Notes from NOCIL Q1 FY23 concall:

-

Capacity utilization was 75%. Realization was flat.

-

Expecting 10% volume growth for H1 FY23 (this implies a 0-4% volume growth in Q2 as per my calculations)

-

Optimum capacity utilization target of Sep 23 will get extended by 3 to 6 months due to moderation in demand.

-

Debottlenecking exercise will take 12 months, which will satisfy demand for another 1 to 2 years. Capex for this is very small. How much the capacity will be enhanced due to this is not revealed, but one can take around 10 - 12 % per annum growth and calculate.

-

During the quarter, volume growth was largely from domestic business as there have been changes in the geographical dynamics. Exports are Rs.165 crores for the quarter, lower this quarter but overall, they are increasing for us. Our normal domestic market share is 42-43 %.

-

Following HS Codes for rubber chemicals is misleading as the code may contain several items which we are not manufacturing, and some of our items may be in other HS Codes.

-

Dahej land utilization is around 50-60% and there is scope for brownfield expansion. Navi Mumbai land is almost 100% utilized.

-

In a declining RM pricing scenario, so far delta has been maintained by the players, but need to see how it goes along.

-

From Oct - Nov 20, we have seen a shift in the strategy of Chinese manufacturers. They are adjusting their prices according to the RM price movements (I think what is implied is that there is no rampant dumping by the Chinese players).

-

New capacities are not coming up other than China Sunsine which is already known.

-

Government is now-a-days rejecting most of the anti-dumping duty recommendations.

-

Rubber chemicals global demand is 10.50 lac TPA i.e., 3.5% of global rubber consumption.

-

Anti-dumping duty was Rs.45 crores per annum in FY17 to FY19 . You can exclude that while calculating the EBIDTA margin.

-

One of the key things export customers are looking for is how assured is the supply i.e., commitment to delivery schedules.

-

About 25% revenue is coming from value added / speciality chemicals and we intend to maintain that. In overall scheme if things, this market is may be 5% of the overall market. As against that we are at 25%. So, to grow beyond this will be difficult.

-

Among non-Chinese manufacturers, we are World no 1 when it comes to capacities, all around product portfolio and self-sufficiency of intermediates which is a key aspect in this business. Two major non-Chinese players are - Lanxess which has dependency on China for their intermediates and Eastman (sold to One Rock Capital) which is a single product portfolio.

-

If US removes anti-dumping duty on Chinese rubber chemicals, at the most we may grow slower than at present. But there will be no loss of existing volumes.

-

Some new products are in the pipeline.

-

Europe demand is 12 % of the world market and supply is 15% for Europe incorporated entities. Europe production may be around 10% (just a guess).

Disc: Invested.

13 Likes

I guess nocil is getting inventory gain, as the stocking was visible during feb & march , then commodities sudden rise while they were immune to that, may be silent on China side due to covid & stock pile of inventory give them a good topline gain in the past 2 qtr, Sunshine is coming with more volume that may dump in USA/EU/Asia pacific so headwind is visible in my opinion,

