Will it be in the best interest of both the state and central govt to restart the operations quickly or will they let it drag out? Aren’t the laws in favour of NMDC as the central govt has modified the laws to make it mandatory for state governments to renew the lease? How can a state govt renew the lease then revoke the lease and then auction it? Am I understanding it correctly that at 80% royalty only a captive mine for a steel plant will make sense?

One of my assumptions for investing in NMDC was that there will be much fewer regulatory issues since the company is government owned. My assumption has turned out to be disappointingly incorrect.

So when you say district level, is it the district causing the issue? I am not sure I understand how they have any say over the matter.

1 Like

Earlier it was due to State Govt wanting 80% royalty , which was not acceptable to the company.

Now its about the number of years the lease to be considered , NMDC doesnt want the years mine was not operational to be counted in the lease period and is seeking extension .

Stata Govt has come back with reduced number of leased years + 22 % higher royalty .

2 Likes

But if royalty is not an issue, why can’t they be allowed to operate the mines while the discussions are continued in parallel? I got the impression from reading the above article that there is some objection raised by the state government as the promised committee to finalise the premium amount is yet to be formed by the central govt. The premium of 22% is an interim rate and not the final rate. Anyway, it looks like lot more questions than answers right now. We might need to wait for more clarity.

4 Likes

Investing in NMDC at the current juncture comes with a lot of uncertainties but if someone is WILLING TO TAKE THE RISK, following is my analysis which can help in calculating the underlying risk. (Please read my next comment before you read my following analysis)

Please note that I have tried to calculate risks and one can increase or decrease the risks given the knowledge they have about the sector.

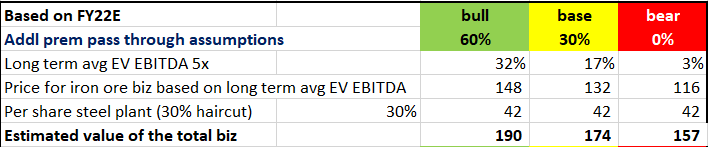

Risk no.1: What if the iron ore prices corrects upto 30% from current levels?

Analysis: At the current iron ore prices, NMDC can achieve EBITDA to the north of INR 42bn in Q4(it made INR 27bn ebitda in Q3). Just FYI, INR 42bn is almost 68% to the EBITDA of what they generated in FY20. But let’s add some risk element to this. Let’s say the iron ore prices drop (because of x reason) by 30% (current avg of lump & fines iron ore prices of nmdc is ~INR 4655/T). Based on that and taking 38mn tons sales vol for FY22 (conservative no. against 40mn guided by the management), the company shall make an EBITDA of ~INR 8700cr in fy22e.

Risk no.2: Levy of additional premium of 22.5%

Analysis: Let’s take 3 scenarios here.

Bull scenario: 60% of 22.5% will be allowed to be pass through

Base scenario: 30% of 22.5% will be allowed to be pass through

Bear scenario: NO pass through, i.e., entire 22.5% will be reduced from company’s ebitda

Please note that the in the latest concall the management stated they ‘guess’ that there would be some pass through of the 22.5%.

Continuing with our arbitrary assumption of 30% drop in iron ore prices, the Company will be able to generate INR 7500cr in Bull case, INR 6700cr in Base case and INR 5872cr in Bear case for fy22e.

Following is the valuation worked by me after implementing the aforesaid risks:

(the company’s long term ev ebitda multiple is 5x) (assumed 30% haircut on the steel plant)

3 Likes

Above analysis is just for calculating the company’s downside risk. It doesn’t make sense to race blindfolded. We need to have some basis to invest and hence I thought of calculating the risk, obviously with some assumptions. Comments and feedbacks are welcome. One can have a different view such as: iron ore prices corrects by 50% or Sales vol expected at less than or more than 38mn tons etc etc.

You can put your input and see what price you derive based on that. Above analysis is to compute the DOWNSIDE PROTECTION with some NEAR TERM view.

Thanks.

Disc.: Invested

In valuation, earnings matter but what also matters is capital allocation. NMDC in their recent concall mentioned that they will invest in their steel plant as part of upcoming Capex. This is a U-turn considering they would like to hive off the steel plant and get its own listing benefits. Considering the hike in iron ore price, ideally any shareholder friendly company would like to invest this upcycle gains in areas where they can do capex to generate value for shareholders. NMDC is undervalued by market considering their treatment of minority shareholders.

-

NMDC has a overhang of government policy. In the concall, you can sense Sumit Deb’s uneasiness to answer about concrete decisions of Royalty.

