On an avg, it is 15% of the price of the iron ore mined for NMDC.

So 15% of that, converts into 22.5% of additional duty.

Following is the text of the latest MMDR Amendments as introduced in Lok Sabha

The bill has already got approvals from both the houses.

The recent price hike by NMDC (price inc by 19% in lumps and 11% in fines) seems to be the action by the co. to pass through some part of the additional premium under the MMDR Amendment 2021

With economic relationship between Australia and China are not going great as of now, Iron ore is having a good time. NMDC is mostly domestic supplier and barring RINL (PSU entity) almost all of its large customers are getting self reliant putting a volume risk.

I am looking for exit strategy since I am not comfortable with its management which always over promise and under delivered, having a very poor execution strategy in respect of its steel project.

I am not a technical guy but NMDC has given a multiyear breakout on charts so is it advisable to ride the momentum till it last

NMDC conducted an e-auction on 23 June’21 for 105,000 t of iron ore slimes (Fe 57/58%) from its Bacheli mines in Chhattisgarh. According to sources, the entire quantity received bids at INR 3,020/t (basic, excluding royalty, DMF and NMET) against the set base price of INR 2,800/t.

Source: steelmint

Auctions are saying that still consumers are paying higher than base price and these prices may sustain in short term if not increased…

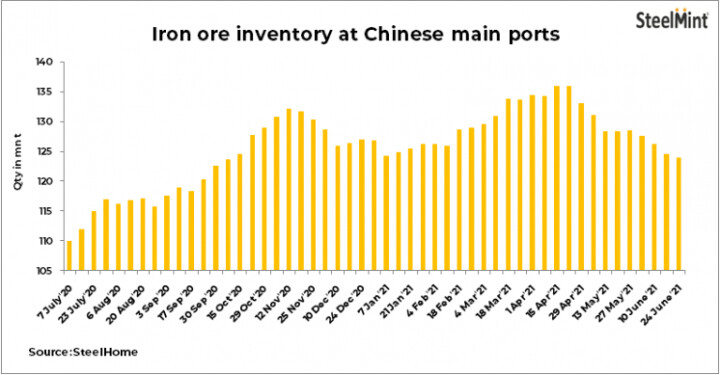

Chinese ports iron ore inventory also in decreasing trend

Management during concall says changes additional royalty of 150% (22.5%) cannot be fully passed through. Sharpe increase in month of April and May may be a step because of higher royalty. As far as my earlier understanding NMDC prices are excluding royalty, DMF etc.

This news gone out of site due to OFS issues…

Many triggers such as steel plant commissioning demerger, Donimalai mine new revenue stream, bailadila mine LOI are being ignored by market…?

I think the OFS floor price was 165, correct? Is that why the share price tugged that price when the GOI offloaded the shares in the open market as they sold roughly 7% shares in the co?

Anyway, definitely looks like market is ignoring the steel plant, increased rate of iron ore, LOI for Bailadila. If they keep up the earnings, we can expect a decent dividend next year.

There is no cash consideration involved in the Scheme.

As consideration for transfer and vesting of the Demerged Undertaking into NMDC Steel, NMDC Steel Limed shall without any further application or deed, issue and allot 2930605850 equity shares of face value of INR 10 each as consideration to each equity shareholder of NMDC Limited, whose name is recorded in the register of members of NMDC Limited as on Record date, in the following manner:

"2930605850fal(y paid up Equity Shares of INR 101- each of NMDC Steel Limited shall

be issued and allotted to the Equity Shareholders of NMDC Limited, against 2930605850

fully paid up equity shares of INR 1- each held by them in NMDC Limited.,

Whether listing would be sought for the resulting entity

The new shares of NMDC Steel Limited to be issued and allotted to the shareholders of NMDC Limited a consideration under the scheme would be applied for listing on all the stock exchanges where the existing equity shares of NMDC Limited are currently listed.

This is still subject to various approvals SEBI,MCA, GoI etc etc. I think the time taken for the same should be 9-12 months.

Its a 3 MTPA plant company has invested close to 17k crs of equity and around 1k of debt. Current Replacement cost will be around $3bn i.e. 22k crs. This is subject to true price discovery, but if the govt. simply asks SAIL to take over because is a naxal infested area then it could be lower. even at 15k crs realisation the value would be close to Rs 50/share.

This based on an assumption that the plant will have a Iron ore mine for captive consumption.

NMDC will also get some money from sale of NINL they hold ~12% eq in the company and some 100crs of debt. NINL has a capacity of 1.1mn tonnes and a captive iron ore mine.

In the conference call it was clear, that transactions between steel plant and NMDC Will be at arms length basis. No special mine will be allotted to the steel plant.

The plant is not commissioned yet, if I am not mistaken. Can the plant be run profitably? What are the problems caused by running a plant in a volatile region? Didn’t the state of Chattisgarh offer to buy the plant as they wanted to keep it as a public enterprise? Lot of questions on this demerger.

I really feel that this plant will go to Sail and NMDC will get the value that it has invested. In this region the locals dont trust pvt. companies much. That is the reason why TATA couldnt enter CG. I’m sure that this plant is a very valuable asset and none of the big guys (Tata, Jindal, Arcelor Mittal, Vedanta or Sail) will just let it pass.

So far NMDC has invested about 16.5k crs and debt of around 1k crs. This is what the company will get in the worst case scenario.

Also a point to be noted this plant is not yet operational and the plant has faced cost overruns. Generally a pvt company sets up a 1MTPA plant for around $700mn but it seems that NMDC’s cost is about $900mn.

there is strong possibility that iron ore price will sustain around present level for a year or two atleast considering opening up of all economies… China’s present RRR cut indicates that liquidity would be abundant an so as the commodity prices…

Does anyone know how exactly the bid premium works. What is the basis of IBM price.

As per my understanding the companies who have mines under the old regime will benefit immensely.

Sail mines 58mn tonnes and Tata Steel mines 38mn tonnes. They will keep enjoying super normal profits till the lease of these mines expire.

NMDC will benefit because small players are surrendering iron ore mines taken during the auctions. For that matter even JSW might surrender two mines with 125% & 140% bid prem,