Disc:- invested

2 Likes

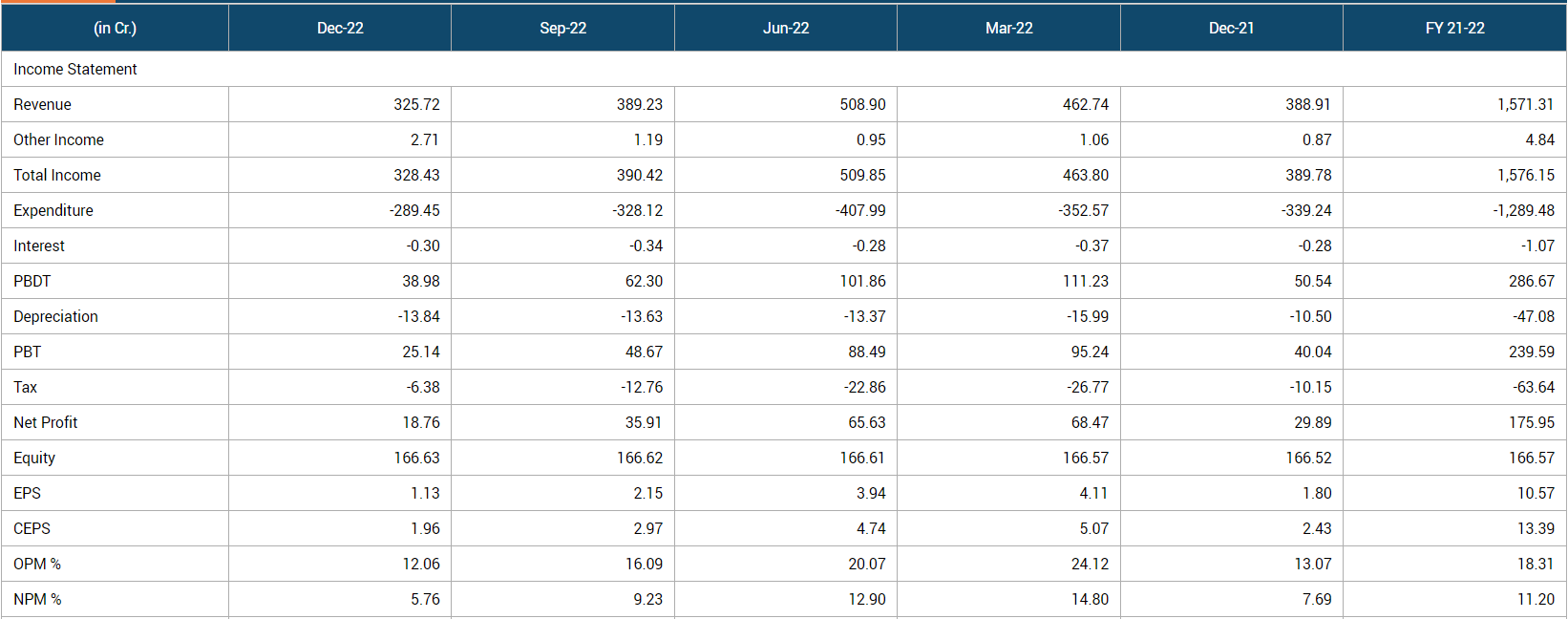

Q3 FY2023 quarter results have been disappointing. Total income dropped from 390.09 crores to 327.93 crores QoQ. Net profit took a beating, from 35.73 crores to Rs. 18.62 crores QoQ. Can someone with expertise in this domain, comment on the headwinds being faced by NOCIL and if we can expect better quarters going ahead?

Also, during July 2022, they had said that the forecast for revenue growth was set to grow at 6.5% p.a. on average during the next 3 years, compared to a 12% growth forecast for the Chemicals industry in India. Can anyone provide insights into why that is, given that NOCIL is the largest player in India in rubber chemicals.

2 Likes

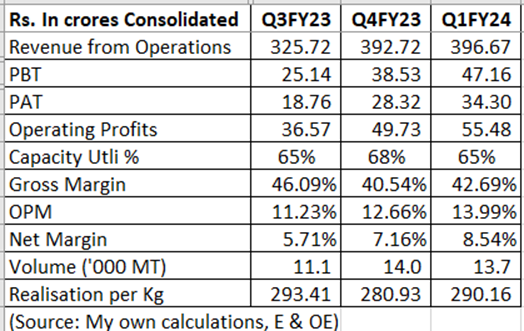

The Q1 FY24 results looked disastrous on a YoY basis. Moreover, in the concall the newly appointed MD VS Anand said there has been aggressive Chinese dumping, and it has in fact intensified in July. I am surprised that despite this, the stock has not fallen since the results. This may be because sequential revenues, operating margins and profits have risen for two consecutive quarters, volumes have inched up and realizations have remained stable.

Capacity utilization in Q1 was 65 %, so there is ample scope for growth without incurring any major capex. Even at current scale of operations (i.e., assuming no growth), the company should earn around Rs.150 crore of CFO per year. Debt is zero. Maintenance capex is around Rs. 30 crores. Cash in hand is more than Rs.200 crore and there should be a cash accretion of more than Rs.125 crore per year going ahead. This is assuming no growth.

