Noticed that Mr. Damani has increased his stake from 0.12% to 0.19% this Quarter:

Q1FY22

Q4FY21

Comparative July21 metrics

The state-owned miner’s iron ore production climbed 39.72% to 3.06 million tonnes (MT) in July 2021 from 2.19 MT in July 2020.

NMDC’s iron ore sales jumped 28.01% to 3.29 MT in July 2021 from 2.57 MT in July 2020.

https://www.nmdc.co.in/Investor%20News/Handlers/DownloadFile.ashx?ID=cf849904-fc40-4bdd-a1aa-a4cdde41e80f

Q1 Concall transcript

The issue with NMDC is its capital allocation mis-management.

It earned huge money over last 10 years, remained debt free.

But what did it do with that money- it built a steel plant which hasn’t added much value.

Also, it gave the money away in Dividends, as govt wants dividends from PSUs.

It spends extra money on CSR, donates to PMCare funds (over and above required limit).

It may earn huge money in coming years, but the issue remains how it invests that cash.

The employee bonuses, dividends, CSR as it did in the past? or some better use of money.

If shareholders are not getting that money compounded for their benefit, then whats the use of that money for shareholders?

Co is still planning to do capex in new steel plants. Captive iron ore by steel players is major risk. JSW and Essar both have captive iron ore mines now. Sales volume didn’t go any where in last 10 years. Unable to ramp up pellet plant speaks about poor execution and PSU work culture.

Since, iron ore mines are being sold at 120-140% premium and production of those mines is very limited, the risk of lower volumes of NMDC is minimal in coming yrs.

Volumes didn’t increase because of Donamalai mine issue which is solved now I guess but at 22% additional royalty.

Owning an iron ore mine is a very asset light, high free cash flow business. But the company that owns the mine should be able to utilize the free cash flow in building assets that further generate free cash flows with high margins for the shareholders.

Incremental return on capital is non-existent in case of NMDC so far.

What is the value that you ascribe to the steel plant?

I think the minimum 5% of net worth or 30% of PAT to be distributed as a dividend has been a really good move by the government. Dividend/Buyback is probably the best way to allocate capital in companies like NMDC.

At least the book value - Capital WIP can be taken as a benchmark valuation probably. Anything more than that is a free topping on the pizza

But in current market capitalisation its not even worth 50% of book value. Cost incurred by co has been including preoperative expenses which get capitalised. So the inefficiency of the management is hidden in CWIP and market is rightly (most of the time) discounting the same.

State-owned mining company NMDC on Tuesday slashed prices of lump ore by Rs 750 a tonne and fines Rs 200 per tonne, with immediate effect.

In a regulatory filing, the company said it has revised the rates of lump ore or higher grade ore to Rs 5,200 a tonne.

