Northern Arc: The White Revolution of Finance !

Wall Street Capital. Village Street Borrowers. One Invisible Bridge.

Seventy years ago, India faced a “Milk Paradox.”

We had millions of dairy farmers in rural Gujarat with surplus milk, and we had millions of urban families in Bombay wanting to buy it. But they couldn’t meet. The supply was fragmented, the logistics were impossible, and the commodity was perishable—milk would spoil long before it reached the city.

The solution wasn’t just to buy more cows. The solution was Amul .

Amul didn’t just trade milk; they built the “Cold Chain.” They created the hard infrastructure to collect, pasteurize, process, and distribute a perishable commodity at a scale the world had never seen. They turned a disorganized, risky cottage industry into a standardized, reliable asset class.

Northern Arc Capital is doing for Money what Amul did for Milk.

The Money Paradox

Today, India faces a similar paradox in finance.

On one side, you have Global Capital —trillions of dollars in sovereign wealth funds, mutual funds, and big banks—desperate for yield.

On the other side, you have Bharat’s Aspirations —the truck driver in Salem, the kirana store owner in Bihar, the women’s self-help group in Odisha. They are credit-worthy, hardworking, and hungry for capital.

But just like raw milk, this credit demand is “perishable.” To a big bank in Mumbai, a ₹50,000 loan in a remote village looks too small, too costly to service, and too risky to touch. The “spoilage rate” (risk of default) is perceived to be too high.

Most NBFCs try to solve this by acting like local milkmen—they lend directly, take all the risk, and hope for the best. When the season turns bad (like the recent Microfinance stress), they suffer.

Northern Arc is different. Northern Arc built the Cold Chain.

They have spent the last 15 years building a financial operating system designed to collect “raw” credit demand from the deepest corners of India, process it, and deliver it to the world’s most sophisticated investors.

Here is how their “Credit Cold Chain” works:

