Royalty is not 25 percent higher as in 15 percent to 18 percent. It is 25 percent more as in 15 to 37 percent or almost 150 percent higher. Take average margins right now are 50 percent after old royalty. If you remove 25 percent higher royalty margins will fall to 25 percent or they will half. Considering profit will fall by half it suddenly does not look that attractive like it did a few months back before the prospects of profit falling by half.

2 Likes

Yes, I also feel the talks were about additional premium/duty of 20-25% and as private cos have been paying very high premiums, there is a very high chance of this getting implemented. The concern was that in one of the interview the MD of NMDC said that this won’t be a pass through.

1 Like

I didn’t get your calculation, Can we talk in terms of P&L for more clarity about how profits will become half ?

In FY20

Royalty is = 18% of Rev from operation. (= 2096/11699).

For profits to become half - New Royalty should be = Rs 5205.5

Which is 45% of Rev from operation.

You mean the new one is 27% more on the old one i.e, = 18+27 = 45% ? That means actually 150% hike in the royalty in % term ?

It seems like royalty will be around 22-23 percent higher. from 15 to 37-38 percent. Obviously this is just speculative calculation based on news report and management interviews. In term of profits just reduce ebidta margins by 23 percent to take into account effect of new royalty. Assuming earlier ebitda margin of 50 percent new margin will be 50-23=27 percent.

Then this mining rule change is also on the cards -

I don’t get it whats going on in this sector

Is this consensus now that margins will fall drastically (like from 50% to 27%) , Is it believed to be the case going forward ? Or is it already happening in the mines like Donimalai.

I tried googling about this info, its not very clear whats the resolution about Donimalai. As per mining rule change they might not have to pay and no state gov can ask for royalty hike like Karnataka did but somewhere i see 20% hike in royalty finally get negotiated - which you claim is actually 150% .

I don’t see evidence of all that anywhere.

1 Like

NMDC share buyback proposal of Rs 1378/- crores. 13.12 crores shares to be bought back at a price if 105/- in cash. CMP ~90/-.

Conference call takeaways

Expect good pricing environment to continue due to shortage of Odisha iron ore on

the back of delays in resumption of auctioned mine and high premiums paid.

Management reiterated that FY21 sale will be c. 32mn tonnes, implying aggressive

volumes in 2H. Eventually in 3-4 years it plans to ramp up to c.50mn tonnes (post

doubling of railway line and commissioning of slurry pipeline).

Discussion to restart Donimalai mines is on and expects to commence by end 3Q.

Steel mill demerger to complete in 9-10 months. Current CWIP stands at Rs 172bn

(remaining capex of Rs 30-40bn to be met by debt in steel mill book).

Indicated that buy back is not lieu of dividend (in future board may still announce).

Kumarswamy mine may take 7-8 months be increase capacity from 7mn tpa to

10mn tpa. Karnataka has enough evacuation to support 16mn tpa capacity.

Ex-Steel plant, NMDC would be doing Rs 15-20bn annual capex for FY22-23 (Rs 10bn

each for 3 years on slurry pipeline and Rs 10bn on screening plant).

