Well as it is rightly said by someone you need to know yourself first and then invest. I have very little experience in the stock market less than 2 years and from what I have known about my behavior I kept that in mind and designed a strategy for myself.

I intend to stay conservatively invested for one cycle at-least ( close to 9-10 years) in companies which give me quality comfort and reasonable assurance of both return of capital and return of capital. As far as valuations are concerned maybe they are over priced, but one thing that I have kept in mind is most of the stocks have gotten long runway ahead. besides these companies have stood the test of time and created immense wealth for its investors(almost all companies). Obviously this does not guarantee they will do the same in the future but probability is good.

To protect myself from loosing I have added one more filter of stop loss as suggested by Jatin Khemnani in one of his videos is time stop loss which is you exit stock if it doesn’t moves for 2-3 years straight. Now i am sure there might be a few in my PF which wont and I would be ready to exit those in that case.

Now one thing I know from my nature is I am not very comfortable with running behind stocks which are high growth as it is unsustainable in the long run and as you also suggested that market de rates them very fast and heavily.

Also I am open to suggestions if you can give me some in small and mid cap quality stocks as mentioned by you.

Also I would appreciate if instead of using words like its sad etc if you could keep your thoughts in a better way and share some examples where you feel are not trading at lofty valuations so we all can have healthy discussion and learn.

I think both of you read my above post with some pre conceived notion, instead of looking at it from a fresh perspective. I understand you want to protect your capital ![]() and you are not interested in generating high alpha. In fact, my entire post was to give you a different perspective regarding this only.

and you are not interested in generating high alpha. In fact, my entire post was to give you a different perspective regarding this only.

At the risk of repeating myself again, buying extremely high valuation companies without relevant growth is not a net of safety and regarding this I provided some examples. That doesn’t mean I am advising you to chase for growth stocks.

Growth is not the only parameter agree, but it is one of the most important for high pe stocks. Here is the profit growth data of past 5 years of some of these companies-

HUL (11.5%), Asian Paints (12.14%), Britannia (24.5%, respectable), Nestle (7.7%), Colgate (9%). All of these companies trade in a pe band of 50-75! I alluded in my previous post how Page and Castrol, which also used to get clubbed in the same basket of “invest at whatever price” fared in the absence of growth.

In your free time, search google with these keywords- irrational exuberance Schiller. That will tell you why price and valuations are important ![]()

That was in response to @Investor_No_1’s previous post where he asked “what else better remains”. There are many good companies in small and midcap, and actually even in large cap with excellent fundamentals. Some of them may not be winners of “past trends” because of some temporary issues, but why because of which they will be at good valuations. Some examples- Gmm Pfaudler, Alkyl Amines, HCL, Maruti and Bajaj Auto, Sundram Fasteners, Procter and Gamble Health Limited, Caplin Point etc. Even celebrated names where I also agree like Itc, Hdfc bank etc. Some of them may have high p/e or p/b multiple but they have good growth rates (or future growth possibilities) to back that up. Recent corrections in market, in companies like Bajaj Finance for example are opening even more possibilities.

I refrained from listing them earlier because it would seem like I am advertising my portfolio in your thread ![]() , which was not my intention.

, which was not my intention.

Disc.- I do have positions in some of them, and pretty much all of them in my permanent watchlist.

Very nicely said.

My intentions were on the same lines.

HUL is great business and I have nothing against it.

I am just concerned with the valuation it is trading now.

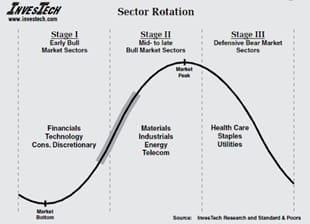

This graph might give you better idea what I am suggesting.

Another thing, I would like to add is one usually takes more risk when he’s younger.

His risk appetite should decrease with the age.

Eg. A 60 year old portfolio should mostly consists of high Dividend paying stock as that would benefit him greatly.

Point well taken

I will update my philosophy with a time exit strategy and ruthlessly cut my losers if they don’t do anything for 2-3 years.

A longer term horizon gives me comfort over valuation parameter so I used to almost neglect it which I think I should be a little more cautious with. (wold also admit I know little with respect to valuing companies but will get a broad based parameter no on0

Planning to exit CG consumer elec. completely as not comfortable with the PE firm pledging almost 65% of their stake add to this continuous reduction in their stake ( which they might exit anytime).

You should also think more in depth about this strategy as well.

Many a times, stock remains range bound before start flying.