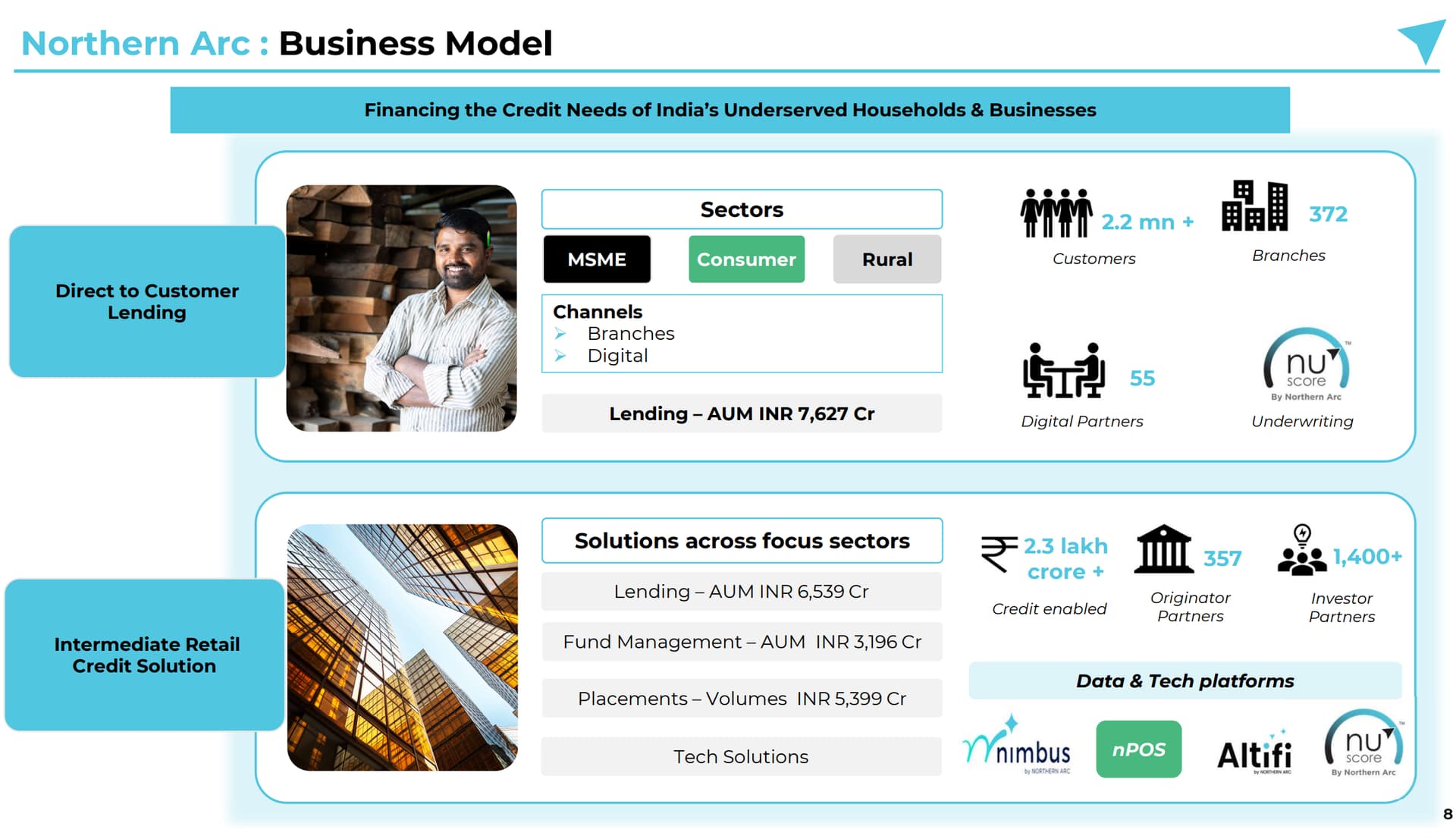

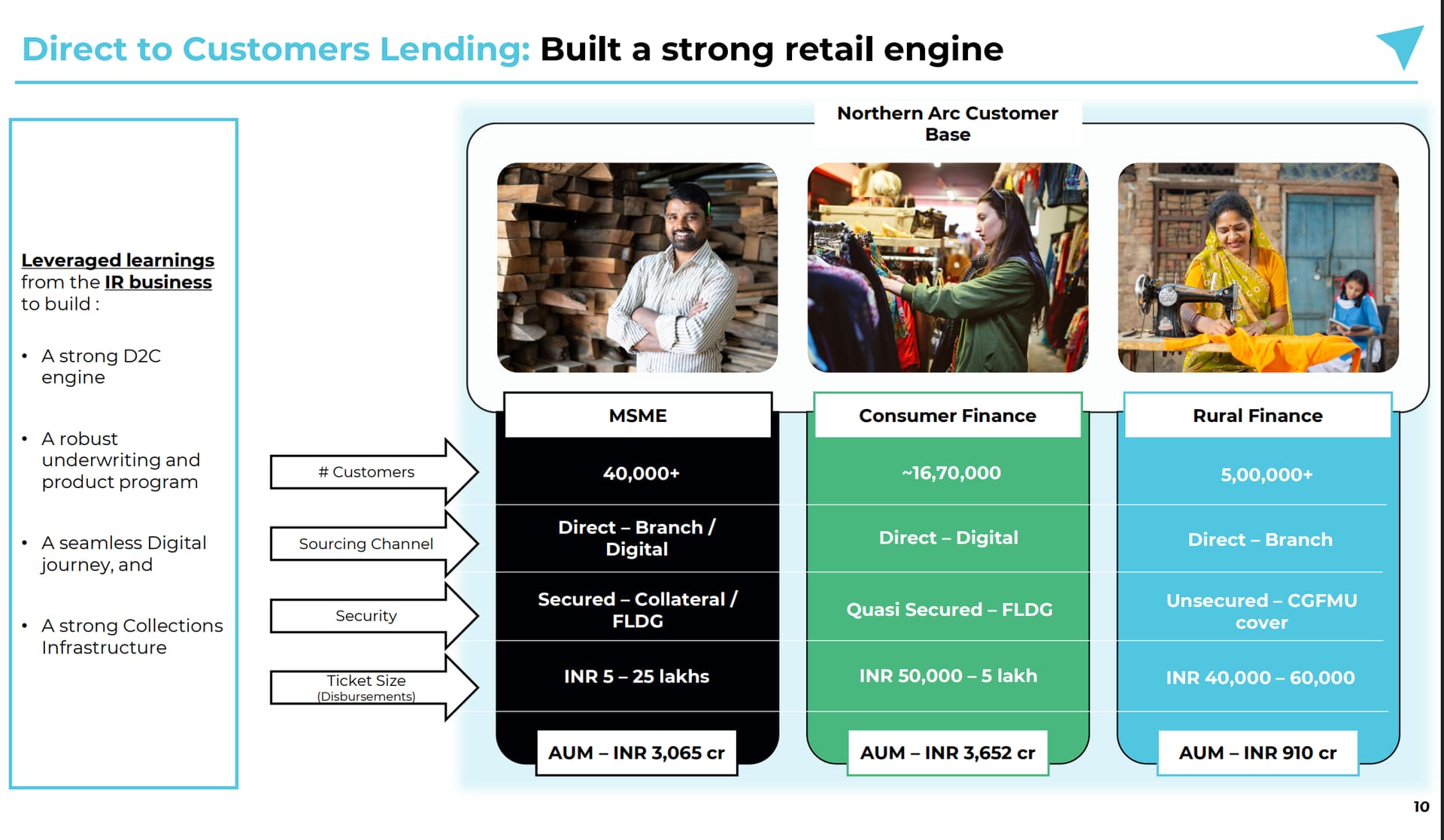

- Collection (The Reach): Just as Amul connects 3.6 million farmers, Northern Arc has built pipelines into 671 districts across India. They don’t just wait for borrowers; they actively source credit demand through 357+ originator partners , reaching areas where big banks fear to tread.

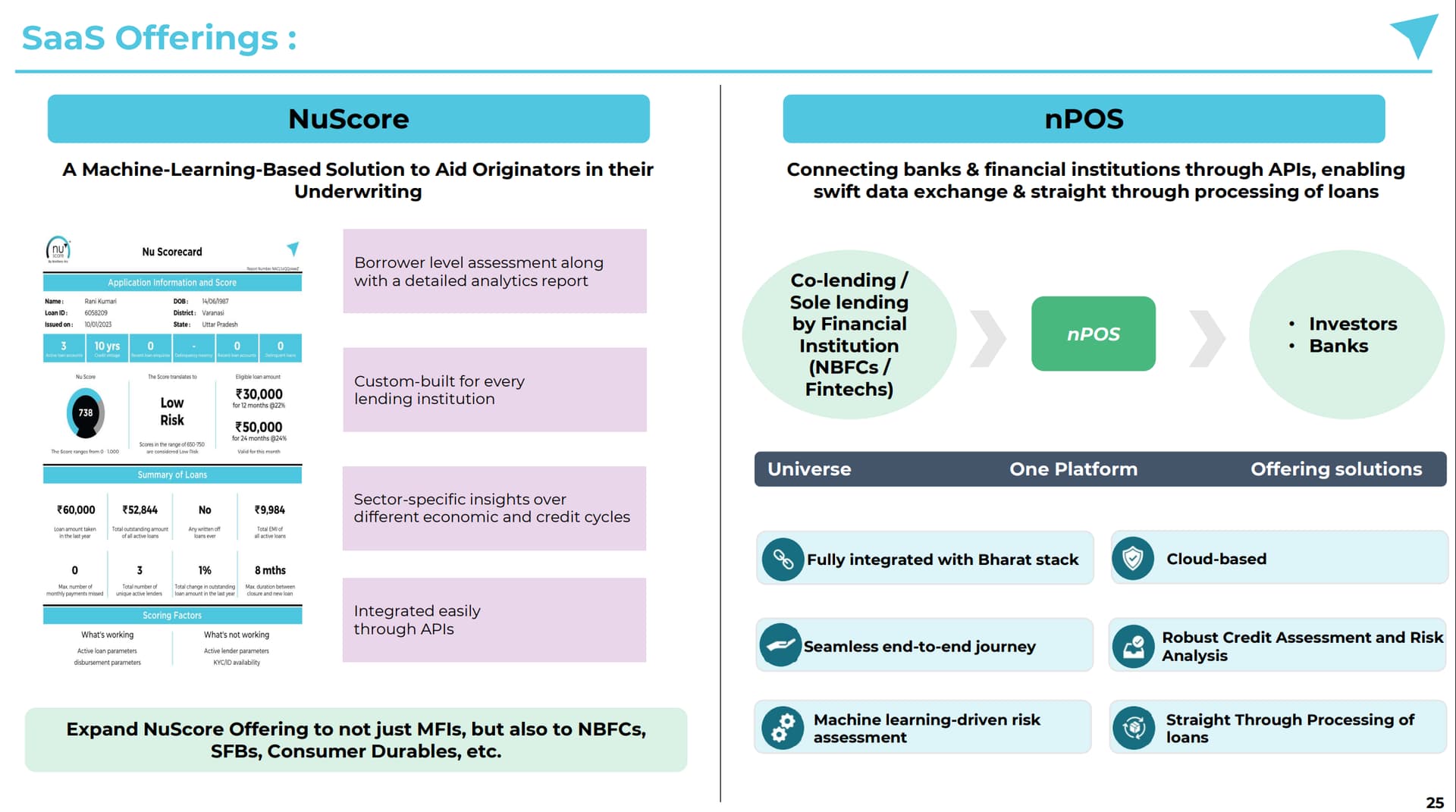

- Pasteurization (The Technology): Raw milk has bacteria; raw credit has default risk. Northern Arc runs every loan through NuScore —their proprietary risk engine. Having analyzed over 48 million loan performance data points , they don’t guess who will default; they know . They filter out the “bacteria” (bad risk) before it enters the system.

