Hi All,

Any ADD announcement happened? Where to check these details.

Please advise.

Hi All,

Any ADD announcement happened? Where to check these details.

Please advise.

HDFC Sec initiates coverage on NOCIL

CFO and other Key managerial personnel SOLD shares recently…Any views on this…Is there any info which we need to worry on this sale…Is management forsee any problems …thats why they SOLD…Any pointers here

The anti-dumping duty imposed on the import of Aniline from China. Aniline is a major raw material for them.

When this happened… source please

Sale of ESOPs by senior employees is generally a routine occurrence and nothing much to write about. It is not the same as sale by Promoters.

Here is the official link.

https://www.cbic.gov.in/resources//htdocs-cbec/customs/cs-act/notifications/notfns-2021/cs-add2021/csadd08-2021.pdf;jsessionid=2F72419B6E4681AEC77325EEB16A4835

NOCIL Q3FY21 Notes.pdf (341.6 KB)

Nocil

Concall highlights

Operating highlights

Demand was challenging in Q1, improving from Jul. Production is being ramping up m/m and utilisation crossed pre-Covid levels in Q3.

Value added products contributed 25% to the total business.

Conversion cost declined to 28%, from 35% in Q2 FY20. The company targets to bring this down to 25% with greater utilisation.

Sourcing issues led to prices of some raw materials rising substantially in the past few months. Further, due to the demand-supply gap, price rises could not be passed on to customers in 9M FY21. The company raised prices in Jan’21 and in Apr’21. Ahead, it expects better margins.

Utilisation

Utilisation touched 85% in Q4 on the present 90,000-ton capacity.

In Q4 FY21m the company commissioned the second expansion phase. Now, it has manufacturing capacity of 110,000 tons. It expects optimum utilisation (95%) by Sep’23.

Market share and industry highlights

Industry data show that demand has risen, post-Jul’20, and is picking up continuously.

The company expects more sales volumes in coming months, in exports and domestically.

The government has imposed duty on import of tyres. This would benefit domestic tyre manufacturers and result in greater utilisation.

Global rubber consumption slipped 7% in CY20 (vs. down ~15% in H1 CY20). Domestic rubber consumption declined 5% in CY20. On the other hand, Nocil recorded 5% growth in CY20. It expects to have gained some market share from competitors.

Monthly rubber consumption has returned to early 2019 levels.

The auto industry is experiencing strong demand recovery in OEMs and the replacement market, and expects the growth momentum to continue in coming quarters.

Government measures (AtamaNirbhar, Bharat Abhiyan) would benefit domestic auto and auto-ancillary manufacturers, and reduce dependence on other countries.

Exports

Management says exports are doing well. It said it is receiving more enquiries and orders from overseas clients.

The proportion of exports rose to 35% in FY21 (vs. 30% the year prior), which the company expects to change to 60:40 in the next 3-4 years.

Ahead, the company expects strong export demand as global manufacturers are shifting sourcing from China to sourcing from India

It is receiving more orders and enquiries from international customers.

The share of specialty products is higher in exports and the company expects higher margins.

Capex

The phase-II expansion would become operational in Q4 FY21.

In the Q2 concall, the company had talked about optimum utilisation in 4-4.5 years. This has now been revised to 3–3.5 years. In the Q3 concall, it again revised this, and talk of optimum utilisation by Sep’23 considering better demand domestically and in exports. The company maintained that guidance in the Q4 call also.

It is not looking at any capex in the medium term and will focus on volumes and market share.

It is working on some products and projects, and will come out with more details after finalising them.

Guidance

Management has not given any “guidance” about the FY22 performance but expects Q1 FY22 to be better than Q1 FY21.

It expects the margin to improve in coming quarters owing to better absorption of costs due to greater utilisation. Management said that absolute EBITDA would improve once the market stabilises.

It guided to maintaining the gross margin at 50% in the long term and expects an EBITDA-margin expansion at peak utilisation.

It said it would focus on exports and on increasing the proportion of specialty products.