Eg

HUL during 2002 - 2010

ITC during Feb 14 - Feb 17

So blindly following above strategy would be harmful

This would involve opportunity cost too so lets see how I evolve the strategy, just broad based thing in mind wont be the only factor to base my decisions on

I guess we will have to agree to disagree.

We have different ways in which we want to generate alpha. I believe if I pick up 10 stocks and 2 out of them fall and become zero. Two of them turn out to be like gillette and Castrol, the alpha generated by the other 6 companies will make up and pull up the overall returns of the portfolio. A team effort instead of very high focus on single stocks performance.

If still go with over longer term, valuation will not matter if earning is stable and growing which is a result of moat, good capital allocation, management.

I’ve read the book coffee can investing, the thoughtful investor by Basant Maheshwari and other investors and consciously chose to stick to this style where there is zero focus in valuation and very high focus on the above mentioned parameters. Because I’m an average retail investor who is kind of lazy. Choosing ignorance as it’s easier than trying to catch falling knives.

Data points:

https://marcellus.in/blogs/the-stock-price-of-a-company-tells-you-nothing-useful/

Excerpt from a conversation between Vishal Khandelwal of Safal Niveshak and Basant Maheshwari.

Makes a lot of sense.

- SN: One of the problems that new or small investors face is that they can’t really get their heads around valuation. It seems so complex. A lot of the terminology is complex, and so are the concepts. How can valuations be made easier? How have you made it easier? Or can it not be made easier?

BM: There are two aspects to valuation. One is to evaluate the longevity of the business, which is what Buffett talks about – the business quality, moats, etc. But since we can’t get numbers on them, we don’t do it.Now, while starting a valuation sheet, how many people ask this question on the first row of the excel sheet – “Is this company going to remain in business by, say, 2020?” Most people don’t do!

And then they don’t know which metric to use when. If I am doing a DCF on Sterlite, or a DCF on Hindalco, and the Supreme Court suddenly thinks that it should de-allocate the coal mines given to these companies, then all the DCF goes for a toss. Let’s assume the Supreme Court is kind enough, and says,” Okay, since you’ve started work on the mines, we’ll give you time to look into it,” who will take care of the London Metal Exchange?

So for cyclical companies, there is no valuation metric that can be used with confidence. Just buy such companies when they are making their five-year lows, and sell them when they go up 3-4 times.

Tata Steel, for instance, will go 3-4 times from the bottom to the top. If it rises so much, you sell. There’s no need to value it anymore. If somebody has to make money, let him make money on it.

But, on the other hand, if you have bought a stable and structural growth company, and if you can predict the growth, then ask how much money it will make in the next 2-3 years. That will be a good time for you to actually look at it from different angles, because you’re sure about the company.

You see, most of the time, it’s not a numbers game only, or it’s not a business game only. It’s just a combination of it. But if you ask me the PEG (price-to-earnings growth) ratio, for instance, I don’t use it at all. I am a big Peter Lynch fan for the book that he has written, but I don’t believe in PEG. Let’s say there’s a company that will never be able to grow, you think it will sell for free because ‘G’ is zero? PEG is just a very broad approximation.

But in most of the reports, I see people using PEG.

You see, P/E can go up also for high cash companies. P/E can go up for dividend yield stocks also. You will always try to tear your hair off why this stock is trading at a P/E of 40x, but if it trades at a P/E of 10x, the dividend yield will also be at around 10%. Look at Nestle. Assume the stock trades at a P/E of 10x – just reduce the Stock price to get it to 10x P/E – and then work out the dividend yield, you would find that it will be an exorbitantly high yield, which will never happen.So there’s no single mechanism to get around this thing. Also, there are companies whose P/E are a function of the management also, which you cannot define. Just because growth is a very good number to work on, most people put P/E equal to G, and then they work on it. It may work in many cases, but in many cases it won’t work at all. This is when there’s something else that is more significant than the G, then that will take over, like the dividend. And there’s nothing more real than the dividend.

Anyways, let me now talk about how to value a moat. Let me give you an example. Semi-urban and rural India is going to see a boom in the next 5-10 years. One thing that this government is also focusing on is rural housing. I will give you an example of a stock that currently trades at a P/BV (price-to-book value) of more than 10x – Gruh Finance. Now whether this is expensive or not is another issue.

Now consider this – there is a shortfall of more than 6 crore households in India, and Gruh Finance, along with the other rural housing finance companies, doesn’t even have 6-8 lac accounts with them. At maximum, they would have 10 lac accounts. And the total market is for 6

crore homes. Now, why would Gruh do so well? A guy who borrows Rs 2-5 lac to actually build his home will always be someone who does not maintain a bank account, at least in most cases.