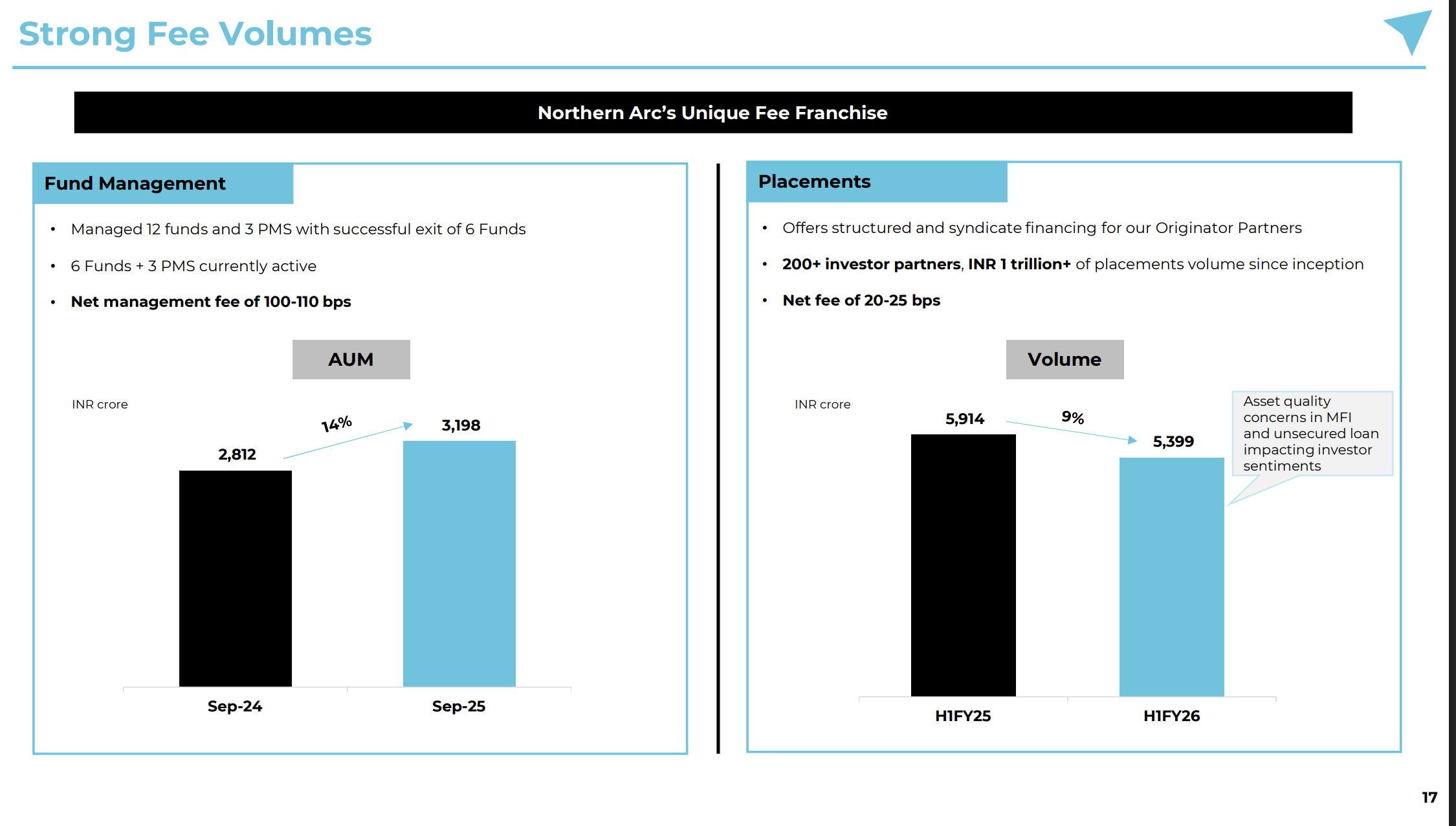

- Packaging (The Structuring): You can’t sell loose milk to a global pension fund. Northern Arc packages these tiny, fragmented loans into rated, standardized securities (Securitization) or wraps them in government-backed guarantees (like CGFMU). They turn risky borrower demand into Triple-A investment products.

