Thanks! I was asking because this point threw me off. Company has completed its CAPEX plans and is debt-free since FY16. Yet Care somehow thinks NOCIL will take on debt that too on a ‘sustained basis’

1 Like

Good analysis .

Some areas of concerns for Nocil,

-No pricing power.

-China’s Sunsine is running at full capacity ,whereas Nocil is just around 65% of capacity utilization.

-I never heard them talking about their clients or even mentioning about any long term contracts.

-Pure play of operating leverage ,business is relying purely on market condition and hoping the demand to get better.

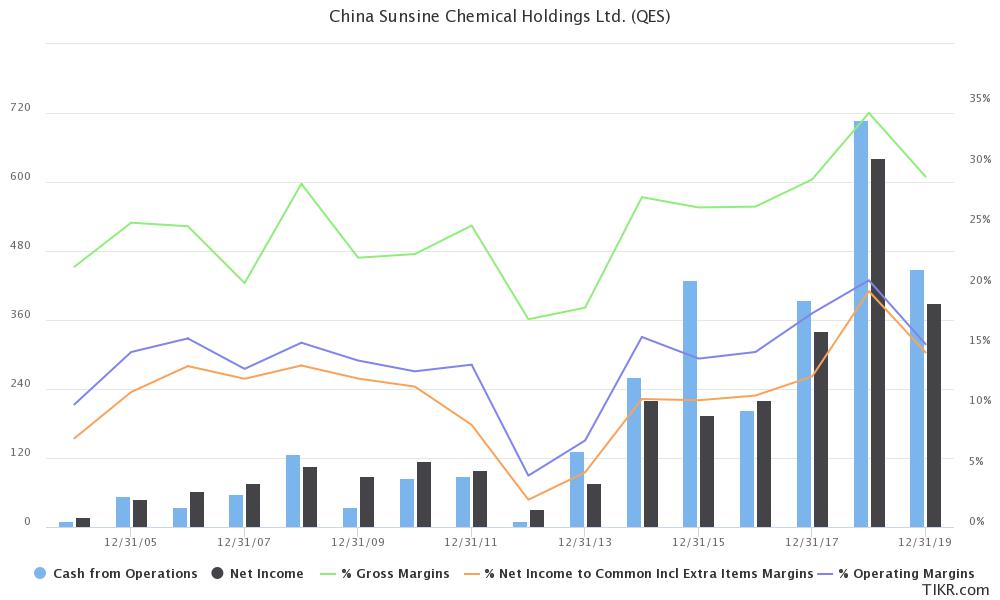

Key NOCIL competitor - China Sunshine - Trades in Singapore - China Sunsine Chemical Holdings Ltd. (SGX:QES)

Trades at 4.5x P/E ratio

Trades at 0.7x Revenue

No debt. 60% of M.Cap is Net Cash

EV/EBITDA is 1x

Operating performance super impressive.

Compare this with Nocil and it will look super expensive. Not sure why stocks in India always trade so expensive!

Not invested but researching

2 Likes

To add - 14% dividend yield (2019). Regular dividend payment

And China Sunshine is more than 2x the NOCIL 2019 capacity and the leader in the space.

1 Like

You are right, clearly valuations for China Sunshine are at cyclical lows (EV/sales, EV/EBIT and P/B; taken from tikr).

One thing that worries me is the high margins (which shows that the sector is close to its historical high).

1 Like

In commodity / commodoity chemicals - peak margin and bottom of cycle valuation means margin is about to fall. That is what market is saying/expecting. (Peter Lynch, One up on wall street)