This is because, in most cases, the situation is where the husband is driving a truck and the wife is selling vegetables. They don’t have a bank account, so how can banks fund them? They won’t, because there is no income proof. So, even if they are creditworthy, they have nothing to show that they are creditworthy. And thus this market remains untapped. This is why these guys lend at 12% whereas banks lend at 10%. And this is the 2% that they make. They make it because they understand the structure so well. They understand the market so well. This is a huge competitive advantage I think.Now, why wouldn’t banks get into it? This is because no bank would be interested in that kind of granular lending.

If you see India’s banking history, most banks have the higher number of NPAs when they have tried to lend below Rs 15 lac. So if you ask me, I think this is one place where can you get the next 20, 30, 40 bagger. Now whether this company does well or some other companies do well…some companies will surely do very well, if India is to grow. Over the last few years, you have seen NREGA, land prices going up, people from villages going to towns and cities and earning, working in software companies, and writing cheques back for their parents. So there’s too much money reaching rural homes these days.

Also, prices of food and vegetables are going up, but in some way that is helping rural India. So there’s a transfer of wealth happening. In the Rs 5-15 lac category, there aren’t too many companies around who can lend and who have a history of lending. I don’t think there are more than 60 registered housing finance companies in India. So there’s a huge opportunity here.

The point is, if you try and focus on this sector, then you will make it big. This is one sector where you can find good companies with sustainable moats. But then, this is a 20 year story, not a 10 year story.

- SN: I think not knowing the trend breaking up in foresight is what causes people to overpay. How do you differentiate between whether you are paying up for a stock or overpaying?

BM: It depends on which year’s earnings you consider. Are you in FY14 or FY16? Today, if you look at many of the engineering companies, they are doing well because people assume things will change. And on an FY16 basis, they are at around 25x P/E. And a classic secular growth company, on an FY16 basis, could be on 30x P/E.So why won’t I pay 5x more and buy a classic secular growth company instead of trying to become the smart guy out there by first assuming how this engineering company will turn around and how much it will make in FTY16 and then try to say that this company is better because in FY16 it will trade at 25x against your secular growth company that is trading at 30x?

The first problem of overpaying or not overpaying comes because who will decide which year’s earnings have to be looked at.And for companies that have predictable growth, where there is surety, the market will put the stock at an expanded level for as many years as much as you can predict the growth. Like HDFC Bank, I think, remained in a range for four years between 1999 and 2003. It traded at a price-to-book of more than 7x. And then it came down to less than 3x also. But the point is, how many people would have thought that at 7x, HDFC Bank could have done nothing from there on, and sold it.Good companies, like good life partners, are not too many. You find one, you stay with it, till the time the partner doesn’t do that you don’t want it to do.But I think the biggest problem is that when we compare companies, we compare them with trailing earnings. Like I will compare Tata Steel’s with Tata Motors’s trailing earnings. But Tata Motors’s earnings are more predictable than Tata Steel’s. ITC’s earnings are more predictable than Tata Motors’s. Because of government regulations on ITC, Nestle’s earnings are more predictable than the former. So I can’t put everything in FY14 (trailing) earnings. And nobody knows whether you should look at FY15, or FY16, or FY17.

In all, overpaying is not a problem, as long as the trend remains, and as long as you can predict.Also, overpaying is not a problem with predictable businesses. However, you also need to see that the prediction you are making is on the right scale. You just can’t predict endlessly.

exited CG consumer Elec. and also Asian Paints as the conviction I have is low from what I understand, definitely going contrarian betting on financial services sector, before people jump again to say they might not be next leaders let me clear myself I am not trying to find next cycle leaders not that I mind if I find them but it fairly obvious a lot of people are in that boat and I know I dont hae any edge over them, so I am fine with strong franchise business doing bad temporarily and falling from great heights lets say a bajaj finance or HDFC bank, slowly adding them at dips and building my position. Simultaneously looking to increase exposure in IT sector, havent added any yet.

Any particular reason behind Asian Paints exit?

weakest conviction among other portfolio stocks and valuation concerns going forward.

Hi @valuelife

I do not know of your current portfolio but I am going by the first post you mentioned. So as requested I will try to give a view on what I can make out and also on those stocks I track.