The Proof in the Pudding

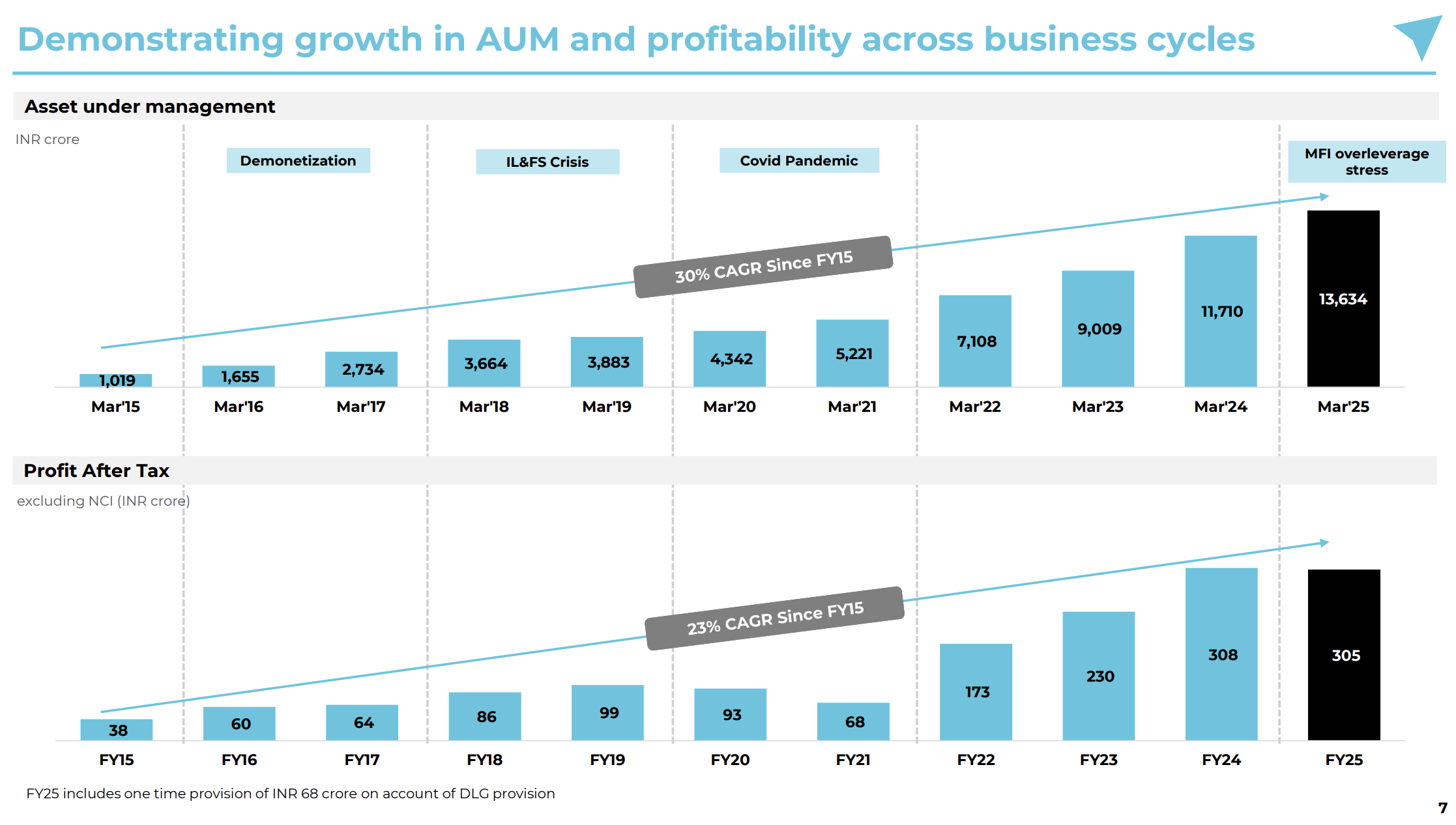

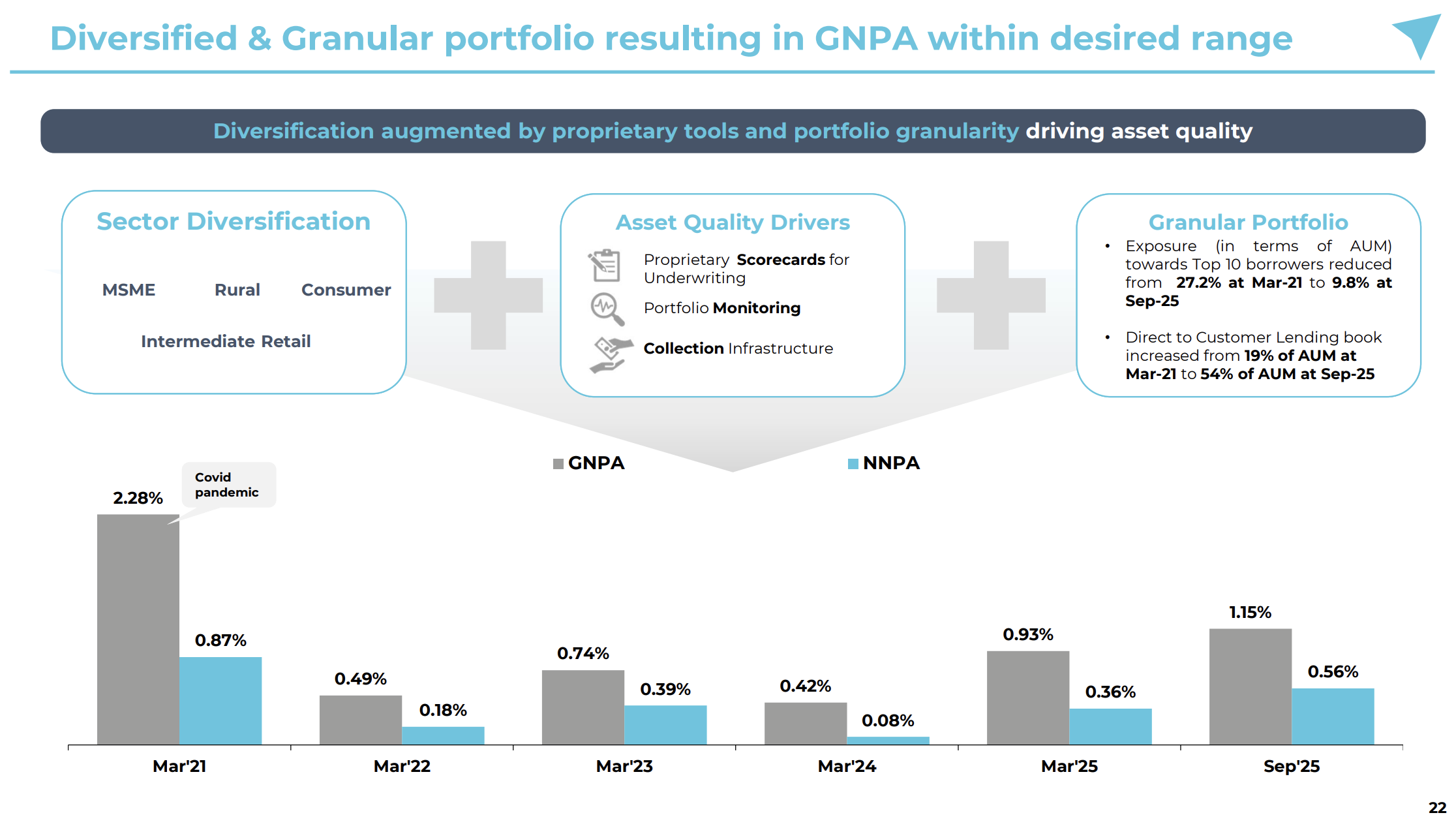

The true test of infrastructure is a storm. In FY25, the Indian Microfinance sector faced a crisis of over-leveraging. While many lenders saw their books curdle, Northern Arc’s “Cold Chain” held firm.

Their sensors tripped early. They calibrated their intake, slowing MFI growth to just 6% while ramping up secured MSME lending by 42% .

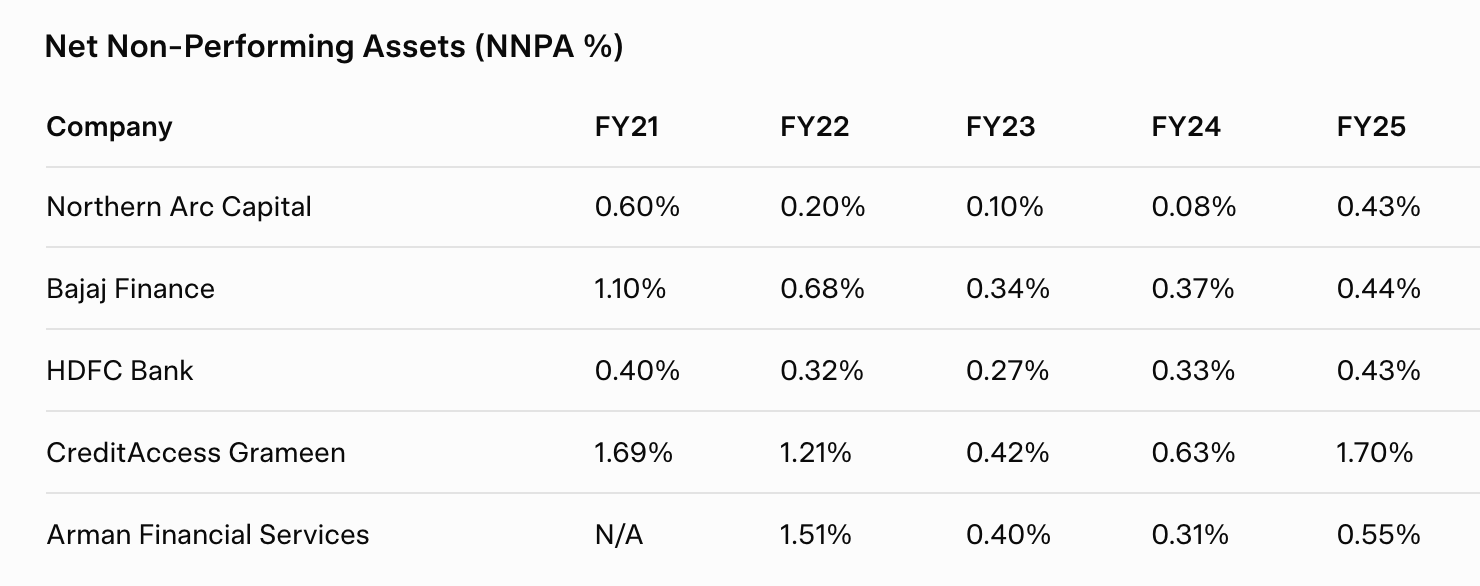

The result? In a year of industry-wide stress, Northern Arc delivered a 2.6% Return on Assets (RoA) with Net NPAs controlled at just 0.56% .