-

NMDC already spent 17000 cr on steel plant and there is another 5000cr expected capex. The plan is to use some of the earnings to complete it and probably start operations by July.

-

NMDC shelled out 3% on CSR when the minimum expected is 2% and received best PSU in CSR category. The focus is more on the buyback and CSR rather than minority shareholder interest. Like HCL Technologies marked 700 crores as bonus for its employees to mark their 10 billion dollar market cap achievement. It is a nice gesture eventually benefiting whole ecosystem.

-

Companies like HEG and Graphite India made merry during graphite electrode upcycle but here NMDC’s wings are clipped…overhang on exports quantity and tax…

At one point of time, NMDC has 19000 cr cash equivalents. 53% of its market cap. If you can do valuation based on these metrics, I am sure, the number will be much bigger.

Yeh muskaan ki chamkaan kahi aur…

Disclosure - Invested

3 Likes

I personally see this as a negative. NMDC need to focus only on mining. The company has not been strong in project execution on time and within budget.

2 Likes

Yeh muskaan ki chamkaan kahi aur…meaning?

In response to your steel plant capex, just fyi, residual capex is to be financed by debt which shall be taken in the steel subsidiary’s books. It’s clarified by them that no further amt shall be invested in form of equity by Nmdc.

2 Likes

I mean to say the main focus of the company is elsewhere.

Regarding Capex, I am referring to the below concall transcript.

Saket Kapoor, [17] -------------------------------------------------------------------------------- And on the utilization of cash, sir, what is your – incremental cash and the entries we have grown with a buyback earlier, so what kind of dividend payout can we look with improved enhanced cash flow which we have done for the 9 months, barring the – if you deduct the buyback amount? And going forward, for the fourth quarter also, you are giving a very bullish outlook. So what kind of dividend payout can we look? And sir, in the recent auction, I think, sir, there was some lukewarm response out of the number of rigs offered and the bids which were there. So what could be the reason for that, sir? And my last point will be on the demerger of the steel plant, sir. Are you facing any more headwinds? What is the update on the same, sir? -------------------------------------------------------------------------------- Sumit Deb, NMDC Limited - Chairman of the Board, MD & Director of Personnel [18] -------------------------------------------------------------------------------- Sure. I’ll take the last question first. Yes, the demerger process is on target, and we intend to finish it in another 5 to 6 months period. So that is there. So there is no issue on that count. As far as auctions goes, we have sold all the materials which have been there. So there is no question of any response. Whatever we intended to sell, we have sold. So there’s no issue on that account also. There was a utilization of – you’re talking of cash? Yes, we have the CapEx in place. And apart from that dividend, obviously, we’ll take a call in our Board as and when it comes. -------------------------------------------------------------------------------- Saket Kapoor, [19] -------------------------------------------------------------------------------- So what is the CapEx plan, sir? If you could elaborate for – coming 3 years CapEx, if you can articulate, then we can have a better understanding. -------------------------------------------------------------------------------- Sumit Deb, NMDC Limited - Chairman of the Board, MD & Director of Personnel [20] -------------------------------------------------------------------------------- See, currently, this year, we almost are doing INR 1,900 crores. So next year also, we intend to spend around INR 2,500 crores or INR 3,000 crores. So these are the numbers which you are talking about. -------------------------------------------------------------------------------- Saket Kapoor, [21] -------------------------------------------------------------------------------- And you have the split up on the same, sir? Where are you putting this money, sir? -------------------------------------------------------------------------------- Sumit Deb, NMDC Limited - Chairman of the Board, MD & Director of Personnel [22] -------------------------------------------------------------------------------- So primarily, most of the cash is going into the steel plant. Obviously, but there are steel plants in Donimalai, in Kirandul also, and plus, our Slurry Pipeline Project, the first plant project in Jagdalpur. So all this is going to – I mean we’re going to spend on this CapEx.

Based on the above verbatim, I assumed the earnings(cash) is going towards steel plant. You may be right in your assumption that residual capex is going to be financed by debt but what I mean here is, the earnings during this upcycle are already going to steel plant. So, the residual capex if any will then be financed.

Please correct me in case my understanding is wrong.

1 Like

Yes, your understanding is wrong

Steel plant will be funded through the debt. They have clarified the same many times. No further equity will be invested in the steel plant for the residual capex.

They will need cash for the capex towards their slurry pipeline, starting of coal blocks and other capex given in their Feb’20 detailed presentation. As of Feb’20, pending capex (EXCEPT steel plant) was ct INR 11,000cr which the co. will incur over next 3-4Y from their cash.