7 Likes

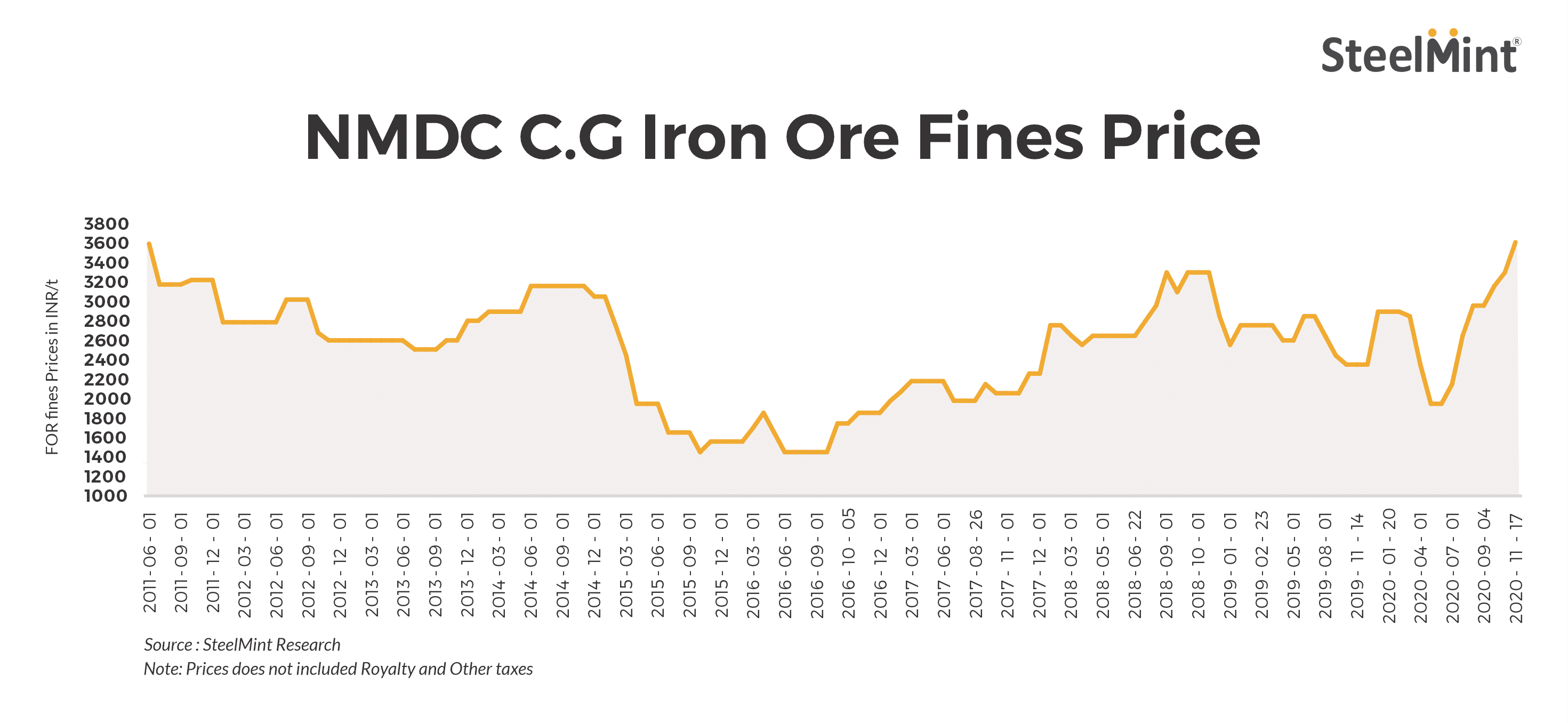

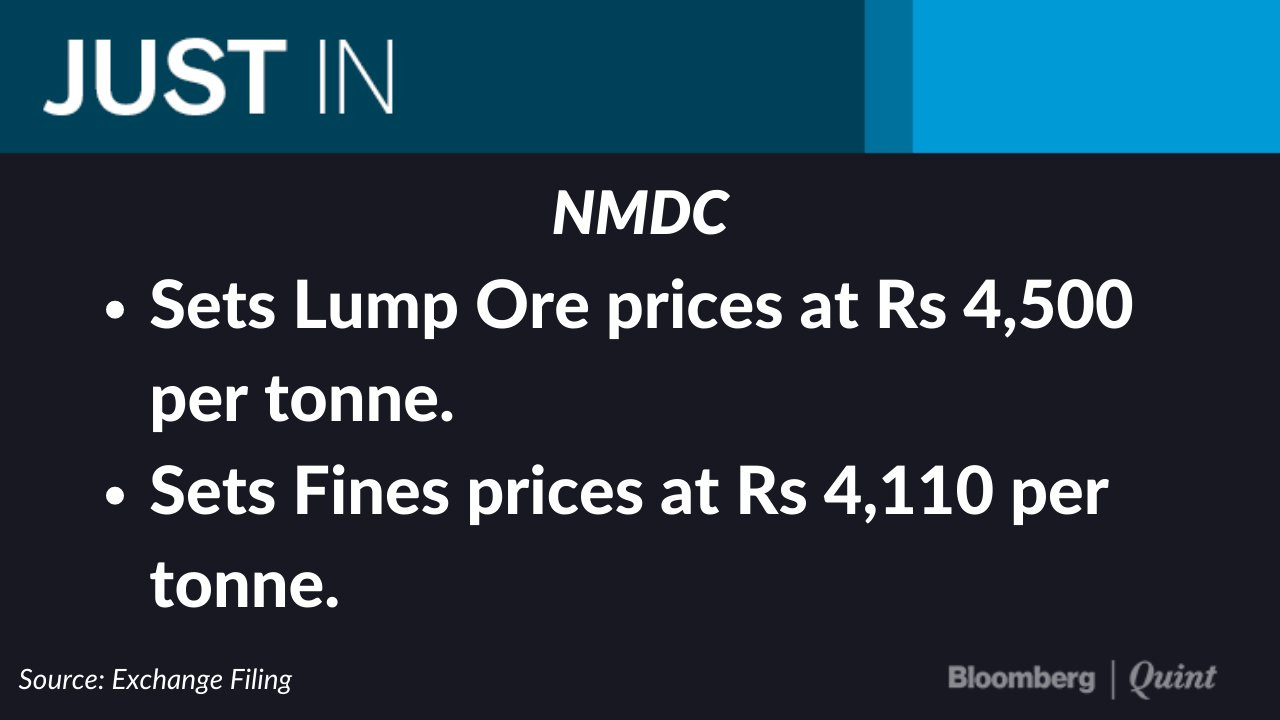

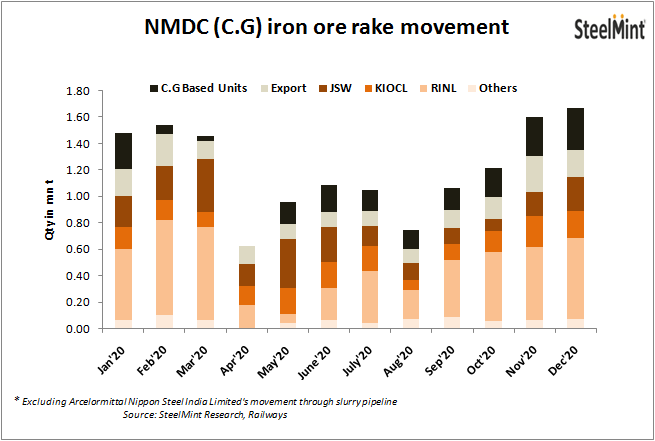