In this deep dive, we are going to look under the hood of this financial refinery. We will explore how they make money, why their “diversified wheel” strategy makes them resilient to shocks, and why they might just be the most important financial institution you haven’t looked closely at yet.

Part 2: The Deep Dive – The Hidden Alpha

If the “Amul” analogy explains what Northern Arc does (aggregating the fragmented), this deep dive explains why they will win.

Most investors see a lender. A few see a platform. Almost no one sees the data engine hidden underneath.

1. The “Hidden” Flywheel: The Data-Debt Cycle

Northern Arc doesn’t just lend money; they underwrite the originator’s underwriting. Unlike traditional NBFCs which operate on a linear model (Lend $\rightarrow$ Collect), Northern Arc operates on a circular platform model.

The Mechanism is simple but compounding:

It starts with Aggregation. Small partners (MFIs) plug into the Nimbus platform to access capital. This gives Northern Arc granular loan data that big banks never see.

This data feeds the Intelligence layer. Their Nu Score algorithm processes millions of repayment points, allowing them to price “thin-file” risk with higher accuracy than any competitor.

The result is Risk Reduction . Better data leads to superior asset quality (~1.15% GNPA vs Industry Avg). Because the book is clean, global giants (like Warburg) trust them with cheaper debt capital. This cheaper capital fuels Scale , which generates more data, making the system smarter with every rupee lent.

The Punchline: Banks see a borrower; Northern Arc sees a pattern .

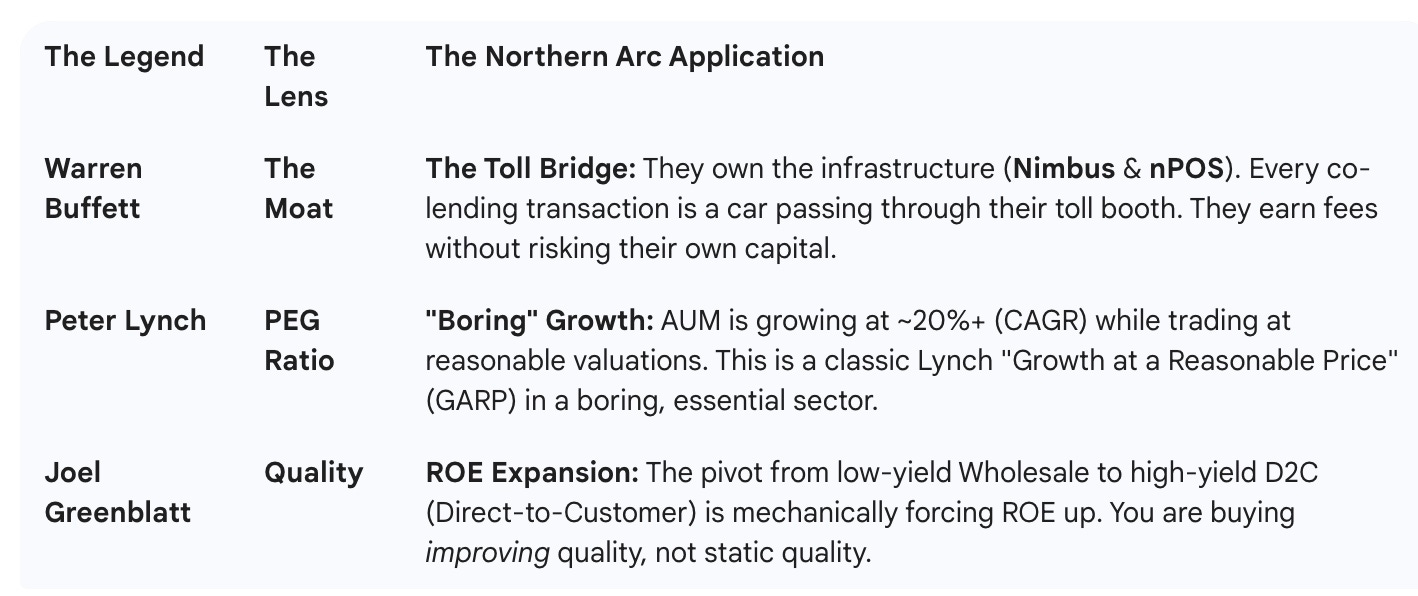

2. The Legends’ Lens: Valuation Frameworks

If we stress-test this thesis through the eyes of investing giants, the picture changes.

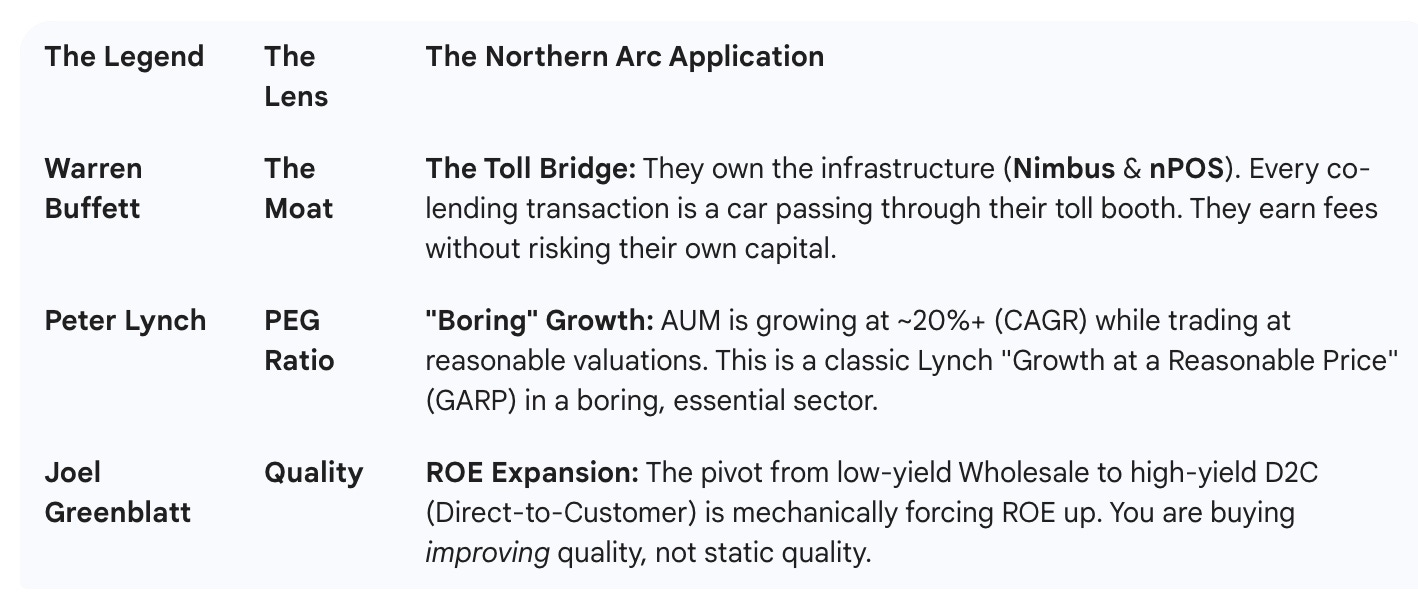

The Warren Buffett View (The Toll Bridge)

Buffett loves infrastructure. Northern Arc owns the toll booth (Nimbus & nPOS). Every co-lending transaction between a bank and a partner is a car passing through their toll booth. They earn fees on the flow without always risking their own capital on the loan.

