To give a brief background I have recently started working and have been investing since 2018 but realigned my portfolio in line with some learning which I will share later in the post. I have a long runway as I have recently started working and have no responsibilities yet and fixed monthly income in the form of salary. I intend to buy only those securities which are sector leaders with top quality management. Have no intentions of trading or F&O and investing only in companies which I can hold for 10years and possibly build up positions through SIP. Having said that I am extremely passionate about investing with exposure only to equities. Return of capital is of utmost importance to me ( not really recency bias as this has been since I wrote my investment philosophy). I am okay with earning a CAGR of 15% for my entire investing career as my objective is wealth creation and not income generation.

Hope everyone is home and taking care of themselves amidst corona issue. Inviting views from fellow members. This is my first post so pardon me for my mistakes , hoping to learn from all of you.

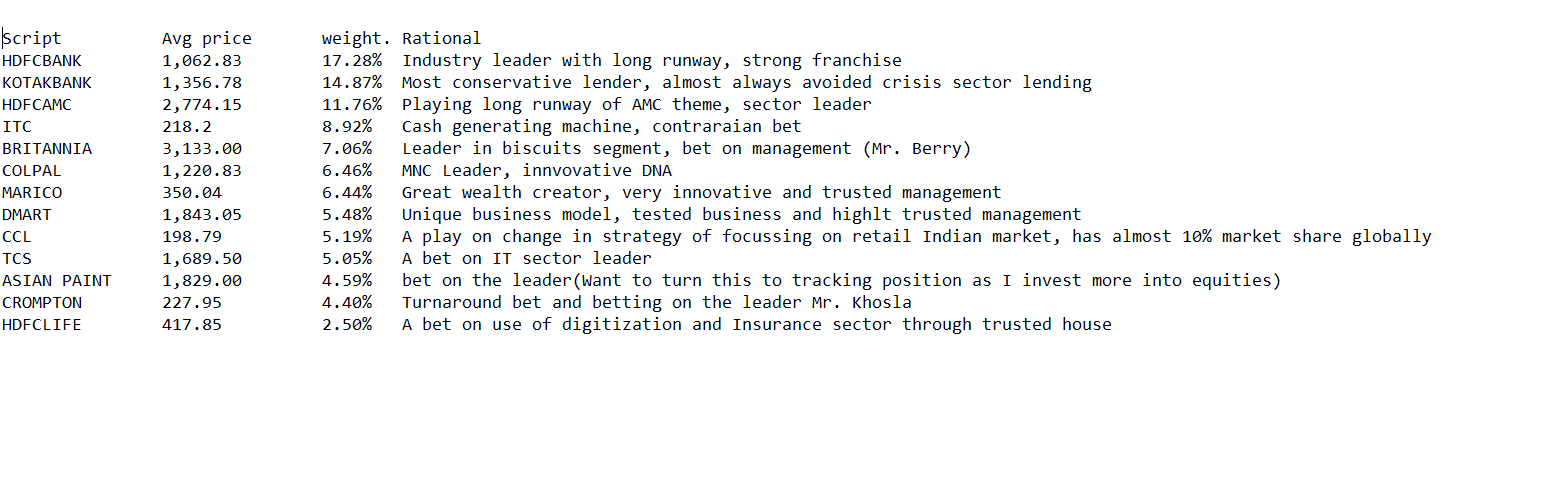

Thought of sharing my Investment Philosophy (behavioral)

Return Of capital is of utmost importance

If I cannot stay invested for 10 years in a stock I shall pass

Slow returns are better than negative or no returns

Do no intend to hold more than 15 stocks at any point in time

Sell only when underlying business has changed or management issues are faced

I understand my nature which is risk averse and should always bear that in mind

Increase my holdings slowly through SIP and earn with thee underlying business

Motive is to create wealth

Last one Keep it simple

The following are on my watch-list, would add on subsequent falls. Not waiting for entire dust to settle as I think that would be trying to time the market plus nibbling quantities is in line with my approach of SIP-ing and longer time horizon gives me comfort keeping me little away from fear.

Jubilant Foodworks: Wanted to add this script since long, these falls are giving good levels to start entering. Might take time once the economy starts for people to come back to normal but I dont think Dominos wont come back with a bang withing 1-3 year time horizon.

