---|---|

| N R Agarwal | 386 | 3.31 | 32% | 2.43 |

| JK Paper | 1730 | 4.92 | 20% | 4.23 |

| West Coast Paper | 1264 | 3.41 | 30% | 2.56 |

| Andhra Paper | 897 | 6.84 | 24% | 3.81 |

| T N Newsprint | 869 | 25.6 | 8% | 5.37 |

| Century Textiles | 3751 | 10.84 | 13% | 9.59 |

· P/E is way below industry average.

· RoE slightly better than industry.

· EV/EBDITA is low because of the fall during Covid-19 Lockdown.

Challenges-

- Cyclical stock, raw material price increase can hamper operating margins.

- Lack of demand due to Covid-19 (Company recently stopped operations (temporary) in Unit 2 due to lack or orders)

- Digital Transformation will reduce use of paper for office use as manual work will be shifted to computers.

My Take-

- Company has progressed nicely in the last 3-4 years. However, raw material prices will dictate the profit margins of the company.

- Covid impact has been huge on the company and the company is expecting a bad quarter, also had to shut down one unit temporarily.

- Long term wise it looks good especially beacause company looks undervalued in the market and company also has plans to increase Duplex Board capacity becuase of growing demand.

(Since this is my first attempt, there might be some mistakes or vague conclusions. Please let me know I will rectify them, it will be a learning experience for me. It would be great if people reading this can also give me suggestions on how to improve in the future, what other parameters to look at and how to understand the numbers from a long term perspective. Open to all suggestions/feedbacks.)

16 Likes

Yes, with these valuations (3 PE), it is difficult to see why such a well run business is not valued well. I do not understand paper cyclicality but, would a downturn have such a bad impact on this company that the market has thrashed the valuation?