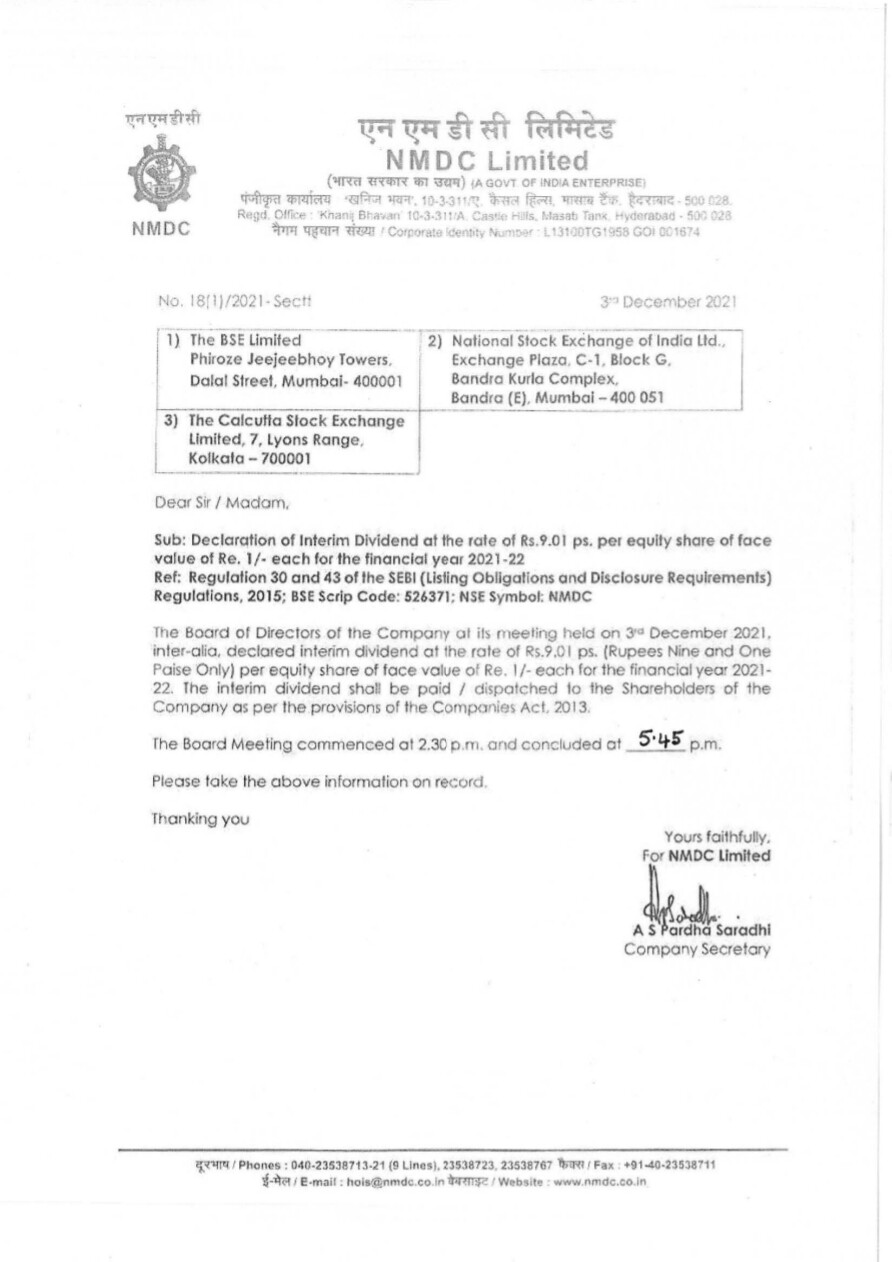

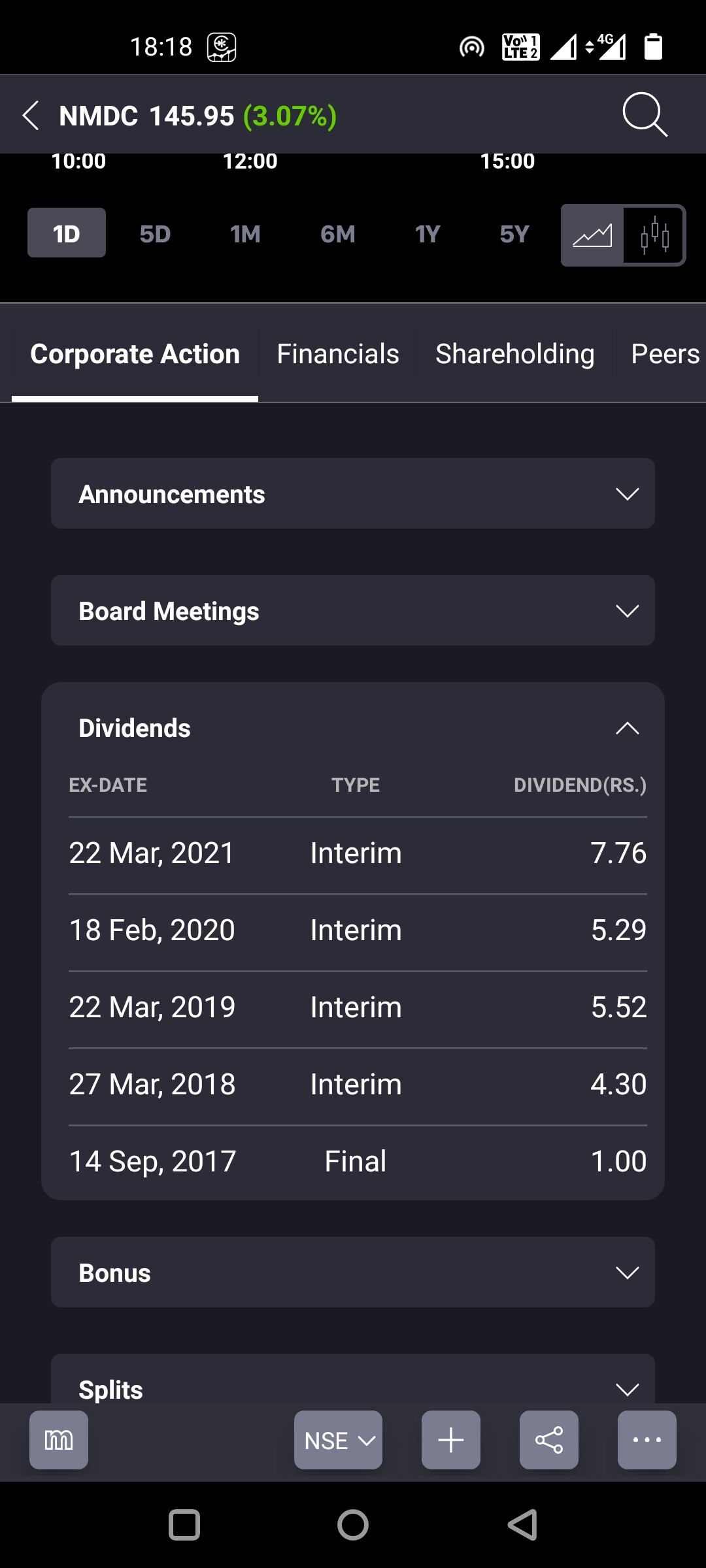

NMDC has declared a dividend of Rs. 9 per share. On today’s closing share price of Rs. 146, this translates to a yield of 6%.

This is their highest dividend in the past 5 years as per moneycontrol.

Another thing that I noticed is that, in the recent past all dividends have been given in Feb or March but this has been way before. So, we could have another dividend for the year. This is probably because of the dividend policy that govt. has initiated.

This was the headline back in 2017

2017 headline

So, my question is - was there so much of delay?

And the demerger, as you can expect in India, is opposed by the workers

A 1 MT plant is behind sold for 12000 crs. The plant has over 6000 crs. of debt and huge accumulated losses. The plant is old and a part of its is shut down. The machinery is relatively less efficient.

The NMDC plant is of 3 MT. Has a fresh slate without negligible debt. The machinery is new and has the latest technology and is thus far efficient. Just extrapolating that, NMDC plant’s value can come out to be 36000 crs. The market cap of NMDC is at 40500 crores. Am I missing something?

Here is another article that gives more information regarding the NINL deal.

Following are some interesting points from the above article:

Central PSU Minerals and Metals Trading Corporation (MMTC) is the largest shareholder of NINL having a 49.78 per cent share, apart from NMDC, which holds 10.10 per cent.