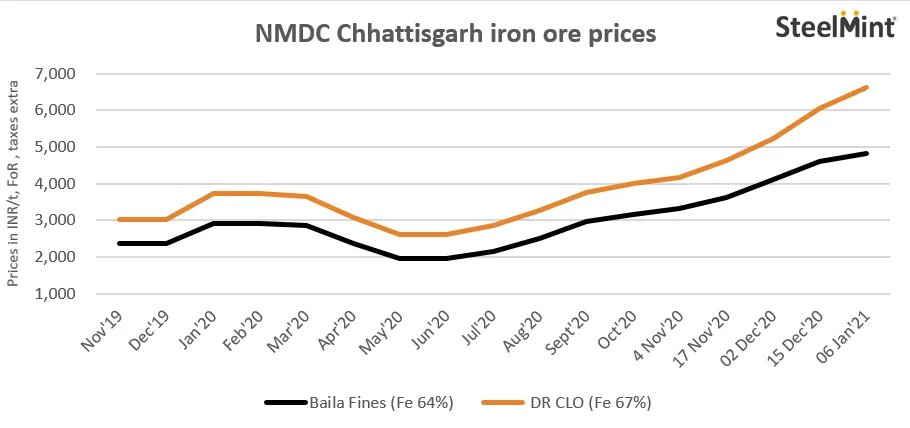

NMDC has announced 2nd price hike iron ore for this month. Prices have increased further upto 11%.