It is seeing a gradual uptrend in volumes and expects the performance to improve in coming quarters.

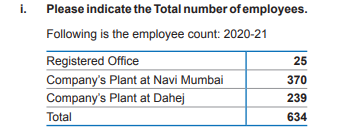

Excluding the employees at its two plants (mostly factory workers), NOCIL has just 25 white-collared employees. Impressive !

Interesting development on the appointment of Mr.V.R.Gupte.

c6ff0fe6-8fe1-482c-8a3f-89f8122074b4.pdf (bseindia.com)

I too had felt that his appointment as Independent Director was quite odd when I first read it. Though there are no doubts on his personal integrity and even on NOCIL’s governance standards, given his long association with the company this was quite avoidable as matter of principle. Will be interesting to see how the institutions vote.

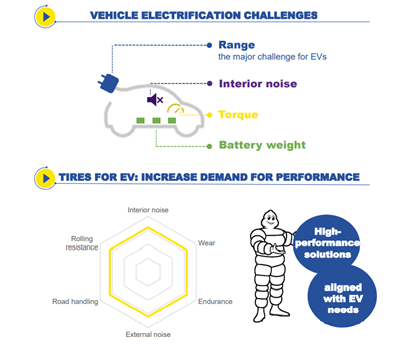

NOCIL is as much an auto stock as it is a chemical stock, since a large part of its output goes into making tyres. This makes it vulnerable to the ups & downs of the automobile industry. Given that the auto sector is on the cusp of a major change due to the arrival of EVs, one needs to understand what impact if any the EV revolution will have on NOCIL.

On the face of it, there seems to be not much. Though many parts of the conventional (ICE) vehicle are not required in an EV, tyres will obviously continue to exist. However, an EV tyre is different from an ICE tyre due to different characteristics of the two vehicle types.

Range anxiety is a key concern in an EV and tyres can directly impact vehicle range. An EV is considerably heavier and silent than its comparable ICE counterpart. EV tyres are therefore required to have lower rolling resistance, much lower tyre noise and high torque resistance than conventional tyres to maintain reasonable tyre life. However, technically these requirements are self- contradictory, making it more challenging to manufacture such tyres. Many OEMs choose an optimal combination of these characteristics as suited to their specific vehicle attributes, leading to a trend of customized tyres. Tyre makers classify EV tyres at the upper end of the sophistication spectrum along with “high performance tyres” and the like.

Source: Michelin Investor Presentation

Due to the EV’s heavy weight, it is said tyres may wear out faster in an EV than an ICE vehicle. A faster tyre replacement cycle for an EV is an obvious long-term positive for NOCIL. It appears (but I could not confirm this with certainty) the EV demand for ‘stronger’ tyres could also translate into a more complex or sophisticated rubber chemical requirement, leading to more of higher margin or premium products for NOCIL. I do understand that EV tyres are more expensive than normal tyres.

On the other hand, as part of the larger trend towards sustainability and more in sync with the EV theme, OEMs are working towards making tyres from ‘sustainable’ materials rather than chemical compounds. It is not clear how this will impact rubber chemicals. There is also a trend towards getting rid of the spare tyre altogether, which means a direct reduction of 20% in OEM tyre demand.

Please do share any other inputs you have on how EVs will impact NOCIL.

(Disc.: Invested)

Just adding some more points to the impact of ev in tyres . However didn’t get any specific details about how chemical structure/usage changes in these tyres . NOCIL as a pure cyclical play will reach full capacity by around 2023 and that time around I will start turn cautious

I have a 4 year old position in NOCIL. The one thing I find most important to track is how are the competitors doing esp. China Sunshine. China_Sunsine_Chemical_Holdings_Ltd_-_Positive_ASP_trends_to_drive_strong_earnings_growth-30-Sept-2021.pdf (315.7 KB)

I have attached a research report for China Sunsine dtd 30 sept 21.

You can see ASP of rubber chemicals is again on increasing trend , which bodes really well for NOCIL.

