Demerger may unlock value to NMDC since it already spend 15K cr on this and market is not valuing it even at 50%. But selling/privatising the nagarnar steel plant is very difficult. Chattisgarh CM (congress ruling state) has already threatened company against privatising of steel plant. They may not renew there lease as well, so it will be very difficult to privatised it.

True. The sale of Nagarnar steel plant is going to be difficult and like @ayushmit mentioned in the recent post above, government may not do divestment due to natural resources. So, 15,500 crore worth steel plant obviously can fetch a good amount of money to central government now. It especially will be seen as national interest by central government to proceed in this direction. On the other hand, iron ore prices in the international markets reached to the earlier peak levels of 2014. I see little downside here due to structural changes happening in Iron Ore industry as well. However, anything can happen.

Disclosure - Invested and add more in last few days

1 Like

Management is saying steel plant may be listed separately mirroring the shareholding of NMDC. Separate plant may not get new tax benefit (lower tax rate 18%) since it doesn’t apply for de-merged entity. This is as per director finance on concall. NMDC will supply iron ore at arm’s length price to steel plant. No capitve mine for Nagarnar steel plant.

No clarity on Donimalali plant. (management is not sounding confident).

2 Likes

2 Likes

How is the steel plant performing

Is it making profits

Or just bleeding for years

All mines of NMDC or it includes other companies too?

I think there are broadly three news items related to NMDC.

- Demerger of steel plant where 16000 cr is spent and not reflected in current valuation. This is positive for existing shareholders as the steel plant will be listed with mirror shareholding and so the listing price can be around 50 rs. Al

-

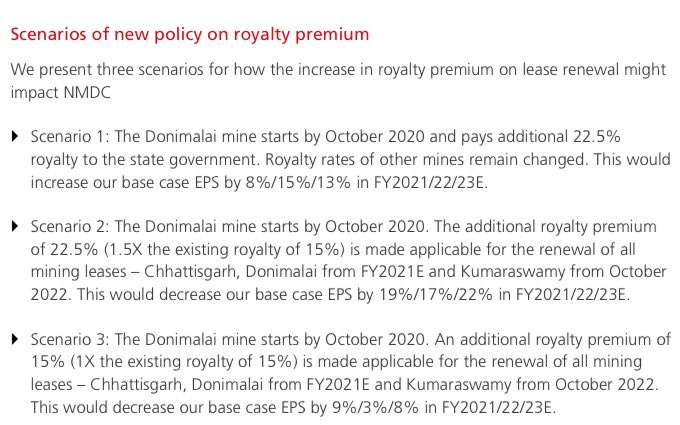

New Royalty premium being asked by states from all PSUs. Here, the decision will be taken in 3 months time. This is negative for shareholders as NMDC has to shell out more premium.

-

Private steel companies like JSW Steel are pushing for reauction of mines held by mining companies. In these times of low GST collection and states looking for more revenue, I think logically this option will be pushed hard. Especially, when there is 250 billion dollar revenue opportunity.This is negative for NMDC shareholders and if worked well, can start glorious steel bull run.

Disclosure - Invested in NMDC and JSW Steel

2 Likes

SteelMint

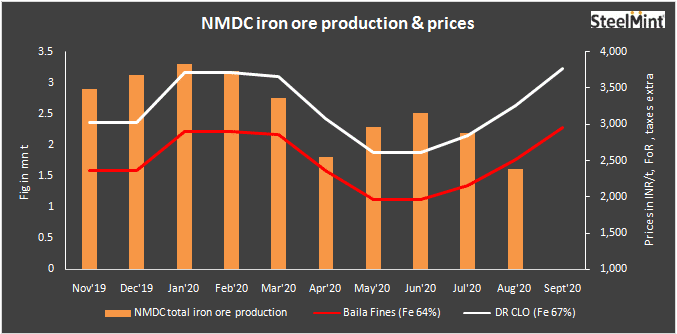

National Mineral Development Corporation (NMDC) has increased prices by INR 290-340/t for Sep’20. The prices for Baila lump and fines have been increased by INR 300/t and that of DR CLO by INR 340/t. Domestic iron ore prices in India have rallied on limited merchant availability in Odisha as most of the auctioned mines are yet to resume production.

The revised prices for Baila fines stands at INR 2,960/t, lump prices assessed at INR 3,250/t and DR CLO at INR 3,770/t. NMDC sets prices on a free-on-road (FoR) basis and does not include royalty and taxes. The miner continued to raise price after two successive price hikes in Aug '20.