Also pls don’t state this ‘At one point of time, NMDC has 19000 cr cash equivalents. 53% of its market cap. If you can do valuation based on these metrics, I am sure, the number will be much bigger.’

That was a diff year and PAST. There was definitely wrong allocation of capital in the past. 17,000cr of capex towards steel plant is a sizeable percentage to their net worth. However, you can’t look at that 19,000cr of cash. That was accumulated because of many good years in Iron ore. As I have stated in my analysis, just 1 quarter will fetch them INR 42bn+ ebitda (this excludes 22.5% additional duty) at the current iron ore prices. Though after removing 22.5% addl duty (once imposed), the cash profits will reduce but still, you can calculate by yourself what the cash profits shall be, if the iron ore prices continues to remain elevated for the next 5-6 quarters. However, instead of that ROSY picture, I thought of a more conservative approach by taking 30% price cut in the current iron ore prices.

Thanks for your responses.

4 Likes

Credit Suisse has initiated coverage on the stock with an ‘Outperform’ rating. It also has a target price of Rs 162 on the stock, implying around 45 per cent upside from Monday’s closing price of Rs 112 on the BSE. Anyone with the details in the report?

Thanks

2 Likes

Donimalai mines restarts after 2 years

3 Likes

JSW contributes almost 25% of the total revenues for NMDC and after winning bids for Odisha Mines, it has taken care of its entire iron ore need. It seems JSW will not take iron ore orders from NMDC once Odisha mines are fully operational in a year or two. I listened to last 3 conference calls with NMDC management and there were few questions around how NMDC plans to sell this iron ore once JSW becomes self sufficient in its iron ore requirement. There was no clear answer around this question by NMDC management and all I could get from their comments is that “It is not a major issue and NMDC will supply to NMDC’s steel plant which is about to be commissioned and to RINL which is currently running only at 50% capacity”.

How can it not be a major issue when NMDC’s new steel plant is of 3mn Tonnes capacity and would require only around 5-6 mn Tonnes of iron ore that too when fully operational, and the situation of RINL is not good as lot of NMDC’s receivables are stuck there.

On the other hand I believe Arcelor Mittal which again is a major customer of NMDC and contributes 20-25% of the NMDC’s revenues, won few iron ore mines in Odisha.

With such major customers (which contribute almost 50% of the revenues) on the way to become fully captive steel producers maybe in next 2 years, and no clear and convincing response from NMDC management on this question of how to replace these top customers, I am not sure what to make out of this.

Could anyone please throw some light on this and help me understand.

5 Likes

The mines won by JSW and Arcelor Mittal were earlier operating merchant mines. While JSW and Arcelor Mittal may not buy from NMDC but the small mills who were buying from these mines will now have to buy from NMDC. So net net no change in India’s iron ore demand and supply. Btw it is cheaper for JSW and Arcelor to buy from NMDC rather than mine from their own mine and pay 100% royalty on market rate. So they will still buy some quantity from NMDC

4 Likes

I have tried to estimate the Revenue numbers with very simple forecasting.

Sale x Average Price = R Factor

Change in R Factor should tie back with change in Revenue over the Qtr.

| Period | Sale Qty (MT) | Price | Qty*Price (R Factor) |

% Change in R Factor over last qtr | Reported Revenue | % Change in Revenue | |

|---|---|---|---|---|---|---|---|

| Q4 2021 | 11.07 | 5,349.44 | 59,218.35 | 156% | 6,314.75 | 145% | Estimate |

| Q3 2021 | 9.44 | 4,017.39 | 37,924.17 | 207% | 4,355.00 | 195% | Actual |

| Q2 2021 | 6.47 | 2,832.61 | 18,326.98 | 117% | 2,230.00 | 115% | Actual |

| Q1 2021 | 6.41 | 2,435.71 | 15,612.93 | 57% | 1,938.00 | 61% | Actual |

| Q4 2020 | 8.57 | 3,200.00 | 27,424.00 | 115% | 3,187.00 | 106% | Actual |

| Q3 2020 | 8.44 | 2,813.59 | 23,746.67 | 137% | 3,006.00 | 134% | Actual |

| Q2 2020 | 5.81 | 2,982.61 | 17,328.96 | 71% | 2,242.00 | 69% | Actual |

| Q1 2020 | 8.3 | 2,954.95 | 24,526.04 | 80% | 3,264.00 | 90% | Actual |

| Q4 2019 | 10.25 | 2,995.56 | 30,704.44 | 3,643.00 | Actual |

With consistent margin (should increase as mining cost do not change with price rise)… Expected NP for Q4 2021 should be ~3200-3500 Cr.