The miner has raised price for Baila fines and lump by INR 300 and INR 400 respectively while that of DR CLO by INR 460/t. With today’s price revision made, company’s fines price has hit an all-time high while that of lumps are hovering close to five-year high levels.

The revised prices for Baila fines (Fe 64%) stands at INR 3,610/t, Baila lump (Fe 65.5%) is assessed at INR 4,000/t and DR CLO (Fe 67%) at INR 4,640/t. NMDC sets prices on a free-on-road (FoR) basis and does not include royalty and taxes.

Reasons behind hike in prices -

Tighter supplies - The Odisha government "successfully"auctioned16 iron ore mines earlier this year. The auctions saw active and aggressive participation from the industry fetching premiums as high as 150%. However, as on Sep’20 only 7, of the 16 mines auctioned, have been able to start production. 2 bidders are unlikely to sign leases and 3 auctioned mines are subject of legal dispute.

The Odisha High Court hearing on plea for extension of timeline for disposal of iron ore stocks with erstwhile lessees scheduled for 16 Nov’20 has been postponed to 20 Nov’20, sources told SteelMint. The stocks, assessed at over 16 mn t, had to be cleared by 31 Oct’20. SteelMint estimates most of these stocks to be of low grade (below 58%) ore and to be difficult to liquidate.

4 Likes

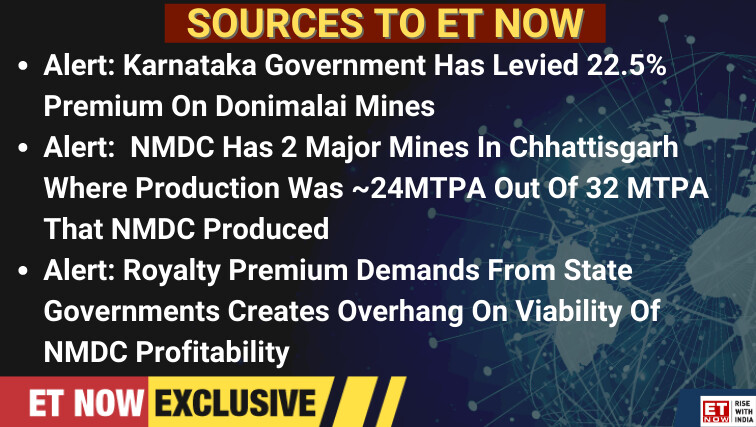

NMDC, India’s largest iron ore producer, can restart the 7mnt capacity Donimalai mine with the Central government’s official stamp of approval to a temporary levy or ‘premium’ of 22.5 per cent of an average sale price.

With an order dated 29 Nov’20, that SteelMint has reviewed, the Ministry of Mines approved this additional premium using its powers to authorise terms different from the established rules and keeping in mind the current “shortage of iron ore”.

This effectively ends the two-year standoff between Karnataka and Centre but comes as a clear warning that mining for NMDC and other central government PSUs will henceforth be more costly.