Restrictions remain in place for tyre imports, though there is no complete ban. Tyre imports into India went up 15 % in FY23 (by value), but they don’t seem to be a major worry for tyre makers in India right now, going by their commentary. This augurs well for domestic tyre production, and consequently for NOCIL.

With no major capex on the horizon, zero debt and surplus cash, there is a lot of optionality in the company, either to increase the dividends / buyback or deploy funds for other initiatives. VS Anand took over as MD of NOCIL from 1st August 2023. A new chief always kindles hopes of injecting new life into the company. In reply to a question on what he would like to change at NOCIL, he said he would like to be bold and brave in international markets. I am not sure what this means, but I would be watching closely his strategic actions.

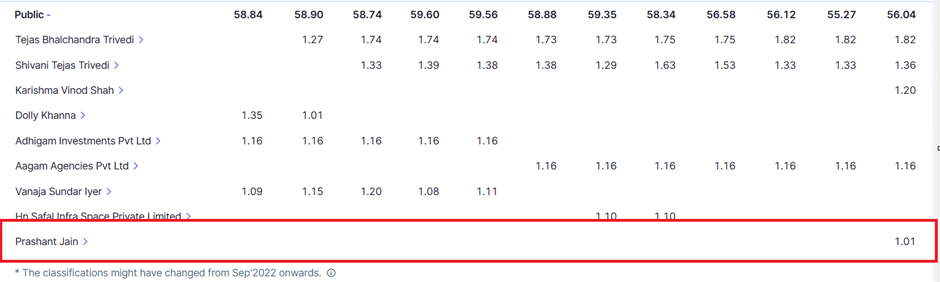

Finally, I notice that one Prashant Jain has taken a 1 % stake in the company last quarter. Not sure if it is the “same” Prashant Jain we all know, but he was also a “value” investor.

Based purely on price action, it seems to me the stock may just have bottomed out.

(Disc.: Invested. Not a recommendation)

12 Likes

China will disturb few more qtrs bcoz of their low domestic demand & dumping products in Asian countries & other places, but how much China is going to make losses in near term, so sales may come back but few qtrs is going to be disturbed or flat sales, may be the worst part mkt has already discounted,

It was a tough Q2 FY24 concall for NOCIL management as the analysts grilled the management for a stagnant quarter and lack of concrete plan of action for the future.

Some highlights:

-

On a sequential basis, the company had a marginal degrowth in volumes on a quarter-on-quarter basis. The volumes in the domestic market remained flattish, company experienced a decline in export volume. For the quarter volume degrowth is about 4% and selling price de-grew by 7.5%. So total revenue degrowth of 11.5 % Exports are more or less in the range of 30% to 35% of the volumes for the quarter and also for H1. Capacity utilization for Q2 was about 65 %

-

But on a YoY basis, the company has grown significantly in exports in Q2 because the low base has been corrected now because of additional volumes traction coming in from non-latex products. Domestic market - there is a small volume growth in single digit.

-

Exports break up - about roughly close to 20%, 25% would be in Europe, about 50% in Asia and 25 % is Americas. In terms of new capacities coming up, the management said we are not really hearing of significant expansions in these markets.

-

Due to the lack of domestic demand in China and the lukewarm demand in their predominant export market, there has been a significant influx of heavily discounted imports from China.

-

The latex part of revenues has come down due to latex demand going down. The management said we see that the non-latex part that comprises of the tire sector and the tire companies has been going up. So that has compensated for that part that has been going down.

-

Overall demand per se has come down.

-

Latex was 30% in the overall export basket earlier (post covid peak), that has trickled down to about 12% or thereabout now, whereas the non-latex which was earlier 70 is probably about 85, 88 or something like that today. Non-latex market is more sustainable.

-

Specialty percentage has dropped down. It’s below 15%. Latex is specialty.

-

Nothing to report on the capex for adjacencies, said the management.

-

Company looking at renewable power generation which will come next year.

-

In future, in the domestic market NOCIL already has a high market share. So, the growth will always come from plus or minus – more on the plus side of a few hundred basis points compared to the growth of the industry because they have a sizable market share already. Whereas the growth in the international markets, where it has a much lesser presence, would significantly be higher.

