Even if the iron ore prices tank, it should revert back to a price at which it is still worth mining it profitably so I think NMDC might have a good margin of safety right now because of the low iron ore prices. Isn’t the market completely disregarding the value of the steel plant? Even if the steel plant fetches 1/3rd of the capital employed in erecting it, it is still good value for the investors in my opinion.

Since the govt seeks a good dividend payout from the NMDC, I feel NMDC is at the very least a much better investment than a bank FD with a decent dividend yield, ignored steel plant investment, and the profitable iron ore mining business.

3 Likes

If the company is sold first it should fetch atleast 32000 crore because NINL was sold by government for 12,000 crore which was a 1.1 MT plant.NMDC steel plant is new and hence should atleast fetch 3/1.1 *12000 which is 32000 crore.

If the government sells it first then it would sell it for 32k crore and will give a one time dividend which should make the buy worthwhile.However if the government demerges it first the actual price may not be reflected in the share price which would not make it a compelling option.

1 Like

The plant wont get sold at subpar value .NINL which is 1.1MT got 12000 crore valuation.The seller again was Government .The stock seems undervalued but a lot depends on when the demerger takes place.If the government sells it’s shares to a strategic buyer the stock price will become equal to the Private equity price(generally).

How would the core biz be valued is the major question here.

1 Like

Agree with all the points. As I said earlier too, I also believe it is undervalued. It’s just that it’s hard to know how much it can go up given the uncertainties. There are two risks - iron ore price crash and some legal/policy judgment (like it happened with Donimalai). But I think the chances are somewhat remote for either. So yes, certainly worth investing in. I am invested myself. But it’s also been a good lesson for me to take most profits off the table on PSUs when they go up a lot. In hindsight, I should probably have sold off completely (sold partially) when it ran up to 190-200, and then got back in when it went down to 110 levels.

No, NINL also had attached iron ore mine at old rates.

The value was in the mine and not the plant.

Here, for NMDC plant, they are not giving any mine with it.

If it fetches even 6000 crore/MT, it will be a great price.

And, the govt may ask NMDC to spend that money to acquire some other sick steel govt company or to acquire assets overseas.

Very poor corporate governance of govt companies. One of the worst promoters.

4 Likes

The article is self explanatory.

64th AGM meeting link - part of this few of share holder questions are answered by management - navigate at 01hr:36min to watch through Q&A commentary -

things that pretty much covered are -

Demerger status, future vision, Capex plans, NINL production timeline, domestic steel demand, financial questions etc…

Take a watch, you will definitely like the session.

Disc - Invested from 2021 and enjoying dividends, have plans to accumulate more

1 Like

Thanks for sharing this. Unfortunately, the CMD says they are now hoping to commission the steel plant at the end of this financial year! That’s another 6 month delay. Also interesting to know their plans to prospect for lithium mines even though it’s early stage.

Gents:

Please be careful while estimating when the steel plant is getting commissioned.

I have spoken to one of the major equipment suppliers to the Nagarnar steel plant.

He said the steel plant in its entirety is far from getting commissioned!

Please note he was talking about the complete plant. Piecemeal commissioning can happen before that.

FYI.

4 Likes

While the usual issues associated with government owned businesses such as slow decision-making, bureaucratic interference, etc. are all applicable to NMDC as well, there is another side to all the negativity and criticism.

There seems to be quite a bit of misconception regarding NMDC’s Nagarnar Steel Plant. The project has been criticized for being highly delayed. But it is not an easy project to build. If memory serves me right, the last greenfield project successfully commissioned in India was the 6 MTPA plant of Jindal Steel & Power in Angul Odisha way back in 2013.

To the best of my knowledge, not a single greenfield steel plant of any meaningful size has come up in India even from the private & public sector in the last decade. Even POSCO Steel, Korea has struggled for years. Arcelor Mittal had to buy out Essar Steel to enter the Indian market.

Firstly, the entire plant is being constructed in an area called Jagdalpur in Bastar district, which happens to be in the heart of the Naxalite zone with negligible infrastructure and rail / road connectivity in the surrounding region.