Consequence

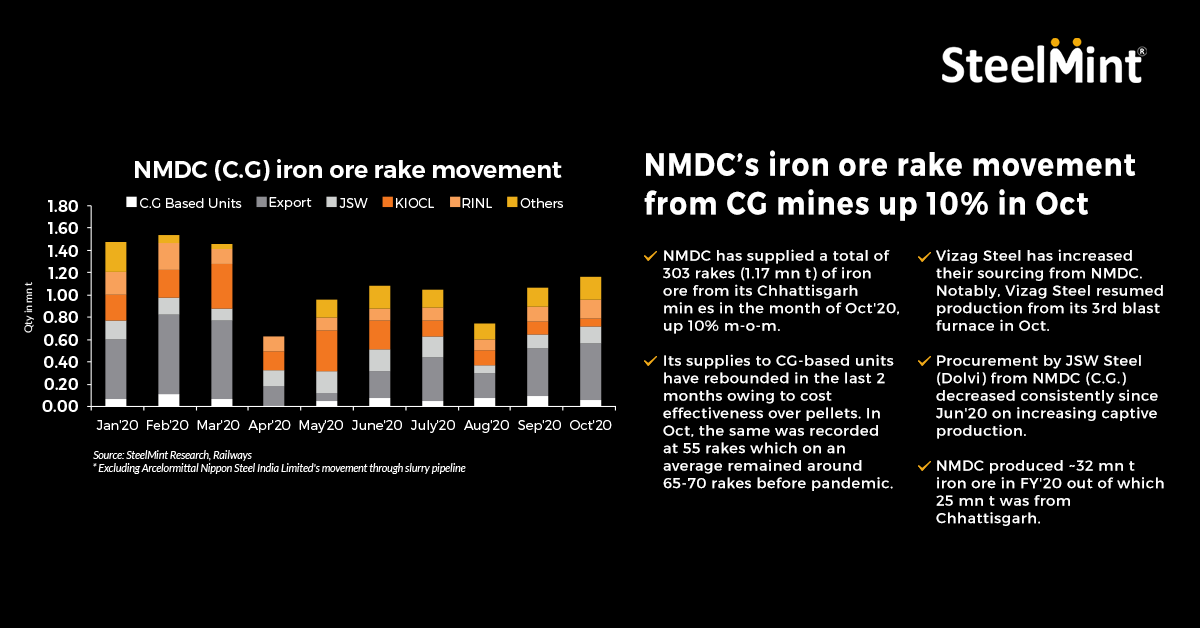

Industry experts expect a demand for a similar additional premium by other states such as Indian National Congress-led Chhattisgarh where NMDC produces 25 mn t annually. In the recent past, the Chhattisgarh government has flexed its muscles halting Bailadila more than once while pointing out how generously it had acted by renewing NMDC’s mines compared to BJP-ruled Karnataka. NMDC is hoping to develop new iron ore deposits in partnership with the Chhattisgarh Mineral Development Corporation.

5 Likes

So, current uptick in NMDC share prices may be attributed to:

-

Iron ore prices going up due to increased Chinese demand and supply bottlenecks. Not sure how long this price increase will last.

-

Buyback of around 1378 crores.

Also, a possible trigger in the future for rerating is the demerger of the steel plant. Not sure how well that will go because plant is yet to be commissioned after multiple delays.

Also, Donimalai mines is again going online after 2 years adding to their earnings.

With the vaccines for covid on the horizon, seems like the company is poised for a re-rating. However, a concern is how well the demerger of the Nagarnar Steel Plant goes. What are the risks related to the steel plant that could affect NMDC? For example, if the demerger doesn’t go through, how profitable or loss making is the new plant going to be? Would be helpful to get the insight of some VP seniors here regarding this.

2 Likes

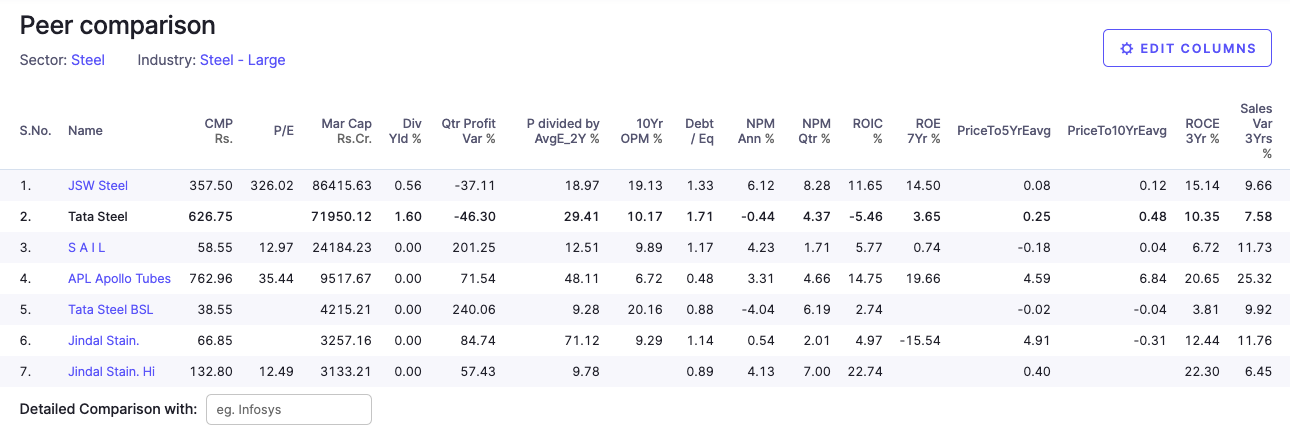

Also, looks like the steel industry enjoys only single digit net profit margins and only JSW steel seems to have ROIC and ROE above 10%.