@Chandragupta Recent concall, analyst asked how EV will impact tyres and management indicates there is no dependence in fact higher ebita as EV tyres require more rubber chemicals. Both natural and synthetic rubber uses same rubber chemicals.

other points

No announcement on capacity expansion coming from other companies except china sunshine

Higher raw material cost, china supply chain constraints, logistics costs etc will have impact on this quarter and cannot be predicted

volume growth guidance intact and in conservative side. margin down due to because of high inventory in q1 . Price hike will be there for spot customers due to raw material cost. Spot market is 40%

utilization is 70%. full utilization in next 2 years intact

Q3 FY22 concall

Notes from AR - FY - 21-22 iro NOCIL Ltd -

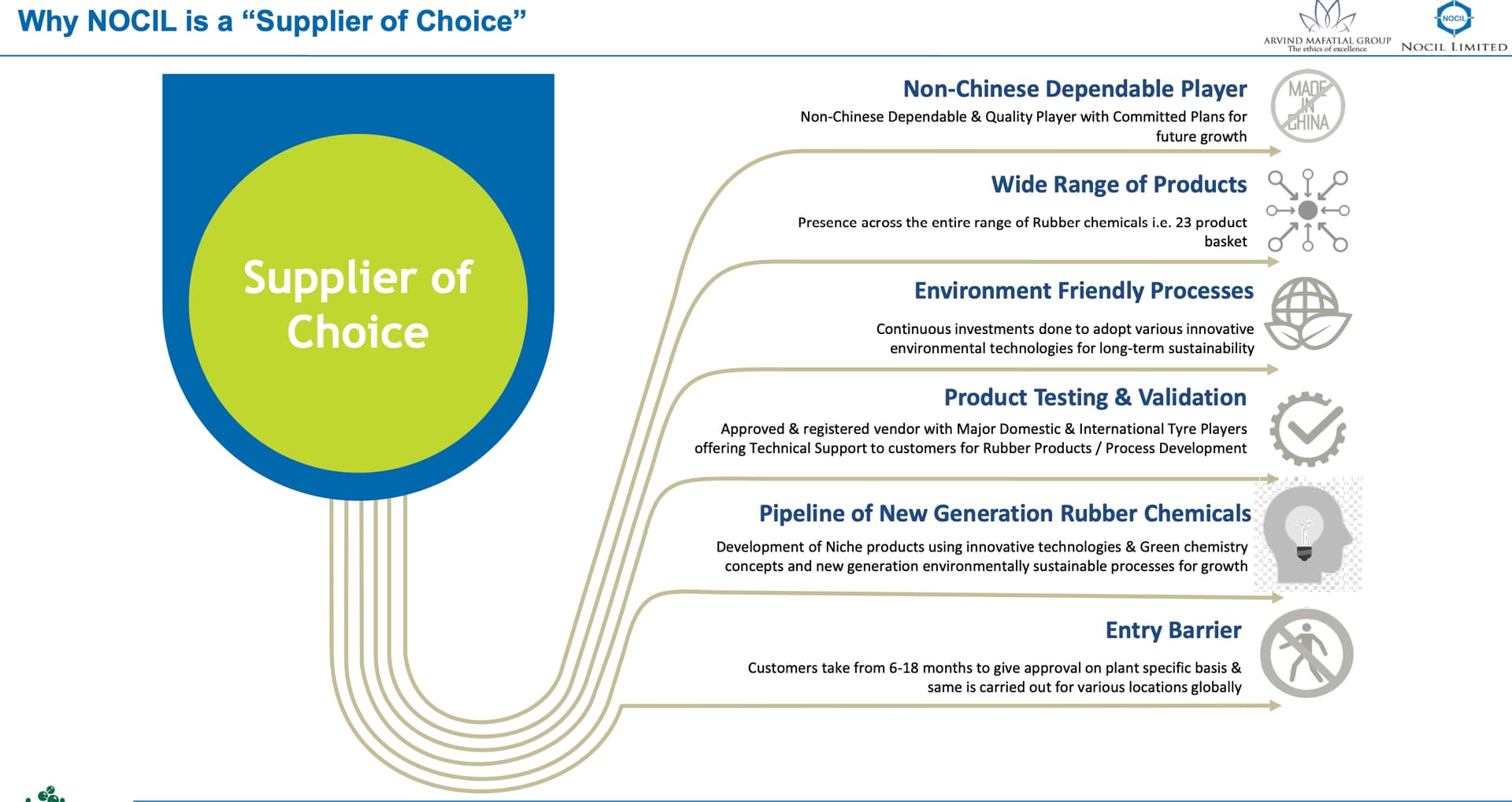

Company is largest Indian rubber chemical manufacturer with broad customer base across 40 countries. Company is a part of esteemed Arvind Mafatlal group. Company strives to continuously improve processes, efficiencies, quality, pricing and environmental standards.

Company has over 40 yrs experience in the rubber chemicals industry. Has strong position in high value added products. Exceptional R&D capabilities lead to significant reduction in production costs. As the business is scaling up, operating leverage is kicking in.

End user industries - Tyres and Tubes, moulded components for vehicles, industrial belts, gloves and other latex applications, hoses and footwear. Company produces 20+ variety of rubber chemicals.

Last 8 yrs performance highlights -

Sales growth - 8 pc CAGR

EBITDA growth - 26 pc CAGR

Dividend payouts - 30 pc of PAT for last 5 yrs

Company is witnessing clear echo for a China plus one strategy wherein global tyre majors are considering de-risking their value chains away from single county dependence. India and NOCIL stands to benefit from this trend.

Company’s plants -

Mumbai plant - set up in 1976. Has state of the art technology to make entire range of rubber chemicals for tyre and other rubber products.