-

For Q3, the management said there have been some price corrections (i.e. improvement). But they would expect that if there is lower demand in China, pricing pressure cannot be ruled out. At least next quarter and a couple of quarters, volumes should trend slightly on the positive side.

Overall, the management blamed the global demand slowdown and Chinese dumping for the muted performance. But many analysts seemed unconvinced and grilled the management on various counts.

One analyst noted that the markets such as Indonesia, Vietnam, Thailand have started showing the improved demand. The demand has picked up there. Even if we see their July, August tire output data, that is up close to 15% on a Y-o-Y basis. And the September month also shows the increase in their ASPs, like average selling price of close to 23% with the commensurate increase in the aniline prices, which was close to 19%. Another one pointed out H1 of China Sunsine and H1 of this calendar year '23, they have shown some 10% volume growth. Even last year, their base was also very high. So, on that 90,000 tons of volume, their volume was close to 1 lakh tons. So, they have shown 10% growth. One analyst said our competitor have expanded the capacity recently but are operating at a low utilization (i.e. there is risk of further dumping). It was also pointed out China Sunsine are adding a 30,000-ton capacity, that could come by December end. But they are using it for their captive consumption. One analyst said why we are getting impacted with the demand slowdown in the industry. I would have understood it if we had a very high market share, like 40%, 50%. But since our starting positions in global markets are very low, then why is the demand slowdown impacting us so drastically? One analyst said U.S antidumping on Chinese rubber chemical is getting over next year but the management said they expect it to get extended. Also, it does not impact pricing though some volumes may be impacted if it does not happen.

Overall, things still look tough for the company. Positive triggers include improvement in China, improvement in US / Europe and improvement in latex demand in SE Asia. What I find disconcerting is any lack of proactive steps on the part of the management (so far) to utilize / return surplus cash or diversify into new revenue streams.

My views and position remain the same, as mentioned in the previous post.

11 Likes

I think I finally found the answer.

-

For Q4 FY24, volume increased 12 % Q-o-Q but selling price dropped by 6.5 %. Domestic volumes grew in high single digits while export volume growth was higher. Operating profit for Q4 was down from Rs.50 crore to Rs.45 crore.

-

Full year FY24 recorded a volume growth of 9 % in export segment while domestic was flattish, giving an overall volume growth of 2 %. Most of the growth was in non latex chemicals.

-

Margins declined but the situation has bottomed out, says the management.

-

Between FY22 and now, the latex market has degrown by 40 %. In the Q4 FY24 concall, one analyst noted that there is some improvement in this in the last one month.

-

Aggressive dumping from China and other markets continue. This will go on until domestic consumption in China picks up. Demand growth in key destinations such as US and Europe remains muted.

-

One analyst noted that the top three Chinese players are further adding capacity in accelerator as well as antioxidants.

Overall, things look grim, don’t they.

-

Meanwhile, work has begun on a Rs. 250 crore expansion at Dahej. Though overall capacity utilization is at just 65 %, the products that the company is planning to expand in here are running at peak capacity, hence the need to invest to capture further growth, says the management. The capacity will get operational in the second half of FY27.

-

Work on diversification into new chemistries is continuing, says the management but no further details are announced.

In the concall, one analyst noted that the molecules the industry uses have been as it is since past 50 - 60 years and nothing much has changed. Also in terms of the operational efficiencies through improvement in processes, most of the benefits have already been extracted. So the scope for incremental improvement is also limited. I wonder if this explains why almost nothing seems to change at NOCIL as well, not just in term of products and processes but thinking as well. As a debt free company in a capital-intensive business and an extremely efficiently run operation, I have often wondered why NOCIL cannot achieve more. The business remains hostage to what China does, with no efforts by the management to derisk or diversify. The Rs.250 crore expansion will not change this structural vulnerability to external factors.

The company is sitting on more than Rs.400 crore of cash and generates almost Rs.150 crore of FCF per year. If nothing else, annual cash flows are good enough to buyback a whopping 3 % of share capital every year. Even the appointment of a new CEO - often a harbinger of change - seems to have not made a difference. Some out-of-the box thinking, some risk taking, some dynamism is what I would like to see at NOCIL.

(Disc.: Invested)

7 Likes