The Peter Lynch View (GARP)

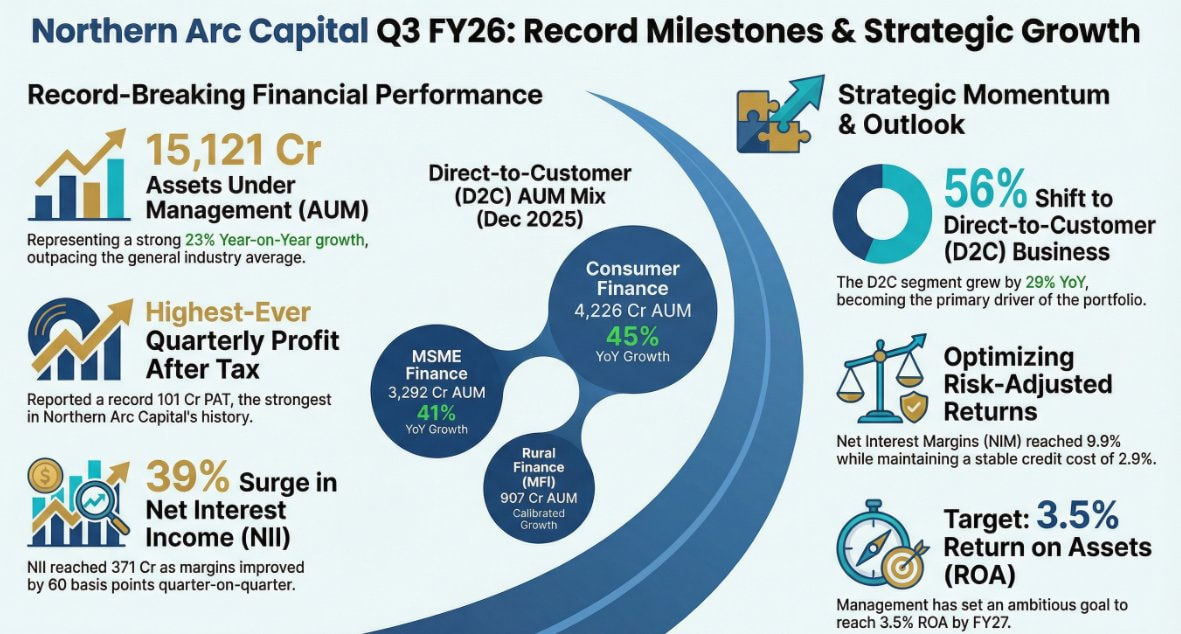

Lynch loved “boring” growth. Northern Arc is growing AUM at 20%+ while trading at ~1.2x Book. It fits the classic Lynch setup: a boring, essential business (Credit) with a misunderstood growth story and a “Growth at a Reasonable Price” valuation.

The Joel Greenblatt View (Quality)

Greenblatt focuses on capital efficiency. The company is pivoting from low-yield Wholesale lending to high-yield D2C (Direct-to-Customer). This pivot is mechanically forcing ROE Expansion (targeting 17.5%). You are buying improving quality, not static quality.

3. The Alpha: The 2025 Regulatory “Sword”

This is the insight 99% of retail investors will miss.

The RBI’s Co-Lending Directions (2025) introduce a game-changing rule: “Synchronised NPA.”

This mandates that if one partner in a co-lending pair marks a borrower as NPA, the other must automatically do the same immediately. This eliminates the “sovereignty” over asset quality—a partner’s error becomes Northern Arc’s headache.

Why is this good?

It acts as a survival filter. It will kill “lazy” aggregators who rely on manual reporting. Only tech-first platforms like Northern Arc, which integrate real-time via APIs, can survive this compliance burden. The moat just got wider.

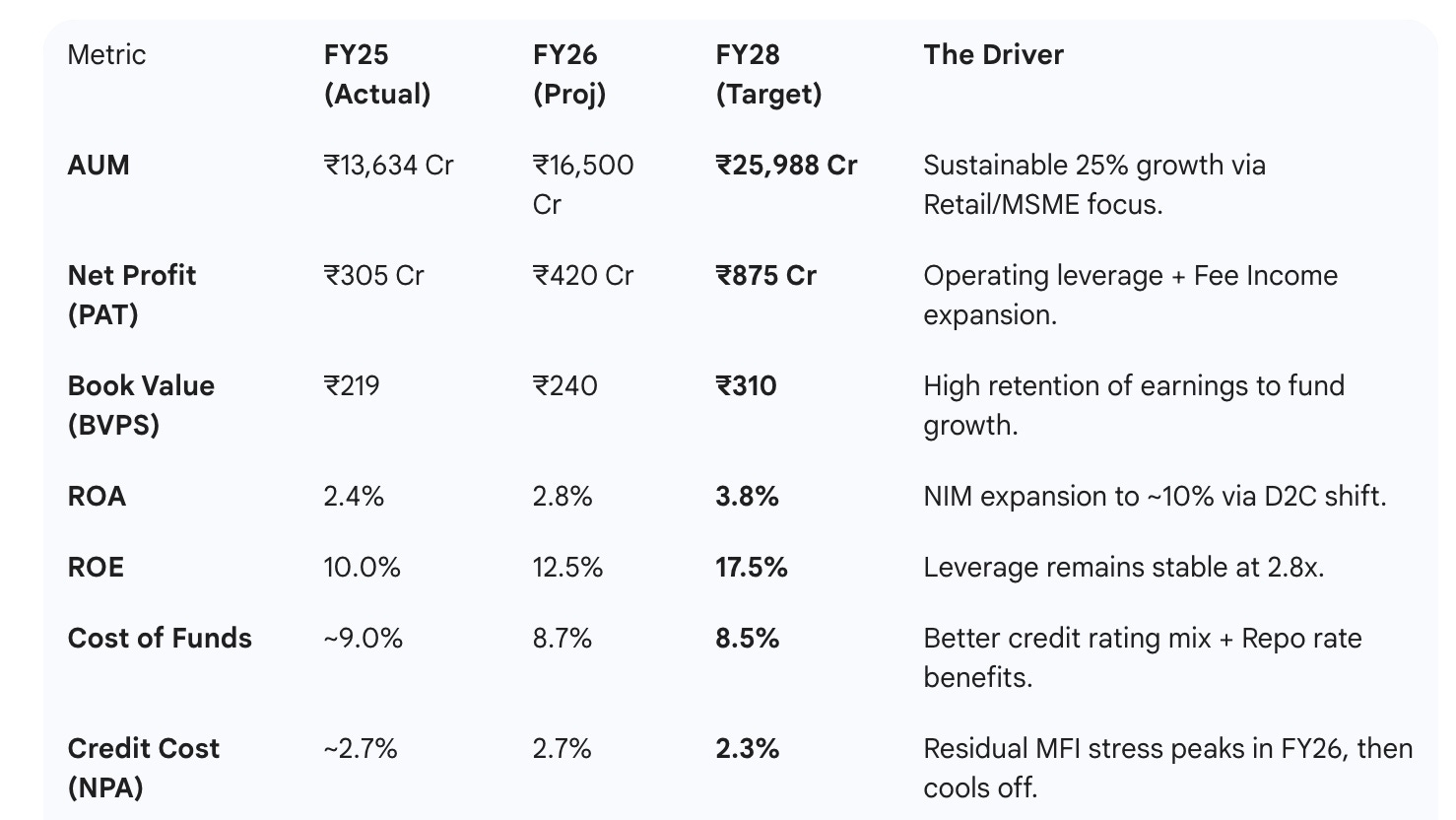

4. Projections: The Path to ₹875 Cr PAT

We don’t need to guess. Management has laid out a clear roadmap to FY28. The driver is the D2C Mix shifting to >70%, which expands margins without needing more equity.