Hopefully, NMDC will get a decent return for the nearly 15K crore investment in this steel plant. I guess the positives could be captive iron ore. However, the demerged company will be saddled with 5K crore debt but that is not as high as both JSW and Tata Steel Ltd in terms of debt to equity. How much of a difference will that make with respect to finance costs and therefore the profitability of the new steel plant? Will that be sufficient for a good outcome with either the demerger or profitability if the demerger falls through?

Would other steel makers be interested in this steel plant? Does it have any inherent advantages? I guess the idea for this plant was conceived when the steel rates were high. Any chance that the steel cycle is favourable now for the steel plant?

Also, let’s say the company gets only 10K crore back from its 15K crore investment. Then the company is going for 25K crore with an increase in production volume from Donimalai, an increase in iron ore prices minus the increased premium paid to the Karnataka govt.

Also with regards to buyback, would the govt be tendering at Rs 105? Are they obligated to tender their shares because of the buyback offer? Couldn’t they just sell some shares in the open market when the market rate is 10% above the tender price?

1 Like

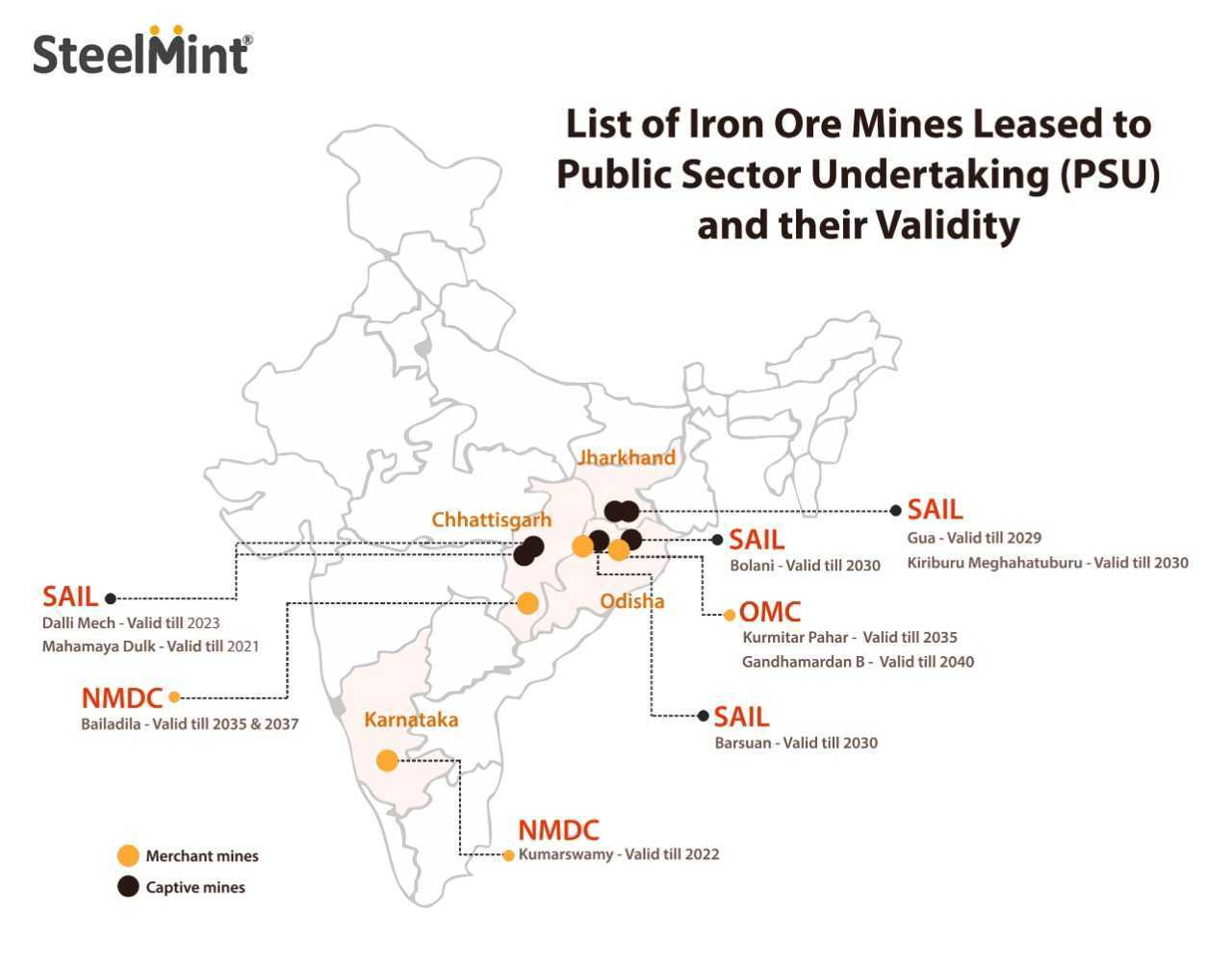

Govt. extends NMDC’s Donimalai iron ore lease after two years suspension Government of India has signed an agreement with Govt. of Karnataka and the Ministry of Steel to extend Donimalai Iron ore lease. NMDC has been operating the mine, but operations were suspended since November 2018. The mine is extended for 20 years with effect from November 2018. Donimalai iron ore mine, which has a total concession area of 597.54 hectares and estimated resources of 149 million tonnes, will increase the annual iron ore production by seven million tonnes per annum.