3 Likes

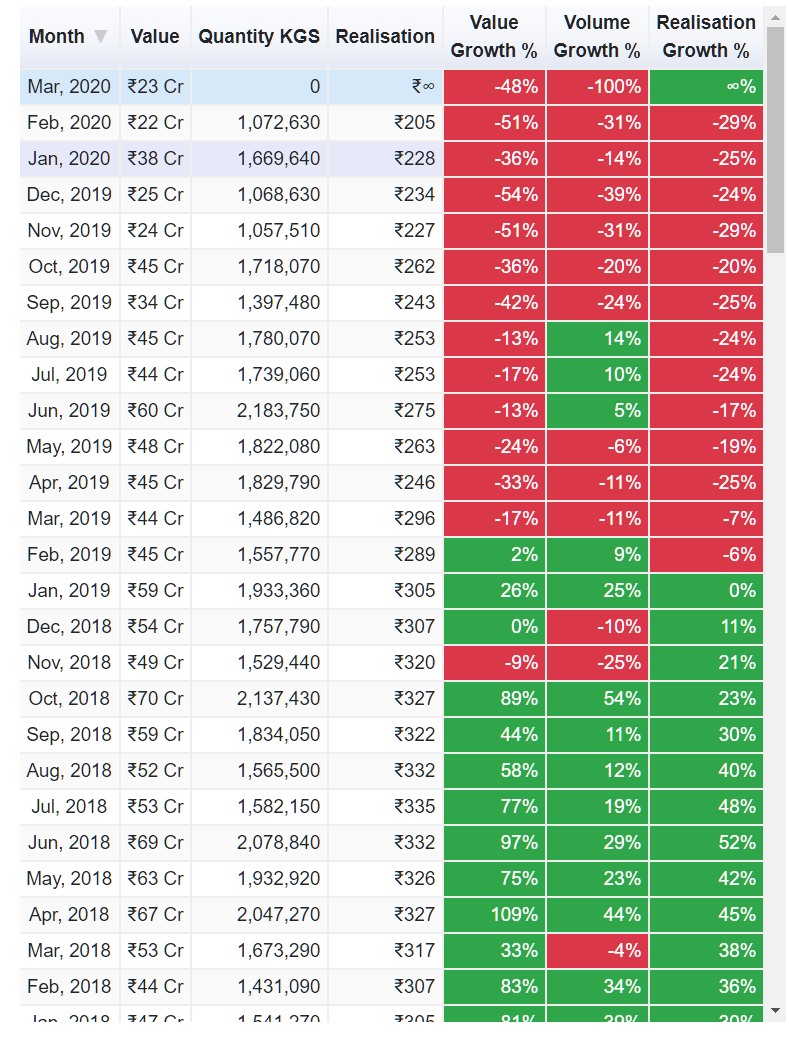

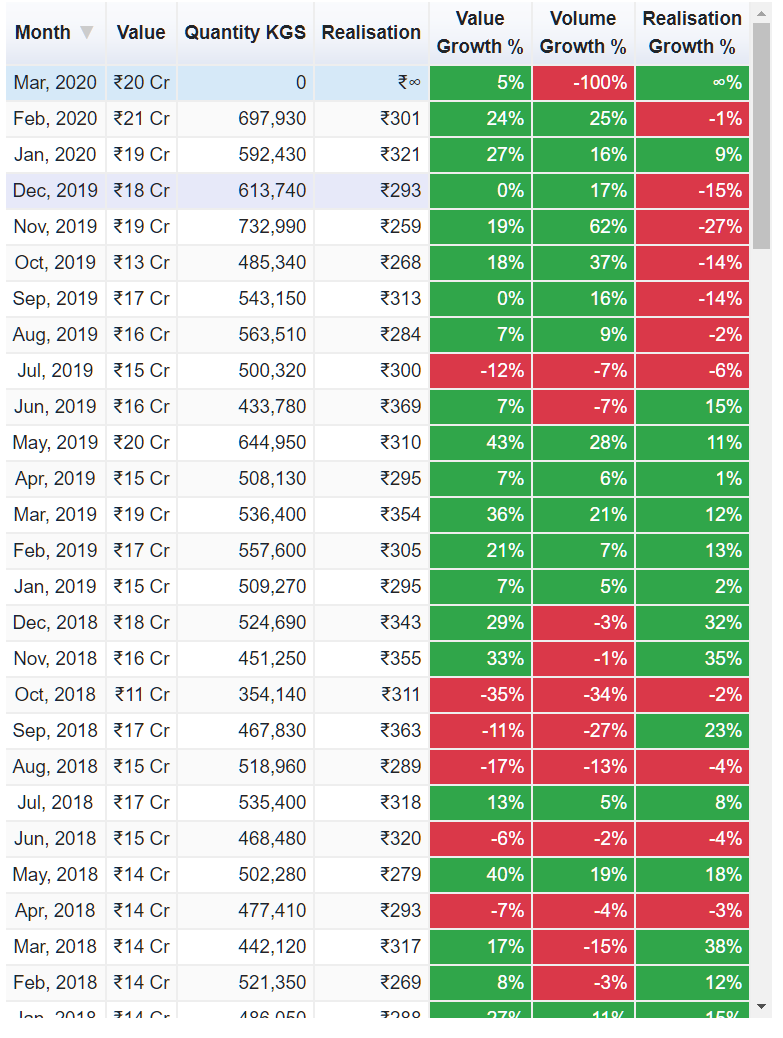

Looks like the company has started another anti-dumping charge against Chinese dumping of PX-13

This time they may have a better case. These are the import prices which are in 220-250 range (check Realisation between Apr-19 and Mar-20)

While these are the export prices (280-320 range)

PX-13 must make up 40% or more of the company’s topline if my earlier research is right.