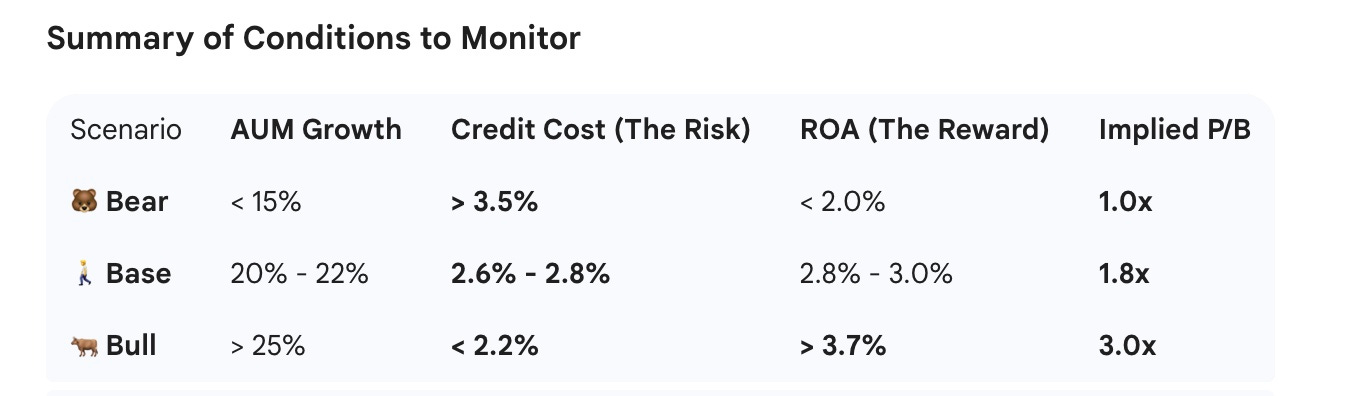

The Scenario Framework: Bull, Bear, & Base

We do not predict the future; we price it. Here are the three distinct paths for Northern Arc, defined by specific financial conditions that you can track quarterly.

The Bear Case: “The MFI Trap” (Probability: 20%)

The Bear Case: “The MFI Trap” (Probability: 20%)

The Thesis Breaks. Rural stress deepens, and the “Partner Model” backfires as contagion spreads from smaller MFIs to Northern Arc’s books.

- The Condition (Trigger):

- Credit Costs > 3.5%: The “Nu Score” fails to predict defaults in a downcycle.

- Partner Failure: A Top 5 exposure partner faces insolvency or severe regulatory action.

- D2C Stalls: Retail mix stays below 50%, forcing reliance on low-margin wholesale lending.

- The Valuation: 0.8x - 1.0x Book Value (Stock trades at liquidation value).

The Base Case: “The Execution Play” (Probability: 60%)

The Base Case: “The Execution Play” (Probability: 60%)

Management Delivers. They hit their stated guidance. The pivot to retail continues, but at a measured pace. MFI stress lingers but is contained.

- The Condition (Trigger):

- AUM Growth: Consistent 20-22% (CAGR).

- ROA: Stabilizes at 2.8% - 3.0% .

- Credit Costs: Averages 2.5% - 2.7% (Management Guidance).

- The Valuation: 1.8x Book Value (Re-rates to industry average for 15% ROE).

The Bull Case: “The Platform Re-rating” (Probability: 20%)

The Bull Case: “The Platform Re-rating” (Probability: 20%)

The “Amul” Moment. The platform (Nimbus) becomes the primary driver. Fee income explodes, decoupling profits from capital requirements.

- The Condition (Trigger):

- ROA > 3.5%: Driven by high-margin fee income (not just interest income).

- D2C Mix > 70%: Successful conquest of the “New-to-Credit” MSME/Consumer market.

- Credit Costs < 2.0%: Data advantage proves structural, even as they scale.

- The Valuation: 3.0x Book Value (Market prices them as a Fintech/Platform, not a Lender).