But what happened to all those pessimism when it was trading around 85-88 ?

States increasing tax ?

Repeat of donimalai issue

Steel companies buying Iron ore mines - becoming integrated players.

PSU - management .

etc ?

1 Like

Market is still pessimistic as it has always been with PSUs. However, when they were trading around 85 and even lower, the iron prices were not as high as it is now. So, maybe that has changed the opinion of the market.

1 Like

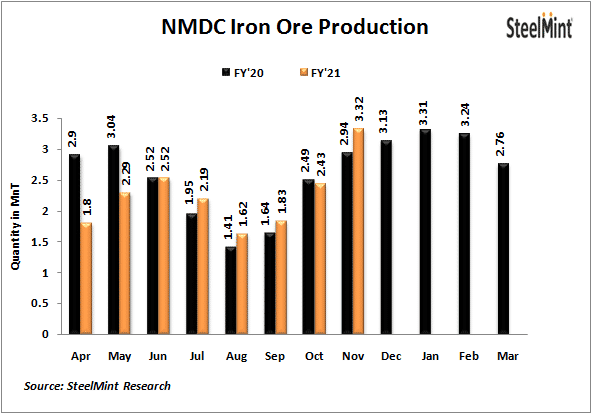

Iron ore production for the month of Dec’20 is 3.86 mn t against the production level of 3.13 mn t in Dec’19, thereby registering a growth of 23.3%. Production volume has increased by 16% in Dec’20 compared with Nov’20.

Iron ore production in Q3 of FY21 is 9.61 mnt against the production of 8.56 mnt in Q3 of FY20, thereby registering a growth of 12.3% against the CPLY.

Iron ore sales for the month of Dec’20 is 3.62 mnt against the sales level of 3.04 mnt in Dec’19, thereby registering a growth of 19.1%.

For Q3 of FY21, iron ore sales stood at 9.44 mnt against the sales in Q3 of FY20 is 8.44, thereby registering a growth of 11.8% over CPLY.

4 Likes

NMDC increases prices for 3rd time in 35 days

Hikes From todayDown pointing backhand index

FireFines +200/tn

FireLumps +500/tn

Reasons

Right pointing backhand indexIron ore shortage

Right pointing backhand indexGlobal iron ore price surge

1 Like

1 Like