Dahej plant - started production in 2013. Is located at synergistically important proximity to petrochemicals industry and Hazaria port. Has fully automated process plant developed completely with in house technology.

Over and above China +1, increased environmental compliances levied by the Chinese govt is increasing the cost of production in China. This is creating a level playing field for NOCIL as the company was always complying with these norms.

Company’s major product lines -

Anti - Degradants / Anti - oxidants - Deter ageing and inhibit degradation of rubber compounds due to oxygen attack on rubber compounds

Accelerators - Increase the speed of vulcanisation. Allow vulcanisation to proceed at lower temperatures with greater efficiencies

Other applications - Pre-vulcanisation inhibition, post vulcanisation stabilisation, improving cross links in rubber products.

Disc: initiated a tracking position. Biased.

Q 4 Conf Call updates:

Planning to achieve 100 % utilization before Sept 2023. Right now 70 to 75% capacity utilization

Planning to debottleneck existing capacity with small capex

Product mix also helped to increase the margins in current Qtr

Price hike obviously helped top line, price hike is as per same lines of other competitors.

Current export 35 % of Total

6.There is long term plan on Capex…not yet decided the numbers and which products

Please add if I missed any.

Q4FY22 Concall

Some back of envelope calculations : (can be abysmally wrong ![]() )

)

FY22 revenue is 1571cr. at 75% utilisation. Optimistically, By FY24 should reach roughly 1800-2000cr revenues.

or at current realisation of 1.8-1.9L/tonne for 1L tonne capacity (90% by H1FY24) realisation comes again around 1800-1900cr.

If OPM is 20% (due to 25% value added products); Net profit could be between 210-245cr. translating to an EPS of 12.5-16.5. At current PE of 24 share price could be between 300-390.

Margins may improve further if crude oil cools down or share of value add chemicals increases.