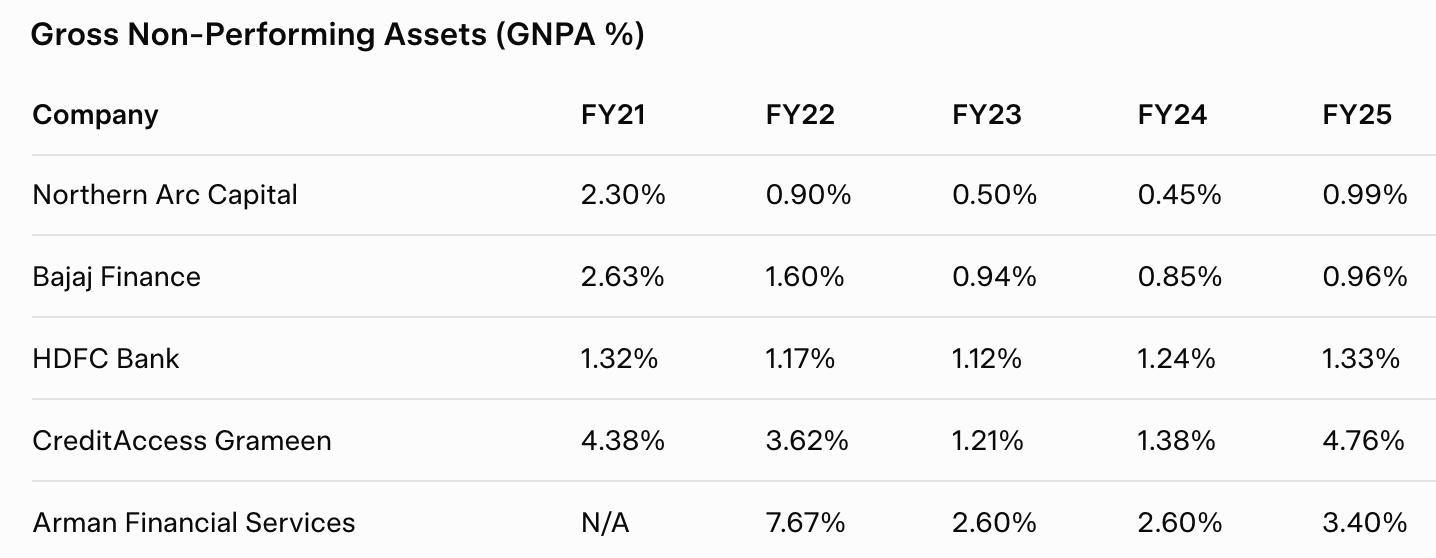

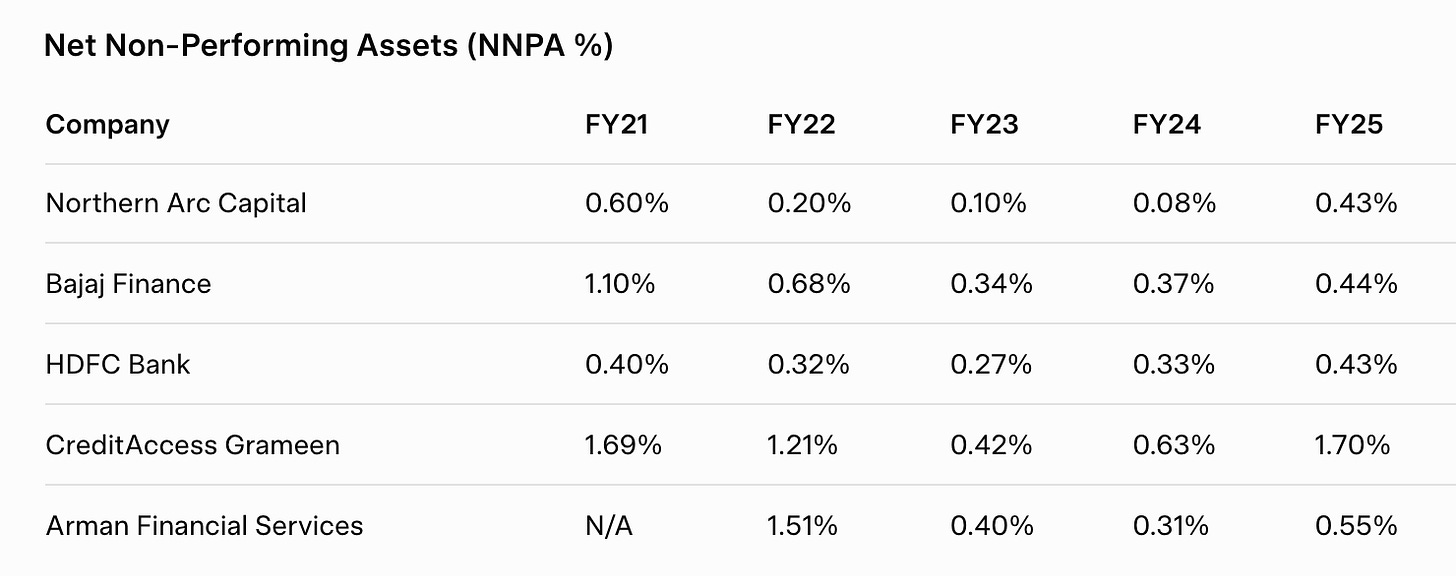

The Scorecard: Beating the Giants

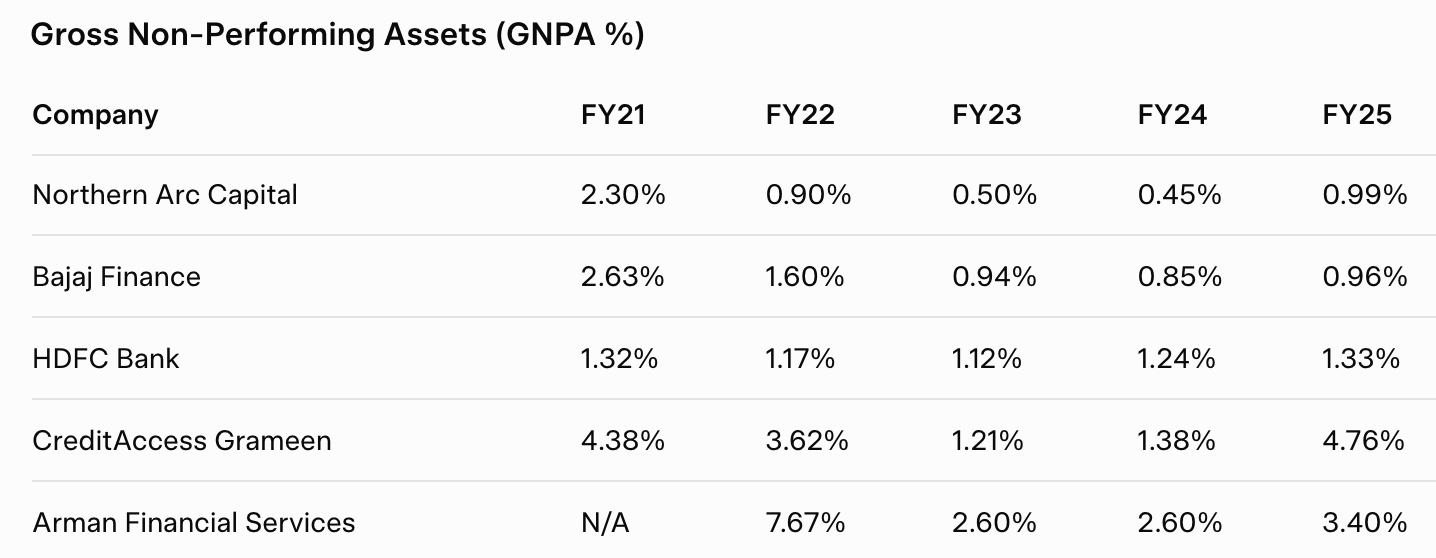

It is easy to say you have “better technology.” It is harder to prove it. The ultimate proof of a lender’s quality is their Gross NPA (Bad Loans).

If Northern Arc’s “Cold Chain” model truly works, their loan book should be cleaner than the industry average. But it isn’t just cleaner than the average; it is cleaner than the giants .

Compare Northern Arc’s asset quality (GNPA) against the heavyweights of Indian Finance over the last few years:

- CreditAccess/Arman (Pure MFI Peers): Often range between 2% – 4% due to sector volatility.

- HDFC Bank (The Banking Gold Standard): Typically maintains a GNPA of ~1.2% .

- Bajaj Finance (The Consumer King): Operates in the 0.8% – 1.2% range.

Northern Arc? In FY24, their Gross NPA was just 0.45% . Even in FY25, amidst a sector-wide Microfinance crisis, they held it at 0.93% —still lower than what most banks aspire to in a good year.

This is the “Moneyball” moment. Northern Arc is lending to the same “risky” rural borrowers as the MFI players, but by using their 15-year data advantage to filter the intake, they are producing asset quality that beats HDFC Bank. They aren’t just managing risk; they are engineering it out of the system

5. The Verdict

Investing in Northern Arc is a bet on the financialization of the invisible Indian.

You are effectively buying a Data Company disguised as a Lender.

- The Floor: If the pivot struggles, you own a growing lender at ~1.2x Book. (Capital Protection)

- The Ceiling: If they hit the ₹875 Cr PAT target, you own a high-ROE Fintech platform. (Asymmetric Reward)

Heads, you win 3x. Tails, you don’t lose much.

Disclaimer

- I am not a SEBI-registered research analyst or investment advisor.

- I hold a long position in Northern Arc and therefore have a vested interest.

- Nothing here is investment advice, a recommendation, or a solicitation to buy/sell securities.

- All facts are from the company’s official filings and earnings call dated 13–14 November 2025.

- Do your own research. Your capital, your responsibility.