Disc: Have trading position

10 Likes

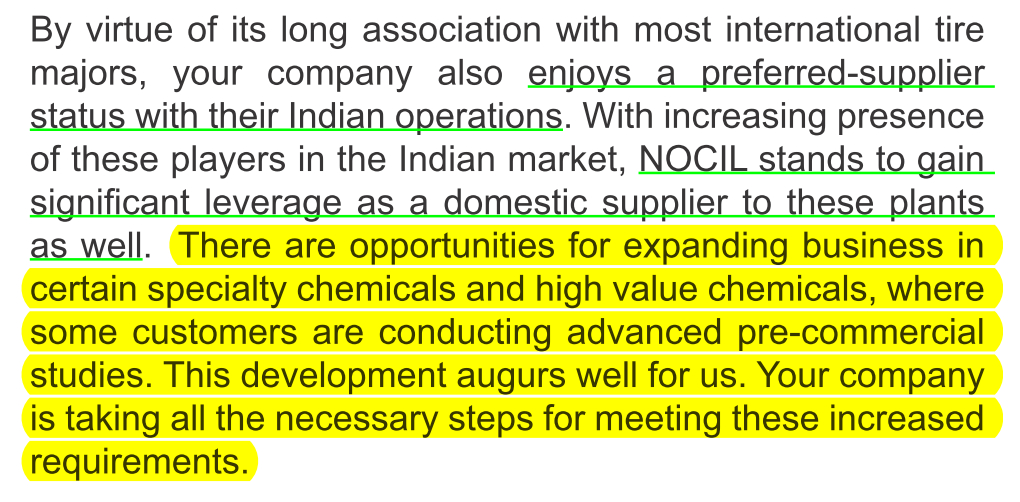

From AR 2019-20

According to previous two quarters’ concall they are targeting 25% revenue from the specialty chemicals, some of which goes to healthcare industry in making surgical gloves etc.

9 Likes

results: https://www.bseindia.com/xml-data/corpfiling/AttachLive/92b0f478-cddd-459e-8fe7-d4f689ffd60f.pdf

Gross margins improved both YoY & QoQ, otherwise nothing much to write home about in the Q1 results. However, the market seems to have been enthused by company’s claim that Q2 will be better than Q2 of last year in absolute terms. That’s quite an encouraging statement to be made in the current scenario.

More importantly, I think completion of such a huge capex (almost complete now) funded entirely by internal accruals without any cost or time overruns while retaining a debt free status in such a capital intensive industry is quite an amazing feat. Not many managements in the country can boast of such capabilities. Capacity is now doubled, and NOCIL stands well placed to seize the opportunity as and when the economy improves.

9 Likes

I spoke to their IR team. Sunshine and other 2 chinese players are also expanding capacity. 2 of the chinese competitors have raised money for this purpose. There will be a lot of undercutting. NOCIL cannot be protected unless Government announces ADD. These are peak gross margins and Co. will have to face price wars. While he government can protect them in the domestic market, nothing can help them in the export market which the Co. is keen to expand.

7 Likes

Nocil

Conference Call Highlights:

Q1 volumes were at 50% of Q4 levels. Plants started operating from 8th May.

Utilization level continue to improve post June.

Nocil remains confident of exceeding Q2FY20 volumes in the current quarter.

Company followed an aggressive market gain strategy even in a weak demand

environment.

RM prices remain stable but impacted Q1 gross margin as the company had to use expensive RM.

CY20 global rubber demand is likely to be hit due to the pandemic, however,

management expects demand recovery to mirror CY08-10 demand.

Yes, I agree Chinese capacity is a permanent problem. And that is why NOCIL is not a very favoured stock. The move by global suppliers to diversify outside China and have at least one non-Chinese player will help NOCIL. But we have to wait and see how much regular volumes it will bring. Only time will tell.

4 Likes

@Chandragupta

since you seem to follow this story, would you mind answering the following.

Growth in Rubber Chemicals essentially follow the growth in Rubber consumption. Rubber consumption is growing in low single digits. Given that NOCIL is amongst the top 5 rubber chemical players globally, how long one should assume it to grow bottom line at more than 20% CAGR. For NOCIL most of the top line growth came from market share gain and most of the bottom line gain came from operating leverage. I am aware that NOCIL still mainly caters to the Indian market and so export contribution is less.

@sujay85 I don’t generally make projections, and it is especially difficult in a business like NOCIL. The management has said it will take three years to utilize full capacity, one should assume four to be conservative. This means full capacity utilization can be reached in FY25. But even this is by volume; we know nothing about the price it will fetch. Looking at the past data, 12-year sales growth has been only 8% though profit growth has been 20% plus. But these numbers have recency bias since the numbers improved sharply between FY15-19 and have begun to decline since then.

My learning from this investment is that the best strategy to use is to continuously assess where we stand within the various cycles – macro-economic (especially auto), commodity prices (rubber chemicals & RM) and market sentiment. When most of these are veering towards pessimism, the stock is a buy (with stop loss) and when most of these are veering towards optimism, it is a sell.