No reason, this stock should not trade at 10 PE for TTM numbers.

Disclosure - Invested and increasing holding.

4 Likes

Ya but such co. can’t buy from nmdc instead of mining from their own mines. There is a min royalty which you need to pay if you don’t mine.

Also, how many cases do we have where we have an operating co not mining and rather buying it from outside

And why would selling output can ever be a problem for nmdc? (just sharing my view. I know that’s not your query. Just extending your point.) Even with exports duty in place, domestic iron ore price would be cheaper than international price on a like to like basis. (cost break up very well explained in the latest Credit Suisse initiating coverage I mentioned earlier). It’s just that as India promote steel and Nmdc is a govt co, it has to first fulfil domestic req. Noone shall prohibit them from exporting if they have surplus ore.

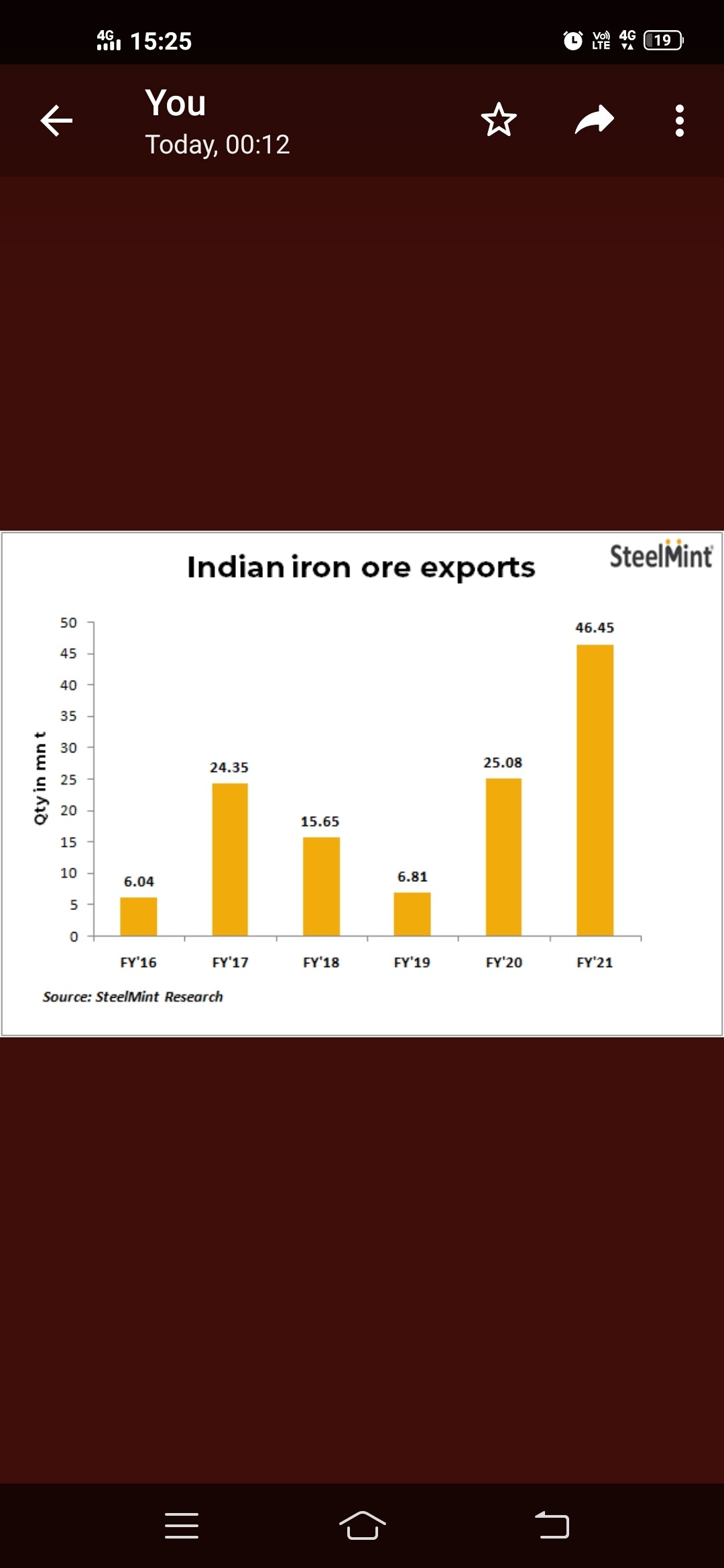

I am attaching chart which shows extraordinary spike in iron ore exports of India in fy21. International markets are more advantageous than domestic.