Disclosure: invested

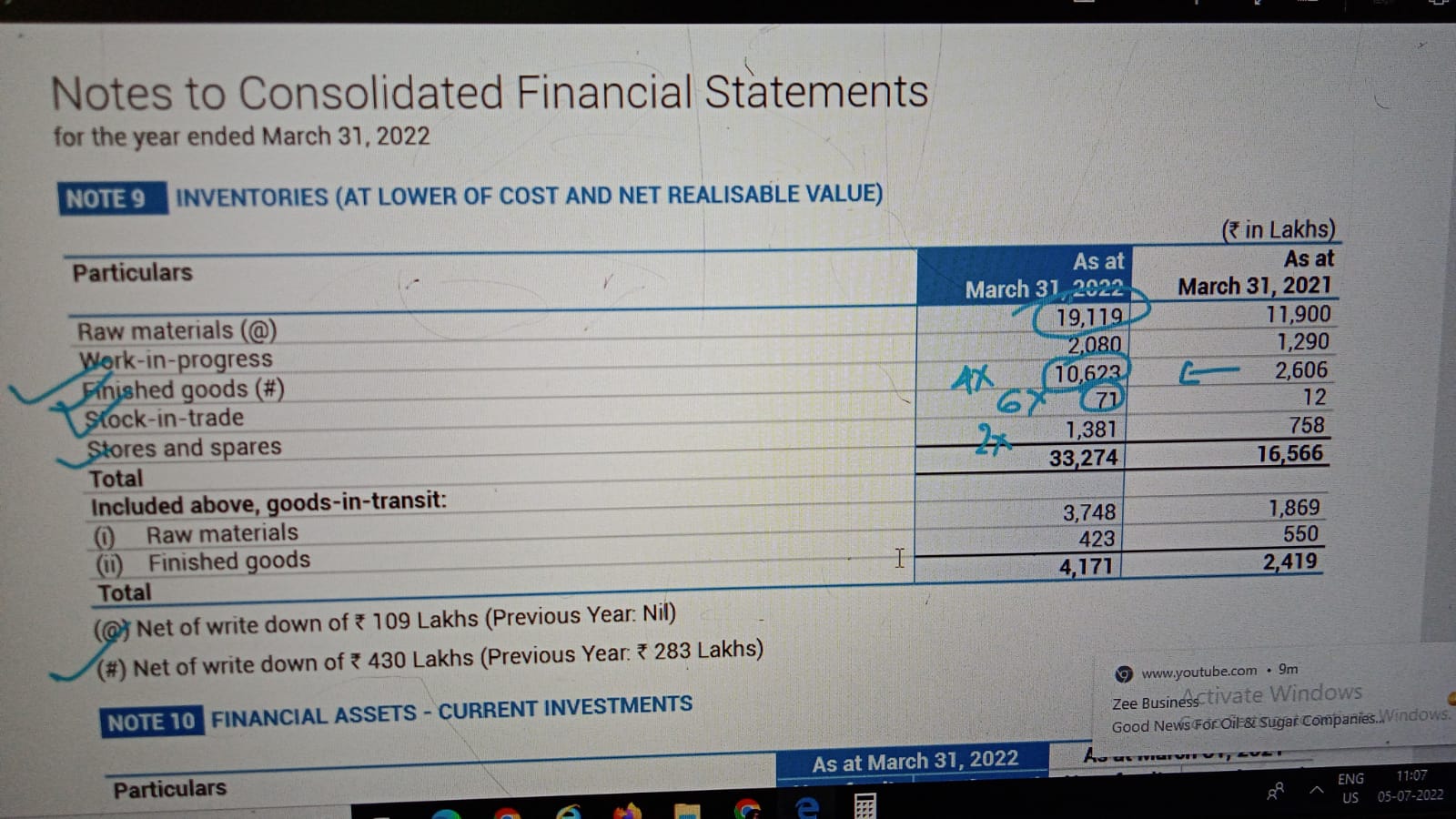

Looking at the pattern of sales, the sales seems to be some kind of sudden gain, may be due to supply chain disruption from China, huge inventory has been piled up as per Annual report will they get benefit out of that from Q1 onwards or China will bounce back with cheap oil from Russia & dump cheap commodity type rubber chemicals to others nations, if this situation happens in coming Qtr then big set back for Nocil, if China doesn’t come back & crude remain elevated then Nocil can hit upper circuit bcoz of gaining inventory gain, any one can put some light on Sunshine in coming Qtr via concall or any data ,