Company Overview:

Northern Arc Capital Limited is a diversified financial services company focused on providing credit solutions to underserved households and businesses in India.

Established 15 years ago, the company aims to facilitate the flow of credit from capital providers to users in a reliable and responsible manner.

Management Insights

- Ashish Mehrotra (MD & CEO) emphasized the company’s mission to impact millions of lives by enabling access to finance.

- The management team is committed to building a culture of collaboration, innovation, integrity, and transparency.

- The company has successfully facilitated credit financing of over INR 1.8 trillion, impacting over 101 million lives since inception.

Business Model:

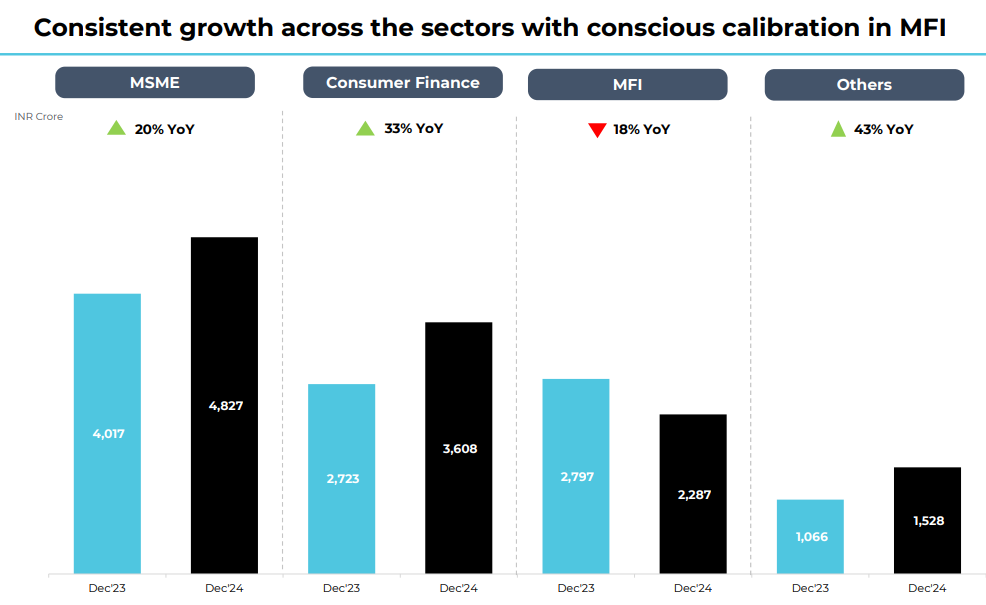

- Focused on six key sectors: MSME, Microfinance, Consumer Finance, Vehicle Finance, Affordable Housing, and Agricultural Supply Chain.

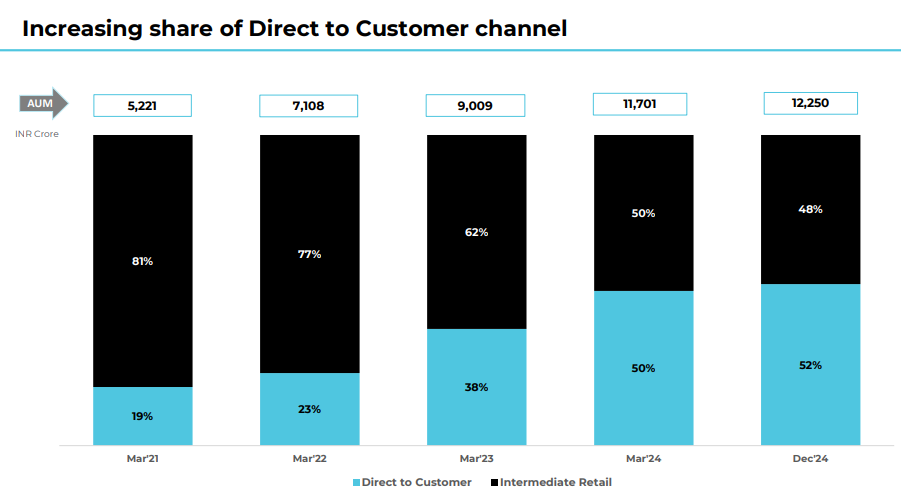

- Utilizes a multi-channel strategy to provide credit solutions directly and through intermediary partners.

- Pioneered innovative products such as PERSEC (Perpetual Securitization) and MOSEC (Multi-Originator Securitization).

Financial Performance (Q1FY25):

- Assets Under Management (AUM) reached INR 11,869 crores, reflecting a 32% year-on-year growth.

- Net Revenue was INR 297 crores, marking a 40% year-on-year growth.

- Pre-Provisioning Operating Profit (PPoP) increased by 43% year-on-year, reaching INR 174 crores.