Secondly, this is an integrated iron and steel plant, which includes conversion of iron ore to iron to raw steel to hot rolled steel and finally to specialized steels. This project includes a power plant to supply at least 40% of the total power requirement of the plant, an internal railway line, plus a large township complex. For more details on the size and scope of the project, you can refer the environment clearance report from 2014:

Q.1 Why construct the steel plant if the location is so difficult then?

Primarily, three reasons:

- Large Indian Steel OEMs like JSW are doing backward integration by getting into mining operations. Naturally, if your large customers are increasingly investing in backward integration with captive mineral supplies, then as a mining operator NMDC will be compelled to plan for forward integration to secure consumers of their iron ore.

- NMDC is a highly cash rich PSU. All the investments in the steel plant have come from internal accruals.

- Access to high quality iron ore from NMDC mines in Chhattisgarh in the neighbouring Dantewada district.

In general, iron ore is of different grades:

- Magnetite: 70-75% concentration of Iron (Fe)

- Haematite: 60-70% concentration of Iron (Fe)

- Limonite: 40-60% concentration of Iron (Fe)

- Siderite: 40-50% concentration of Iron (not worth mining)

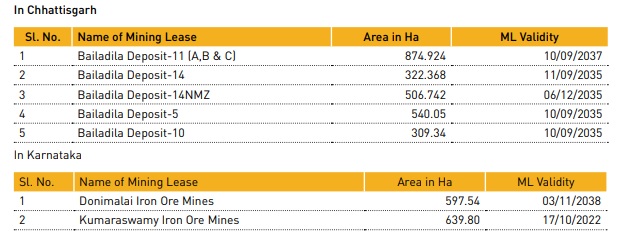

Please refer NMDC Annual Report 2021, Page 8:

- Baila ROM: 10 mm to 150 mm size with Fe 65.5%

- Baila lump: 6.3 mm to 40 mm size with Fe 65.5%

- DR CLO: 10 mm to 40 mm size with Fe 67%

- 10-20 mm Baila Sized Lump: 10-20 mm with Fe 65.5%

- Baila Fine: -10mm with Fe 64%

- Doni lump: 6.3 mm to 31.5 mm size with Fe 65%

- Kumaraswamy Lump: 6.3 mm to 31.5 mm size with Fe 64.5%

- 10-20 mm sized Kumaraswamy Lump: 6.3 mm to 31.5 mm size with Fe 64.5%

- Doni Fines: - 10 mm with Fe 64%

- Kumaraswamy Fine: -10 mm with Fe 64%

As can be seen, most of their iron ore is of high quality in both Chhattisgarh and Karnataka.

Usually, people would associate mining with digging deep in underground tunnels. However, most of NMDC’s mines are open-cast (Refer the image on page 10 of Annual Report 2021).

A combination of high-quality iron ore accessible above the surface level makes mining a lot easier and cheaper as compared to extracting minerals from rocks deep below the surface, which gives NMDC a major cost advantage.

Q.2 Is this cost advantage sustainable?

Please refer Annual Report 2022, Page 35: NMDC has mining licenses for most of their mines till 2035-2037. Therefore, this advantage may be sustainable for a long period of time.

Q.3 How are the raw material supplies be secured if the Mining and Steel businesses demerge?

Annual Report 2022, Page 24: Shared Assets

NMDC and NSL shall enter into shared services agreements and long-term supply agreement, as may be necessary, on terms and conditions that may be agreed between NMDC and NSL and on payment of consideration on an arm’s length basis and which is in the ordinary course of business.

Q.4 How has NMDC constructed this project without any know-how on setting up a steel plant?

The complete project consultancy, plant design, evaluation of suppliers and tenders, inspection and supervision of commissioning has been outsourced to MECON Limited. MECON is another PSU under the Steel Ministry and has been primarily responsible for setting up and modernization of almost all the steel plants of SAIL – Durgapur, Burnpur, Rourkela, Bokaro, Bhilai as well as RVNL and RINL.