First things first you need to know that if you have a 100 rupee portfolio how much are you going to keep in equity and how much in debt (FD/Liquid etc.). This is as important as getting stock selection right imho. I have my own views on this and everyone has to develop his own individual philosophy I think.

So that out of the way. I would next suggest do maintain your portfolio systematically.

- Cash Flows in and out of your portfolio

- Dividends

- Any bonus split

- Calculate CAGR, Sharpe Ratio and Beta of Portfolio. This will become very helpful at a later point of time.

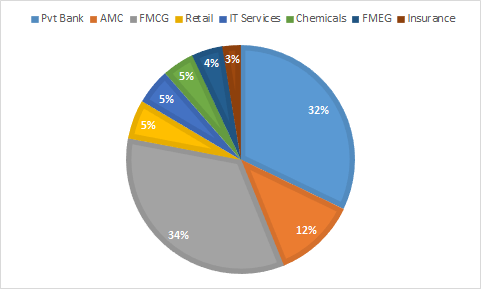

Next do a sector wise split. Here it seems you are fairly balanced.

I would recommend to split (mentally) the portfolio into 2 parts - a core part and second a satellite where you have your bets like Crompton (turnaround bet in this case).

You seem fairly well concentrated but personally there are a lot of FMCG names 1/3rd of it. Over time I would perosnally have reduced this. More importantly so your buy prices are all at the peak. Sorry to say in hindsight this could be a bad thing. So think about it. FMCG will be very stable but could not give great returns you are looking at. Keep some of it in core part and where you dont have conviction move it to satellite and then out completely.

Coming to stock wise. My views are personal for the ones I track.

HDFC Bank: Your buy price is ok. But I think you will get a chance to add in the coming quarters. This is ‘the’ best bet on the Indian banking sector. Currently there are headwinds and I would give most of the deratings by analyst a pass if my timeframe is 5+ years at the minimum.

Kotak Bank: This is the only other bank I would like to bet on. I think this too you have bought at a high price. Its currently very highly valued. But here the bet the market is making on is the jockey. Good to have it in a portfolio.

HDFC AMC: This might also have headwinds. And your buy price seems high. But out of the AMCs HDFC AMC & Nippon in my opinion are the ones to go after in this theme.

ITC: This is a pure valuation play. And it is a consensus buy amongst us value investors. There is an excellent article on medium which was floating around, do read that. I don’t know how much pain remains for ITC though.

Asian Paints: This is the best paints company in India but I think it is trading at very steep high valuations. I do not know if it deserves so. I will have it in my tracker but not sure if it would give good returns with the current valuations in the future.

HDFC Life: The life insurance space again could have headwinds now. But I think though HDFC Life is the most valued.

Dmart: Those who hold it swear by it and those who dont expect a collapse every day. Your buy prices is very high I think and it might turn out to be a bad investment in an otherwise excellent company.

Stocks I dont track: Colpal, Britannia, Marico, CCL, TCS, Crompton

So overall a good set of companies but I think equity debt matters a lot because at the right price you will be able to become a part of exceptionally good businesses. Do explore a few smaller cap businesses which are either going to have earnings jump or re ratings. There is one post by a gentelman on VP on what we should look for. Let me find that put a link to that here. Its an excellent post.

Here it is:

Why I say have a sattelite portfolio because those can serve as trading bets. For instance I had a few companies like GMM Pfaulder, Aarti Ind, Alkyl Amines. Now in my opinion say a GMM is trading at valuations like FMCG companies 70x or so.

I am not advising specific stocks.

Let me know if you need some more inputs on the portfolio.

Rgds and all the best.

Deepak

Hi @deevee

Even though I started investing almost 2 years ago, I am yet to figure out rule based criteria for a debt equity allocation. I am still trying to figure that out. I am inclined on a 80-20 or 70-30(equity to debt) kind of allocation but I dont really have any specific reason for it. I am also a little reluctant on having to change the allocation from time to time.