5 Likes

Can someone please clarify the following:

-

Royalty applicable on Iron Ore and is it uniform across states and

-

I understand from the recent MMDR Amendment Bill (Fifth Schedule) that extension of mining lease would attract 150% of additional royalty payable. So, if royalty is say 20%, an additional royalty of 30% would be applicable. Is this understanding correct?

Thanks

Anupam

1 Like

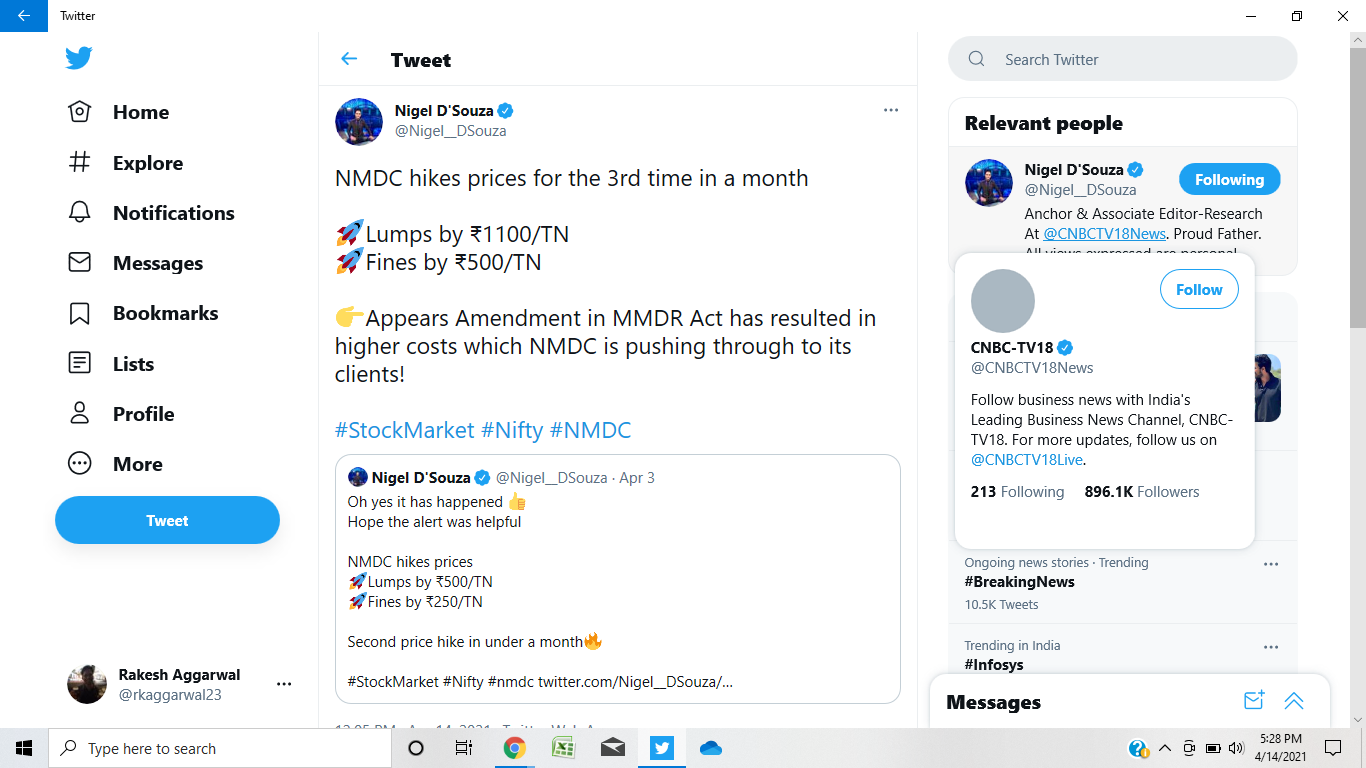

Steelmint: India’s largest merchant and govt-owned iron ore miner, NMDC has announced a second price hike for Apr’21, SteelMint learned from credible sources. The price of DR CLO (Fe 67%) has been increased by INR 1,280/t, Baila lump by INR 1,100/t and that of fines by INR 500/t. The miner’s total iron ore production for FY’21 was recorded at 34.11 mn t, up 8% y-o-y. The recently announced changes in MMDR Amendment Act, 2021 for charging additional amount on grant/extension of mining leases granted after 2015, has resulted in iron ore price hike.

4 Likes