Reasons behind hike in prices -

-

Global price hike -

Strong seaborne iron ore prices and escalating domestic steel prices form the immediate backdrop to the price hike, it is believed. Spot iron ore price rise to over 6.5 years high on strong demand. Spot iron ore prices continued to rally on strong demand for medium grades. Price of Fe 62% fines was assessed at $130.80/t, CNF China, increased by $2.75 d-o-d. Firm end-user demand for mainstream Australian fines and limited portside inventory continued to support prices. -

Supply tightness in Odisha -

The persistent supply imbalance in Odisha due to 14 of the 19 newly auctioned mines failing to start operations has resulted in production loss of around 4 mn t per month. The supply squeeze in Odisha, which contributes over 50% of the country’s annual iron ore output, is evident. Total production from 5 auctioned mines (4 mines of JSW and 1 mine of AMNS) was at 1.5 mn t during Apr-Jul’20 against target production of 17.4 mn t pa -

Recent OMC’s auction fetched hike in bids -

Orissa Mining Corporation’s auctions of 492,000 t iron ore held on 3rd Sep’20, as reported by SteelMint, received a surprisingly high premium of INR 800-2,050/t over the base price . -

Fall in NMDC’s iron ore output amid monsoons -

NMDC recorded iron ore production of 1.62 mn t in Aug’20, down 26% on a monthly basis compared to 2.19 mn t in July’20. However, on a yearly basis sales increased 15% compared to 1.41 mn t in Aug’19. Sources highlighted that heavy rains resulted in lower iron ore production. -

Hike in Indian steel prices -

Indian steel manufacturers have increased domestic HRC prices by INR 2,000/t ($27) for Sept’20 deliveries. Prices have moved up on the back of supply concerns due to maintenance shutdowns and hike in global steel prices.

7 Likes

Risks and Concerns from NMDC Annual Report 2019-20

Introduction of Auction rule has increased risks for NMDC as its major customers have acquired captive mines in mineral-rich states, mainly JSW & AM-NS. With recent auction in before expiry of iron ore lease before March 2020, few more steel players have acquired mines causing a reduction in demand from merchant players. JSW has already started production from newly acquired mines & planned to increase it further in the near future. Arcelor Mittal-Nippon Steel, India is also looking to start its mines in Odisha by Oct-Dec’2020. More auctions of iron ore mines are likely to come up in the near future for the end-users. This is likely to adversely impact the market for NMDC over the medium to long term.

1 Like

Does this mean that company can export?

“Today, the Cabinet decided to offer on lease 600 hectares at Donimalai located at Sandur Taluk in Ballari district, provided the company clears the royalty dues of around ₹500 crore, and a new lease amount of ₹670 crore is to be paid over a year,” he added

Even though NMDC has positive global cues with increase in iron ore price, they are in a mess with royalty stuff and also Nagarnar steel plant which is very difficult to get privatized and needs around 4K Crore additional capex to operationalize. The state governments are now in a hunt to get more revenue as there is significant shortfall in GST collections and push hard on royalty. With regulations on the iron-ore export, it also cannot fully make use of existing demand situation outside.

Disclosure - Invested. Planning to reduce position size.

Notes on NMDC_AR2020.docx (247.8 KB)

NMDC is depositing money to monitoring committee from its sale from Donimalai mines from last several years. Though they made provision against the same following expected credit loss model. But do any one aware what it is the issue and why monitoring committee has kept this money (About Rs 2400 Cr)

Common Cause Judgement for Bailadila Sector: The Company had received Show Cause Notices dated 31 .07.2018 from Dist. Collector, South Bastar Dantewada as to why NMDC should not be asked to deposit an amount of Rs. 7,241.35 crore as compensation as calculated by Collector based on the Hon’ble Supreme Court Common Cause Judgement related to Orissa Iron ore mines ( Writ Petition Civil No 114 of 2014 dated 2nd August 2017). The Company had been contesting the Show Cause Notices with Dist. Collector, South Bastar Dantewada on the ground that the said judgement is not applicable to NMDC . Meanwhile, revised showcause notices dated 26.09.2019 were received for a revised amount of Rs 1,623.44 Crore from Dist. Collector, South Bastar, Dantewada, to be replied within 21 days of notice. NMDC while reiterating the fact of non-applicability of the Hon’ble Supreme Court Judgement in the state of Chhattisgarh, has sought time for replying to the show cause notices. Further to above, Dist. Collector, South Bastar, Dantewada had issued Demand notices dated 15/11 /2019 for the amount to Rs 1,623.44 Crore towards EC Capacity violation and proposed production violation as per approved Mining Plan / Scheme respectively (Bacheli - Rs 1,131.97 Crore & Kirandul Rs 491.47 Crore) asking to deposit the amount within 15 days.

As the Mining Leases of the company in the State of Chhattisgarh were expiring on 31 .3.2020 and due for renewal, the Company has paid an adhoc amount of Rs 600 Crore under protest and filed writ petitions in the Hon’ble High Court of Bilaspur, Chhattisgarh and a Revision application with Mines Tribunal, Ministry of mines, Government of India , New Delhi praying to set aside the demand notices. Hon’ble High Court of Bilaspur has heard the WPs on 19.02.2020 and sought certain clarifications from the respondent and directed ‘no coercive action till 12.3.2020 and listed the case for 12.3.2020. However due to COVID-19 situation, no further hearings could take place The demand amount of Rs 1,623.44 crores has been shown under ‘Contingent Liabilities’.