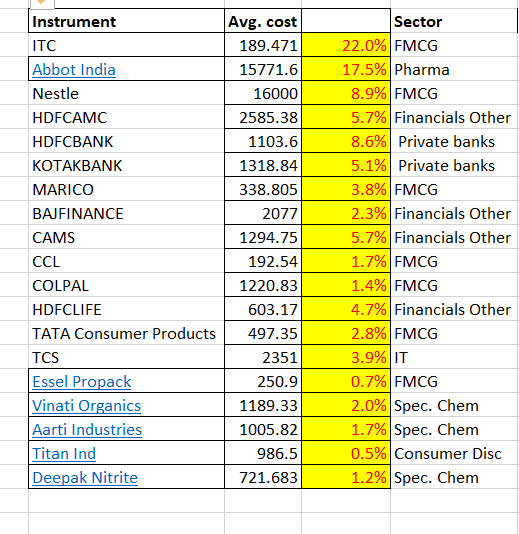

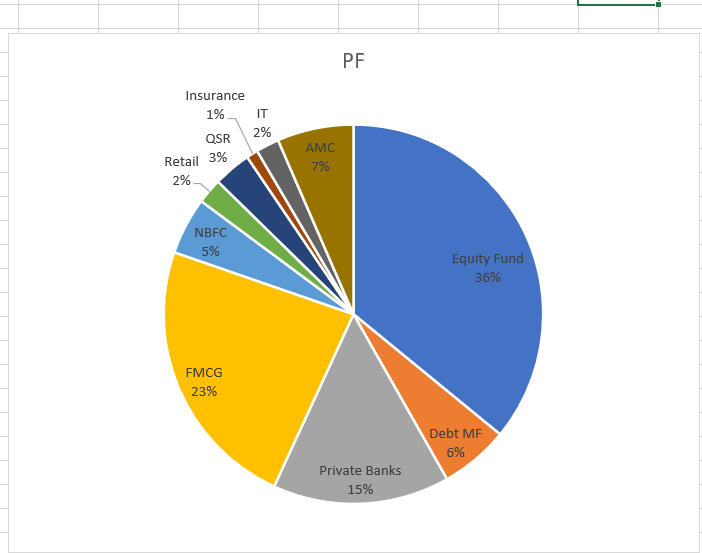

here is my complete portfolio, earlier I did not include MF investments as I wanted review on equity portfolio only but now I see the bigger PF picture.

The equity mutual fund is significant part s of now because when I first started investing I started with SIP and continued it for almost 18 months before i started investing into direct equity. I havent touched this yet because as I my direct equity investing gradually increases month on month the equity nutual fund will become smaller & smaller portion of the total PF.

Here is my latest equity PF

I like the idea of core portfolio and satellite portfolio but I dont exactly know tools for taking such shorter time period bets ( technical analysis would be best suited I guess), but I am open to the thought and might take small bets as and when comfortable which would mostly be momentum bets ( the reason I was avoiding this was I dint want to loose capital in trading).

I started out invsting mostly based on the thought of investing in companies primarily engaged with customers directly as these would have long runways hence retail banks and FMCG. I did not give valuations much though as I started taking positions gradually since last May and ended up buying at high prices but the good part is havent invested all the money I have.

Slowly adding companies which I feel I would be comfortable holding for 5-10 years.

Lastly thanks for taking out time and helping, views always welcome.

First, the good thing about your portfolio. Almost all companies are sector leaders and have proven track record. Return of capital is certain.

Negative I see is nearly 40% weightage to financials, a sector undergoing pain and getting out of favour.

Plus the kind of portfolio you have will require disciplined SIP kind of investment over next 6-12 months atleast.

I dont see any pharma, speciality chemicals company. In near term and maybe even longer, these are likely to outperform.

Overall a coffee can type portfolio, and if held long enough, should do well.

Thanks for the kind words @hitesh2710 , I am on SIP mode when it comes to Financials, buying almost whenever I get good discounts on them and have cash.

Reason for having financials was I believe they have long runway and relative under performance of 1-3 years is fine because the companies are rock solid. I have my biases here one of which maybe hindsight bias where I have seen them doing really well which might not be the case going forward but my expectations are relatively low I guess a 12-15% cagr.

Regarding Pharma & Specialty chem I somehow believe it is hot sector plus I don’t really have much knowledge about the same so having difficult time in being able to bet on them. Also one more bias or blind-spot I have is almost all stocks I have are of companies which I have been a customer of or have seen products/ experienced services of, I dont know how to over come this blind-spot.

I am not a big investor like others but let me air my opinion anyway:

- HDFC & Kotak: In My radar. Haven’t bought yet. I would like to hold on for long term so not worried about short term head winds but i do want to buy in discount to improve my returns hence the wait.

- AMC’s : Index funds are the future hence i am not very bullish on AMC’s.

- ITC: I don’t track.

- Britannia: High debt. Increased drastically off late.

- FMCG: In general, I look for low volume high OPM companies so most FMCG’s don’t cut into my study.

- TCS: In my radar. Would add when it gets cheaper. For now it is overvalued. Considering head winds in the upcoming quarters.