Avenue Supermart: Excellent business model, always been expensive , doing everything to serve people in difficult times, not sure about valuations but business & management quality gives me a margin of safety

Looking to add more in the following businesses:

CCL Products India

CG Consumer

Kotak Bank

Marico

Not going to buy everything in one go, will add in 3 tranches till cash is exhausted. Since I am employed full time & will be getting fixed cash flow(so grateful given the conditions) even if the market goes down from here will have some cash to buy.

Some more stocks on my list waiting to add:

HDFC AMC: Believe in the larger picture of long runway ahead and penetration possiblities

Bajaj Finance: Gold standard NBFC which shall do good IMO after the dust settles, so want to start buying

Sonata Software: Frankly dont know much about the company other than a good turnaround story, generates good cash & pays dividend. The next quater reduction in profit seems to be priced in but not sure if this company fits in my 10yr period criteria (views Invited).

Update:

Entered Bajaj Finance & added CCL products India and CG Consumer. Not trying to call bottom in any of them just trying to stick to my buying. Also have zero exposure to any other asset class apart from equity and cash but this seems to be a good time to plan the asset allocation strategy, might add debt MF for diversification across assets.

As far as my understanding goes a stock under ASM is not a red flag, does not happen due to any fundamental change. It is due to high volatility and volume action. Not a red flag for me, the yield on stock is attractive and so is the cash that it generates, management seems to be clean and thread on valupickr on the stock suggests only one red flag i.e. significant increase in receivables.

I am heavy on return of capital philosophy and not very comfortable taking a lot of risk, thats the reason I have kept heavy weights on sector leaders. Now they happen to be leaders in the previous bull cycle but that isn’t a reason good enough to believe that they wont be doing well.

2-3 days ago I saw Mr. Manish Chokhani’s video call where he answered this question of previous bull cycle leaders- Infy & TCS lead the cycle back in 2000’s but even after that until 2020 the returns they have given are great. Plus I beleive that once we come out of this crisis the bigs are going to get even bigger and stronger.

Having said this I have mostly chosen companies with good governance practices and proven business models which gives me good safety net.

My aim is achieve a CAGR of 15% (which is hard and fast) which would be over next 10-20 years, so chasing growth stocks and churning portfolio often is not something that I am very comfortable with.(one of the reasons I have chosen mostly B2C businesses with long runway)

I intend to hold almost all stocks across cycles and not sell them.

Lets not come down to individual stock comparisons because I am sure far more money has been lost in chasing the next growth stock, hot stock and multibaggers.

Having said that sure I might end up having one or maybe more stocks with such mediocre results plus having a growth stock doesn’t necessarily mean high returns.

Such stocks give me a comfort in terms of business quality which I don’t get in chasing growth, now this might change in coming years maybe as I do see a point in your argument but for me right now it boils down to knowing my behavior and investing accordingly.

I am not chasing returns as I subscribe to the thought of take care of the downside and upside will eventually come.

Which is why we have a portfolio of companies. It’s not a single stocks responsibility to get us returns. It’s a team work.

Some will give negative returns and fall yo zero maybe. Some will grow slowly and some will grow a lot at a faster pace.

The overall performance from this needs to meet out expectations.

That is why diversification and stock specific allocation will play a big role.

Like this portfolio. Very similar to my philosophy.

High roce, increase in slaes and profit, low debt, good management, small ticket size products and services, sustainable competitive advantage. With a high focus on earnings engine of any company and low focus on price. Because any price expansion we get from PE expansion will be short lived when not accompanied by earnings growths. But if we buy a high earning company even at a lofty PE, we can still earn very good returns. Because everytime the E in P/E increaes and the PE falls, the price is I’ll increse to match the previous higher PE (an indicator of markets faith in competence and consistency of earnings from a company. Safety and quality is always available at a premium)

It is sad if you think these are the only good companies where you have to invest. A lot of that is perhaps because of recent (past 5-10 years) performance ?

There are many excellent quality companies availabe in midcap and small cap spaces, but not many will notice them simply because they are not in trend…today!

This is a completely false assertion. And there are countless examples from history to refute this. Infact, the growth in the companies mentioned are nothing extraordinary.