12 Likes

Also, anti-China sentiment can be a temporary thing and not the permanent thing.

Businesses and businessmen in the long term don’t care about sentiments.

1 Like

Short Note on Nocil

5 Likes

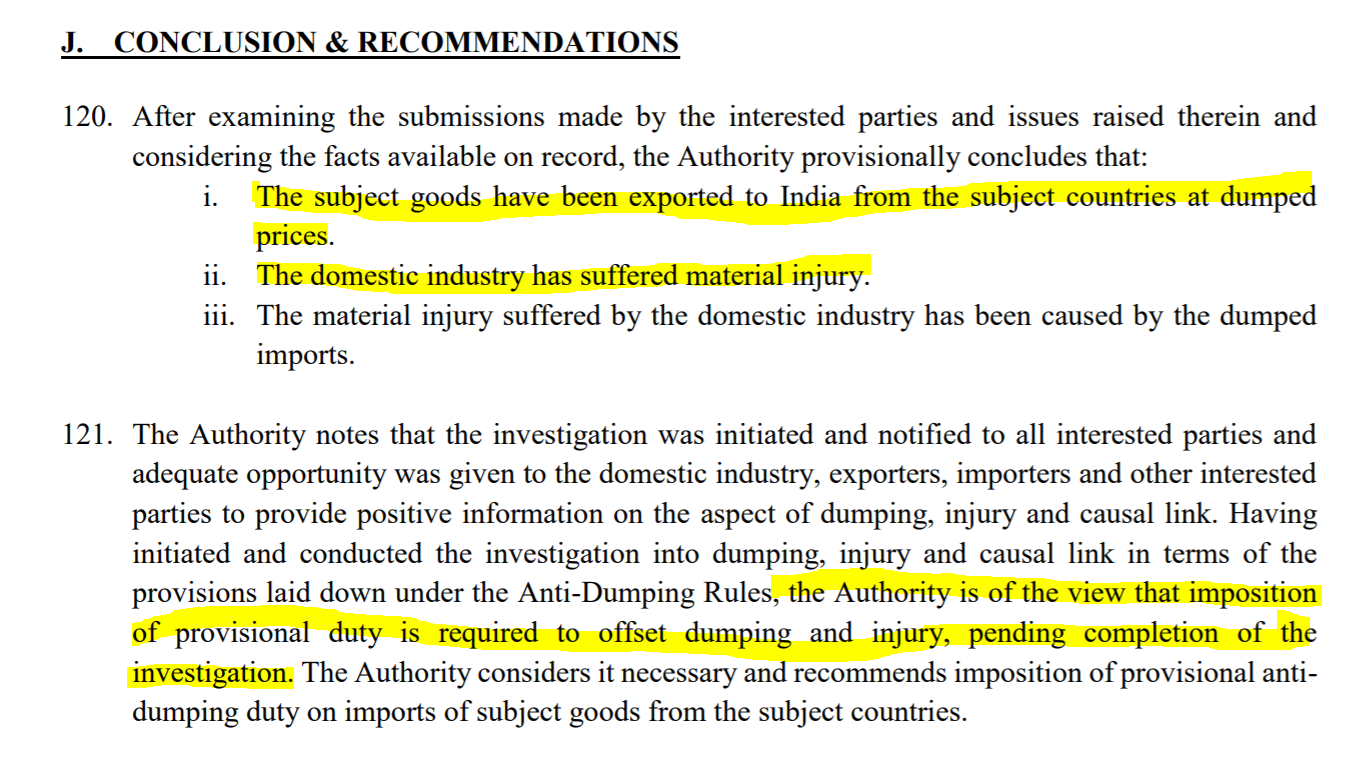

Looks like the preliminary findings on anti-dumping investigation of PX-13 has come out.

http://www.dgtr.gov.in/sites/default/files/NCV%20%20PF%20dated%2011th%20November%2C%202020.pdf

and it might work out in Nocil’s favor going by the conclusions

Nocil has a 70% market share in PX-13 and PX-13 probably (based on my calculations earlier in this thread) makes up a bout 40-50% of the topline.

Also DGTR has notified anti-dumping duty on Radial tyres for buses and lorries last week - this is likely to increase domestic demand for rubber chemicals as well.

http://www.dgtr.gov.in/sites/default/files/Tyre%20FF%20NCV.pdf

Disc: Have a trading position

8 Likes

Thanks.

This is around 3 weeks old now. Looks like there is still ambiguity and some new data has been asked for. I believe there was a brief upmove and after that the price has stabilized around 140. Looks to me like market is in a ‘wait and watch’ mode and any further movements are likely to happen only post some confirmation.

2 Likes