- PAT for the quarter saw a 43% year-on-year increase, reaching INR 93 crores.

Risk Management:

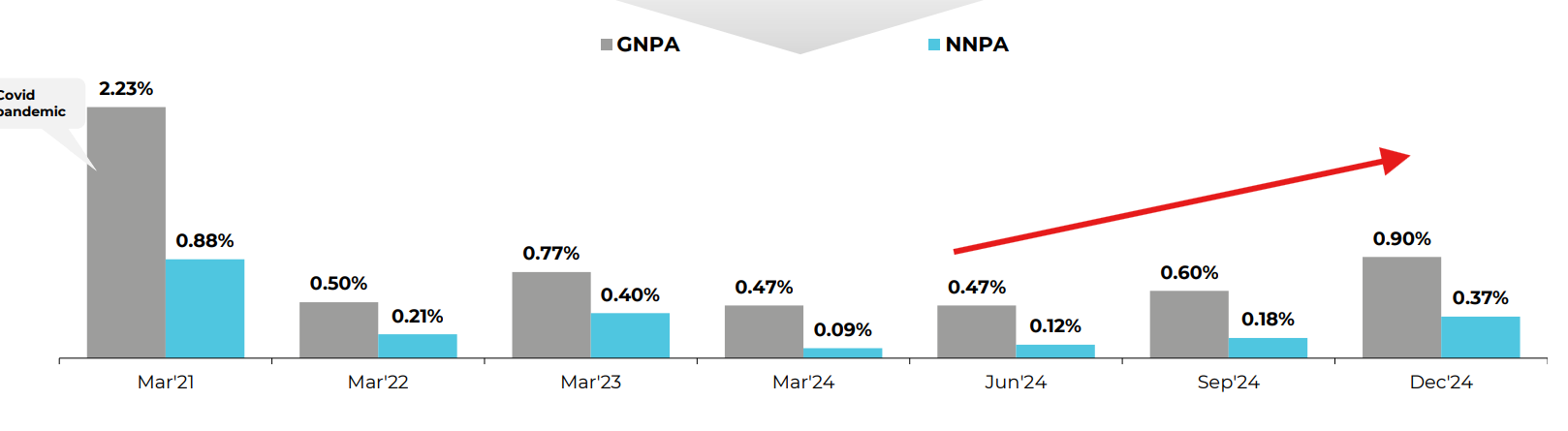

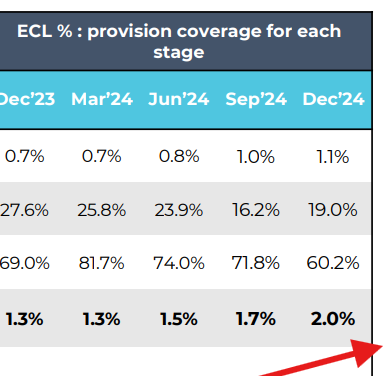

- Gross NPA at 0.47% and Net NPA at 0.12%, indicating strong asset quality.

- Proactive approach to credit costs, with a focus on borrower selection and strengthening collection processes.

- Increased provisions anticipating potential stress in the portfolio, especially in the microfinance sector.

Market Dynamics:

- The MSME sector is growing at 29% year-on-year, with increasing credit demand despite observed delinquency trends.

- Microfinance remains a focus area, but there are concerns about over-leveraging among borrowers due to relaxed RBI norms.

- Consumer Finance is driven by rising disposable incomes and digital lending innovations, with a shift towards cash flow assessments for loan approvals.

Competitive Advantages:

- Domain Expertise: Deep understanding of the credit needs of underserved households and businesses.

- Network Effect: Strong distribution network with 340+ branches, 50+ retail lending partners, and 1,000+ investor partners.

- Technology Infrastructure: Proprietary platforms like Nimbus and Nimbus Partner Origination System (nPOS) facilitate seamless credit flow and underwriting.

Future Outlook:

- Management expects to maintain growth rates in line with historical performance, targeting 30%+ CAGR.

- Anticipates a pickup in credit demand in H2 due to seasonal factors and ongoing economic recovery.

- Plans to leverage the INR 500 crores raised from the IPO to enhance growth and profitability.

Headwinds and Challenges:

- Potential increase in delinquencies in microfinance due to over-leveraging and socio-political disruptions in certain regions.

- Management remains cautious about macroeconomic factors affecting borrower repayment capabilities.

Strategic Initiatives:

- Focus on maintaining a diversified portfolio to navigate sector-specific challenges.

- Emphasis on continuous improvement in risk management frameworks and collection processes.

- Introduction of new funds and investment opportunities through the Fund Management Business, which has run 10 funds with a strong performance record.

From the latest con-call

IPO (Price action)

Issue price - 263

Open price - 350

Current price - 251

Disclaimer- Invested and biased , will be adding more at the current levels.

Not a buy/sell recommendation.