I can completely understand your point of view and empathise with it. What I will advice is this- simply search on google about what happened to companies that have traded at extreme valuations without earnings growth to back them up. See the reports of people who have conducted research about the same and the kind of returns which such companies have posted in the long run.

Don’t get buoyed by past performances, I agree companies like Asian Paints, Colgate, Britannia etc. have defied valuations for an extended period of time, but that is not a guarantee that they will continue to do so in future. If they do post excellent growth then its a different matter. But without earnings growth to back up, there is simply no logical reason why any company should trade at high multiples.

Irrational and illogical euphoria about certain sectors/companies have existed countless times in history, once in a while even for an extended period of time, this is not something new. Infact right in this forum, there was a similar “just invest at whatever price and ignore the valuations” euphoria for Page, you can check its thread. Now think, what would have happened to someone who would have invested in the company 5 years ago.

Similar euphoria existed in late 90s for internet and software companies, I think someone already mentioned earlier how buying even a good company like infosys at extreme valuations would have resulted in, even after 20 long years!

Another company that comes to my mind is Castrol. At one time, it used to get traded at 40-50 pe multiple and had excellent roe, roce, working capital, inventory turnover, high market share etc., you get the point- all those things which are highly looked into. Except for one thing- earnings growth. And see its fate. Its cagr for past 10 years is 2% and negative for past 5-7 years (the company has given excellent dividends though, I will admit). HUL suffered similar fate last decade.

The point is, no matter how good a business is, buying it at an extreme high valuation is no net of safety. The businesses may still be alive and kicking, however you can’t say the same about their stocks. For every Nestle and Asian Paints, there are other counter examples like I mentioned above. If there is no growth to back up the lofty valuations, then investing in such companies is just pure speculation.

Different styles work for different people, I agree to that. There are more than one way to create alpha.

If growth was the only criterion for a good company, then high beta companies would have the highest valuations. Almost everyone ignores emphasising enough on stability and longevity of earnings which play a big role in a valuation given to a company. Eg: rain, heg, avanti etc.

I don’t know exactly what you mean by “defied valuations for an extended period” keeping in mind the whole subject of valuation is relative and everytime market collectively gives (An individual can agree to that notion or rejecte it) a price to every 1 re of a companies earnings, it not only depends on its ability to genrate cashflow in future but also it’s longevity and stability. Which again depends on if the company has a sustainable competitive advantage, able management and does good capital allocation and redeploys the cash into business to generate superior roe and roce yoy.

It would be very one dimensional to call a company good only because it is a large cap and it has a brand name and is covered by various analysts if it lacks in the few above basic criterion. Example: Infosys, hul.

Similarly it would be very one dimensional to shun off investing in a company which has been generating superior cash flow and roce because it is trading at high pe. Without finding out WHY it has been given such a high premium by the market collectively. Example: Nestle, asian paints, relaxo, Marico etc.

And yes, market is not always right! So due diligence is very necessary.

This boils everything down for me to certain points:

Looking to buy companies with the above criterias. Because I believe it is far more safe to predict and discount the future earnings of a company when it satisfies the checklists. Because when the earnings power of a company is intact (yes this is very important) the high relative valuation is probably not actually high. Thus generating alpha through only earnings.

It would be a best case scenario to buy companies which have the above said criterias and also are trading at far lower valuation compared similar cash generating franchises. Generating alpha through both pe expansion and earnings growth.

Having a narrow focus on price and only buying based on cigarette butt style investing introduced by Ben Graham and looking for margin of safety. Where the stock prices rises from PE expansion but then stops appreciating when the earnings do not move up as expected. Often forcing investors in such stocks to constantly sell and buy different scrips to take advantage of similar pe expansion opportunities.

No matter how mouth watering the valuation is, without focus on a company’s ability to generate free cash flow and competence in redeploying it in the business, buying it is no safety net.

I am someone who will anyday avoid style number 3 because I am lazy. It would be my dream to pull off style 2 frequently. But being realistic neither am I that competent yet nor can I time investing.

So my bets bet is to stick to style 1. I might lose some alpha but my capital protection will receive it’s priority that it deserves.

In a shorter run, valuations will make a difference. But if the earnings engine is in place and the management is competent, honest over a longer term, the valuation difference will be totally wiped away.