In simple words, NMDC spends the money, but MECON is the technical brains and decision maker behind the project. And MECON has more than enough experience in setting up steel plants of all kinds in India.

Unlike some of the private sector companies which have bought Chinese equipment, NMDC’s Nagarnar Steel Plant has a lot of equipment from Tier-1 European OEMs like SMS Group (Germany), Danieli (Italy) and Primetals (Mitsubishi-Siemens). Many of their auxiliary packages have been set up by Tier-1 EPC contractors like L&T (Eg. Water Treatment Plant) and Tata Projects (Eg. Blast Furnace).

Q.5 Does this Iron & Steel Plant have any meaningful functional value?

While the project has definitely gotten delayed which has increased the cost beyond their original target cost, a new plant constructed by Tier-1 companies is definitely valuable. Since this project has been funded mainly from internal accruals, interest cost burden isn’t very high.

The total project is spread over 1980 acres, which leaves enough land for brownfield expansion in future to upgrade from 3MT to 5-6MT capacity. Any future expansion will be a lot easier as most of the utilities such as roads, township, etc. are already built. Jagdalpur now also has an airport with a daily flight from both Hyderabad and Raipur.

Q.6 Valuation:

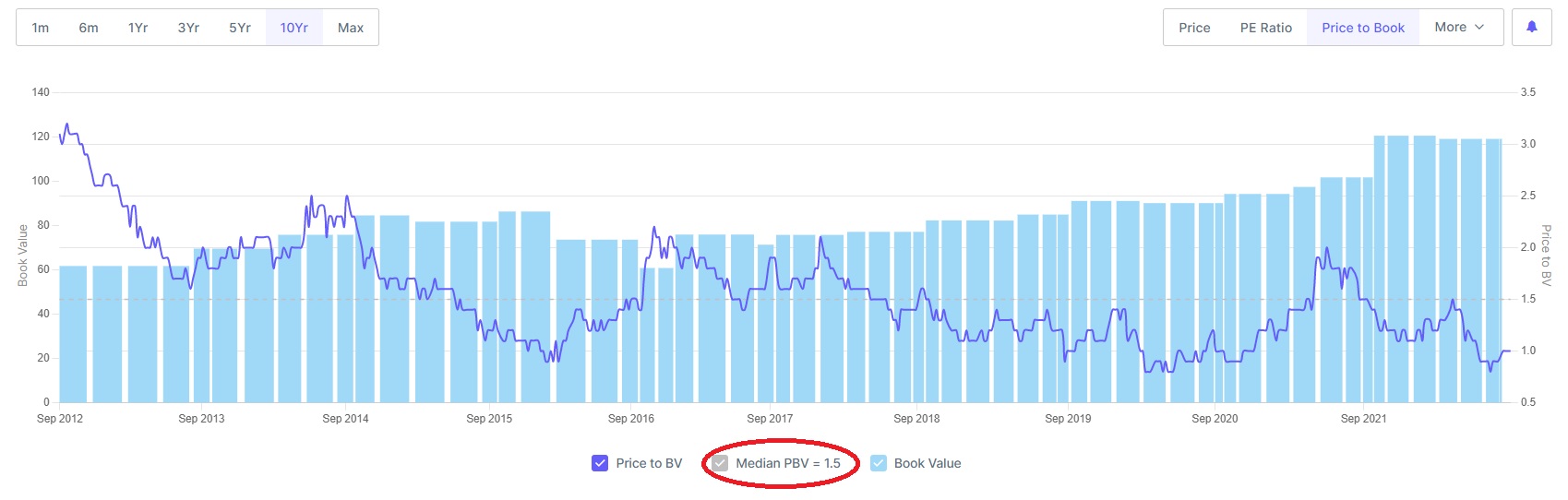

NMDC’s 10-year median Price to Book value is 1.5 (Source: screener.in). Currently it is at P/B = 1. This P/B ratio is based on NMDC’s March 2022 balance sheet where their fixed assets are Rs. 3,966 crores. The complete investment in the steel plant is shown in CWIP (Capital Work in Progress) of Rs. 18,300 crores. At some point, this Steel Plant will eventually be completed and commissioned. So, this Rs. 18,300 crores will be added to the gross block of Rs. 3,966 crores (less depreciation). Even if the P/B remains at 1, which is at a 33% discount to its long run average, it represents is a significant upside to CMP of approx. 125.

