MECON is hired to run steel plant. Tentative timeline of commissioning the plant - July 2022

Demerger on track, MCA approval awaited. NMDC has requested for creditor approval exemption. Tentative timeline - April 2022

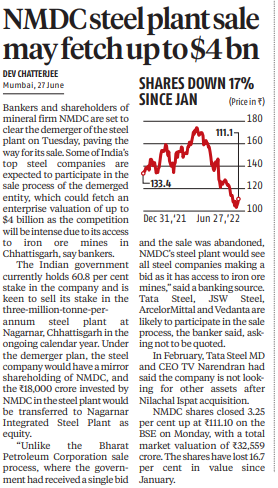

Demerger details - NMDC spend of Rs 18000 Cr (currently in CWIP of NMDC) will be transferred as Equity of NISP(Steel Plant) and Rs 5000 Cr debt taken will also be transferred to NISP.

Capex (FY23) - 1500 Cr (efficiency and volume increase - 500 Cr on Slurry pipeline) + 2000 Cr (Steel Plant)

NINL stake sale (10%) to Tata will fetch around Rs 500 Cr.

High grade Iron Ore exports command 30% export tax and hence unviable. Due to this high grade iron ore sells at 30 to 50% discount compared to international prices. Freight cost is high for exports and royalty is not paid by importer, hence it makes exporting iron ore unviable.

Pellets do not have any export duty, so it makes sense to convert high grade Iron ore to Pellet and export. But as of now NMDC has not explored this option.

Most of the Concall notes have already been covered so I will not mention them again.

Iron ore production target: The target is to produce around 44 Mt of iron ore till the end of the year. In the 9 months of FY22, NMDC has produced 29 Mt, this means they target to produce 15 Mt in Q4. They have already produced 4.5 Mt in January so this seems achievable.

Assuming that the prices of iron ore remain same as Q3 (are much higher already) and there is no benefit from operating leverage, they can do a PAT of 3500 crores (10 Mt PAT in Q3= 2000 crs. so 15 Mt PAT in Q4= 2000* 15/10).

Steel plant: coke oven will start at the end of March or beginning of April, and hot metal in May or June, finished product by June end or July.

I have a doubt here and it would be great if someone could clear this. I am also invested in Sandur Manganese and there they have already setup a coke oven for their integrated steel plant and are already selling coke from it. Can NMDC also do this?

Secondly, there can be massive increase in margins of the steel plant as they will increase production from 2 MT(FY23) to 2.5MT(FY24) and finally 3 MT(FY25). This is just debottlenecking and rampup and thus doesn’t require much capital.

Additionally, the management mentioned that there is land to increas the steel plant from 3 MT to 6 MT. This provides a lot of longevity. for the steel plant.

Very good technical inputs and in fact, as you rightly predicted, NMDC is on its upmove. I have done fundamental analysis on the stock and created a video on NMDC. Wanted to share a link to the video here for the benefit of all. Request everyone to take a look at it and suggest if you like it or things which i could have also covered in the video, that will be great.

Online Iron Ore Auction in Karnataka through Monitoring committee is discontinued based on court orders. This will have positive impact on NMDC as Monitoring Committee used keep 20% of proceeds.

Apart from this, NMDC has ~Rs 2500 Cr receivable from Monitoring committee, for which hearing is going on for last few years in supreme court.

Demerger of Steel Plant on track, Sharholders and Creditors meeting scheduled in June, expected listing of steel plant by year end 2022.

Expected Iron ore production in FY23 is ~ 45 MT. Capex for FY23 ~ 3500 Cr, 2000 Cr towards steel plant.

80% sales to private players (JSW , Arcelor Mittal and one more constitute 70% of total sales) and 20% to Government entitis.

Cash on Books - 8000 Cr, CWIP on Steel Plant - 20,000 Cr.

Can anyone please share what can be concluded for retail shareholders from this demerger.

What could be possible pros of holding this share till this play out.

Any links to possible reports would also be helpful

Thanks!

I think there is reasonable margin of safety at the current price. While any major up-move depends completely on iron ore prices, one can expect 3.5-4K in net profits over the next 12 months if prices hover around this range or even a tad lower. Dividends will be reasonable, and there is the optionality of the steel plant (how that will pan out remains to be seen). Export duty will go away/be cut at some point.

The steel plant is valued at 30000 crore .The company has market cap of 35000 crore.Only issue is when the company will be listed.If it takes year or more then there may not be a lot of gain.

Regarding the steel plant valuation - we will see when it actually happens. It can get sold off at sub-par valuation, it may get demerged and listed. I have no idea. If all goes well, certainly the stock is substantially undervalued. If it doesn’t, the stock is still somewhat undervalued so long as iron ore prices don’t tank completely.