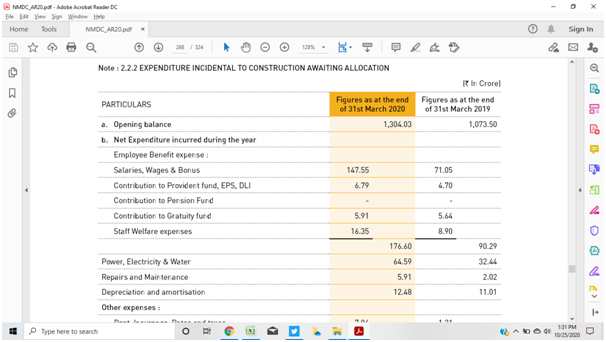

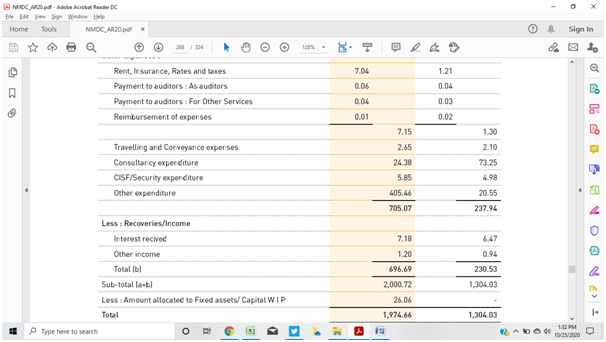

Capital Work in Progress (Mainly Steel Plant)

Rs 15500 cr are lying in CWIP, out of which about 2000 cr are preoperative expenses likes of salary, power etc. Following is extract from its FY2019-20 annual report

Other expense include something about 400 cr, no further information.

4 Likes

This is govt owned company highly profitable contributing heavily to GOI informs of Dividend, Taxes, Royalty and generously contributing in CSR activities. But seems like respective district collector, state government are making too many disruptions to its activities. Ultimately it is the loss to exchequers.

3 Likes

Hi Ayush, How do u see this news now ?

https://steelguru.com/steel/ccea-approves-demerger-of-nagarnar-steel-plant-from-nmdc/564265

Seems like markets are still sceptical about this happening ? are the odds against it ?

1 Like

NMDC also has an earmarked iron ore mine for this steel plant. Along with the mine, this steel plant would be very attractive to private steel companies. In worst case, Government might ask SAIL or RINL to take this over and can pocket the cash from NMDC as dividend. In any case, iron ore prices have increased by 40% in last 3-4months and NMDC should report good profits.

As per the latest media articles, the plant will be demerged with mirroring of NMDC shareholding then the govt stake (around 69.6% as per current shareholding) in the demerged entity (plant) will be put on sale

The floor price is cost of building the plant. Need to compare with existing company valuations vs replacement cost to see if it attracts any private player.

.

1 Like

Hi Amit, I think this will be a great development if they can actually sell off the steel plant event at some discount. PSU stocks have been really out of flavour and have been falling in recent times but things like these can be big positive triggers.

Regards,

Ayush

Disc: not invested. Had invested earlier but exited when there were issues around premium to be charged recently

2 Likes

Hi Ayush,

Royalty used to be around 17% of sales -

Lets say not only Donimalai but all of them increased by 20%, it will be = Rs 2515, Net impact on profits will be -

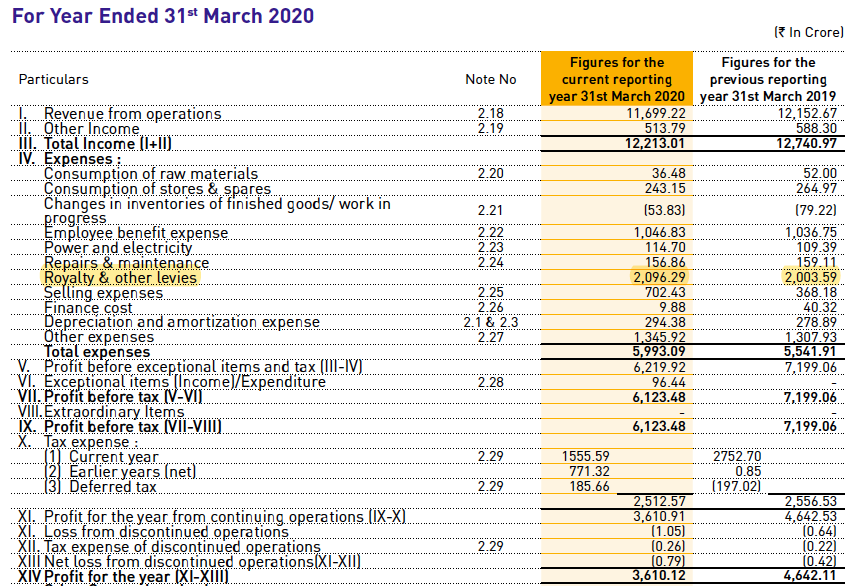

Profit before tax = 5704 Vs 6123 ( -6.8%).

Its an very high margin company, when ore prices are low they make 30-40% when ore prices are at peak they make 60% margin. Donimalai has very high grade iron ore and there was not royalty hike for years , i think inflation adjusted this hike is not much even retrospectively.

I can’t think of any other rational reason why these kind of PSU stocks should trade this cheap.