Since the demerger is going to result in a mirroring of shareholder pattern, I haven’t gone into the separate valuation of the two demerged businesses.

Disc: Biased

- Invested in NMDC since over 1 year

- Vendor to NMDC Nagarnar Project for plant & machinery, with regular onsite visits by my team at site for machinery installation

56 Likes

such a well and exploratory written statements, I’m much delighted to read this, thanks!

Phew…hats off,delighted to see such 1st hand inputs and that too from someone, who has skin in the game

Great analysis. Thanks

So as per your own assessment of the whole situation, when do you think the plant will be commissioned commercially?

I have been careful to only share information that is already in the public domain. Due to the existing business relationship with NMDC, I won’t be able to answer your question. Please ask the company’s Investor Relations department regarding the steel plant commissioning date and commercial production.

5 Likes

How the above stands in current times? Does it limit the number of bidders?

Great analysis.I have been closely following NMDC because of two reasons

1)Radhakishan damani buying shares

2)The demerger of steel business could trigger an open offer for the shares of the steel plant in the hands of the public from private steel business.

However it is difficult to value the core iron ore business.What do you think is the scenario of the iron ore price in the near future…

I guess Mr Damani’s name appeared in April 21 shareholding pattern (May21 was highest price NMDC traded in last 10 years) and since then I could not find his name in NMDC shareholder list.

@Surender : Your question isn’t very clear, but I’m assuming that you are referring to the bidding for the prospective privatisation of the steel plant. Firstly, I definitely would not make any investment decision on based on this news considering the government’s sketchy track record of PSU privatisation (BPCL, SCI, BEML, etc.). The poor accessibility was the history of the location and not the current status. The mines are operational since several years and thousands of crores of equipment have been delivered to the steel plant. So it is obvious that the roads have been built by now. Both Transport Corporation of India (TCI) and Associated Road Carriers (ARC) have full fledged transport hubs in Jagdalpur. You can look up their Branch Office Locator for PIN Code 494001. Having said that, the rail network is still quite poor in this region owing to a topography of dense forests. So there is scope for improvement of road / rail infrastructure. But that’s not really in direct control of NMDC.

That’s why you need to study their Slurry Pipeline and Pellet Plant projects which will make the evacuation of the ores a lot easier. I will have to write a separate post on both of these, else this will become a very long essay. ![]()

@Gothamcapital: Same reply for your query as above; that I would not make any investment decision on whether any high profile investor / government is buying or selling shares of the company. This is because we have no prior information regarding what price and volume did they enter or exit. By the time the news comes out in public, it is stale and mostly irrelevant.

Regarding the core iron ore mining business, I would not base any investment decisions on the price movement of iron ore as that is akin to astrology.

In order to invest in these types of companies, please study the following:

- Ore quality (concentration of minerals) and quantity of extractable reserves

- Ease of extraction (surface level ores or deep underground mines)

- Ease of evacuation (connectivity to the location of consumption)

- Longevity of the mining license and royalty pay-out to the Government

- Long term tie ups with downstream consumers and ability to be a price maker instead of being a pure price taker (no one can completely dictate prices, but at least they should have some bargaining power)

- Track record of the miner (following environment / safety norms / accidents, etc, relationship with government & people around the plant)

NMDC controls nearly 30% of the iron ore market in India. So it has decent bargaining power, especially with the smaller buyers that they can sell through auctions, since JSW and Arcelor Mittal (former Essar Steel) are now trying to use their own captive mines.