- Asian Paints: Overvalued. Limited upside. Risk-reward doesn’t favour buy at this valuation.

- I don’t track insurance because i don’t understand industry that well.

In general, I look companies with long term applicability, who is working of future technology, High OPM/Low volume companies, consistent EPS growth, share holder friendly management(Buybacks, bonus and dividends, no pref shares, no CD’s, avoid companies which often creates sweat equities specially for top management), Companies with vision(I read through AR and quarterly transcripts to make sure company is really serious about their vision and how they are getting there) and on top of that companies which can generate in excess of top rated mutual funds. If i can’t find a company which cannot generate returns in excess of MF’s or 1-2% more than the MF’s i don’t consider such companies. So far i could find only 4-5 companies which match above criteria and i am yet to buy anything in 3 of them. Waiting for the clarity about the current uncertain environment.

Indeed you have very strict, intersting and good criterias. I feel very few companies in india will pass the test, could be some US companies. Can you pls share which companies passed your criterias?

Ok, This is not investment recommendation. Investor please do your own research.

- Vinati organics - 25% profit growth , Very high OPM > 35%, great financial strength.

- Aarti Industries - 15% consistent profit growth in last 10 years, Management guidance of 40% OPM, Increasing OPM yoy

- TCS - 10% consistent profit growth for last 10 years, OPM > 25%.

- HDFC Bank - 20% profit growth for last 20 years, High NIM

- Bajaj finance - 40% profit growth in lat 10 years - short term pressure due to NBFC’s crisis but company of this quality can come out of it stronger.

That’s it. May there were few other companies which i didn’t select because of lack of vision, management, cyclic and higher valuations.

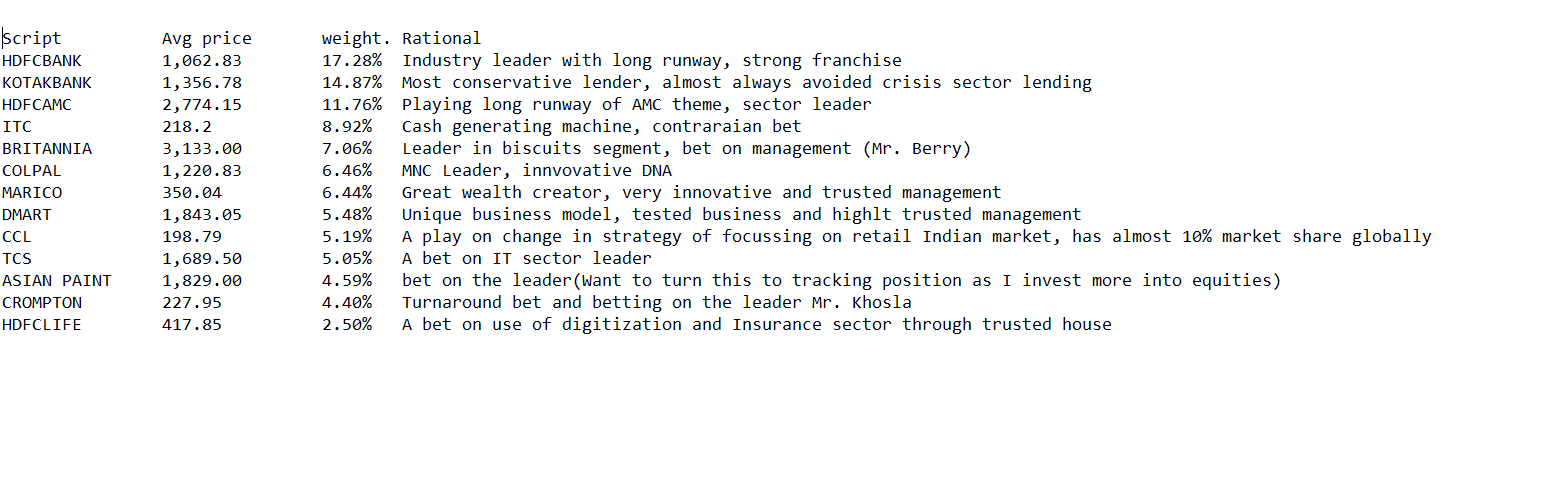

PF update.

Been 6-7 months since last update.

I have been adding stocks that I feel have steam going forward for at least a decade.

Every month I allocate money to equity and increase position or add new stocks.

A change in my way of thinking which came about in the past months is not being too rigid on the number of stocks I hold and being flexible in terms of new opportunities.