Does this mean that NMDC gets 10% of the 12000 crores?

According to the preliminary information memorandum circulated by the department of investment and public asset management, the successful bidder will get full ownership of the company, apart from the mining rights and leasehold land spread over 2,500 acres.

However, the biggest asset of NINL, which makes pig iron and long products , appears to be the land in Kalinganagar, apart from a captive iron ore mine.

Tata Steel has a strong presence in Odisha where it operates a 3mt plant at Kalinganagar. It is being scaled up by another 5mt. The company has expressed a desire to bid for NINL because of the strategic fit to the existing unit, apart from increasing exposure to the long products.

Tata Steel Long is buying Neelachal Ispat Nigam(NIN) at an enterprise value of 12K Crore. Note that the debt in the books of NIN is at least 6500 Crore. So the actual cash payment upon acquisition to existing share holders will not exceed 5500 Crore. NMDC is likely to get 10% of the equity value amounting to 550 Crore.

AJ

Disclosure: Invested in NMDC from lower levels.

But NMDC investment in the company is ~100 Cr. So overall it should be a good outcome for the company. Not very material, but can be a part of the next distribution.

Just read about the politics - CG CM and local Junta working there don’t want privatization and they are saying that openly .

there were even news CG Gov will buy it from centre …lol…

I find it hard to see they will be able to sell easily.