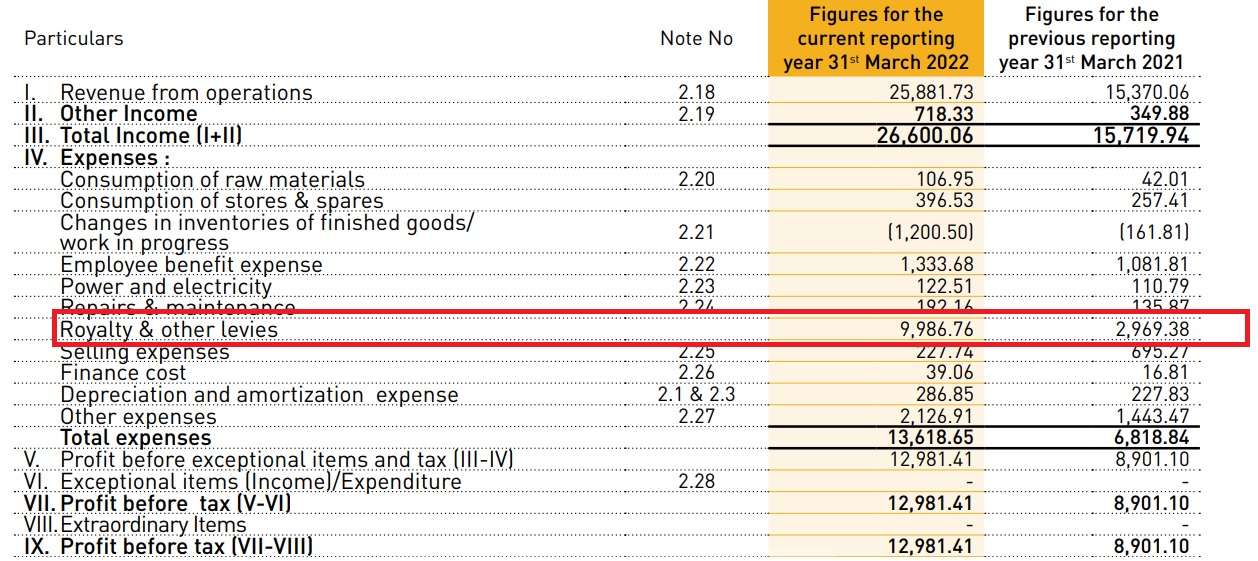

The biggest hit on NMDC’s profitability is the increase in Royalties. From Rs. 2969 crores in March 2021, it has gone up to Rs. 9,986 crores in March 2022.

If the government gets too greedy with royalties / levies / taxes, it can be trouble for the entire mining industry and not just NMDC (remember telecom licences?). On the flip side, it also means that new entrants will find it that much tougher to venture into the mining business and compete with the incumbents.

I read a lot of comments from the investor community that all commodity business are brutal and that any tom-dick-harry can come and suddenly increasing supply. However, that is not a very accurate way of assessing the business especially in the backdrop of high pro-ESG stand by governments, investors and public sentiment. It takes years to operationalise mines or steel plants and start commercial production.

This doesn’t mean that steels and mining businesses should be trading at P/B of 4 or 5. However, I feel that the present share prices are unduly pessimistic. With 12% dividend yield, the current prices offer decent margin of safety ( I of course could be wrong and you need to do your own research).

16 Likes

Thanks, @Viral. I was keen to know whether disturbance due to Naxalite activity is still a significant factor. ’ Lloyds Metals & Energy Ltd’ could partially operate their mines for multiple years due to a similar situation. For example - From the AR of FY13-14: “due to insurrection by Naxals near Surjagarh Iron Ore Mine in which one of the official of the Company was killed, the Mining Operations of the Company at Surjagarh Iron Ore Mine at Surjagarh Village, Gadchiroli District, Maharashtra has been temporarily discontinued w.e.f. July, 2013 and the same facts has been informed to the concerned Govt. Authority.”

Any idea why NMDC not able to scale up its pellet plant even after almost 5 years of operation?

2 Likes